Peter Praet: Deleveraging and Monetary Policy

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Deleveraging and the Aftermath of Overexpansion

May 28th, 2009 Jeffrey Owen Herzog Deleveraging and the aftermath of overexpansion [email protected] O The deleveraging process for commercial banks is likely to last years and overshoot compared to fundamentals Banking System Asset and Leverage Growth O A strong procyclical correlation exists between asset growth and Nominal Values, 1934-2008 leverage growth over the past 75 years 25% O At the level of the firm, boom times generate decreasing 20% 1942 collateralization rates and increasing average loan sizes 15% O Given two-year loan losses of $1.1tr and leverage declines of -5% 10% 2008 to -7.5%, we expect deleveraging to curtail commercial bank 5% credit by $646bn and $687bn per year for 2009-2010 0% -5% Trends in deleveraging and commercial banking over time Leverage Growth -10% 2004 -15% 1946 Deleveraging is the process whereby commercial banks reduce their ratio of -20% assets to equity capital, thus bringing down their aggregate exposure to the 0% 5% -5% 10% 15% 20% 25% 30% economy. Many commentators point to this process as an eventual destination -10% Asset Growth for the US commercial banking system, but few have described where or how Source: FDIC we arrive at a more deleveraged commercial banking system. Commercial Bank Assets and Equity Adjusted for Inflation by CPI, $tr Over the past seventy years, the commercial banking sector’s aggregate 0.6 6 balance sheet has demonstrated a strong positive correlation between leverage and asset growth. For the banking industry, 2004 was an 0.5 5 S&L Crisis, 1989-1991 exceptionally unusual year, with equity increasing yoy by 22%. -

Friday, June 21, 2013 the Failures That Ignited America's Financial

Friday, June 21, 2013 The Failures that Ignited America’s Financial Panics: A Clinical Survey Hugh Rockoff Department of Economics Rutgers University, 75 Hamilton Street New Brunswick NJ 08901 [email protected] Preliminary. Please do not cite without permission. 1 Abstract This paper surveys the key failures that ignited the major peacetime financial panics in the United States, beginning with the Panic of 1819 and ending with the Panic of 2008. In a few cases panics were triggered by the failure of a single firm, but typically panics resulted from a cluster of failures. In every case “shadow banks” were the source of the panic or a prominent member of the cluster. The firms that failed had excellent reputations prior to their failure. But they had made long-term investments concentrated in one sector of the economy, and financed those investments with short-term liabilities. Real estate, canals and railroads (real estate at one remove), mining, and cotton were the major problems. The panic of 2008, at least in these ways, was a repetition of earlier panics in the United States. 2 “Such accidental events are of the most various nature: a bad harvest, an apprehension of foreign invasion, the sudden failure of a great firm which everybody trusted, and many other similar events, have all caused a sudden demand for cash” (Walter Bagehot 1924 [1873], 118). 1. The Role of Famous Failures1 The failure of a famous financial firm features prominently in the narrative histories of most U.S. financial panics.2 In this respect the most recent panic is typical: Lehman brothers failed on September 15, 2008: and … all hell broke loose. -

The Historical Role of the European Shadow Banking System in the Development and Evolution of Our Monetary Institutions

CITYPERC Working Paper Series The Historical Role of the European Shadow Banking System in the Development and Evolution of Our Monetary Institutions Israel Cedillo Lazcano CITYPERC Working Paper No. 2013-05 City Political Economy Research Centre [email protected] / @cityperc City, University of London Northampton Square London EC1V 0HB United Kingdom The Historical Role of the European Shadow Banking System in the Development and Evolution of Our Monetary Institutions Israel Cedillo Lazcano* Abstract When we hear about the 2008 Lehman Brothers crisis, immediately we relate it to the concept of “shadow banking system”; however, the credit intermediation involving lightly regulated entities and activities outside the traditional banking system are not new for the European Financial Systems, after all, many innovations developed in the past, were adopted by European nations and exported to the rest of the world (i.e. coinage and central banking), and European innovators unleashed several financial crises related to “shadowy” financial intermediaries (i.e. the Gebroeders de Neufville crisis of 1763). However, despite not many academics, legislators and regulators even agree on what “shadow banking” is, this latter does not refer exclusively to the functions of credit intermediation and maturity transformation. This concept also refers to the creation of assets such as digital media of exchange which are designed under the influence of Friedrich Hayek and the Austrian School of Economics. This lack of a uniform definition of “shadow banking” has limited our regulatory efforts on key issues like the private money creation, a source of vulnerability in the financial system that, paradoxically, at the same time could result in an opportunity to renovate European institutions, heirs of the tradition of the Wisselbank and the Bank of England which, during the seventeenth century, faced monetary innovations and led the European monetary revolution that originated the current monetary and regulatory practices implemented around the world. -

Nber Working Paper Series International Borrowing

NBER WORKING PAPER SERIES INTERNATIONAL BORROWING CYCLES: A NEW HISTORICAL DATABASE Graciela L. Kaminsky Working Paper 22819 http://www.nber.org/papers/w22819 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge, MA 02138 November 2016 I gratefully acknowledge support from the National Science Foundation (Award No 1023681) and the Institute for New Economic Thinking (Grant No INO14-00009). I want to thank Katherine Carpenter, Samuel Mackey, Jeffrey Messina, Andrew Olenski, and Pablo Vega-García for superb research assistance. The views expressed herein are those of the author and do not necessarily reflect the views of the National Bureau of Economic Research. NBER working papers are circulated for discussion and comment purposes. They have not been peer-reviewed or been subject to the review by the NBER Board of Directors that accompanies official NBER publications. © 2016 by Graciela L. Kaminsky. All rights reserved. Short sections of text, not to exceed two paragraphs, may be quoted without explicit permission provided that full credit, including © notice, is given to the source. International Borrowing Cycles: A New Historical Database Graciela L. Kaminsky NBER Working Paper No. 22819 November 2016 JEL No. F30,F34,F65 ABSTRACT The ongoing slowdown in international capital flows has brought again to the attention the booms and bust cycles in international borrowing. Many suggest that capital flow bonanzas are excessive, ending in crises. One of the most frequently mentioned culprits are the cycles of monetary easing and tightening in the financial centers. More recently, the 2008 Subprime Crisis in the United States has also been blamed for the retrenchment in capital flows to both developed and developing countries. -

The Deleveraging of U.S. Households: Credit Card Debt Over the Lifecycle

2016 n Number 11 ECONOMIC Synopses The Deleveraging of U.S. Households: Credit Card Debt over the Lifecycle Helu Jiang, Technical Research Associate Juan M. Sanchez, Research Officer and Economist ggertsson and Krugman (2012) contend that “if there Total Credit Card Debt is a single word that appears most frequently in dis - $ Billions cussions of the economic problems now afflicting E 900 both the United States and Europe, that word is surely 858 865 debt.” These authors and others offer theoretical models 850 that present the debt phenomenon as follows: The econo my 800 788 792 756 is populated by impatient and patient individuals. Impatient 744 751 750 individuals borrow as much as possible, up to a debt limit. 718 When the debt limit suddenly tightens, impatient individ - 700 683 665 656 648 uals must cut expenditures to pay their debt, depressing 650 aggregate demand and generating debt-driven slumps. Such 600 a reduction in debt is called deleveraging . 2004 2005 2006 2007 2008 2009 2010 20 11 2012 2013 2014 2015 SOURCE: Federal Reserve Bank of New York Consumer Credit Panel/Equifax. Individuals younger than 46 deleveraged the most after the Share of the Change in Total Credit Card Debt financial crisis of 2008. by Age Group Percent 25 21 20 The evolution of total credit card debt around the finan - 14 14 14 15 13 11 cial crisis of 2008 appears consistent with that sequence: 8 10 6 Credit card debt increased quickly before the financial cri sis 5 1 3 3 0 and then fell for six years after that episode. -

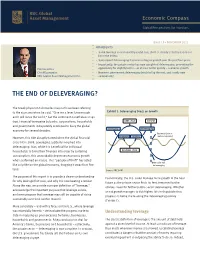

The End of Deleveraging?

Economic Compass Global Perspectives for Investors Issue 19 • NOVEMBER 2012 HIGHLIGHTS › Some leverage is economically useful, but, the U.S. clearly took this notion too far in the 2000s. › Subsequent deleveraging has been a drag on growth over the past four years. › Importantly, the private sector has now completed deleveraging, presenting the Eric Lascelles opportunity for slightly better – or at least better quality – economic growth. Chief Economist › However, government deleveraging tends to lag the rest, and is only now RBC Global Asset Management Inc. commencing. THE END OF DELEVERAGING? The Greek physicist Archimedes may not have been referring to the economy when he said, “Give me a lever long enough Exhibit 1: Deleveraging Drags on Growth and I will move the world,” but the sentiment nonetheless rings true. Financial leveraging by banks, corporations, households DEBT CYCLE PRESENT and governments indisputably combined to buoy the global Leveraging Deleveraging economy for several decades. Business Cycle in However, this tide abruptly turned when the global financial Downswing Upswing cautious upswing crisis hit in 2008. Leveraging suddenly morphed into deleveraging. Alas, while it is beneficial for individual households to bring their finances into order by curtailing BUSINESS CYCLE consumption, this unavoidably depresses economic growth when performed en masse. This “paradox of thrift” has acted Debt Cycle still like a riptide on the global economy, dragging it away from firm deleveraging land. Source: RBC GAM The purpose of this report is to provide a clearer understanding Economically, the U.S. could manage more growth in the near for why leverage first rose, and why it is now beating a retreat. -

Credit Reallocation, Deleveraging, and Financial Crises

Credit Reallocation, Deleveraging, and Financial Crises Junghwan Hyun Raoul Minetti∗ Hiroshima University Michigan State University Abstract This paper studies how the process of reallocation of credit across firms behaves before and after financial crises. Applying the methodology proposed by Davis and Haltiwanger (1992) for measuring job reallocation, we track the dynamics of credit reallocation across Korean firms for over three decades (1980 2012). The credit − boom preceding the 1997 crisis featured a slowdown of credit reallocation. Af- ter the crisis and the associated reforms, the creditless recovery (deleveraging) masked a dramatic intensification and increased procyclicality of credit realloca- tion. The findings suggest that the crisis and the associated reforms have triggered an efficiency-enhancing increase in the fluidity of the credit market. Keywords: Credit Reallocation, Credit Growth, Financial Crises. JEL Codes: E44 ∗Raoul Minetti: Department of Economics, 486 W. Circle Drive, 110 Marshall-Adams Hall, Michi- gan State University, East Lansing, MI 48824-1038. E-mail: [email protected] . Junghwan Hyun: gre- [email protected] . We wish to thank several seminar and conference participants for their comments and suggestions. All remaining errors are ours. 1 Credit Reallocation, Deleveraging, and Financial Crises Abstract This paper studies how the process of reallocation of credit across firms behaves before and after financial crises. Applying the method- ology proposed by Davis and Haltiwanger (1992) for measuring job re- allocation, we track the dynamics of credit reallocation across Korean firms for over three decades (1980 2012). The credit boom preceding − the 1997 crisis featured a slowdown of credit reallocation. After the crisis and the associated reforms, the creditless recovery (deleveraging) masked a dramatic intensification and increased procyclicality of credit reallocation. -

The Foundations of the Valuation of Insurance Liabilities

The foundations of the valuation of insurance liabilities Philipp Keller 14 April 2016 Audit. Tax. Consulting. Financial Advisory. Content • The importance and complexity of valuation • The basics of valuation • Valuation and risk • Market consistent valuation • The importance of consistency of market consistency • Financial repression and valuation under pressure • Hold-to-maturity • Conclusions and outlook 2 The foundations of the valuation of insurance liabilities The importance and complexity of valuation 3 The foundations of the valuation of insurance liabilities Valuation Making or breaking companies and nations Greece: Creative accounting and valuation and swaps allowed Greece to satisfy the Maastricht requirements for entering the EUR zone. Hungary: To satisfy the Maastricht requirements, Hungary forced private pension-holders to transfer their pensions to the public pension fund. Hungary then used this pension money to plug government debts. Of USD 15bn initially in 2011, less than 1 million remained at 2013. This approach worked because the public pension fund does not have to value its liabilities on an economic basis. Ireland: The Irish government issued a blanket state guarantee to Irish banks for 2 years for all retail and corporate accounts. Ireland then nationalized Anglo Irish and Anglo Irish Bank. The total bailout cost was 40% of GDP. US public pension debt: US public pension debt is underestimated by about USD 3.4 tn due to a valuation standard that grossly overestimates the expected future return on pension funds’ asset. (FT, 11 April 2016) European Life insurers: European life insurers used an amortized cost approach for the valuation of their life insurance liability, which allowed them to sell long-term guarantee products. -

Debt Overhang and Deleveraging in the US

Working Paper Series Bruno Albuquerque and Debt overhang and deleveraging Georgi Krustev in the US household sector: gauging the impact on consumption No 1843 / August 2015 Note: This Working Paper should not be reported as representing the views of the European Central Bank (ECB). The views expressed are those of the authors and do not necessarily reflect those of the ECB Abstract Using a novel dataset for the US states, this paper examines whether household debt and the protracted debt deleveraging help explain the dismal performance of US consumption since 2007 in the aftermath of the housing bubble. By separating the concepts of deleveraging and debt overhang { a flow and a stock effect { we find that excessive indebtedness exerted a meaningful drag on consumption over and beyond income and wealth effects. The overall impact, however, is modest { around one-sixth of the slowdown in consumption between 2000-06 and 2007-12 { and mostly driven by states with particularly large imbalances in their household sector. This might be indicative of non-linearities, whereby indebtedness begins to bite only when misalignments from sustainable debt dynamics become excessive. Keywords: Household deleveraging, Debt overhang, Consumption function, Housing wealth. JEL Classification: C13, C23, C52, D12, H31 ECB Working Paper 1843, August 2015 1 Non-technical summary The leveraging and subsequent deleveraging cycle in the US household sector played a significant role in affecting the performance of economic activity in the years around the Great Recession. A growing body of theoretical and empirical studies have thus focused on explaining to what extent and through which channels the excessive build-up of debt and the deleveraging phase might have contributed to depress economic activity and consumption growth. -

How to Prevent a Banking Panic: the Barings Crisis of 1890

How to Prevent a Banking Panic: the Barings Crisis of 1890 Financial histories have treated the Barings Crisis of 1890 as a minor or pseudo-crisis with no threat to the systems of payment and settlement. New evidence reveals that Baring Brothers was not simply suffering from a temporary liquidity problem but was an insolvent institution. Just as knowledge of its true condition was revealed and a full-scale panic was about to ignite, the Bank of England stepped in: but it did not respond as Bagehot recommended---and is generally believed. Instead of waiting for the panic to break and then lending freely at a high rate on good collateral, the Bank organized a pre-emptive lifeboat operation. A large domestic financial crisis was avoided, while effective steps were taken to mitigate the effects of moral hazard from this discretionary intervention. Eugene N. White Rutgers University and NBER Department of Economics New Brunswick, NJ 08901, USA [email protected] Economic History Association September 16-18, 2016 0 Since the failure of Northern Rock in the U.K. and the collapse of Baer Sterns, Lehman Brothers and AIG in the U.S. in 2007-2008, arguments have intensified over whether central banks should follow a Bagehot-style policy in a financial crisis or intervene to save a failing SIFI (systemically important financial institution). In this debate, the experience of central banks during the classical gold standard is regarded as crucially informative. Most scholars have concluded that the Bank of England eliminated panics by strictly following Walter Bagehot’s dictum in Lombard Street (1873) to lend freely at a high rate of interest on good collateral in a crisis. -

How to Prevent a Banking Panic: the Barings Crisis of 1890

How to Prevent a Banking Panic: the Barings Crisis of 1890 Eugene N. White Rutgers University and NBER Department of Economics New Brunswick, NJ 08901, USA [email protected] 175 Years of The Economist A Conference on Economics and the Media London, September 24-25, 2015 0 Since the failure of Northern Rock in the U.K. and the collapse of Baer Sterns, Lehman Brothers and AIG in the U.S. in 2007-2008, arguments have intensified over whether central banks should follow a Bagehot-style policy in a financial crisis or intervene to save a failing SIFI (systemically important financial institution). In this debate, the experience of central banks during the classical gold standard is regarded as crucially informative. Most scholars have concluded that the Bank of England eliminated panics by strictly following Walter Bagehot’s dictum in Lombard Street (1873) to lend freely at a high rate of interest on good collateral in a crisis. This paper re-examines the first major threat to British financial stability after the publication of Lombard Street, the Barings Crisis of 1890. Previous financial histories have treated it as a minor crisis, arising from a temporary liquidity problem that posed no threat to the systems of payment and settlement. However, contemporaries believed that a panic would engulf the financial system if Baring Brothers & Co., Britain’s second largest merchant/investment bank and a highly interconnected global institution, collapsed. New evidence reveals that this SIFI was a deeply insolvent bank whose true condition was obscured in the effort to halt a panic. -

Why Was Japan Hit So Hard by the Global Financial Crisis?

ADBI Working Paper Series Why was Japan Hit So Hard by the Global Financial Crisis? Masahiro Kawai and Shinji Takagi No. 153 October 2009 Asian Development Bank Institute ADBI Working Paper 153 Kawai and Takagi Masahiro Kawai is the dean of the Asian Development Bank Institute. Shinji Takagi is a professor, Graduate School of Economics, Osaka University, Osaka, Japan. This is a revised version of the paper presented at the Samuel Hsieh Memorial Conference, hosted by the Chung-Hua Institution for Economic Research, Taipei,China 9–10 July 2009. The authors are thankful to Ainslie Smith for her editorial work. The views expressed in this paper are the views of the authors and do not necessarily reflect the views or policies of ADBI, the Asian Development Bank (ADB), its Board of Directors, or the governments they represent. ADBI does not guarantee the accuracy of the data included in this paper and accepts no responsibility for any consequences of their use. Terminology used may not necessarily be consistent with ADB official terms. The Working Paper series is a continuation of the formerly named Discussion Paper series; the numbering of the papers continued without interruption or change. ADBI’s working papers reflect initial ideas on a topic and are posted online for discussion. ADBI encourages readers to post their comments on the main page for each working paper (given in the citation below). Some working papers may develop into other forms of publication. Suggested citation: Kawai, M., and S. Takagi. 2009. Why was Japan Hit So Hard by the Global Financial Crisis? ADBI Working Paper 153.