Deleveraging, Deflation and Depreciation in the Euro Area

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Debt-Deflation Theory of Great Depressions by Irving Fisher

THE DEBT-DEFLATION THEORY OF GREAT DEPRESSIONS BY IRVING FISHER INTRODUCTORY IN Booms and Depressions, I have developed, theoretically and sta- tistically, what may be called a debt-deflation theory of great depres- sions. In the preface, I stated that the results "seem largely new," I spoke thus cautiously because of my unfamiliarity with the vast literature on the subject. Since the book was published its special con- clusions have been widely accepted and, so far as I know, no one has yet found them anticipated by previous writers, though several, in- cluding myself, have zealously sought to find such anticipations. Two of the best-read authorities in this field assure me that those conclu- sions are, in the words of one of them, "both new and important." Partly to specify what some of these special conclusions are which are believed to be new and partly to fit them into the conclusions of other students in this field, I am offering this paper as embodying, in brief, my present "creed" on the whole subject of so-called "cycle theory." My "creed" consists of 49 "articles" some of which are old and some new. I say "creed" because, for brevity, it is purposely ex- pressed dogmatically and without proof. But it is not a creed in the sense that my faith in it does not rest on evidence and that I am not ready to modify it on presentation of new evidence. On the contrary, it is quite tentative. It may serve as a challenge to others and as raw material to help them work out a better product. -

Deleveraging and the Aftermath of Overexpansion

May 28th, 2009 Jeffrey Owen Herzog Deleveraging and the aftermath of overexpansion [email protected] O The deleveraging process for commercial banks is likely to last years and overshoot compared to fundamentals Banking System Asset and Leverage Growth O A strong procyclical correlation exists between asset growth and Nominal Values, 1934-2008 leverage growth over the past 75 years 25% O At the level of the firm, boom times generate decreasing 20% 1942 collateralization rates and increasing average loan sizes 15% O Given two-year loan losses of $1.1tr and leverage declines of -5% 10% 2008 to -7.5%, we expect deleveraging to curtail commercial bank 5% credit by $646bn and $687bn per year for 2009-2010 0% -5% Trends in deleveraging and commercial banking over time Leverage Growth -10% 2004 -15% 1946 Deleveraging is the process whereby commercial banks reduce their ratio of -20% assets to equity capital, thus bringing down their aggregate exposure to the 0% 5% -5% 10% 15% 20% 25% 30% economy. Many commentators point to this process as an eventual destination -10% Asset Growth for the US commercial banking system, but few have described where or how Source: FDIC we arrive at a more deleveraged commercial banking system. Commercial Bank Assets and Equity Adjusted for Inflation by CPI, $tr Over the past seventy years, the commercial banking sector’s aggregate 0.6 6 balance sheet has demonstrated a strong positive correlation between leverage and asset growth. For the banking industry, 2004 was an 0.5 5 S&L Crisis, 1989-1991 exceptionally unusual year, with equity increasing yoy by 22%. -

The Deleveraging of U.S. Households: Credit Card Debt Over the Lifecycle

2016 n Number 11 ECONOMIC Synopses The Deleveraging of U.S. Households: Credit Card Debt over the Lifecycle Helu Jiang, Technical Research Associate Juan M. Sanchez, Research Officer and Economist ggertsson and Krugman (2012) contend that “if there Total Credit Card Debt is a single word that appears most frequently in dis - $ Billions cussions of the economic problems now afflicting E 900 both the United States and Europe, that word is surely 858 865 debt.” These authors and others offer theoretical models 850 that present the debt phenomenon as follows: The econo my 800 788 792 756 is populated by impatient and patient individuals. Impatient 744 751 750 individuals borrow as much as possible, up to a debt limit. 718 When the debt limit suddenly tightens, impatient individ - 700 683 665 656 648 uals must cut expenditures to pay their debt, depressing 650 aggregate demand and generating debt-driven slumps. Such 600 a reduction in debt is called deleveraging . 2004 2005 2006 2007 2008 2009 2010 20 11 2012 2013 2014 2015 SOURCE: Federal Reserve Bank of New York Consumer Credit Panel/Equifax. Individuals younger than 46 deleveraged the most after the Share of the Change in Total Credit Card Debt financial crisis of 2008. by Age Group Percent 25 21 20 The evolution of total credit card debt around the finan - 14 14 14 15 13 11 cial crisis of 2008 appears consistent with that sequence: 8 10 6 Credit card debt increased quickly before the financial cri sis 5 1 3 3 0 and then fell for six years after that episode. -

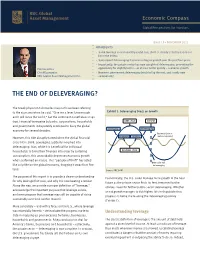

The End of Deleveraging?

Economic Compass Global Perspectives for Investors Issue 19 • NOVEMBER 2012 HIGHLIGHTS › Some leverage is economically useful, but, the U.S. clearly took this notion too far in the 2000s. › Subsequent deleveraging has been a drag on growth over the past four years. › Importantly, the private sector has now completed deleveraging, presenting the Eric Lascelles opportunity for slightly better – or at least better quality – economic growth. Chief Economist › However, government deleveraging tends to lag the rest, and is only now RBC Global Asset Management Inc. commencing. THE END OF DELEVERAGING? The Greek physicist Archimedes may not have been referring to the economy when he said, “Give me a lever long enough Exhibit 1: Deleveraging Drags on Growth and I will move the world,” but the sentiment nonetheless rings true. Financial leveraging by banks, corporations, households DEBT CYCLE PRESENT and governments indisputably combined to buoy the global Leveraging Deleveraging economy for several decades. Business Cycle in However, this tide abruptly turned when the global financial Downswing Upswing cautious upswing crisis hit in 2008. Leveraging suddenly morphed into deleveraging. Alas, while it is beneficial for individual households to bring their finances into order by curtailing BUSINESS CYCLE consumption, this unavoidably depresses economic growth when performed en masse. This “paradox of thrift” has acted Debt Cycle still like a riptide on the global economy, dragging it away from firm deleveraging land. Source: RBC GAM The purpose of this report is to provide a clearer understanding Economically, the U.S. could manage more growth in the near for why leverage first rose, and why it is now beating a retreat. -

Credit Reallocation, Deleveraging, and Financial Crises

Credit Reallocation, Deleveraging, and Financial Crises Junghwan Hyun Raoul Minetti∗ Hiroshima University Michigan State University Abstract This paper studies how the process of reallocation of credit across firms behaves before and after financial crises. Applying the methodology proposed by Davis and Haltiwanger (1992) for measuring job reallocation, we track the dynamics of credit reallocation across Korean firms for over three decades (1980 2012). The credit − boom preceding the 1997 crisis featured a slowdown of credit reallocation. Af- ter the crisis and the associated reforms, the creditless recovery (deleveraging) masked a dramatic intensification and increased procyclicality of credit realloca- tion. The findings suggest that the crisis and the associated reforms have triggered an efficiency-enhancing increase in the fluidity of the credit market. Keywords: Credit Reallocation, Credit Growth, Financial Crises. JEL Codes: E44 ∗Raoul Minetti: Department of Economics, 486 W. Circle Drive, 110 Marshall-Adams Hall, Michi- gan State University, East Lansing, MI 48824-1038. E-mail: [email protected] . Junghwan Hyun: gre- [email protected] . We wish to thank several seminar and conference participants for their comments and suggestions. All remaining errors are ours. 1 Credit Reallocation, Deleveraging, and Financial Crises Abstract This paper studies how the process of reallocation of credit across firms behaves before and after financial crises. Applying the method- ology proposed by Davis and Haltiwanger (1992) for measuring job re- allocation, we track the dynamics of credit reallocation across Korean firms for over three decades (1980 2012). The credit boom preceding − the 1997 crisis featured a slowdown of credit reallocation. After the crisis and the associated reforms, the creditless recovery (deleveraging) masked a dramatic intensification and increased procyclicality of credit reallocation. -

Debt Overhang and Deleveraging in the US

Working Paper Series Bruno Albuquerque and Debt overhang and deleveraging Georgi Krustev in the US household sector: gauging the impact on consumption No 1843 / August 2015 Note: This Working Paper should not be reported as representing the views of the European Central Bank (ECB). The views expressed are those of the authors and do not necessarily reflect those of the ECB Abstract Using a novel dataset for the US states, this paper examines whether household debt and the protracted debt deleveraging help explain the dismal performance of US consumption since 2007 in the aftermath of the housing bubble. By separating the concepts of deleveraging and debt overhang { a flow and a stock effect { we find that excessive indebtedness exerted a meaningful drag on consumption over and beyond income and wealth effects. The overall impact, however, is modest { around one-sixth of the slowdown in consumption between 2000-06 and 2007-12 { and mostly driven by states with particularly large imbalances in their household sector. This might be indicative of non-linearities, whereby indebtedness begins to bite only when misalignments from sustainable debt dynamics become excessive. Keywords: Household deleveraging, Debt overhang, Consumption function, Housing wealth. JEL Classification: C13, C23, C52, D12, H31 ECB Working Paper 1843, August 2015 1 Non-technical summary The leveraging and subsequent deleveraging cycle in the US household sector played a significant role in affecting the performance of economic activity in the years around the Great Recession. A growing body of theoretical and empirical studies have thus focused on explaining to what extent and through which channels the excessive build-up of debt and the deleveraging phase might have contributed to depress economic activity and consumption growth. -

Firm Debt Deflation, Household Precautionary Savings, and the Amplification of Aggregate Shocks*

Firm Debt Deflation, Household Precautionary Savings, and the Amplification of Aggregate Shocks Andrea Caggese Angelo Gutierrez Ander Pérez-Orive Universitat Pompeu Fabra, Universitat Pompeu Fabra Federal Reserve Board CREI & Barcelona GSE [PRELIMINARY AND INCOMPLETE] (This Version: February 2019) Abstract Deleveraging shocks that increase household precautionary savings, and financial and uncertainty shocks to firms, interact and amplify each other, even when these same shocks separately have moderate effects on output and employment. This result is obtained in a model in which heterogeneous households face financial frictions and unemployment risk and in which heterogeneous firms borrow funds using nominally fixed long-term debt and face costly bankruptcy. This novel amplification mechanism is based on a dynamic feedback between the precautionary behavior of households and the bankruptcy and entry decisions of firms. Our results support the view that firm financial frictions are important to understand the effect of household deleveraging on unemployment, consistent with recent empirical studies examining the 2007-2009 Great Recession. Keywords: Financial Shocks, Amplification, Precautionary Savings, Unemployment Risk, Borrowing Constraints, Firm Bankruptcy Risk JEL Classification: E21, E24, G33 * A previous version of this paper circulated with the title "The Interaction between Household and Firm Dynamics and the Amplification of Financial Shocks". We thank Chris Carroll, Wouter den Haan, Simon Gilchrist, Joao Gomes (discussant), Bob Hall, Juan Jimeno -

Why Was Japan Hit So Hard by the Global Financial Crisis?

ADBI Working Paper Series Why was Japan Hit So Hard by the Global Financial Crisis? Masahiro Kawai and Shinji Takagi No. 153 October 2009 Asian Development Bank Institute ADBI Working Paper 153 Kawai and Takagi Masahiro Kawai is the dean of the Asian Development Bank Institute. Shinji Takagi is a professor, Graduate School of Economics, Osaka University, Osaka, Japan. This is a revised version of the paper presented at the Samuel Hsieh Memorial Conference, hosted by the Chung-Hua Institution for Economic Research, Taipei,China 9–10 July 2009. The authors are thankful to Ainslie Smith for her editorial work. The views expressed in this paper are the views of the authors and do not necessarily reflect the views or policies of ADBI, the Asian Development Bank (ADB), its Board of Directors, or the governments they represent. ADBI does not guarantee the accuracy of the data included in this paper and accepts no responsibility for any consequences of their use. Terminology used may not necessarily be consistent with ADB official terms. The Working Paper series is a continuation of the formerly named Discussion Paper series; the numbering of the papers continued without interruption or change. ADBI’s working papers reflect initial ideas on a topic and are posted online for discussion. ADBI encourages readers to post their comments on the main page for each working paper (given in the citation below). Some working papers may develop into other forms of publication. Suggested citation: Kawai, M., and S. Takagi. 2009. Why was Japan Hit So Hard by the Global Financial Crisis? ADBI Working Paper 153. -

The U .S . Recovery from the Great Recession: a Story of Debt and Deleveraging Brady Lavender and Nicolas Parent, International Economic Analysis

THE u .S . RECOVERY FROM THE GREAT RECEssION: A STORY OF DEbt AND DELEVERAGING 13 BANK OF CANADA REVIEW • WIntER 2012–2013 The U .S . Recovery from the Great Recession: A Story of Debt and Deleveraging Brady Lavender and Nicolas Parent, International Economic Analysis The prolonged period of deficient demand in the United States following the Great Recession is unusual relative to past U.S. recessions, but is consistent with historical international experience in the aftermath of severe financial crises. Loose lending standards and relatively low interest rates in the pre-crisis period contributed to a sharp buildup in household debt. Subsequently, household deleveraging has been the most important factor holding back the recovery. While a large fiscal expansion helped to sustain aggregate demand during the crisis and its aftermath, the federal debt in the United States is currently on an unsustainable trajectory. The government sector now needs to delever, which will represent a drag on economic growth for years to come. Given Canada’s close real and financial linkages with the United States, understanding the trajectory and characteristics of the U.S. recovery has important implications for the Canadian economy and thus monetary policy. In December 2007, the U.S. economy entered its longest and deepest recession since the Great Depression. Historically, in the early stages of a recovery, U.S. GDP has typically grown at a faster rate than the potential growth rate of the economy, reflecting pent-up demand from businesses and consumers and some rebuilding of inventories. Deep economic down- turns thus tend to be associated with stronger rebounds (Howard, Martin and Wilson 2011). -

Overborrowing, Deleveraging and a Great Recession ∗

Overborrowing, Deleveraging and a Great Recession ∗ Phuong V. Ngoy Cleveland State University Abstract This paper examines the role of overborrowing, deleveraging, and an incomplete financial market in driving an economy to a great recession with a binding zero lower bound on the nominal interest rate (ZLB). There are two key features that differentiate my work from the current literature of deleveraging and the ZLB. First, I endogenize the debt limit of borrowers by tying it to the market value of collateral assets. Second, and more importantly, I allow for overborrowing by calibrating the model to match with the high debt-to-income ratio at the onset of the Great Recession for the U.S. homeowners that owned a house in 1997. I am able to show that the second feature makes the ZLB more likely to bind under an adverse shock to the credit market. When the ZLB binds, a great recession emerges with a free fall in output and the price level, mostly due to the Fisherian debt deflation that puts more debt burden on the borrowers. JEL classification: E21, E32, E44, C61. Keywords: overborrowing, deleveraging, the ZLB, liquidity trap, Taylor rule, Great Recession, Fisherian debt deflation. ∗I would like to thank Jianjun Miao, Robert King, Francois Gourio, J.Christina Wang and Alisdair McKay for their discussion and comments. Also, I would like to thank the participants of the BU dissertation workshop, BU macro reading group, and Cleveland State University seminar, Fall 2013 Midwest Macro Meeting for their comments and suggestions. All errors in the paper are mine. yDepartment of Economics, Cleveland State University, 2121 Euclid Avenue, Cleveland, OH 44115. -

Mark Carney: Growth in the Age of Deleveraging

Mark Carney: Growth in the age of deleveraging Remarks by Mr Mark Carney, Governor of the Bank of Canada and Chairman of the Financial Stability Board, to the Empire Club of Canada/Canadian Club of Toronto, Toronto, Ontario, 12 December 2011. * * * Introduction These are trying times. In our largest trading partner, households are undergoing a long process of balance-sheet repair. Partly as a consequence, American demand for Canadian exports is $30 billion lower than normal. In Europe, a renewed crisis is underway. An increasing number of countries are being forced to pay unsustainable rates on their borrowings. With a vicious deleveraging process taking hold in its banking sector, the euro area is sinking into recession. Given ties of trade, finance and confidence, the rest of the world is beginning to feel the effects. Most fundamentally, current events mark a rupture. Advanced economies have steadily increased leverage for decades. That era is now decisively over. The direction may be clear, but the magnitude and abruptness of the process are not. It could be long and orderly or it could be sharp and chaotic. How we manage it will do much to determine our relative prosperity. This is my subject today: how Canada can grow in this environment of global deleveraging. How we got here: the debt super cycle First, it is important to get a sense of the scale of the challenge. Accumulating the mountain of debt now weighing on advanced economies has been the work of a generation. Across G-7 countries, total non-financial debt has doubled since 1980 to 300 per cent of GDP. -

On the Optimal Speed of Sovereign Deleveraging

On the Optimal Speed of Sovereign Deleveraging with Precautionary Savings∗ Thomas Philippon† and Francisco Roldán‡ March 2018 Abstract We study the interaction between sovereign risk and aggregate demand driven by the endogenous response of savers to sovereign risk. We obtain two main results. First, this new sovereign risk / aggregate demand channel creates a tradeoff between the recessionary impact of fiscal consolidation and the risk of a future sovereign debt crisis. Risk aversion has a large impact on output losses and on welfare when sovereign debt is risky. Second, we find that savers and borrowers disagree about the optimal path of sovereign deleveraging. The sovereign risk channel can therefore explain some of the rise in political disagreement about fiscal policy. Using a version of the model calibrated to the Eurozone crisis, we find that sovereign risk justifies starting to deleverage about two years after the beginning of the recession. We also find that, after 2012, the channel was weakened so that active deleveraging in a recession is no longer justified. JEL: E2, G2, N2 ∗We are grateful to Marcos Chamon, Olivier Blanchard, Linda Tesar and Pierre-Olivier Gourinchas for comments and discussions. †Stern School of Business, New York University; NBER and CEPR. ‡New York University 1 How fast should governments reduce their leverage? The question has been at the center of much policy debate in the aftermath of the Great Recession and of the Eurozone crisis. One side of the tradeoff is rather straightforward. In a non-Ricardian world, fiscal consolidation can depress aggregate demand and decrease employment. Whether this is good or bad depends on the state of the economy.