Fiscal Period Business Report Th (Statement of Financial Performance) 14 June 1, 2012 ~ November 30, 2012

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

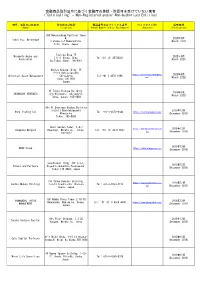

金融商品取引法令に基づく金融庁の登録・許認可を受けていない業者 ("Cold Calling" - Non-Registered And/Or Non-Authorized Entities)

金融商品取引法令に基づく金融庁の登録・許認可を受けていない業者 ("Cold Calling" - Non-Registered and/or Non-Authorized Entities) 商号、名称又は氏名等 所在地又は住所 電話番号又はファックス番号 ウェブサイトURL 掲載時期 (Name) (Location) (Phone Number and/or Fax Number) (Website) (Publication) 28F Nakanoshima Festival Tower W. 2020年3月 Tokai Fuji Brokerage 3 Chome-2-4 Nakanoshima. (March 2020) Kita. Osaka. Japan Toshida Bldg 7F Miyamoto Asuka and 2020年3月 1-6-11 Ginza, Chuo- Tel:+81 (3) 45720321 Associates (March 2021) ku,Tokyo,Japan. 104-0061 Hibiya Kokusai Bldg, 7F 2-2-3 Uchisaiwaicho https://universalassetmgmt.c 2020年3月 Universal Asset Management Chiyoda-ku Tel:+81 3 4578 1998 om/ (March 2022) Tokyo 100-0011 Japan 9F Tokyu Yotsuya Building, 2020年3月 SHINBASHI VENTURES 6-6 Kojimachi, Chiyoda-ku (March 2023) Tokyo, Japan, 102-0083 9th Fl Onarimon Odakyu Building 3-23-11 Nishishinbashi 2019年12月 Rock Trading Inc Tel: +81-3-4579-0344 https://rocktradinginc.com/ Minato-ku (December 2019) Tokyo, 105-0003 Izumi Garden Tower, 1-6-1 https://thompsonmergers.co 2019年12月 Thompson Mergers Roppongi, Minato-ku, Tokyo, Tel: +81 (3) 4578 0657 m/ (December 2019) 106-6012 2019年12月 SBAV Group https://www.sbavgroup.com (December 2019) Sunshine60 Bldg. 42F 3-1-1, 2019年12月 Hikaro and Partners Higashi-ikebukuro Toshima-ku, (December 2019) Tokyo 170-6042, Japan 31F Osaka Kokusai Building, https://www.smhpartners.co 2019年12月 Sendai Mubuki Holdings 2-3-13 Azuchi-cho, Chuo-ku, Tel: +81-6-4560-4410 m/ (December 2019) Osaka, Japan. 16F Namba Parks Tower 2-10-70 YAMANASHI KYOTO 2019年12月 Nanbanaka, Naniwa-ku, Osaka, Tel: +81 (0) 6-4560-4440 https://www.ykmglobal.com/ MANAGEMENT (December 2019) Japan 8th Floor Shidome, 1.2.20 2019年12月 Tenshi Venture Capital Kaigan, Minatu-ku, Tokyo (December 2019) 6flr Nishi Bldg. -

Yamato Valve Delivery Record

YAMATO VALVE DELIVERY RECORD Since 1919 Region map : Index Hokkaido 山路を登りながら Tohoku Tokai Chugoku Tokyo Kanto Kyusyu Kansai Okinawa 05 Kanto 11 Kansai 07 Hokkaido 13 Chugoku 08 Tohoku 13 Kyusyu 11 Tokai 13 Okinawa 1 2 Tokyo Tokyo Skytree Tokyo Soramachi National Museum of Roppongi Hills Nature and Science Mori Tower TOHO Cinemas Shinjuku Kabukiza Theatre 1 2 Tokyo Tokyo Metropolitan Shibuya Stream Police Department Prime Minister's Offi cial Residence fi rst members' offi ce building Tokyo Metropolitan of the house of representatives Government Building 3 4 Tokyo National Museum of Western Art Ōta Incineration Plant Supreme Court of Japan Ministry of Defense Tokyo Baycourt Club Hotel & Spa Resort 3 4 Kanto region Yokota Air Base Atsugi Air Base the prime minister's offi cial residence Fleet Activities Yokosuka Central Joint Government Building National Defense Academy of Japan Supreme Court of Japan National Defense Medical College Tokyo High Court JGSDF, Camp Tachikawa Ministry of Foreign AffairsJoint Government JGSDF Camp Ōmiya Building JGSDF Camp Asaka Saitama-shintoshin Joint Government JMSDF Yokosuka Naval Base Building No.1, No.2 National Cancer Center Hospital Central Gov't Bldg. No.1 Sagamihara National Hospital Central Gov't Bldg. No.3 Ministry of Finance Main building Central Gov't Bldg. No.5 National Tax Agency Central Gov't Bldg. No.6 JAPAN Patent Offi ce building Central Gov't Bldg. No.2 Ryutsu Keizai University National Sakura History and Folklore Yokohama City University Museum Keio University Japan Meteorological Agency -

Register of Medical Institutions Issuing COVID-19 Testing

Register of Medical Institutions Issuing COVID-19 Testing Certificates as of September 20th, 2021 【About Antigen test kit (qualitative antigen test)】 ・In Japan, PCR Test including LAMP Method and Quantitative Antigen Test are permitted for asymptomatic patient as appropriate test method, but Antigen test kit (qualitative antigen test) are not permitted. ・At the request of the destination, Antigen test kit (qualitative antigen test) is used for asymptomatic patient, and if the test result is positive, PCR Test or other appropriate test method may be performed based on doctor's judgement. ※Permitted test method in Japan are highlighted in light blue at the table below. ※Reference: Guidelines for COVID-19 Pathogen Test Basic Information of Medical Institution Inspection Information Contact Address Testing Methods for Issuing a Certificate Information TeCOT PCR Testing PCR Testing Antigen Testing Antigen Testing No Reservation LAMP Method Other Methods Real-Time Method Non-Real-Time Method Simple Kit Quantitative Availability Medical Institution Name Phone Prefecture Municipality Street Address Nasopharynx Saliva Nasopharynx Saliva Nasopharynx Saliva Nasopharynx Saliva Nasopharynx Saliva Nasopharynx Saliva Number Min. Req. Min. Req. Min. Req. Min. Req. Min. Req. Min. Req. Min. Req. Min. Req. Min. Req. Min. Req. Min. Req. Min. Req. Availability Availability Availability Availability Availability Availability Availability Availability Availability Availability Availability Availability Time Time Time Time Time Time Time Time Time Time Time Time -

MARKET TREND SURVEY of LARGE-SCALE OFFICE BUILDINGS in TOKYO's 23 WARDS (“Ku”)

May 10, 2006 MARKET TREND SURVEY of LARGE-SCALE OFFICE BUILDINGS IN TOKYO’S 23 WARDS (“ku”) (As of December 2005) Supply of extremely large-scale office buildings (buildings with total office floor space of over 30,000 m2) will be concentrated in the three central wards. With more office consolidation, the office environment in the Tokyo Central Business District (CBD) is expected to be further invigorated. Office space demand remains steady, especially in the three central wards. With continuing business expansion, the number of office employees will increase further. What users expect of the office environment: ٤Views of general affairs departments and facility management staff are different from that of office workers; The ideal office environment for the future on the basis of what office workers expect of ٤ offices. Since 1986, Mori Building Company Ltd. (Headquarters: Minato-ku, Tokyo; President and CEO: Minoru Mori) has been regularly conducting surveys of demand and supply trends of large office buildings with total office floor space of over 10,000 m2 (in this survey, they will be referred to as “large-scale office buildings”) throughout Tokyo’s 23 wards. Forecasts of future trends in the office market are also carried out by analyzing the results of this survey from a variety of angles. The results of the survey as of December 2005 are contained in this report. Outline of Market Trend Survey ع Survey date: December end, 2005 Coverage: Tokyo’s 23 wards (“ku”) Type of property: Large office buildings with total office floor space of over 10,000 m2 (built after 1986) (Notes on the contents) ̪ This survey is not only based on publicly available information, but also shows the results of the compilation of on-site observations and direct interviews with developers on the progress and other conditions of each project. -

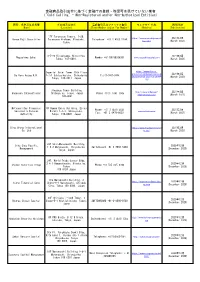

金融商品取引法令に基づく金融庁の登録・許認可を受けていない業者 ("Cold Calling" - Non-Registered And/Or Non-Authorized Entities)

金融商品取引法令に基づく金融庁の登録・許認可を受けていない業者 ("Cold Calling" - Non-Registered and/or Non-Authorized Entities) 商号、名称又は氏名等 所在地又は住所 電話番号又はファックス番号 ウェブサイトURL 掲載時期 (Name) (Location) (Phone Number and/or Fax Number) (Website) (Publication) Marunouchi Kitaguchi Bldg. http://japaninternational 2018年8月 Japan International Commodities 1-6-5, Marunouchi, Chiyoda-ku, commodities.com/ (August 2018) Tokyo, ZIP 100-8262 Resona Dai-Ichi Group/Resona Head Office: 32F, Toranomon Hills, 1-23- https://www.rdgfinancial. 2018年8月 Tel: +81 3 4540 6704 Day-Ichi Group 4, Toranomon, Minato-ku, Tokyo com/ (August 2018) Izumi Garden Tower, 1 Chome-6-1 https://taylormckenzie.ne 2018年8月 Taylor mckenzie Roppongi, Minato-ku, Tokyo, ZIP 106- Tel: +81 3 4579 5691 t/ (August 2018) 0032 48F Shinbashi Tokyu Bldg 4-21-3, http://www.fsajp.com/delw 2018年8月 Delwebb Limited Shinbashi Minato-ku, Tokyo, ZIP 105- Tel: +81 345 405 931 ebb-limited/ (August 2018) 0004 22F Hibiya Kokusai Building, 2018年8月 Kangyo Yokohama Securities 2-2-3 Uchisaiwai-cho, Chiyoda-ku, Tel: +81 3 4579 0434 https://www.kysecurities.com (August 2018) Tokyo 4FL Yusen Building http://phoenixdirectmanagem 2018年8月 Phoenix Direct Management 2-3-2 Marunouchi, Chiyoda-ku Tel: +81 3 4578 7985 ent.com/ (August 2018) Tokyo, ZIP 100-0005 Grace Investment/ Grace Tokyo Shinjuku Park Tower, 29/F, 2018年8月 Investment L.L.C Nishishinjuku 3-7-1, 163-1055 Tokyo (August 2018) IBG Capital Partners Gran Tokyo North Tower, 1-208-5 Yaesu, 2018年8月 Chiyoda-ku, Tokyo (August 2018) 13F Harumi Island Triton Square 2018年8月 Shinhan Daiwa Brokerage Office -

2017 EBC WP-E W Cover and Advertisement.Pdf

First Milestone Achieved The EBC Report on the Japanese Business Environment 2017 The European Business Council in Japan The European (EU) Chamber of Commerce in Japan European Business Council in Japan European (EU) Chamber of Commerce in Japan The EBC is the trade policy arm of the following European national chambers of commerce and business organisations in Japan: Austrian Business Council Belgium-Luxembourg Chamber of Commerce in Japan British Chamber of Commerce in Japan Czech Chamber of Commerce and Industry in Japan Danish Chamber of Commerce in Japan Finnish Chamber of Commerce in Japan French Chamber of Commerce and Industry in Japan German Chamber of Commerce and Industry in Japan Greek Chamber of Commerce in Japan Icelandic Chamber of Commerce in Japan Ireland Japan Chamber of Commerce Italian Chamber of Commerce in Japan Netherlands Chamber of Commerce in Japan Norwegian Chamber of Commerce in Japan Polish Chamber of Commerce & Industry in Japan Spanish Institute of Foreign Trade Swedish Chamber of Commerce and Industry in Japan Swiss Chamber of Commerce and Industry in Japan Executive Operating Board Chairman: Danny Risberg First Vice-Chairman: Michael A. Loefflad Vice-Chairman: Carl-Gustav Eklund Treasurer: Erik Ullner Executive Operating Board: Michael A. Loefflad (Austria) Els Verhulst (Belgium/Luxembourg) Florian Kohlbacher (Britain) Claus Eilersen (Denmark) Erik Ullner (Finland) Guy Bonaud (France) Marcus Schuermann (Germany) Athanasios Fragkis (Greece) Lorcan Brophy (Ireland) Francesco Tiberio (Italy) Karsten Vijge (Netherlands) Rune Nordgaard (Norway) Pawel Komender (Poland) Takeshi Fujiwara (Sweden) Masao (Mark) Torii (Switzerland) Executive Director: Alison Murray Policy Director: Bjorn Kongstad Communications Manager: Yoko Hijikuro First Milestone Achieved About the EBC: The EBC Report on the Japanese Business Environment The European Business Council (EBC) is the trade 2017 policy arm of the 18 European national chambers of commerce and business associations in Japan. -

Nuclear Energy Buyers Guide in Japan 2016-17 Introduction

Nuclear Energy Buyers Guide in Japan 2016-17 Introduction CC OO NN TT EE NN TT SS Nuclear Power Nuclear Vendors Nuclear Fuel 01 Hitachi, Ltd. 4 01 Mitsubishi Nuclear Fuel Co., Ltd. 52 Energy choice for a sustainable world 02 Hitachi-GE Nuclear Energy, Ltd. 5 02 Nippon Nuclear Fuel Development Co., Ltd. 53 03 Mitsubishi Electric Corporation 6 03 Nuclear Fuel Industries, Ltd. 54 04 Mitsubishi Heavy Industries, Ltd. 7 05 Toshiba Corporation 8 Transportation Manufacturing 01 Kamigumi Co., Ltd. (Heavy Cargo & Energy Transportation HQ) 58 02 Nuclear Fuel Transport Co., Ltd. 59 01 ABB 12 02 Advanced Fusion Technology, Co., Ltd. 13 Chemical & Water Treatment 03 Chiyoda Technol Corporation 14 04 Dainichi Machine and Engineering Co., Ltd. 15 ® 01 Kurion , Inc. 62 05 Dainippon Plastics Co., Ltd. 16 02 Organo Corporation 63 06 Fuji Electric Co., Ltd. 17 03 Tomiyama Pure Chemical Industries, Ltd. 64 07 Fujikin® Carp® Group 18 08 Hirata Valve Industry Co., Ltd. 19 09 Hitachi, Ltd. 20 Emergency Management 10 Hitachi Zosen Corporation 21 01 Nohmi Bosai Ltd. 68 11 IHI Corporation 22 02 Teikoku Sen-i Co., Ltd. 69 12 Kimura Chemical Plants Co., Ltd. 23 03 Tokyo Bosai Setsubi Co., Ltd. 70 13 Konecranes Nuclear Equipment & Service, Llc 24 14 Okano Valve MFG. Co. Ltd. 25 Services 15 Toa Valve Engineering Inc. 26 16 Yokogawa Electric Corporation 27 01 Association for Nuclear Technology in Medicine 74 02 Computer Simulation & Analysis Japan 75 Steel, Metal & Materials 03 Japan Environment Research Co., Ltd. 76 04 The Japan Power Engineering and Inspection Corporation 77 01 Chouetsu-glass Kaken Co., Ltd. -

The Fourth Arrow

TThhee FFoouurrtthh AArrrrooww TThhee EEBBCC RReeppoorrtt oonn tthhee JJaappaanneessee BBuussiiinneessss EEnnvviiirroonnmmeenntt 22001133 The European Business Council in Japan The European (EU) Chamber of Commerce in Japan The Fourth Arrow The EBC Report on the Japanese Business Environment 2013 The European Business Council in Japan The European (EU) Chamber of Commerce in Japan European Business Council in Japan European (EU) Chamber of Commerce in Japan The EBC is the trade policy arm of the following European national chambers of commerce and business organisations in Japan: Austrian Business Council Belgium-Luxembourg Chamber of Commerce in Japan British Chamber of Commerce in Japan Danish Chamber of Commerce in Japan Finnish Chamber of Commerce in Japan French Chamber of Commerce and Industry in Japan German Chamber of Commerce and Industry in Japan Hellenic Foreign Trade Board Icelandic Chamber of Commerce in Japan Ireland Japan Chamber of Commerce Italian Chamber of Commerce in Japan Netherlands Chamber of Commerce in Japan Norwegian Chamber of Commerce in Japan Polish Chamber of Commerce & Industry in Japan Spanish Institute of Foreign Trade Swedish Chamber of Commerce and Industry in Japan Swiss Chamber of Commerce and Industry in Japan Executive Operating Board Chairman: Duco B. Delgorge Senior Vice-Chairman: Michel Theoval Vice-Chairman: Danny Risberg Executive Operating Board: Michael A. Loefflad (Austria) Bernard de le Court (Belgium/Luxembourg) Richard Thornley (Britain) Claus Eilersen (Denmark) Erik Ullner (Finland) Albert X. Kirchmann (Germany) Gerard Mulligan (Ireland) Paolo Mattioli (Italy) Hiroshi Ishiwata (Netherlands) Rune Nordgaard (Norway) Takeshi Fujiwara (Sweden) Andreas Bernhard (Switzerland) Executive Director: Alison Murray Policy Director: Bjorn Kongstad Communications Manager: Yoko Hijikuro Communications & P.R. -

MARKET TREND SURVEY of LARGE-SCALE OFFICE BUILDINGS in TOKYO’S 23 WARDS (December 2006)

May 14, 2007 MARKET TREND SURVEY of LARGE-SCALE OFFICE BUILDINGS IN TOKYO’S 23 WARDS (December 2006) Supply volume in 2007 will remain consistent with past average levels, but is projected to decline considerably in 2008. Office space demand remains strong in the three central wards, as a result of further business expansion and increased hiring of office employees. As a result, the supply/demand gap will tighten in 2008. ⇒ Tokyo’s office market continues to be sound in the short term. ~Mid- and long-term perspective of the Tokyo office market~ ○ Concerns over Tokyo’s possible declining competitiveness in the global context. ○ Tokyo must enhance its attractiveness as a business and financial center. Since 1986, Mori Building Company Ltd. (Headquarters: Minato-ku, Tokyo; President and CEO: Minoru Mori) has regularly conducted surveys of demand and supply trends of large office buildings with total office floor area of over 10,000 sq.m. (in this survey, they will be referred to as “large-scale office build- ings”) throughout Tokyo’s 23 wards. Forecasts of future trends in the office market are also carried out by analyzing the results of this survey from a variety of angles. This report present the results of the survey as of the end of December 2006. ■ Outline of Market Trend Survey Survey date: End-December, 2006 Coverage: Tokyo’s 23 wards Type of property: Large office buildings with total office floor area of over 10,000 sq.m. built after 1986. <Notes on the contents> ※ This survey is based on publicly available information, the results of the compilation of on-site observations and direct interviews with developers on the progress and other conditions of each project. -

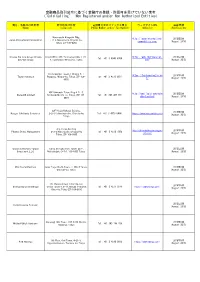

金融商品取引法令に基づく金融庁の登録・許認可を受けていない業者 ("Cold Calling" - Non-Registered And/Or Non-Authorized Entities)

金融商品取引法令に基づく金融庁の登録・許認可を受けていない業者 ("Cold Calling" - Non-Registered and/or Non-Authorized Entities) 商号、名称又は氏名等 所在地又は住所 電話番号又はファックス番号 ウェブサイトURL 掲載時期 (Name) (Location) (Phone Number and/or Fax Number) (Website) (Publication) 17F Toranomon Towers, 1-28, https://www.gunmafujisecurit 2021年3月 Gunma Fuji Securities Toranomon 4-chome, Minatoku, Telephone: +81 3 4565 5204 ies.com/ (March 2021) Tokyo 3-5-20 Kitaaoyama, Minato-ku, 2021年3月 Nagashima Sakai Number +81(50)58936981 www.nagashimasakai.com Tokyo, 107-0061. (March 2021) Imperial Hotel Tower 15th Floor https://www.devere- group.com/globalpresence/gl 2021年3月 De Vere Acuma K.K. 1-1-1 Uchisaiwaicho, Chiyoda-ku Tel: 03-3507-5684 obalpresence.aspx?officePK= (March 2021) Tokyo, 100-0011 Japan 118 Jingumae Tower Building http://www.andersen- 2021年3月 Andersen International Shibuya-ku, Tokyo, Japan Phone (813) 6741 7585 international.com/ (March 2021) 105-0001 Metropolitan Financial 8F Humax Ebisu Building, Ebisu Phone: +81 3 4579-5647 2021年3月 Services & Futures Minami 1-1-1, Shibuya-ku, www.mfinsfa.com Fax: +81 3 6478-8029 (March 2021) Authority Tokyo, 150-0022 Japan Ding Sheng International https://www.heydayint.com/z 2021年3月 Co. Ltd h-cn/ (March 2021) 23F Shin-Marunouchi Building, Oita Chuo Pacific 2020年12月 1-6-2 Marunouchi, Chiyoda-ku, Switchboard +81 3 6863 5404 Management (December 2020) Tokyo, Japan 24F, World Trade Center Bldg. 2-4-1 Hamamatsucho, Minato-ku, 2020年12月 Chinen Securties Group Phone +81 505 865 9240 Tokyo (December 2020) 105-6124 Japan The Marunouchi Building, 2 https://www.stonefinancialco 2020年12月 Stone Financial Corp Chome-4-1 Marunouchi, Chiyoda rp.com (December 2020) City, Tokyo 100-6390, Japan 38F Shinjuku i-Land Tower, 6 2020年12月 Okuras Global Capital Chome-5-1 Nishishinjuku, Tokyo, SWITCHBOARD +81-3-4590-0730 (December 2020) Japan 8F PMO Ginza, 8-12-8 Ginza, http://www.hshmanagement.c 2020年12月 Hokkaido Security Holdings Switchboard +81 3 4578 1355 Chuo-ku, Tokyo, Japan om (December 2020) 5th Fl. -

Swiss World in Japan

2021 SWISS WORLD IN JAPAN Japan External Trade Organization 1 MAJOR REGIONS OF JAPAN 2 DIRECTORY OF SWISS COMPANIES IN JAPAN BUSINESS SERVICES Adeco Group Ltd. BOARD Japan Inc. Kasumigaseki Tokyo Bldg., 3-7-1 Marunouchi Kitaguchi Bldg., 9Fl., Kasumigaseki, Chiyoda-ku 1-6-5 Marunouchi, Chiyoda-ku, Tokyo 100-0013 Tokyo 100-0005 Phone: +81 (0)50 2000 7044 Phone: +81 (0)3 6478 2070 www.adecco.co.jp [email protected] www.linkedin.com/company/adecco www.board.com / www.linkedin.com/company/ board/ Adecco Group Ltd. Grand Front Osaka Tower A, 14Fl., Chain IQ Japan K.K. 4-20 Ofuka-cho, Kita-ku, Tokyo Shinmarunouchi Center Bldg., Osaka 530-0011 20FL., Phone: +81 (0)6 7733 0733 1-6-2 Marunouchi, Chiyoda-ku, www.adecco.co.jp Tokyo 100-0001 www.linkedin.com/company/adecco www.chainiq.com / www.linkedin.com/company/ chain-iq/ ACROSEC Inc. Sensan Bldg., 5Fl., CH Projects Management Ltd. 2-1-5 Tsunashima Nishi Yokohama, Hirakawa-cho Bldg., 7Fl., 2- Kohoku-ku, Kanagawa 223-0052 6-1 Hirakawa-cho Phone: +81 (0)45 716 9905 Chiyoda-ku, Tokyo 102-0093 www.acrosec.jp/ Phone: +81 (0)3 3288 3255 Fax: +81 (0)3 3288 3284 [email protected] www.chpm.co.jp 3 Cream-Digital Creative Studio Euro Far East K.K. Liberty Shin- 3-6-18 Shibuya, Shibuya-ku, Yokohama Bldg., 8Fl., Tokyo 150-0002 3-17-15 Shin-Yokohama, Phone: + 81 (0)3 6303 2553 Kohoku-ku, Yokohama 222-0033 [email protected] Phone: +81 (0)45 620 2013 www.cream-touch.com [email protected] www.linkedin.com/company/cre www.euro-fareast.co.jp am-digital-studio/ Genedata K.K. -

Ready for a New Partnership the EBC Report on the Japanese Business Environment 2018

Ready For A New Partnership The EBC Report on the Japanese Business Environment 2018 The European Business Council in Japan The European (EU) Chamber of Commerce in Japan European Business Council in Japan European (EU) Chamber of Commerce in Japan The EBC is the trade policy arm of the following European national chambers of commerce and business organisations in Japan: Austrian Business Council Belgium-Luxembourg Chamber of Commerce in Japan British Chamber of Commerce in Japan Czech Chamber of Commerce and Industry in Japan Danish Chamber of Commerce in Japan Finnish Chamber of Commerce in Japan French Chamber of Commerce and Industry in Japan German Chamber of Commerce and Industry in Japan Greek Chamber of Commerce in Japan Icelandic Chamber of Commerce in Japan Ireland Japan Chamber of Commerce Italian Chamber of Commerce in Japan Netherlands Chamber of Commerce in Japan Polish Chamber of Commerce & Industry in Japan Spanish Chamber of Commerce in Japan Swedish Chamber of Commerce and Industry in Japan Swiss Chamber of Commerce and Industry in Japan Executive Operating Board Acting Chairman: Michael A. Loefflad First Vice-Chairman: Michael A. Loefflad Vice-Chairman: Carl-Gustav Eklund Treasurer: Erik Ullner Members: Michael A. Loefflad (Austria) Gregory Van Bellinghen (Belgium/Luxembourg) Florian Kohlbacher (Britain) Claus Eilersen (Denmark) Erik Ullner (Finland) Guy Bonaud (France) Marcus Schuermann (Germany) Athanasios Fragkis (Greece) Lorcan Brophy (Ireland) Marco Zoli (Italy) Kiminobu Yoshida (Netherlands) Pawel Komender (Poland) Takeshi Fujiwara (Sweden) Masao (Mark) Torii (Switzerland) Executive Director: Francesco Formiconi Policy Director: Bjorn Kongstad Communications Manager: Yoko Hijikuro About the EBC: Ready For A New Partnership The European Business Council (EBC) is the trade policy arm of the 17 European national chambers of The EBC Report on the Japanese Business Environment commerce and business associations in Japan.