Deleveraging and the Aftermath of Overexpansion

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko Federal Reserve Bank of New York Staff Reports, No

Federal Reserve Bank of New York Staff Reports Intermediary Leverage Cycles and Financial Stability Tobias Adrian Nina Boyarchenko Staff Report No. 567 August 2012 Revised February 2015 This paper presents preliminary findings and is being distributed to economists and other interested readers solely to stimulate discussion and elicit comments. The views expressed in this paper are those of the authors and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author. Intermediary Leverage Cycles and Financial Stability Tobias Adrian and Nina Boyarchenko Federal Reserve Bank of New York Staff Reports, no. 567 August 2012; revised February 2015 JEL classification: E02, E32, G00, G28 Abstract We present a theory of financial intermediary leverage cycles within a dynamic model of the macroeconomy. Intermediaries face risk-based funding constraints that give rise to procyclical leverage and a procyclical share of intermediated credit. The pricing of risk varies as a function of intermediary leverage, and asset return exposures to intermediary leverage shocks earn a positive risk premium. Relative to an economy with constant leverage, financial intermediaries generate higher consumption growth and lower consumption volatility in normal times, at the cost of endogenous systemic financial risk. The severity of systemic crisis depends on two state variables: intermediaries’ leverage and net worth. Regulations that tighten funding constraints affect the systemic risk-return tradeoff by lowering the likelihood of systemic crises at the cost of higher pricing of risk. Key words: financial stability, macro-finance, macroprudential, capital regulation, dynamic equilibrium models, asset pricing _________________ Adrian, Boyarchenko: Federal Reserve Bank of New York (e-mail: [email protected], [email protected]). -

Facts and Challenges from the Great Recession for Forecasting and Macroeconomic Modeling

NBER WORKING PAPER SERIES FACTS AND CHALLENGES FROM THE GREAT RECESSION FOR FORECASTING AND MACROECONOMIC MODELING Serena Ng Jonathan H. Wright Working Paper 19469 http://www.nber.org/papers/w19469 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge, MA 02138 September 2013 We are grateful to Frank Diebold and two anonymous referees for very helpful comments on earlier versions of this paper. Kyle Jurado provided excellent research assistance. The first author acknowledges financial support from the National Science Foundation (SES-0962431). All errors are our sole responsibility. The views expressed herein are those of the authors and do not necessarily reflect the views of the National Bureau of Economic Research. At least one co-author has disclosed a financial relationship of potential relevance for this research. Further information is available online at http://www.nber.org/papers/w19469.ack NBER working papers are circulated for discussion and comment purposes. They have not been peer- reviewed or been subject to the review by the NBER Board of Directors that accompanies official NBER publications. © 2013 by Serena Ng and Jonathan H. Wright. All rights reserved. Short sections of text, not to exceed two paragraphs, may be quoted without explicit permission provided that full credit, including © notice, is given to the source. Facts and Challenges from the Great Recession for Forecasting and Macroeconomic Modeling Serena Ng and Jonathan H. Wright NBER Working Paper No. 19469 September 2013 JEL No. C22,C32,E32,E37 ABSTRACT This paper provides a survey of business cycle facts, updated to take account of recent data. Emphasis is given to the Great Recession which was unlike most other post-war recessions in the US in being driven by deleveraging and financial market factors. -

1 Solving the Present Crisis and Managing the Leverage Cycle John Geanakoplos We Are at the Acute Crisis Stage of a Leverage

Solving the Present Crisis and Managing the Leverage Cycle John Geanakoplos1 We are at the acute crisis stage of a leverage cycle, a very big cycle. I write to propose a plan with concrete steps that the government could take to address the severe financial condition that we now find ourselves in. It is critical that any rescue plan be clear and transparent, implementable and not subject to fraud, and comprehensive enough to succeed and to convince the public it will succeed. The law already enacted by Congress was admittedly an emergency measure designed to staunch further immediate hemorrhaging. What to do next is the question; understanding how we got here will help us find the right set of answers. The leverage cycle is a recurring phenomenon in American financial history. Most recently, one ended in the derivatives crisis in 1994 that bankrupted Orange County, and another ended in the Emerging Markets-mortgage crisis of 1998 that bankrupted Long Term Capital. A proper understanding of the origins of the cycle shows the way to manage it and to deal with the final crisis stage. A critical aspect of the leverage cycle is that collateral margin rates change. Two years ago a home buyer could make a 5% downpayment on a house, and borrow the other 95%. Now he must put 25% down. Two years ago a mortgage security buyer could put 3% or 10% down, borrowing the rest. Now he must pay 100% in cash. All leverage cycles end with (1) bad news creating more uncertainty and disagreement, (2) sharply increasing collateral margin rates, and (3) losses and bankruptcies among the leveraged optimists. -

The Deleveraging of U.S. Households: Credit Card Debt Over the Lifecycle

2016 n Number 11 ECONOMIC Synopses The Deleveraging of U.S. Households: Credit Card Debt over the Lifecycle Helu Jiang, Technical Research Associate Juan M. Sanchez, Research Officer and Economist ggertsson and Krugman (2012) contend that “if there Total Credit Card Debt is a single word that appears most frequently in dis - $ Billions cussions of the economic problems now afflicting E 900 both the United States and Europe, that word is surely 858 865 debt.” These authors and others offer theoretical models 850 that present the debt phenomenon as follows: The econo my 800 788 792 756 is populated by impatient and patient individuals. Impatient 744 751 750 individuals borrow as much as possible, up to a debt limit. 718 When the debt limit suddenly tightens, impatient individ - 700 683 665 656 648 uals must cut expenditures to pay their debt, depressing 650 aggregate demand and generating debt-driven slumps. Such 600 a reduction in debt is called deleveraging . 2004 2005 2006 2007 2008 2009 2010 20 11 2012 2013 2014 2015 SOURCE: Federal Reserve Bank of New York Consumer Credit Panel/Equifax. Individuals younger than 46 deleveraged the most after the Share of the Change in Total Credit Card Debt financial crisis of 2008. by Age Group Percent 25 21 20 The evolution of total credit card debt around the finan - 14 14 14 15 13 11 cial crisis of 2008 appears consistent with that sequence: 8 10 6 Credit card debt increased quickly before the financial cri sis 5 1 3 3 0 and then fell for six years after that episode. -

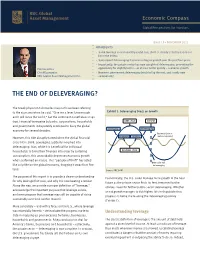

The End of Deleveraging?

Economic Compass Global Perspectives for Investors Issue 19 • NOVEMBER 2012 HIGHLIGHTS › Some leverage is economically useful, but, the U.S. clearly took this notion too far in the 2000s. › Subsequent deleveraging has been a drag on growth over the past four years. › Importantly, the private sector has now completed deleveraging, presenting the Eric Lascelles opportunity for slightly better – or at least better quality – economic growth. Chief Economist › However, government deleveraging tends to lag the rest, and is only now RBC Global Asset Management Inc. commencing. THE END OF DELEVERAGING? The Greek physicist Archimedes may not have been referring to the economy when he said, “Give me a lever long enough Exhibit 1: Deleveraging Drags on Growth and I will move the world,” but the sentiment nonetheless rings true. Financial leveraging by banks, corporations, households DEBT CYCLE PRESENT and governments indisputably combined to buoy the global Leveraging Deleveraging economy for several decades. Business Cycle in However, this tide abruptly turned when the global financial Downswing Upswing cautious upswing crisis hit in 2008. Leveraging suddenly morphed into deleveraging. Alas, while it is beneficial for individual households to bring their finances into order by curtailing BUSINESS CYCLE consumption, this unavoidably depresses economic growth when performed en masse. This “paradox of thrift” has acted Debt Cycle still like a riptide on the global economy, dragging it away from firm deleveraging land. Source: RBC GAM The purpose of this report is to provide a clearer understanding Economically, the U.S. could manage more growth in the near for why leverage first rose, and why it is now beating a retreat. -

Credit Reallocation, Deleveraging, and Financial Crises

Credit Reallocation, Deleveraging, and Financial Crises Junghwan Hyun Raoul Minetti∗ Hiroshima University Michigan State University Abstract This paper studies how the process of reallocation of credit across firms behaves before and after financial crises. Applying the methodology proposed by Davis and Haltiwanger (1992) for measuring job reallocation, we track the dynamics of credit reallocation across Korean firms for over three decades (1980 2012). The credit − boom preceding the 1997 crisis featured a slowdown of credit reallocation. Af- ter the crisis and the associated reforms, the creditless recovery (deleveraging) masked a dramatic intensification and increased procyclicality of credit realloca- tion. The findings suggest that the crisis and the associated reforms have triggered an efficiency-enhancing increase in the fluidity of the credit market. Keywords: Credit Reallocation, Credit Growth, Financial Crises. JEL Codes: E44 ∗Raoul Minetti: Department of Economics, 486 W. Circle Drive, 110 Marshall-Adams Hall, Michi- gan State University, East Lansing, MI 48824-1038. E-mail: [email protected] . Junghwan Hyun: gre- [email protected] . We wish to thank several seminar and conference participants for their comments and suggestions. All remaining errors are ours. 1 Credit Reallocation, Deleveraging, and Financial Crises Abstract This paper studies how the process of reallocation of credit across firms behaves before and after financial crises. Applying the method- ology proposed by Davis and Haltiwanger (1992) for measuring job re- allocation, we track the dynamics of credit reallocation across Korean firms for over three decades (1980 2012). The credit boom preceding − the 1997 crisis featured a slowdown of credit reallocation. After the crisis and the associated reforms, the creditless recovery (deleveraging) masked a dramatic intensification and increased procyclicality of credit reallocation. -

Debt Overhang and Deleveraging in the US

Working Paper Series Bruno Albuquerque and Debt overhang and deleveraging Georgi Krustev in the US household sector: gauging the impact on consumption No 1843 / August 2015 Note: This Working Paper should not be reported as representing the views of the European Central Bank (ECB). The views expressed are those of the authors and do not necessarily reflect those of the ECB Abstract Using a novel dataset for the US states, this paper examines whether household debt and the protracted debt deleveraging help explain the dismal performance of US consumption since 2007 in the aftermath of the housing bubble. By separating the concepts of deleveraging and debt overhang { a flow and a stock effect { we find that excessive indebtedness exerted a meaningful drag on consumption over and beyond income and wealth effects. The overall impact, however, is modest { around one-sixth of the slowdown in consumption between 2000-06 and 2007-12 { and mostly driven by states with particularly large imbalances in their household sector. This might be indicative of non-linearities, whereby indebtedness begins to bite only when misalignments from sustainable debt dynamics become excessive. Keywords: Household deleveraging, Debt overhang, Consumption function, Housing wealth. JEL Classification: C13, C23, C52, D12, H31 ECB Working Paper 1843, August 2015 1 Non-technical summary The leveraging and subsequent deleveraging cycle in the US household sector played a significant role in affecting the performance of economic activity in the years around the Great Recession. A growing body of theoretical and empirical studies have thus focused on explaining to what extent and through which channels the excessive build-up of debt and the deleveraging phase might have contributed to depress economic activity and consumption growth. -

When Credit Bites Back: Leverage, Business Cycles, and Crises∗

February 2012 When Credit Bites Back: Leverage, Business Cycles, and Crises∗ Abstract This paper studies the role of leverage in the business cycle. Based on a study of nearly 200 recession episodes in 14 advanced countries between 1870 and 2008, we document a new stylized fact of the modern business cycle: more credit-intensive booms tend to be followed by deeper recessions and slower recoveries. We find a close relationship between the rate of credit growth relative to GDP in the expansion phase and the severity of the subsequent recession. We use local projection methods to study how leverage impacts the behavior of key macroeconomic variables such as investment, lending, interest rates, and inflation. The effects of leverage are particularly pronounced in recessions that coincide with financial crises, but are also distinctly present in normal cycles. The stylized facts we uncover lend support to the idea that financial factors play an important role in the modern business cycle. Keywords: leverage, financial crises, business cycles, local projections. JEL Codes: C14, C52, E51, F32, F42, N10, N20. Oscar` Jord`a(Federal Reserve Bank of San Francisco and University of California, Davis) e-mail: [email protected]; [email protected] Moritz Schularick (Free University of Berlin) e-mail: [email protected] Alan M. Taylor (University of Virginia, NBER, and CEPR) e-mail: [email protected] ∗The authors gratefully acknowledge financial support through a grant of the Institute for New Economic Thinking (INET) administered by the University of Virginia. Part of this research was undertaken when Schularick was a visitor at the Economics Department, Stern School of Business, New York University. -

Why Was Japan Hit So Hard by the Global Financial Crisis?

ADBI Working Paper Series Why was Japan Hit So Hard by the Global Financial Crisis? Masahiro Kawai and Shinji Takagi No. 153 October 2009 Asian Development Bank Institute ADBI Working Paper 153 Kawai and Takagi Masahiro Kawai is the dean of the Asian Development Bank Institute. Shinji Takagi is a professor, Graduate School of Economics, Osaka University, Osaka, Japan. This is a revised version of the paper presented at the Samuel Hsieh Memorial Conference, hosted by the Chung-Hua Institution for Economic Research, Taipei,China 9–10 July 2009. The authors are thankful to Ainslie Smith for her editorial work. The views expressed in this paper are the views of the authors and do not necessarily reflect the views or policies of ADBI, the Asian Development Bank (ADB), its Board of Directors, or the governments they represent. ADBI does not guarantee the accuracy of the data included in this paper and accepts no responsibility for any consequences of their use. Terminology used may not necessarily be consistent with ADB official terms. The Working Paper series is a continuation of the formerly named Discussion Paper series; the numbering of the papers continued without interruption or change. ADBI’s working papers reflect initial ideas on a topic and are posted online for discussion. ADBI encourages readers to post their comments on the main page for each working paper (given in the citation below). Some working papers may develop into other forms of publication. Suggested citation: Kawai, M., and S. Takagi. 2009. Why was Japan Hit So Hard by the Global Financial Crisis? ADBI Working Paper 153. -

Liquidity, Part 2: Debt, Panics, and Flight to Quality: Lecture 6

14.09: Financial Crises Lecture 6: Collateralized Debt and Information Based Panics Alp Simsek Alp Simsek () Lecture Notes 1 Revisiting runs: Is Diamond-Dybvig the whole story? Diamond-Dybvig provides a plausible account of runs in history, and after some relabeling, a contributing factor to the subprime crisis. However, there is reason to think that it might not be the whole story. Recently (and in history), much debt has been collateralized. An example of collateralized debt is repo (sale-repurchase agreement)... Alp Simsek () Lecture Notes 2 Roadmap 1 Understanding the run on the collateralized debt 2 Information insensitivity of collateralized debt 3 Information-based panics and the leverage cycle 4 Revisiting the run(s) on Bear Stearns Alp Simsek () Lecture Notes 3 Alp Simsek () Lecture Notes 4 What is repo? Repo is effectively a collateralized loan. B (the borrower/the bank), receives some money by temporarily giving collateral such as treasuries, MBSs etc to F (the financier). B pays back the loan with interest and reclaims the collateral. The loan is often short term, e.g., one day, but could also be longer. (The deal is technically structured as an initial sale of the collateral and a right to repurchase with a prespecified price that refiects the interest rate– hence the name.) Alp Simsek () Lecture Notes 5 Repo haircuts As we discussed earlier, the loan usually has a haircut or margin. Recall B could borrow ρ from the Fs by using 1 dollar of the asset as collateral. The difference, 1 ρ, would be the REPO haircut. − Alp Simsek () Lecture Notes 6 Courtesy of the American Economics Association. -

Procyclical Leverage and Value-At-Risk

Procyclical Leverage and Value-at-Risk Tobias Adrian Federal Reserve Bank of New York Hyun Song Shin Downloaded from https://academic.oup.com/rfs/article/27/2/373/1580738 by Bank for International Settlements user on 21 March 2021 Princeton University The availability of credit varies over the business cycle through shifts in the leverage of financial intermediaries. Empirically, we find that intermediary leverage is negatively aligned with the banks’ Value-at-Risk (VaR). Motivated by the evidence, we explore a contracting model that captures the observed features. Under general conditions on the outcome distribution given by extreme value theory (EVT), intermediaries maintain a constant probability of default to shifts in the outcome distribution, implying substantial deleveraging during downturns. For some parameter values, we can solve the model explicitly, thereby endogenizing the VaR threshold probability from the contracting problem. (JEL G01, G23, G32) The availability of credit and how credit varies over the business cycle have been subjects of keen interest, especially in the wake of the financial crisis. Some cyclical variation in total lending is to be expected, even in a frictionless world where the conditions of the Modigliani and Miller (1958) theorem hold. There are more positive net present value (NPV) projects that need funding when the economy is strong than when the economy is weak. Therefore, we should expect total credit to increase during the upswing and decline in the downswing. The debate about procyclicality of the financial system is therefore more subtle. The question is whether the fluctuations in lending are larger than would be justified by changes in the incidence of positive NPV projects. -

Leverage Cycle John Geanakoplos

Leverage Cycle John Geanakoplos Zhe Li SUFE Zhe Li (SUFE) Leverage Cycle 1 / 78 Leverage A homeowner takes a loan using a house as collateral, he negotiates: (a) interest rate (b) how much he can borrow Example house costs $100, loan $80, he pays $20 in cash margin or haircut: 20% loan to value: 80/100 = 80% collateral rate: 100/80 = 1.25 leverage: 1/margin = 5 Zhe Li (SUFE) Leverage Cycle 2 / 78 Motivation In times of crisis: Interest rate (main policy instrument) Collateral rate (equivalently margins, leverage) E¤ectiveness of two instruments: During a crisis, leverage can fall by 50% overnight, and by more over a few days or months A homeowner who brought a house in 2007 by taking out a subprime mortgate with only 5% down payment cannot take out a similar loan in 2009 without putting 30% The odds are great that he won’thave the cash to do it, and reducing the interest rate by 1 or 2% won’tchange his ability to act Zhe Li (SUFE) Leverage Cycle 3 / 78 Heterogeneous beliefs For many assets there is a class of buyer for whom the asset is more valuable than it is for the rest of the public (standard economic theory, in contrast, assumes that asset prices re‡ect some fundamental value). These buyers are willing to pay more, perhaps because they are more sophisticated and know better how to hedge their exposure to the assets, or they are more risk tolerant, or they simply like the assets more Zhe Li (SUFE) Leverage Cycle 4 / 78 Distribution of wealth If the optimistic buyers can get their hands on more money through more highly leveraged borrowing (that is, getting a loan with less collateral), they will spend it on the assets and drive those prices up If they lose wealth, or lose the ability to borrow, they will buy less, so the asset will fall into more pessimistic hands and be valued less Zhe Li (SUFE) Leverage Cycle 5 / 78 Leverage cycle: meaning De…nition In the absence of intervention, leverage becomes too high in boom times, and too low in bad times (leverage is procyclical).