COVID-19 Payment Deferral: Escrow Account Common Inquiries

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Account Guidelines for Managers and Delegates

ACCOUNT/BUDGET GENERAL OPERATING PRINCIPLES for IU SOUTHEAST ACCOUNT MANAGERS / ACCOUNT DELEGATES The Fiscal Year runs from July 1 – June 30. Operating budgets are distributed in June/July. Accounts may not exceed their budgeted amounts within the fiscal year. Account managers will be required to develop a plan to bring the account in balance before the closing of the fiscal year or to carry forward the over- expenditures to the next fiscal year. Allocated funds do not carry forward to the next fiscal year. Unused funds are forfeited. Allocated funds should be spent to or close to zero. Every department has an organization code (contact Melissa Hill in Accounting Services, #2359). Examples: Student Affairs (SSER), Athletics (ATHL). A budget binder or file should be established for each account. All budget documents should be kept for the current fiscal year within the budget binder or file. Receipts/documentation must be kept for all expenditures. All budget documentation must be kept on file for seven years. Use of funds must conform to IU Financial Policies found on web site: http://www.indiana.edu/%7Epolicies/ The Financial Information System (FIS) is used for account transactions and account monitoring. Passwords and access are needed (contact IT or Accounting Services). If FIS training is needed, contact Melissa Hill in Accounting Services (#2359). Monthly operating statements should be printed from FIS (available first of month—notification comes by email) and account transactions should be reconciled by the account manager or delegate on a monthly basis at minimum. Each expenditure must be accounted for with receipts or other appropriate documentation. -

Good Faith Estimate (GFE)

OMB Approval No. 2502-0265 Good Faith Estimate (GFE) Name of Originator Borrower Originator Property Address Address Originator Phone Number Originator Email Date of GFE Purpose This GFE gives you an estimate of your settlement charges and loan terms if you are approved for this loan. For more information, see HUD’s Special Information Booklet on settlement charges, your Truth-in-Lending Disclosures, and other consumer information at www.hud.gov/respa. If you decide you would like to proceed with this loan, contact us. Shopping for Only you can shop for the best loan for you. Compare this GFE with other loan offers, so you can find your loan the best loan. Use the shopping chart on page 3 to compare all the offers you receive. Important dates 1. The interest rate for this GFE is available through . After this time, the interest rate, some of your loan Origination Charges, and the monthly payment shown below can change until you lock your interest rate. 2. This estimate for all other settlement charges is available through . 3. After you lock your interest rate, you must go to settlement within days (your rate lock period) to receive the locked interest rate. 4. You must lock the interest rate at least days before settlement. Summary of Your initial loan amount is $ your loan Your loan term is years Your initial interest rate is % Your initial monthly amount owed for principal, interest, and any mortgage insurance is $ per month Can your interest rate rise? c No c Yes, it can rise to a maximum of %. -

Chapter 3: Escrow, Taxes, and Insurance

HB-2-3550 CHAPTER 3: ESCROW, TAXES, AND INSURANCE 3.1 INTRODUCTION To protect the Agency’s interest in the security property, the Servicing and Asset Management Office (Servicing Office) must ensure that real estate taxes and any other local assessments are paid and that the property remains adequately insured. To ensure that funds are available for these purposes, the Agency requires most borrowers who receive new loans to deposit funds to an escrow account. Borrowers who are not required to establish an escrow account may do so voluntarily. If an escrow account has been established, payments for insurance, taxes, and other assessments are made by the Agency. If an escrow account has not been established, the borrower is responsible for making timely payments. Section 1 of this chapter describes basic requirements for paying taxes and maintaining insurance coverage; Section 2 provides procedure for establishing and maintaining the escrow account; and Section 3 discusses procedures for addressing insured and uninsured losses to the security property. SECTION 1: TAX AND INSURANCE REQUIREMENTS [7 CFR 3550.60 and 3550.61] 3.2 TAXES AND OTHER LOCAL ASSESSMENTS The Agency contracts with a tax service to secure tax information for all borrowers. The tax service obtains tax bills due for payment, determines the optimal time to pay the taxes in order to take advantage of any discounts, and provides delinquent tax status on the portfolio. A. Tax Service Fee All borrowers are charged a tax service fee. Borrowers who obtain a subsequent loan are not required to pay a second tax service fee. -

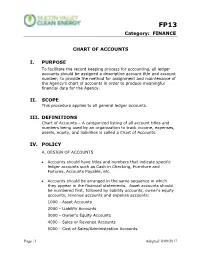

G&A101 Chart of Accounts

FP13 Category: FINANCE CHART OF ACCOUNTS I. PURPOSE To facilitate the record keeping process for accounting, all ledger accounts should be assigned a descriptive account title and account number; to provide the method for assignment and maintenance of the Agency’s chart of accounts in order to produce meaningful financial data for the Agency. II. SCOPE This procedure applies to all general ledger accounts. III. DEFINITIONS Chart of Accounts – A categorized listing of all account titles and numbers being used by an organization to track income, expenses, assets, equity, and liabilities is called a Chart of Accounts. IV. POLICY A. DESIGN OF ACCOUNTS • Accounts should have titles and numbers that indicate specific ledger accounts such as Cash in Checking, Furniture and Fixtures, Accounts Payable, etc. • Accounts should be arranged in the same sequence in which they appear in the financial statements. Asset accounts should be numbered first, followed by liability accounts, owner’s equity accounts, revenue accounts and expense accounts: 1000 - Asset Accounts 2000 - Liability Accounts 3000 - Owner’s Equity Accounts 4000 - Sales or Revenue Accounts 5000 - Cost of Sales/Administration Accounts Page | 1 Adopted: 8/09/2017 FP13 Category: FINANCE 6000 - Debt Service Accounts 8000 - Other Accounts B. DESCRIPTION OF ACCOUNTS • Each account should be given a short title description that is brief but will allow the reader to quickly ascertain the purpose of the account. • For training and consistent transaction coding, as well as to help other non-accounting managers understand why something is recorded as it is, each account should be defined. Definitions should be concise and meaningful. -

TILA Higher-Priced Mortgage Loans (HPML) Escrow Rule

March 2016 TILA Higher-Priced Mortgage Loans (HPML) Escrow Rule Small entity compliance guide Version Log The Bureau updates this guide on a periodic basis to reflect finalized amendments and clarifications to the rule which impact guide content. Below is a version log noting the history of this document and notable rule changes: Date Version Rule Changes March 28, 1.2 Exemption for Small Creditors that Operate in a Rural 2016 or Underserved Area. The September 2015 Final Rule amends the eligibility criteria for small creditors operating in rural or underserved areas for exemption from the requirement to establish an escrow account for higher-priced mortgage loans (HPMLs). The March 2016 Interim Final Rule further amends the definition of rural areas and replaces the requirement that a small creditor operate predominantly in rural and underserved areas to be eligible for the escrow exemption with a requirement that a small creditor operate in a rural or underserved area. The revised rural-or-underserved test extends eligibility to small creditors that originated at least one covered loan secured by a first lien on a property located in a rural or underserved area in the preceding calendar year. It also amends the conditions for exempting small creditors from the requirement to maintain escrows so that an otherwise eligible small creditor will be able to rely on the exemption if it and its affiliates continue to maintain escrows established for first-lien HPMLs if the application for the HPML was received between April 1, 1 2010 and May 1, 2016. (See “What are the exemptions to the TILA HPML Escrow Rule?”on page 13 and “What are the loan volume and size requirements to qualify for the exemption for creditors operating in a rural or underserved area?” on page 14. -

When to Debit and Credit in Accounting

When to Debit and Credit in Accounting Journal entries show a firm’s transactions throughout a period of time; for example, when a company purchases supplies a journal entry will show the amount of supplies bought and money spent. According to the practice of double-entry accounting, every journal entry must: • Include at least two distinct accounts with at least one debit and one credit. • Have the total monetary amount of debits equal to the total monetary amount of credits. • Be consistent with the accounting equation, Assets = Liabilities + Equity. (Wild, Shaw, and Chiappetta, 55) An asset is loosely defined as a resource with economic value that a particular firm has, and includes accounts such as cash, accounts receivable, and office supplies. Liabilities are the debts and obligations a company accumulates in operating the business; it includes accounts such as accounts payable, wages payable, and interest payable. Equity represents the amount of ownership in an asset that is not financed through debt. Equity begins with the owner’s capital, which are personal investments of assets by the owner, and grows as revenues are accrued over the course of business operations. Equity shrinks when the owner withdrawals capital and/or expenses are incurred. Thus the accounting equation, Assets = Liabilities + Equity, can be roughly translated as, “things we have are backed by things we owe and things we own.” A chart of accounts, which list commonly used accounts and their type, is included as an appendix in most accounting text books. The following diagram depicts the accounting equation such that equity is broken down into the component accounts of Capital, Withdrawals, Revenue, and Expenses, and illustrates how each type of account reacts to debits and credits. -

Basic Financial Accounting Review

4259_Jagels_01.qxd 4/11/03 5:01 PM Page 1 CHAPTER 1 BASIC FINANCIAL ACCOUNTING REVIEW INTRODUCTION Every profit or nonprofit business en- transactions, to add, subtract, summa- tity requires a reliable internal system rize, and check for errors. The rapid of accountability. A business account- advancement of computer technology ing system provides this accountabil- has increased operating speed, data ity by recording all activities regard- storage, and reliability accompanied ing the creation of monetary inflows by a significant cost reduction. Inex- of revenue and monetary outflows pensive microcomputers and account- of expenses resulting from operating ing software programs have advanced activities. The accounting system to the point where all of the records provides the financial information posting, calculations, error checking, needed to evaluate the effectiveness and financial reports are provided of current and past operations. In ad- quickly by the computerized system. dition, the accounting system main- The efficiency and cost-effectiveness tains data required to present reports of supporting computer software al- showing the status of asset resources, lows management to maintain direct creditor liabilities, and ownership eq- personal control of the accounting uities of the business entity. system. In the past, much of the work re- To effectively understand con- quired to maintain an effective ac- cepts and analysis techniques dis- counting system required extensive cussed within this text, it is essential individual manual effort that was te- that the reader have a conceptual as dious, aggravating, and time consum- well as a practical understanding ing. Such systems relied on individ- of accounting fundamentals. This ual effort to continually record chapter reviews basic accounting 4259_Jagels_01.qxd 4/11/03 5:01 PM Page 2 2 CHAPTER 1 BASIC FINANCIAL ACCOUNTING REVIEW principles, concepts, conventions, and has taken an introductory accounting practices. -

GA-505 Chart of Accounts Policy Prepared By: Ken Johnston Approved By: Brian Laffey

GA-505 Chart of Accounts Policy Prepared By: Ken Johnston Approved By: Brian Laffey Effective Date: 06/01/2010 Purpose The chart of accounts is structured to ensure the Controller’s Office can manage the stewardship of the university’s funds, produce financial statements per Generally Accepted Accounting Principles (GAAP) and Financial Accounting Standards (FASB) and federal and non-federal funding agency regulations. Policy The chart of accounts is a listing of elements in the university’s financial system using numeric characters to designate the transactions that comprise the Balance Sheet (Assets, Liabilities and Net Assets) and Income Statement (Revenue and Expenses). Definitions The university’s chart of accounts consists of four segments totaling 18 digits. Each segment has a numerical value and a text description. These segments provide the organizing framework for budgeting, recording, and reporting on all financial transactions. The four segments are referred to as the Fund, Organization, Account and Program or commonly referred to as the FOAP. The FOAP string is required to post to the operating ledger while only the fund and account is required to post to the general ledger. 1. The first segment (six digits) is the Fund. The Fund element is used to specify the funding source. The fund is also tied to a fund type which allows more consolidated reporting. 2. The second segment (four digits) is the Organization. The Organization identifies the unit that is responsible for the financial activity captured within the code. PI Org refers to organizations set up based on the principal investigator of the grant. 3. -

Good Faith Estimate (GFE)

OMB Approval No. 2502-0265 Good Faith Estimate (GFE) Name of Originator Borrower Originator Property Address Address Originator Phone Number Originator Email Date of GFE Purpose This GFE gives you an estimate of your settlement charges and loan terms if you are approved for this loan. For more information, see HUD’s Special Information Booklet on settlement charges, your Truth-in-Lending Disclosures, and other consumer information at www.hud.gov/respa. If you decide you would like to proceed with this loan, contact us. Shopping for Only you can shop for the best loan for you. Compare this GFE with other loan offers, so you can find your loan the best loan. Use the shopping chart on page 3 to compare all the offers you receive. Important dates 1. The interest rate for this GFE is available through . After this time, the interest rate, some of your loan Origination Charges, and the monthly payment shown below can change until you lock your interest rate. 2. This estimate for all other settlement charges is available through . 3. After you lock your interest rate, you must go to settlement within days (your rate lock period) to receive the locked interest rate. 4. You must lock the interest rate at least days before settlement. Summary of Your initial loan amount is $ your loan Your loan term is years Your initial interest rate is % Your initial monthly amount owed for principal, interest, and any mortgage insurance is $ per month Can your interest rate rise? c No c Yes, it can rise to a maximum of %. -

Refinancing and Subordination of a Housing

REFINANCING AND SUBORDINATION OF A HOUSING REHABILITATION PROGRAM LOAN (INFORMATION FOR LENDER) Units that have received a loan as part of the City of Hayward Housing Rehabilitation Program (also referred to as the Housing Conservation Program) require City written approval in order to refinance. If the refinance is approved, the City will provide your chosen Lender with an approval letter. The owner will then have to submit a Subordination request. The information provided below is meant to inform the Lender and Escrow Officer about the information the City will require while handling the refinance. It is very important that the Lender and Escrow Officer contact [email protected] for refinance requests as soon as possible in order to ensure timely close of escrow. Please note: Lender must work with a third-party escrow company unaffiliated with the Lender. This is because the City is unable to deposit City documents required for the refinance with the Lender who would be a party to the refinance transaction. SUBMITTING A REFINANCE REQUEST Lenders who have clients who wish to refinance their home should e-mail abel.mora@hayward- ca.gov. LENDER Lenders needs to provide the City with the documents below: 1. 1003 - signed by Borrowers 2. 1008 3. Credit Report 4. Loan Estimate 5. Anticipated closing date 6. Subordination request (in writing to the City of Hayward – Community Services Division) 7. Vesting for trustor, trustee, and beneficiary of new Loan as it will appear on new Deed of Trust and Note ESCROW OFFICER Escrow Officers needs to provide the City with the documents below: 1. -

The Smart Consumer's Guide to Reducing Closing Costs

The Smart Consumer’s Guide to Reducing Closing Costs When buying, selling or refinancing a home The Smart Consumer’s Guide to Reducing Closing Costs TABLE OF CONTENTS An Introduction to Closing Costs ................................................... 4 The Closing Process Begins with a Good Faith Estimate .......................................... 4 What are typical closing costs? ................................................................................ 5 I. Real Estate Broker or Agent Fee ........................................................................... 6 II. Items Payable in Connection with Loan .............................................................. 6 Application fee ............................................................................................................ 6 Loan origination charge ............................................................................................... 6 Discount “points” ......................................................................................................... 7 Wire transfer fee ......................................................................................................... 7 Appraisal fee ............................................................................................................... 7 Lender-required home inspection fee ............................................................................ 7 Termite/pest inspection ............................................................................................... 7 Property -

Chart of Accounts Governance Policy Number

Policy Title: Chart of Accounts Governance Policy Number: Date Issued: June 1, 2020 Responsible Executive: Controller Date Last Revised: June 1, 2020 Responsible Office: Financial Services Chart of Accounts Governance Policy Policy Statement This policy establishes Baylor University’s (“Baylor” or the “University”) rules and standards regarding the chart of accounts governance structure, responsibilities, and requirements. The Financial Services Office, which is responsible for all aspects of financial accounting and reporting, governs the chart of accounts. All requests for new or modified (including closing or inactivating) chart of accounts elements are subject to the chart of accounts governance processes and procedures, as developed and maintained by the Controller’s Office. Reason for the Policy This policy establishes formal responsibility and accountability for how the University processes requests for new, modified, or closed data elements on the chart of accounts. The purpose of standardized governance of the chart of accounts is to: • Create and maintain consistency for the structure of the segments of the chart of accounts; • Create and maintain consistency in how the chart of accounts segments are used in order to facilitate standard accounting and reporting at unit and University levels; • Provide a governance process that includes appropriate stakeholders in decision- making; and • Maintain alignment of critical chart of accounts segments and values across multiple interrelated systems, including subledgers. 1. Chart of Accounts Governance Policy Individuals/Entities Affected by this Policy This policy applies to all Baylor units and departments. Related Documents and Forms Chart of Accounts Segments (Appendix A) COA Request Form – New Chart Element (Appendix B) COA Request Form – Chart Element Modification (Appendix B) Definitions These definitions apply to terms as they are used in this policy.