Closing Disclosure Document with Your Loan Estimate

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Closing Disclosure Document with Your Loan Estimate

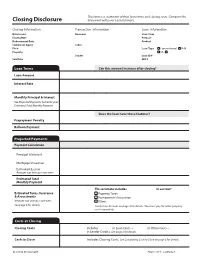

This form is a statement of final loan terms and closing costs. Compare this Closing Disclosure document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued Borrower Loan Term Closing Date Purpose Disbursement Date Product Settlement Agent Seller File # Loan Type Conventional FHA Property VA _____________ Lender Loan ID # Sale Price MIC # Loan Terms Can this amount increase after closing? Loan Amount Interest Rate Monthly Principal & Interest See Projected Payments below for your Estimated Total Monthly Payment Does the loan have these features? Prepayment Penalty Balloon Payment Projected Payments Payment Calculation Principal & Interest Mortgage Insurance Estimated Escrow Amount can increase over time Estimated Total Monthly Payment This estimate includes In escrow? Estimated Taxes, Insurance Property Taxes & Assessments Homeowner’s Insurance Amount can increase over time Other: See page 4 for details See Escrow Account on page 4 for details. You must pay for other property costs separately. Costs at Closing Closing Costs Includes $5,877.00 in Loan Costs + $7,642.43 in Other Costs – $0 in Lender Credits. See page 2 for details. Cash to Close Includes Closing Costs. See Calculating Cash to Close on page 3 for details. CLOSING DISCLOSURE PAGE 1 OF 5 • LOAN ID # 0000000000 This form is a statement of final loan terms and closing costs. Compare this Closing Disclosure document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued Borrower Loan Term -

5/1 MOP Loan Program

GENERAL GUIDELINES 5/1 Maximum Loan-to-Value Ratio: Same as Standard MOP LTV Thresholds Fixed Rate Period: 5 Years ORTGAGE M Maximum Loan Term: 30 Years RIGINATION Qualifying Interest Rate: Initial 5/1 MOP Interest Rate O Minimum Interest Rate: 3.25% ROGRAM P Maximum Payment-to-Income Ratio: 40% Maximum Overall Debt-to-Income Ratio: 48% PROGRAM OVERVIEW 5/1 MOP Initial Interest Rate The 5/1 Mortgage Origination Program (5/1 MOP) loan is a fully-amortizing mortgage loan The initial fixed interest rate* in effect during the Fixed Rate that offers an initial fixed interest rate and payment for the first 5 years of the loan, after which Period of the loan is comprised of the following three (3) the loan converts to a 1-year adjustable rate mortgage (“Standard MOP”) for the remaining components: loan term. The maximum overall loan term is 30 years. All or any portion of the principal Index: 5-year Treasury Bond Yield balance may be prepaid without penalty at any time and there is no negative amortization associated with 5/1 MOP loans. For eligibility requirements, refer to the MOP Brochure. Spread: J.P. Morgan U.S. Liquid Index (JULI) Index Service Fee: .25% IMPORTANT CONSIDERATIONS: *The minimum 5/1 MOP Initial Interest Rate is 3.25% • The 5/1 MOP Initial Interest Rate may be higher or lower than the current Standard Rate offered for a Standard MOP loan. The current interest rate for each of these loan products is available at www.ucop.edu/loan-programs. QUESTIONS? • Fixed rate payments during the first 5 years of the loan provide a stable monthly payment Contact the local Campus Housing Programs to borrowers; however, there is potential for increased monthly payments when the Fixed Representative or the University of California Home Loan Rate Period ends. -

AIG Investments Jumbo Underwriting Guidelines

AIG Investments Jumbo Underwriting Guidelines December 20, 2019 These AIG Investments Jumbo Underwriting Guidelines (Exhibit A-2) are dated December 20, 2019. The Underwriting Guidelines may be updated or modified from time to time. AIG Investments believes the information contained in this document relating to state laws and third party requirements to be accurate as of January 1, 2020. However, this information is provided for informational purposes only and may change at any time without notice. AIG Investments is providing this information without any warranties, express or implied. © 2019 AIG Investments. All Rights Reserved. AIG Investments is an affiliate of American International Group, Inc. ("AIG”). AIG Investments is the program administrator for this program and not the purchaser of the loan. Please refer to the AIG Investments Correspondent Seller's Guide for additional information regarding the relationship between the parties. MC-2-A987C-1016 Table of Contents Table of Contents ..................................................................................................................................................................................................................... 1 Jumbo Loan Underwriting Introduction ................................................................................................................................................................................. 5 Chapter One: General ..................................................................................................................................................................................................... -

The Length of a Title Search in Tg Youdan

THE LENGTH OF A TITLE SEARCH IN NTARI T.G. YOUDAN* Toronto This article deals with the statutory provisions which in the Ontario registry system regulate the length of a vendor's chain of title and which in some cases extinguish claims against the land. The main focus of the article is analysis of newprovisions on the topic which were introduced in 1981 . However, in order to place these provisions in context the author outlines the history - of relevant conveyancing law andpractice in both England and Ontario, and he reviews the effect ofprevious legislation on the same topic. Il s'agit dans cet article des dispositions législatives qui réglementent, dans le système d'enregistrement de l'Ontario, la longueur de la chaîne des titres d'un vendeur et qui, dans certains cas, amène l'extinction du droit à un bien-fonds. L'auteurs'intéresse particulièrement à l'analyse des nouvelles dispositions apportées dans ce domaine en 1981 . Pour replacer ces dispositions dans leur contexte, 1986 CanLIIDocs 62 l'auteur fait, à grands traits, l'histoire du droit des transferts et de la pratique qui s'y rapporte en Angleterre et en Ontario etpasse brièvement en revue l'effet de la législation antérieure dans ce domaine. Introduction In 1981 a new Part III of the Ontario Registry Act was enacted. I It . deals with proof of title by a vendor of land and determines the appropriate length of a search; it also has corresponding provisions which extinguish claims against land on the ground of their. antiquity. This is a topic of great importance, and the new provisions were clently intended to make major changes in conveyancing law and practice. -

Guide to Completing the Loan Estimate (LE)

Guide to Completing the Loan Estimate (LE) NOTE: This Guide is provided to help brokers complete the Loan Estimate form for loans that will be submitted to T.J. Financial, Inc., therefore may only refer to products offered by T.J. Financial, Inc. The information contained in this Guide is intended for use by T.J. Financial, Inc. clients only and should not be distributed to or used by consumers or other third-parties. Recipients of this Guide should consult with their compliance or legal counsel as to the specifics of the final rule. Nothing herein should be construed as legal advice and may not be relied upon as such. T.J. Financial, Inc. shall not be held liable, in any way, for any damages incurred by any person or business as a result of this Guide. LE PAGE 1 1 2 1 LETTERHEAD/ HEADER – Please leave blank or complete with TJ’s information as shown above. Should not disclose broker’s information. DATE ISSUED – Date LE is mailed or delivered to the borrower. APPLICANTS – Name and mailing address of all borrowers applying for the loan. An additional page may be added if space is insufficient to list all. PROPERTY – Full address of subject property. Zip code required. Additional page may not be added if space is insufficient. SALE PRICE – If loan is purchase money, use sales price. Otherwise, use estimated value or appraised value for refinance. LOAN TERM – Reflect in whole years. (ie: 15 years, 30 years) PURPOSE – Purchase or Refinance PRODUCT – Fixed Rate or Adjustable Rate. Adjustable Rate must disclose duration of introductory rate or payment period and the first adjustment period, as applicable. -

Good Faith Estimate (GFE)

OMB Approval No. 2502-0265 Good Faith Estimate (GFE) Name of Originator Borrower Originator Property Address Address Originator Phone Number Originator Email Date of GFE Purpose This GFE gives you an estimate of your settlement charges and loan terms if you are approved for this loan. For more information, see HUD’s Special Information Booklet on settlement charges, your Truth-in-Lending Disclosures, and other consumer information at www.hud.gov/respa. If you decide you would like to proceed with this loan, contact us. Shopping for Only you can shop for the best loan for you. Compare this GFE with other loan offers, so you can find your loan the best loan. Use the shopping chart on page 3 to compare all the offers you receive. Important dates 1. The interest rate for this GFE is available through . After this time, the interest rate, some of your loan Origination Charges, and the monthly payment shown below can change until you lock your interest rate. 2. This estimate for all other settlement charges is available through . 3. After you lock your interest rate, you must go to settlement within days (your rate lock period) to receive the locked interest rate. 4. You must lock the interest rate at least days before settlement. Summary of Your initial loan amount is $ your loan Your loan term is years Your initial interest rate is % Your initial monthly amount owed for principal, interest, and any mortgage insurance is $ per month Can your interest rate rise? c No c Yes, it can rise to a maximum of %. -

Agency Guideline Revisions Note: Suntrust Mortgage Specific Overlays Are Underlined

Agency Guideline Revisions Note: SunTrust Mortgage specific overlays are underlined. Impacted Revised Guidelines Topic Impacted Products Current Guidelines Document Effective Immediately for NEW AND EXISTING Loan Applications ON OR After May 26, 2017 Appraisal Correspondent HomeReady® Appraisal Analysis: Agency Loan Programs / Improvements Section of the Appraisal Report Appraisal Analysis: Agency Loan Programs / Improvements Section of the Appraisal Report Requirements Section 1.07 Mortgage / Accessory Appraisal- (non-AUS & Non-AUS Non-AUS Units Guideline DU) Note: Below is an EXCERPT only of the guidance from the above referenced section. All other currently published Note: Below is an EXCERPT only of the guidance from the above referenced section. All other currently published Home guidelines from this section remain the same. guidelines from this section remain the same. Possible® Accessory Units Accessory Units Mortgage Fannie Mae will purchase a one-unit property with an accessory unit. An accessory unit is typically an Fannie Mae will purchase a one-unit property with an accessory unit. An accessory unit is typically an (LPA) additional living area independent of the primary dwelling unit, and includes a fully functioning additional living area independent of the primary dwelling unit, and includes a fully functioning kitchen and bathroom. Some examples may include a living area over a garage and basement units. kitchen and bathroom. Some examples may include a living area over a garage and basement units. Whether a property is defined as a one-unit property with an accessory unit or a two-unit property Whether a property is defined as a one-unit property with an accessory unit or a two-unit property will be based on the characteristics of the property, which may include, but are not limited to, the will be based on the characteristics of the property, which may include, but are not limited to, the existence of separate utilities, a unique postal address, and whether the unit is rented. -

Closing Costs and Other Fees

CHAPTER 5 LOAN CLOSING AND INSURANCE 5-1 LOAN CLOSING. The conditions of the DE lender’s approval (FHA's commitment if applicable) should be discussed with the borrower and, if applicable, the seller or builder. A. Title Insurance. Title insurance is not required at closing. However, the lender is responsible for conveying good, marketable title to FHA when a claim is filed. The one exception to this involves property that previously had been sold by HUD (REO sale) and FHA has insured the mortgage financing the sale by HUD. If such a property had a title defect prior to the original conveyance to FHA, the lender will not be held responsible for any title defects arising prior to the sale by FHA. See 24 CFR 203.390 for additional information. B. Title Objections. Any additional exceptions discovered during the title search should be reported to the DE underwriter before the loan is closed, unless the exceptions are covered by the General Waiver. Lenders should ensure that any conditions of title to the property will be acceptable to FHA. FHA regulations at 24 CFR 203.389 state that FHA will not object to title because of common customary easements, restrictions, and encroachments and provides a general waiver for these title conditions. These include easements for public utilities, party walls, driveways, wooden or wire fences and for other similar purposes. Lenders should review 24 CFR 203.389 for a full description of the general waiver provisions. Other title matters not covered by this general waiver must be reviewed by the lender. -

Chapter 3: Escrow, Taxes, and Insurance

HB-2-3550 CHAPTER 3: ESCROW, TAXES, AND INSURANCE 3.1 INTRODUCTION To protect the Agency’s interest in the security property, the Servicing and Asset Management Office (Servicing Office) must ensure that real estate taxes and any other local assessments are paid and that the property remains adequately insured. To ensure that funds are available for these purposes, the Agency requires most borrowers who receive new loans to deposit funds to an escrow account. Borrowers who are not required to establish an escrow account may do so voluntarily. If an escrow account has been established, payments for insurance, taxes, and other assessments are made by the Agency. If an escrow account has not been established, the borrower is responsible for making timely payments. Section 1 of this chapter describes basic requirements for paying taxes and maintaining insurance coverage; Section 2 provides procedure for establishing and maintaining the escrow account; and Section 3 discusses procedures for addressing insured and uninsured losses to the security property. SECTION 1: TAX AND INSURANCE REQUIREMENTS [7 CFR 3550.60 and 3550.61] 3.2 TAXES AND OTHER LOCAL ASSESSMENTS The Agency contracts with a tax service to secure tax information for all borrowers. The tax service obtains tax bills due for payment, determines the optimal time to pay the taxes in order to take advantage of any discounts, and provides delinquent tax status on the portfolio. A. Tax Service Fee All borrowers are charged a tax service fee. Borrowers who obtain a subsequent loan are not required to pay a second tax service fee. -

CHFA Form 381: CHFA Homeaccess Second Mortgage Loan Estimate

Save this Loan Estimate to compare with your Closing Disclosure. Loan Estimate LOAN TERM 30 years PURPOSE Purchase DATE ISSUED PRODUCT 5 Year Interest Only, 5/3 Adjustable Rate APPLICANTS LOAN TYPE Conventional FHA VA _____________ LOAN ID # 1330172608 RATE LOCK NO YES, until PROPERTY Before closing, your interest rate, points, and lender credits can change unless you lock the interest rate. All other estimated closing costs expire on Sales Price Loan Terms Can this amount increase after closing? Loan Amount Interest Rate Monthly Principal & Interest See Projected Payments below for your Estimated Total Monthly Payment Does the loan have these features? Prepayment Penalty Balloon Payment Projected Payments Payment Calculation Principal & Interest Mortgage Insurance Estimated Escrow Amount can increase over time Estimated Total Monthly Payment This estimate includes In escrow? Property Taxes Estimated Taxes, Insurance & Assessments Homeowner’s Insurance Amount can increase over time Other: See Section G on page 2 for escrowed property costs. You must pay for other property costs separately. Costs at Closing Estimated Closing Costs Includes in Loan Costs + in Other Costs – in Lender Credits. See page 2 for details. Estimated Cash to Close Includes Closing Costs. See Calculating Cash to Close on page 2 for details. Visit for general information and tools. LOAN ESTIMATE PAGE 1 OF 3 • LOAN ID # 1330172608 Closing Cost Details Loan Costs Other Costs A. Origination Charges E. Taxes and Other Government Fees % of Loan Amount (Points) Recording Fees and Other Taxes Desk Review Fee $150 es Loan Origination Fee $1,000 F. Prepaids Processing Fee $300 Rate Lock Fee $525 Homeowner’s Insurance Premium ( months) Underwriting Fee $675 Mortgage Insurance Premium ( months) Verification Fee $200 Prepaid Interest ( per day for days @ ) Property Taxes ( months) G. -

Mortgage-Backed Securities & Collateralized Mortgage Obligations

Mortgage-backed Securities & Collateralized Mortgage Obligations: Prudent CRA INVESTMENT Opportunities by Andrew Kelman,Director, National Business Development M Securities Sales and Trading Group, Freddie Mac Mortgage-backed securities (MBS) have Here is how MBSs work. Lenders because of their stronger guarantees, become a popular vehicle for finan- originate mortgages and provide better liquidity and more favorable cial institutions looking for investment groups of similar mortgage loans to capital treatment. Accordingly, this opportunities in their communities. organizations like Freddie Mac and article will focus on agency MBSs. CRA officers and bank investment of- Fannie Mae, which then securitize The agency MBS issuer or servicer ficers appreciate the return and safety them. Originators use the cash they collects monthly payments from that MBSs provide and they are widely receive to provide additional mort- homeowners and “passes through” the available compared to other qualified gages in their communities. The re- principal and interest to investors. investments. sulting MBSs carry a guarantee of Thus, these pools are known as mort- Mortgage securities play a crucial timely payment of principal and inter- gage pass-throughs or participation role in housing finance in the U.S., est to the investor and are further certificates (PCs). Most MBSs are making financing available to home backed by the mortgaged properties backed by 30-year fixed-rate mort- buyers at lower costs and ensuring that themselves. Ginnie Mae securities are gages, but they can also be backed by funds are available throughout the backed by the full faith and credit of shorter-term fixed-rate mortgages or country. The MBS market is enormous the U.S. -

Buying a Home: What You Need to Know

Buying a Home: What you need to know n Getting Started n Ready to Buy n Refinancing n Condos n Moving to a Larger Home n Vacation Homes Apply anytime, anywhere Fast and easy Total security for your personal information Personal Service from our Mortgage Planners Go to Blackhawkbank.com Mortgages Home Loans/Apply Online Revised 4.2018 Owning a home has long been “the American In Wisconsin: WHEDA Fannie Mae Advantage: When you use the WHEDA Fannie Mae Advantage, you need less cash dream.” It’s a long-term commitment, but as your to close your loan and you will have lower monthly house equity increases with time (and payments) your payments than with most mortgages. What’s more, you’ll have peace of mind that your rate will never change with home will be a source of financial stability for you. their fixed rate and term. WHEDA FHA Advantage: With the WHEDA FHA Advantage, Wisconsin residents have the flexibility to leverage down payment assistance and other There are many things to think about whether you’re advantages to buy a home with an affordable mortgage. buying your first home, moving up, refinancing, or considering a vacation property. Let’s get the In Illinois: IHDA works with financial partners across Illinois conversation started! to offer programs that help qualified Illinois first-time homebuyers to receive down payment and closing cost assistance. Buying a home can be both exciting and intimidating, so IHDA strives to make the goal of homeownership as streamlined as possible. Be sure to ask your Blackhawk Mortgage Planner for a current list what IDHA offers.