Save Fiscal Policy in a Balance Sheet Recession

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Fortnightly Market Wrap up Spring Week Edition 31 March 2013

March 31, 2013 WIC Market Wrap-Up Fortnightly Market Wrap Up Spring Week Edition 31 March 2013 Warwick Investment Club Research Team 1 March 31, 2013 WIC Market Wrap-Up The WIC Market Wrap-Up The WIC Market Wrap-Up is published fortnightly by the Warwick Finance Societies’ (WFS) Warwick Investment Club (WIC) Research Team. Receive the Wrap Up via email newsletter by joining the WFS, or look out for archived issues on www.wfsocieties.com. In this Week’s Issue Editorial – page 3 Italy – page 7 Quantitative Easing and the Italian Political Debacle – Balance Sheet Recession Where we stand now By Daryl Chia, Editor-in-Chief By Marco Ross, Co-Editor US Equities – page 4 Renewables – page 8 Spring in the Step of the Dow Has the Sun Set for the Solar Jones and S&P 500 Industry? By Will Caffrey, Analyst By Richard Low, Analyst The Japanese Economy – page 5 Technology – page 9 Manufacturing – Bad signs for Blackberries – Back in season? the Japanese economy By John Peter Ong, Analyst By Eleanor Gaffney, Analyst Research Team Application Essay – page 10 Cyprus – page 6 The Eurozone Crisis The Significance of the Bailout By Jonathan Denham Deal Research Team Application Essay – page 11 By Melson Chun, Analyst The 2008 Global Financial Crisis By Zak Simpson Warwick Investment Club Research Team 2 March 31, 2013 WIC Market Wrap-Up Editorial nominal line under assets and reduced liquidity-related tail risks, but have not translated to a solution that can Quantitative Easing and the bring about robust long term growth. Balance Sheet Recession Alas, the asset reflation and wealth effect of QE is meaningful only in the short term. -

Monetary Policy and the Long Boom

NOVEMBER/DECEMBER1998 John B. Taylor is a professor of economics at Stanford University. The article that follows is a reprint of The Homer Jones Lecture delivered at Southern Illinois University-Edwardsville on April 16, 1998. Kent Koch provided research assistance. this lecture. This month (April 1998) the Monetary Policy United States economy celebrates seven years of economic expansion. By definition and The Long an economic expansion is the period between recessions; that is, a period of con- Boom tinued growth without a recession. The last recession in the United States ended in April 1991, so as of this April we have had seven John B. Taylor years of expansion and we are still going. This current expansion is a record breaker: regret that I never had the opportunity to to be exact it is the second longest peacetime work or study with Homer Jones. But I expansion in American history. Iknow people who worked and studied with But what is more unusual is that this him, and I have enjoyed talking with them and current expansion was preceded by the reading about their recollections of Homer first longest peacetime expansion in Amer- Jones. What is most striking to me, of all that ican history. That expansion began in has been said and written about Homer Jones, November 1982 and continued through is his incessant striving to learn more about August 1990. It lasted seven years and economics and his use of rigorous economic eight months. Although the 1980s expansion research to improve the practical operation of was the first longest peacetime expansion in economic policy. -

Deleveraging and the Aftermath of Overexpansion

May 28th, 2009 Jeffrey Owen Herzog Deleveraging and the aftermath of overexpansion [email protected] O The deleveraging process for commercial banks is likely to last years and overshoot compared to fundamentals Banking System Asset and Leverage Growth O A strong procyclical correlation exists between asset growth and Nominal Values, 1934-2008 leverage growth over the past 75 years 25% O At the level of the firm, boom times generate decreasing 20% 1942 collateralization rates and increasing average loan sizes 15% O Given two-year loan losses of $1.1tr and leverage declines of -5% 10% 2008 to -7.5%, we expect deleveraging to curtail commercial bank 5% credit by $646bn and $687bn per year for 2009-2010 0% -5% Trends in deleveraging and commercial banking over time Leverage Growth -10% 2004 -15% 1946 Deleveraging is the process whereby commercial banks reduce their ratio of -20% assets to equity capital, thus bringing down their aggregate exposure to the 0% 5% -5% 10% 15% 20% 25% 30% economy. Many commentators point to this process as an eventual destination -10% Asset Growth for the US commercial banking system, but few have described where or how Source: FDIC we arrive at a more deleveraged commercial banking system. Commercial Bank Assets and Equity Adjusted for Inflation by CPI, $tr Over the past seventy years, the commercial banking sector’s aggregate 0.6 6 balance sheet has demonstrated a strong positive correlation between leverage and asset growth. For the banking industry, 2004 was an 0.5 5 S&L Crisis, 1989-1991 exceptionally unusual year, with equity increasing yoy by 22%. -

Understanding the Global Macroeconomic Challenges

On time, stocks and flows: Understanding the global macroeconomic challenges Claudio Borio Bank for International Settlements Abstract Five years after the financial crisis, the global economy remains unbalanced and many of the advanced countries are still struggling to return to robust, sustainable growth. Taking a historical perspective, I argue that this predicament reflects a failure to adjust to profound changes in the economic landscape, which have given rise to the (re-)emergence of major financial booms and busts. The economic developments that really matter now take much longer to unfold – economic time has slowed down relative to calendar time – and yet the planning horizons of economic agents have shortened. The key problems arise from the cumulative effects of past decisions on stocks, and yet these effects are treated as short- term flow issues. The risk is that instability will become entrenched in the system. Policy needs to adjust. JEL classification: E30, E44, E50, G10, G20, G28, H30, H50. Keywords: short horizons, debt, financial cycle, banking crises, balance sheet recessions. 2 Contents Introduction ............................................................................................................................................... 1 I. The broad canvas .......................................................................................................................... 3 Stylised facts: an economic historian’s perspective ....................................................................... 3 Stylised -

UNIVERSITY of CALIFORNIA DEPARTMENT of ECONOMICS LECTURE 25 BALANCE SHEET EFFECTS APRIL 24, 2018 A. Aggregate Demand Or Potentia

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 25 BALANCE SHEET EFFECTS APRIL 24, 2018 I. INTRODUCTION IV. HOUSEHOLD BALANCE SHEETS AND THE GREAT RECESSION A. The housing boom II. KOO’S DIAGNOSIS OF JAPAN’S POOR MACROECONOMIC 1. Mian and Sufi’s hypotheses PERFORMANCE 2. The role of economic fundamentals in house price A. Aggregate demand or potential output? growth B. Credit supply or credit demand? 3. The direction of causation between house prices and C. A “balance sheet” recession credit growth 4. Why did rising house prices raise consumption so III. KOO’S ANALYSIS OF A BALANCE SHEET RECESSION much? A. Koo’s analysis of a balance sheet recession in an IS-MP B. The Great Recession and slow recovery framework 1. Mian and Sufi’s hypothesis B. Is monetary policy effective in Koo’s model of a balance 2. Evidence sheet recession? 3, Discussion C. Is fiscal policy effective in Koo’s model of a balance sheet recession? V. POSSIBLE IMPLICATIONS FOR POLICY D. Is the zero lower bound important in Koo’s model of a balance sheet recession? E. Koo’s evidence F. A balance sheet recession and “debt-deflation” Economics 134 David Romer Spring 2018 LECTURE 25 Balance Sheet Effects April 25, 2018 Final Exam – Basics • Mechanics: • Monday, May 7, 3–6 P.M., 2050 VLSB. • Students with DSP accommodations: You should have received an email from me today. If you did not, please let me know. • Coverage: Whole semester. But: • There will be more emphasis on the material after the midterm. -

Monetary Policy and Economic Developments 3

Monetary Policy and Economic Developments 3 Monetary Policy and the Economic Outlook The economic expansion in the United eventually lead to a pickup in the pace States gathered strength during 2003 of the expansion, the timing and extent while price inflation remained quite low. of the improvement were uncertain. At the beginning of the year, uncertain- During the spring, the rally that occurred ties about the economic outlook and in equity markets when the war-related about the prospects of war in Iraq appar- uncertainties lifted suggested that mar- ently weighed on spending decisions ket participants viewed the economic and extended the period of subpar eco- outlook as generally positive. By then, nomic performance that had begun more the restraints imparted by the earlier than two years earlier. However, with sharp decline in equity prices, the the support of stimulative monetary and retrenchment in capital spending, and fiscal policies, the nation’s economy lapses in corporate governance were weathered that period of heightened receding. As the price of crude oil uncertainty to post a marked accelera- dropped back and consumer confidence tion in economic activity over the sec- rebounded last spring, household spend- ond half of 2003. Still, slack in resource ing seemed to be rising once again at utilization remained substantial, unit a moderate rate. Businesses, however, labor costs continued to decline as remained cautious; although the deterio- productivity surged, and core inflation ration in the labor market showed signs moved lower. The performance of the of abating, private payroll employment economy last year further bolstered the was still declining, and capital spending case that the faster rate of increase in continued to be weak. -

The Deleveraging of U.S. Households: Credit Card Debt Over the Lifecycle

2016 n Number 11 ECONOMIC Synopses The Deleveraging of U.S. Households: Credit Card Debt over the Lifecycle Helu Jiang, Technical Research Associate Juan M. Sanchez, Research Officer and Economist ggertsson and Krugman (2012) contend that “if there Total Credit Card Debt is a single word that appears most frequently in dis - $ Billions cussions of the economic problems now afflicting E 900 both the United States and Europe, that word is surely 858 865 debt.” These authors and others offer theoretical models 850 that present the debt phenomenon as follows: The econo my 800 788 792 756 is populated by impatient and patient individuals. Impatient 744 751 750 individuals borrow as much as possible, up to a debt limit. 718 When the debt limit suddenly tightens, impatient individ - 700 683 665 656 648 uals must cut expenditures to pay their debt, depressing 650 aggregate demand and generating debt-driven slumps. Such 600 a reduction in debt is called deleveraging . 2004 2005 2006 2007 2008 2009 2010 20 11 2012 2013 2014 2015 SOURCE: Federal Reserve Bank of New York Consumer Credit Panel/Equifax. Individuals younger than 46 deleveraged the most after the Share of the Change in Total Credit Card Debt financial crisis of 2008. by Age Group Percent 25 21 20 The evolution of total credit card debt around the finan - 14 14 14 15 13 11 cial crisis of 2008 appears consistent with that sequence: 8 10 6 Credit card debt increased quickly before the financial cri sis 5 1 3 3 0 and then fell for six years after that episode. -

Economic Review Federal Reserve Bank of San Francisco

Economic Review Federal Reserve Bank of San Francisco 1993 Number 3 John P. Judd and Using a Nominal GDP Rule to Uuide Brian Motley Discretionary Monetary Policy Ramon Moreno and Money, Interest Rates and Economic Activity: Sun Bae Kim Stylized Facts for Japan John P. Judd and The Output-Inflation Trade-off in the United Jack H. Beebe States: Has It Changed Since the Late 1970s? Timothy Cogley Adapting to Instability in Money Demand: Forecasting Money Growth with a Time-Varying Parameter Model Ronald H. Schmidt and Water Policy in California and Israel Steven E. Plaut The Output-Inflation Trade-off in the United States: Has It Changed Since the Late 1970s? Since late 1979, the Federal Reserve has pursued disinfla tionary monetary policies that can be characterized as occurring in two stages. First, in 1979-1981 the Fed suc cessfully reduced inflation from double-digit to moderate John P. Judd and Jack H. Beebe rates of around 3Y2 percent in 1983-1985. Beginning in 1988, the Fed began explicitly stating that it intended to The authors are Vice President and Associate Director of achieve a second period of disinflation, gradually moving Research, and Senior Vice President and Director of Re the inflation rate from a moderate level of about 4 percent search, respectively. They would like to thank Timothy at that time to very low levels ("near" price stability) over a Cogley, Frederick Furlong, Ramon Moreno, John Roberts, number of years. In 1992, CPI inflation was 3 percent, and Bharat Trehan for helpful suggestions on an earlier before dropping to about 212 percent in the first ten months draft, and Sean Kelly and,Andrew Biehl for research of 1993, indicating modest progress toward this goal. -

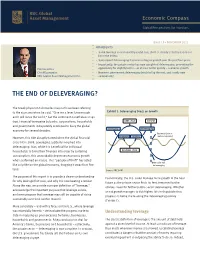

The End of Deleveraging?

Economic Compass Global Perspectives for Investors Issue 19 • NOVEMBER 2012 HIGHLIGHTS › Some leverage is economically useful, but, the U.S. clearly took this notion too far in the 2000s. › Subsequent deleveraging has been a drag on growth over the past four years. › Importantly, the private sector has now completed deleveraging, presenting the Eric Lascelles opportunity for slightly better – or at least better quality – economic growth. Chief Economist › However, government deleveraging tends to lag the rest, and is only now RBC Global Asset Management Inc. commencing. THE END OF DELEVERAGING? The Greek physicist Archimedes may not have been referring to the economy when he said, “Give me a lever long enough Exhibit 1: Deleveraging Drags on Growth and I will move the world,” but the sentiment nonetheless rings true. Financial leveraging by banks, corporations, households DEBT CYCLE PRESENT and governments indisputably combined to buoy the global Leveraging Deleveraging economy for several decades. Business Cycle in However, this tide abruptly turned when the global financial Downswing Upswing cautious upswing crisis hit in 2008. Leveraging suddenly morphed into deleveraging. Alas, while it is beneficial for individual households to bring their finances into order by curtailing BUSINESS CYCLE consumption, this unavoidably depresses economic growth when performed en masse. This “paradox of thrift” has acted Debt Cycle still like a riptide on the global economy, dragging it away from firm deleveraging land. Source: RBC GAM The purpose of this report is to provide a clearer understanding Economically, the U.S. could manage more growth in the near for why leverage first rose, and why it is now beating a retreat. -

Do We Really Know That Oil Caused the Great Stagflation? a Monetary Alternative Author(S): Robert B

Do We Really Know That Oil Caused the Great Stagflation? A Monetary Alternative Author(s): Robert B. Barsky and Lutz Kilian Source: NBER Macroeconomics Annual, Vol. 16, (2001), pp. 137-183 Published by: The University of Chicago Press Stable URL: http://www.jstor.org/stable/3585363 Accessed: 01/07/2008 10:43 Your use of the JSTOR archive indicates your acceptance of JSTOR's Terms and Conditions of Use, available at http://www.jstor.org/page/info/about/policies/terms.jsp. JSTOR's Terms and Conditions of Use provides, in part, that unless you have obtained prior permission, you may not download an entire issue of a journal or multiple copies of articles, and you may use content in the JSTOR archive only for your personal, non-commercial use. Please contact the publisher regarding any further use of this work. Publisher contact information may be obtained at http://www.jstor.org/action/showPublisher?publisherCode=ucpress. Each copy of any part of a JSTOR transmission must contain the same copyright notice that appears on the screen or printed page of such transmission. JSTOR is a not-for-profit organization founded in 1995 to build trusted digital archives for scholarship. We work with the scholarly community to preserve their work and the materials they rely upon, and to build a common research platform that promotes the discovery and use of these resources. For more information about JSTOR, please contact [email protected]. http://www.jstor.org RobertB. Barskyand Lutz Kilian UNIVERSITY OF MICHIGAN AND NBER; AND UNIVERSITY OF MICHIGAN, EUROPEAN CENTRAL BANK, AND CEPR Do We Really Know that Oil Caused the Great Stagflation? A Monetary Alternative 1. -

Credit Reallocation, Deleveraging, and Financial Crises

Credit Reallocation, Deleveraging, and Financial Crises Junghwan Hyun Raoul Minetti∗ Hiroshima University Michigan State University Abstract This paper studies how the process of reallocation of credit across firms behaves before and after financial crises. Applying the methodology proposed by Davis and Haltiwanger (1992) for measuring job reallocation, we track the dynamics of credit reallocation across Korean firms for over three decades (1980 2012). The credit − boom preceding the 1997 crisis featured a slowdown of credit reallocation. Af- ter the crisis and the associated reforms, the creditless recovery (deleveraging) masked a dramatic intensification and increased procyclicality of credit realloca- tion. The findings suggest that the crisis and the associated reforms have triggered an efficiency-enhancing increase in the fluidity of the credit market. Keywords: Credit Reallocation, Credit Growth, Financial Crises. JEL Codes: E44 ∗Raoul Minetti: Department of Economics, 486 W. Circle Drive, 110 Marshall-Adams Hall, Michi- gan State University, East Lansing, MI 48824-1038. E-mail: [email protected] . Junghwan Hyun: gre- [email protected] . We wish to thank several seminar and conference participants for their comments and suggestions. All remaining errors are ours. 1 Credit Reallocation, Deleveraging, and Financial Crises Abstract This paper studies how the process of reallocation of credit across firms behaves before and after financial crises. Applying the method- ology proposed by Davis and Haltiwanger (1992) for measuring job re- allocation, we track the dynamics of credit reallocation across Korean firms for over three decades (1980 2012). The credit boom preceding − the 1997 crisis featured a slowdown of credit reallocation. After the crisis and the associated reforms, the creditless recovery (deleveraging) masked a dramatic intensification and increased procyclicality of credit reallocation. -

Debt Overhang and Deleveraging in the US

Working Paper Series Bruno Albuquerque and Debt overhang and deleveraging Georgi Krustev in the US household sector: gauging the impact on consumption No 1843 / August 2015 Note: This Working Paper should not be reported as representing the views of the European Central Bank (ECB). The views expressed are those of the authors and do not necessarily reflect those of the ECB Abstract Using a novel dataset for the US states, this paper examines whether household debt and the protracted debt deleveraging help explain the dismal performance of US consumption since 2007 in the aftermath of the housing bubble. By separating the concepts of deleveraging and debt overhang { a flow and a stock effect { we find that excessive indebtedness exerted a meaningful drag on consumption over and beyond income and wealth effects. The overall impact, however, is modest { around one-sixth of the slowdown in consumption between 2000-06 and 2007-12 { and mostly driven by states with particularly large imbalances in their household sector. This might be indicative of non-linearities, whereby indebtedness begins to bite only when misalignments from sustainable debt dynamics become excessive. Keywords: Household deleveraging, Debt overhang, Consumption function, Housing wealth. JEL Classification: C13, C23, C52, D12, H31 ECB Working Paper 1843, August 2015 1 Non-technical summary The leveraging and subsequent deleveraging cycle in the US household sector played a significant role in affecting the performance of economic activity in the years around the Great Recession. A growing body of theoretical and empirical studies have thus focused on explaining to what extent and through which channels the excessive build-up of debt and the deleveraging phase might have contributed to depress economic activity and consumption growth.