HCL Connections with Office Profile Integration

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

DXE Liquidity Provider Registered Firms

DXE Liquidity Provider Program Registered Securities European Equities TheCboe following Europe Limited list of symbols specifies which firms are registered to supply liquidity for each symbol in 2021-09-28: 1COVd - Covestro AG Citadel Securities GCS (Ireland) Limited (Program Three) DRW Europe B.V. (Program Three) HRTEU Limited (Program Two) Jane Street Financial Limited (Program Three) Jump Trading Europe B.V. (Program Three) Qube Master Fund Limited (Program One) Societe Generale SA (Program Three) 1U1d - 1&1 AG Citadel Securities GCS (Ireland) Limited (Program Three) HRTEU Limited (Program Two) Jane Street Financial Limited (Program Three) 2GBd - 2G Energy AG Citadel Securities GCS (Ireland) Limited (Program Three) Jane Street Financial Limited (Program Three) 3BALm - WisdomTree EURO STOXX Banks 3x Daily Leveraged HRTEU Limited (Program One) 3DELm - WisdomTree DAX 30 3x Daily Leveraged HRTEU Limited (Program One) 3ITLm - WisdomTree FTSE MIB 3x Daily Leveraged HRTEU Limited (Program One) 3ITSm - WisdomTree FTSE MIB 3x Daily Short HRTEU Limited (Program One) 8TRAd - Traton SE Jane Street Financial Limited (Program Three) 8TRAs - Traton SE Jane Street Financial Limited (Program Three) Cboe Europe Limited is a Recognised Investment Exchange regulated by the Financial Conduct Authority. Cboe Europe Limited is an indirect wholly-owned subsidiary of Cboe Global Markets, Inc. and is a company registered in England and Wales with Company Number 6547680 and registered office at 11 Monument Street, London EC3R 8AF. This document has been established for information purposes only. The data contained herein is believed to be reliable but is not guaranteed. None of the information concerning the services or products described in this document constitutes advice or a recommendation of any product or service. -

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

Corporate Non-Financial Reporting in Germany

Copyright © Development International e.V., 2019 ISBN: 978-3-9820398-1-7 Authors: Chris N. Bayer, PhD Gisella Vogel Sarah Kaltenhäuser Katherine Storrs Jiahua (Java) Xu, PhD Juan Ignacio Ibañez, LL.M. Title: A New Responsibility for Sustainability: Corporate Non-Financial Reporting in Germany Date published: May 6, 2019 Funded by: iPoint-systems gmbh www.ipoint-systems.com Executive Summary Germany's economy is the fourth-largest in the world (by nominal GDP), and with 28% of the euro area market, it represents the largest economy in Europe.1 Considering the supply chains leading to its economy, Germany's cumulative environmental, social and governance performance reverberates globally. The EU Non-Financial Reporting Directive (NFRD) is the impetus behind this study – a new regulation that seeks to “increase the relevance, consistency and comparability of information disclosed by certain large undertakings and groups across the Union.”2 Large undertakings in EU member states are not only required to report on their financial basics, now they are also required by Article 1 of the Directive to account for their non- financial footprint, including adverse impacts they have on the environment and supply chains. In accordance with the Directive, the German transposition stipulates that the non-financial declaration must state which reporting framework was used to create it (or explain why no framework was applied), as well as apply non-financial key performance indicators relevant to the particular business. These requirements are our point of departure: We systematically assess the degree of non-financial transparency and performance reporting for 2017 applying an ex-post assessment framework premised on the Global Reporting Initiative (GRI), the German Sustainability Code (Deutscher Nachhaltigkeitskodex, DNK) and the United Nations Global Compact (UNGC). -

HCL Software's

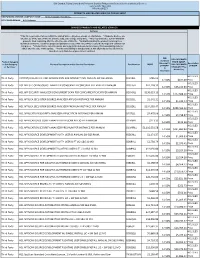

IBM Branded, Fujistu Branded and Panasonic Branded Products and Related Services and Cloud Services Contract DIR-TSO-3999 PRICING SHEET PRODUCTS AND RELATED SERVICES PRICING SHEET RESPONDING VENDOR COMPANY NAME:____Sirius Computer Solutions_______________ PROPOSED BRAND:__HCL Software__________________________ BRANDED PRODUCTS AND RELATED SERVICES Software * This file is generated for use within the United States. All prices shown are US Dollars. * Products & prices are effective as of the date of this file and are subject to change at any time. * HCL may announce new or withdraw products from marketing after the effective date of this file. * Nothwithstanding the product list and prices identified on this file, customer proposals/quotations issued will reflect HCL's current offerings and commercial list prices. * Product list is not all inclusive and may not include products removed from availability (sale) or added after the date of this update. * Product availability is not guaranteed. Not all products listed below are found on every State/Local government contract. DIR DIR CUSTOMER Customer Product Category PRICE (MSRP- Discount % Description or SubCategory Product Description and/or Service Description Part Number MSRP DIR CUSTOMER off MSRP* of MSRP or Services* DISCOUNT Plus (2 Admin Fee) Decimals) HCL SLED Third Party CNTENT/COLLAB ACC AND WEBSPH PRTL SVR INTRANET PVU ANNUAL SW S&S RNWL E045KLL $786.02 14.50% $677.09 Price HCL SLED Third Party HCL APP SEC OPEN SOURCE ANALYZER CONSCAN PER CONCURRENT EVENT PER ANNUM D20H6LL $41,118.32 -

Monitoring Enterprise Collaboration Platform Change and the Building of Digital Transformation Capabilities

Monitoring Enterprise Collaboration Platform Change and the Building of Digital Transformation Capabilities: An Information Infrastructure Perspective by Clara Sabine Nitschke Approved Dissertation thesis for the partial fulfilment of the requirements for a Doctor of Economics and Social Sciences (Dr. rer. pol.) Fachbereich 4: Informatik Universität Koblenz-Landau Chair of PhD Board: Prof. Dr. Ralf Lämmel Chair of PhD Commission: Prof. Dr. Viorica Sofronie-Stokkermans Examiner and Supervisor: Prof. Dr. Susan P. Williams Further Examiners: Prof. Dr. Petra Schubert, Prof. Dr. Catherine A. Hardy Date of the doctoral viva: 28/07/2021 Acknowledgements Many thanks to all the people who supported me on my PhD journey, a life-changing experience. This work was funded by two research grants from the Deutsche Forschungsgemeinschaft (DFG). The related projects were designed as a joint work between two research groups at the University Koblenz-Landau. I am especially grateful to my supervisor Prof. Dr. Sue Williams who provided invaluable support throughout my whole project, particularly through her expertise, as well as her research impulses and discussions. Still, she gave me the freedom to shape my research, so many thanks! Further, I would like to thank my co-advisor Prof. Dr. Petra Schubert for very constructive feedback through the years. I am thankful for having had the unique opportunity to be part of the Center for Enterprise Information Research (CEIR) team with excellent researchers and the IndustryConnect initiative, which helped me bridge the gap between academia and ‘real world’ cases. IndustryConnect, founded by Prof. Dr. Schubert and Prof. Dr. Williams, enabled me to participate in long-term practice-oriented research with industry, a privilege that most other doctoral students cannot enjoy. -

Euro Stoxx® Total Market Index

EURO STOXX® TOTAL MARKET INDEX Components1 Company Supersector Country Weight (%) ASML HLDG Technology Netherlands 3.45 LVMH MOET HENNESSY Consumer Products & Services France 2.76 LINDE Chemicals Germany 2.40 SAP Technology Germany 2.38 TOTAL Energy France 1.99 SANOFI Health Care France 1.88 SIEMENS Industrial Goods & Services Germany 1.84 ALLIANZ Insurance Germany 1.74 L'OREAL Consumer Products & Services France 1.55 IBERDROLA Utilities Spain 1.38 SCHNEIDER ELECTRIC Industrial Goods & Services France 1.35 AIR LIQUIDE Chemicals France 1.33 ENEL Utilities Italy 1.32 BASF Chemicals Germany 1.23 ADYEN Industrial Goods & Services Netherlands 1.13 ADIDAS Consumer Products & Services Germany 1.13 AIRBUS Industrial Goods & Services France 1.08 BNP PARIBAS Banks France 1.05 DAIMLER Automobiles & Parts Germany 1.03 ANHEUSER-BUSCH INBEV Food, Beverage & Tobacco Belgium 1.02 DEUTSCHE TELEKOM Telecommunications Germany 1.02 BAYER Health Care Germany 1.00 VINCI Construction & Materials France 0.98 BCO SANTANDER Banks Spain 0.93 Kering Retail France 0.87 AXA Insurance France 0.86 PHILIPS Health Care Netherlands 0.85 SAFRAN Industrial Goods & Services France 0.85 DEUTSCHE POST Industrial Goods & Services Germany 0.84 INFINEON TECHNOLOGIES Technology Germany 0.84 Prosus Technology Netherlands 0.83 ESSILORLUXOTTICA Health Care France 0.80 DANONE Food, Beverage & Tobacco France 0.73 INTESA SANPAOLO Banks Italy 0.73 MUENCHENER RUECK Insurance Germany 0.72 PERNOD RICARD Food, Beverage & Tobacco France 0.66 ING GRP Banks Netherlands 0.64 HERMES INTERNATIONAL -

Investor Release

INVESTOR RELEASE Noida, India, January 15th, 2021 Revenue at US$ 10,022 mn; up 3.6% YoY in US$ and Constant Currency EBITDA margin at 26.5%, (US GAAP); EBITDA margin at 27.4% (Ind AS); EBIT margin at 21.5% Net Income at US$ 1781 mn (Net Income margin at 17.8%) up 19.8% YoY Revenue at ` 74,327 crores; up 9.2% YoY Net Income at ` 13,202 crores; up 26.0% YoY Revenue at US$ 2,617 mn; up 4.4% QoQ & up 2.9% YoY Revenue in Constant Currency; up 3.5% QoQ & up 1.1% YoY EBITDA margin at 28.2%, (US GAAP); EBITDA margin at 29.1% (Ind AS); EBIT margin at 22.9% Net Income at US$ 540 mn (Net Income margin at 20.6%) up 27.3% QoQ & up 26.5% YoY Revenue at ` 19,302 crores; up 3.8% QoQ & up 6.4% YoY Net Income at ` 3,982 crores; up 26.7% QoQ & up 31.1% YoY Revenue expected to grow QoQ between 2% to 3% in constant currency for Q4, FY’21, including DWS contribution. EBIT expected to be between 21.0% and 21.5% for FY’21 Financial Highlights 2 Corporate Overview 4 Performance Trends 5 Financials in US$ 18 Cash and Cash Equivalents, Investments & Borrowings 21 Revenue Analysis at Company Level 22 Constant Currency Reporting 23 Client Metrics 24 Headcount 24 Financials in ` 25 - 1 - (Amount in US $ Million) CALENDAR YEAR QUARTER ENDED PARTICULARS CY’20 Margin YoY 31-Dec-2020 Margin QoQ YoY Revenue 10,022 3.6% 2,617 4.4% 2.9% Revenue Growth 3.6% 3.5% 1.1% (Constant Currency) EBITDA 2,655 26.5% 19.9% 738 28.2% 10.5% 17.7% EBIT 2,155 21.5% 16.5% 599 22.9% 10.6% 16.4% Net Income 1,781 17.8% 19.8% 540 20.6% 27.3% 26.5% (Amount in ` Crores) CALENDAR YEAR QUARTER ENDED -

Introduction to Chemistry

Introduction to Chemistry Author: Tracy Poulsen Digital Proofer Supported by CK-12 Foundation CK-12 Foundation is a non-profit organization with a mission to reduce the cost of textbook Introduction to Chem... materials for the K-12 market both in the U.S. and worldwide. Using an open-content, web-based Authored by Tracy Poulsen collaborative model termed the “FlexBook,” CK-12 intends to pioneer the generation and 8.5" x 11.0" (21.59 x 27.94 cm) distribution of high-quality educational content that will serve both as core text as well as provide Black & White on White paper an adaptive environment for learning. 250 pages ISBN-13: 9781478298601 Copyright © 2010, CK-12 Foundation, www.ck12.org ISBN-10: 147829860X Except as otherwise noted, all CK-12 Content (including CK-12 Curriculum Material) is made Please carefully review your Digital Proof download for formatting, available to Users in accordance with the Creative Commons Attribution/Non-Commercial/Share grammar, and design issues that may need to be corrected. Alike 3.0 Unported (CC-by-NC-SA) License (http://creativecommons.org/licenses/by-nc- sa/3.0/), as amended and updated by Creative Commons from time to time (the “CC License”), We recommend that you review your book three times, with each time focusing on a different aspect. which is incorporated herein by this reference. Specific details can be found at http://about.ck12.org/terms. Check the format, including headers, footers, page 1 numbers, spacing, table of contents, and index. 2 Review any images or graphics and captions if applicable. -

Shifting Socioemotional Wealth Prioritization During a Crisis

Shifting socioemotional wealth prioritization during a crisis A content analysis of statements to shareholders of family businesses MASTER THESIS WITHIN: Business Administration NUMBER OF CREDITS: 30 ECTS PROGRAMME OF STUDY: Global Management AUTHORS: Stella Alice Gisela Heuer & Lajos Szabó TUTOR: Tommaso Minola JÖNKÖPING May 2021 Master Thesis in Business Administration Title: Shifting socioemotional wealth prioritization during a crisis: A content analysis of statements to shareholders of family businesses Authors: Stella Alice Gisela Heuer and Lajos Szabó Tutor: Tommaso Minola Date: 2021-05-24 Key terms: Family business, socioemotional wealth, FIBER, COVID-19, content analysis, Sweden, Germany Abstract Family businesses are generally considered to be the most prevalent form of business around the world. They have also been shown to differ from their non-family counterparts due the non- economic factors that influence their decision-making. One of the most widely used conceptualization of these factors concerns the controlling family’s socioemotional endowment or in other words, the family’s socioemotional wealth. Newer approaches have proposed that socioemotional wealth can not only be broken down into several component dimensions, but that these dimensions may shift in prioritization in response to different contingencies. The sudden spread of the COVID-19 pandemic and the global crisis that has followed in its wake is one such contingency, impacting economies and family firms virtually everywhere in the world. Studying the crisis’ effects on family firms has thus already been outlined as a major focus of research going forward. This paper aims to develop the concept of socioemotional wealth as a dynamic construct and study the crisis’ effects on family firms. -

PLUMBING DICTIONARY Sixth Edition

as to produce smooth threads. 2. An oil or oily preparation used as a cutting fluid espe cially a water-soluble oil (such as a mineral oil containing- a fatty oil) Cut Grooving (cut groov-ing) the process of machining away material, providing a groove into a pipe to allow for a mechani cal coupling to be installed.This process was invented by Victau - lic Corp. in 1925. Cut Grooving is designed for stanard weight- ceives or heavier wall thickness pipe. tetrafluoroethylene (tet-ra-- theseveral lower variouslyterminal, whichshaped re or decalescensecryolite (de-ca-les-cen- ming and flood consisting(cry-o-lite) of sodium-alumi earthfluo-ro-eth-yl-ene) by alternately dam a colorless, thegrooved vapors tools. from 4. anonpressure tool used by se) a decrease in temperaturea mineral nonflammable gas used in mak- metalworkers to shape material thatnum occurs fluoride. while Usedheating for soldermet- ing a stream. See STANK. or the pressure sterilizers, and - spannering heat resistantwrench and(span-ner acid re - conductsto a desired the form vapors. 5. a tooldirectly used al ingthrough copper a rangeand inalloys which when a mixed with phosphoric acid.- wrench)sistant plastics 1. one ofsuch various as teflon. tools to setthe theouter teeth air. of Sometimesaatmosphere circular or exhaust vent. See change in a structure occurs. Also used for soldering alumi forAbbr. tightening, T.F.E. or loosening,chiefly Brit.: orcalled band vapor, saw. steam,6. a tool used to degree of hazard (de-gree stench trap (stench trap) num bronze when mixed with nutsthermal and bolts.expansion 2. (water) straightenLOCAL VENT. -

Euro Stoxx® Total Market Index

EURO STOXX® TOTAL MARKET INDEX Components1 Company Supersector Country Weight (%) ASML HLDG Technology Netherlands 4.29 LVMH MOET HENNESSY Consumer Products & Services France 3.27 SAP Technology Germany 2.34 LINDE Chemicals Germany 2.26 TOTALENERGIES Energy France 1.89 SANOFI Health Care France 1.82 SIEMENS Industrial Goods & Services Germany 1.81 L'OREAL Consumer Products & Services France 1.73 ALLIANZ Insurance Germany 1.62 SCHNEIDER ELECTRIC Industrial Goods & Services France 1.35 AIR LIQUIDE Chemicals France 1.24 AIRBUS Industrial Goods & Services France 1.19 DAIMLER Automobiles & Parts Germany 1.17 IBERDROLA Utilities Spain 1.14 ENEL Utilities Italy 1.13 BNP PARIBAS Banks France 1.12 BASF Chemicals Germany 1.08 DEUTSCHE TELEKOM Telecommunications Germany 1.03 BCO SANTANDER Banks Spain 1.03 VINCI Construction & Materials France 1.01 DEUTSCHE POST Industrial Goods & Services Germany 1.01 Kering Retail France 1.00 ADYEN Industrial Goods & Services Netherlands 0.98 ANHEUSER-BUSCH INBEV Food, Beverage & Tobacco Belgium 0.97 ADIDAS Consumer Products & Services Germany 0.97 BAYER Health Care Germany 0.94 SAFRAN Industrial Goods & Services France 0.86 AXA Insurance France 0.83 ESSILORLUXOTTICA Health Care France 0.81 INTESA SANPAOLO Banks Italy 0.78 ING GRP Banks Netherlands 0.77 HERMES INTERNATIONAL Consumer Products & Services France 0.77 INFINEON TECHNOLOGIES Technology Germany 0.77 VOLKSWAGEN PREF Automobiles & Parts Germany 0.72 PHILIPS Health Care Netherlands 0.71 DANONE Food, Beverage & Tobacco France 0.69 Prosus Technology Netherlands -

Determinants and Value of Enterprise Risk Management: Empirical Evidence from Germany

Determinants and Value of Enterprise Risk Management: Empirical Evidence from Germany Philipp Lechner, Nadine Gatzert Working Paper Department of Insurance Economics and Risk Management Friedrich-Alexander University Erlangen-Nürnberg (FAU) Version: February 2017 1 DETERMINANTS AND VALUE OF ENTERPRISE RISK MANAGEMENT: EMPIRICAL EVIDENCE FROM GERMANY Philipp Lechner, Nadine Gatzert* This version: February 21, 2017 ABSTRACT Enterprise risk management (ERM) has become increasingly relevant in recent years, espe- cially due to an increasing complexity of risks and the further development of regulatory frameworks. The aim of this paper is to empirically analyze firm characteristics that deter- mine the implementation of an ERM system and to study the impact of ERM on firm value. We focus on companies listed at the German stock exchange, which to the best of our knowledge is the first empirical study with a cross-sectional analysis for Germany and one of the first for a European country. Our findings show that size, international diversifica- tion, and the industry sector (banking, insurance, energy) positively impact the implementa- tion of an ERM system, and financial leverage is negatively related to ERM engagement. In addition, our results confirm a significant positive impact of ERM on shareholder value. Keywords: Enterprise risk management; firm characteristics; shareholder value JEL Classification: G20; G22; G32 1. INTRODUCTION In recent years, enterprise risk management (ERM) has become increasingly relevant, espe- cially against the background of an increasing complexity of risks, increasing dependencies between risk sources, more advanced methods of risk identification and quantification and information technologies, the consideration of ERM systems in rating processes, as well as stricter regulations in the aftermath of the financial crisis, among other drivers (see, e.g., Hoyt and Liebenberg, 2011; Pagach and Warr, 2011).