REVIEWING the TITLE SEARCH by Joseph E. Seagle, Esq. [email protected] INTRODUCTION Before One Can Discuss What a Title Agent Or

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Length of a Title Search in Tg Youdan

THE LENGTH OF A TITLE SEARCH IN NTARI T.G. YOUDAN* Toronto This article deals with the statutory provisions which in the Ontario registry system regulate the length of a vendor's chain of title and which in some cases extinguish claims against the land. The main focus of the article is analysis of newprovisions on the topic which were introduced in 1981 . However, in order to place these provisions in context the author outlines the history - of relevant conveyancing law andpractice in both England and Ontario, and he reviews the effect ofprevious legislation on the same topic. Il s'agit dans cet article des dispositions législatives qui réglementent, dans le système d'enregistrement de l'Ontario, la longueur de la chaîne des titres d'un vendeur et qui, dans certains cas, amène l'extinction du droit à un bien-fonds. L'auteurs'intéresse particulièrement à l'analyse des nouvelles dispositions apportées dans ce domaine en 1981 . Pour replacer ces dispositions dans leur contexte, 1986 CanLIIDocs 62 l'auteur fait, à grands traits, l'histoire du droit des transferts et de la pratique qui s'y rapporte en Angleterre et en Ontario etpasse brièvement en revue l'effet de la législation antérieure dans ce domaine. Introduction In 1981 a new Part III of the Ontario Registry Act was enacted. I It . deals with proof of title by a vendor of land and determines the appropriate length of a search; it also has corresponding provisions which extinguish claims against land on the ground of their. antiquity. This is a topic of great importance, and the new provisions were clently intended to make major changes in conveyancing law and practice. -

How to Buy Title Insurance In

How to Buy Title Insurance in [Insert State] This guide: • Covers the basics of title insurance. • Explains the need for title insurance. • Offers tips to shop for title insurance and closing services. • Gives you questions you should ask before you buy title insurance. [Name] [DOI Logo] [Superintendent of Insurance] [DOI Website Address] Drafting Note: This template has been developed for state departments of insurance who are interested in providing a consumer education publication regarding title insurance. The template was developed as a comprehensive guide that can be edited/personalized to meet the individual needs of a state. DRAFT: 3-23-215-25-21 1 Table of Contents Introduction Page 3 Buying or Refinancing a Property Page 3 What is Title Insurance, and What Does it Cover? Page 4 Two Types of Title Insurance—Owner’s and Lender’s Policies Page 4 What Doesn’t Title Insurance Cover? Page 4 Who Sells Title Insurance? Page 5 The Right to Choose Your Own Title Agent/Company Page 5 Who Pays for Title Insurance? Page 5 What Does Title Insurance Cost? Page 6 Ask if You’re Eligible for Discounts Page 6 The Difference Between Title and Homeowners Insurance Page 6 Questions to Ask Before You Buy Title Insurance Page 6 The Real Estate Closing Page 7 Closing Agents Page 8 Questions to Ask When You Choose a Closing Agent Page 8 Closing Protection Page 8 Shop Around for Title Insurance and Closing Services Page 8 Cost Comparison Chart Page 9 Final Tips to Remember Page 10 How to File a Title Insurance Claim Page 10 The [INSERT DOI NAME] is Here to Help Page 10 Other Resources Available Page 11 Disclaimer: The information included in this publication is meant to serve as a guide and is not a substitute for legal or professional advice. -

TITLE STANDARDS October 10, 2019 10305 ICLE: State Bar Series

TITLE STANDARDS October 10, 2019 10305 ICLE: State Bar Series Thursday, October 10, 2019 TITLE STANDARDS 6 CLE Hours Including 1 Ethics Hour | 1 Professionalism Hour Copyright © 2019 by the Institute of Continuing Legal Education of the State Bar of Georgia. All rights reserved. Printed in the United States of America. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form by any means, electronic, mechanical photocopying, recording, or otherwise, without the prior written permission of ICLE. The Institute of Continuing Legal Education’s publications are intended to provide current and accurate information on designated subject matter. They are off ered as an aid to practicing attorneys to help them maintain professional competence with the understanding that the publisher is not rendering legal, accounting, or other professional advice. Attorneys should not rely solely on ICLE publications. Attorneys should research original and current sources of authority and take any other measures that are necessary and appropriate to ensure that they are in compliance with the pertinent rules of professional conduct for their jurisdiction. ICLE gratefully acknowledges the eff orts of the faculty in the preparation of this publication and the presentation of information on their designated subjects at the seminar. The opinions expressed by the faculty in their papers and presentations are their own and do not necessarily refl ect the opinions of the Institute of Continuing Legal Education, its offi cers, or employees. The faculty is not engaged in rendering legal or other professional advice and this publication is not a substitute for the advice of an attorney. -

County Title Search Standards

COUNTY TITLE SEARCH STANDARDS (A) In general It is the responsibility of all persons making title searches (hereinafter referred to as “searchers”) to keep informed with respect to the time lag of indexing in all the various offices. Generally, in searching the indexes, the rule of idem sonans should be followed. Names such as “A. John Doe” should be searched both under “A” and “J” in indexes using first name divisions; names such as “C(K)arl” and C(K)atherine” should be searched under “C” and “K” in such indexes. Corporate names such as “John A. Smith, Inc.” should be searched both under “J” and “S.” If title is acquired by nickname, the proper name should also be searched. For example, “Tony” requires a search for “Anthony.” Attention is called to the fact that there are special headings used in the various indexes including “schools,” “churches,” “lot owners,” “vacations,” “annexations,” “trustees,” “lodges,” etc. Relative to corporate title holders, since the searcher is to include the Articles of Incorporation, he should also include all pertinent amendments, mergers or consolidations. If a change of name of a corporate title holder is disclosed in any records required by these standards to be searched, the search should be made under both the new name and the former name from the date of the name change. Land Contract vendees must be searched as fee owners. (B) New Indexes and Records It is the responsibility of all searchers to keep informed as to the creation of new indexes subsequent to the adoption of these Search Standards. -

Title Examinations and Title Issues

CHAPTER 7 Title Examinations and Title Issues R. Prescott Jaunich, Esq. Downs Rachlin Martin PLLC, Burlington Timothy S. Sampson, Esq. Downs Rachlin Martin PLLC, Burlington § 7.1 Introduction ................................................................................. 7–1 § 7.2 Marketable Title .......................................................................... 7–4 § 7.2.1 Vermont Title Standards ............................................... 7–4 § 7.2.2 Common Law Marketable Title—Permits as Encumbrances ............................................................... 7–6 § 7.2.3 Vermont Marketable Record Title Act ........................ 7–10 (a) Person ................................................................ 7–11 (b) Unbroken Chain of Title .................................... 7–11 (c) Conveyance ....................................................... 7–12 (d) Preserved Claims Under the Act ........................ 7–13 § 7.3 Conveyancing Requirements .................................................... 7–15 § 7.3.1 Vermont Deed Customs .............................................. 7–15 § 7.3.2 Deeds by Trustees and Deeds to Trust ........................ 7–17 § 7.3.3 Deeds by Executors, Administrators and Guardians .. 7–17 § 7.3.4 Deeds by Divorce Judgment ....................................... 7–18 § 7.3.5 Probate Decree ............................................................ 7–18 § 7.4 Identifying the Real Estate and Property Descriptions .......... 7–18 § 7.4.1 Reference to Prior Deeds and Instruments -

The Title Opinion: an Overview

The Title Opinion: An Overview A title opinion may only be drafted by a licensed attorney. This overview is provided only for educational use and does not constitute and may not be used to give legal advice. The first step in a title opinion is a title search. A title search entails the detailed review of real property records in the county where the land is located. Each state maintains a recording system, which is like a library made up of title-related documents. In West Virginia, real property records are stored in the county clerk’s office. These records include copies of deeds, mortgages, and other instruments that convey an interest in real property to a new owner. The county also maintains estate records, which become relevant when land is given to a new owner through a will. One step in a title search is researching the chain of title: an attorney develops a full chronology of how the property has transferred between owners. For example, A deeds to B; B deeds to C; D inherits property from C; D deeds to E; E mortgages to X; E deeds to F subject to X’s mortgage; X executes a satisfaction of the mortgage; F deeds to G; and so forth.1 The history of the property is frequently much more complicated because, for example, properties may be divided into multiple parcels or conveyed to multiple owners. After the chain of title has been established, the title attorney will identify other encumbrances and activities appearing in the records that have the potential to cloud title. -

Title Insurance Protects Your Investment

Title Insurance Protects Your Investment During the closing process, make sure you request an Owner’s Policy of Title Insurance in addition to a Loan Policy By New Mexico Land Title Association After a months-long search, you finally find your family’s dream home—a safe neighborhood and great schools, and a big backyard for the swimming pool you plan to build. You move in and hire a contractor, but a few days into construction the contractor finds an underground utility line running right through the middle of your backyard. You check your title insurance policy, and find out that the title search did not discover the easement. What do you do? Here’s another scenario. After retiring, you decide to downsize and buy a smaller townhome on a golf course. A month after you move in, a man knocks on your door and claims he is the real owner of your home. Upon further investigation, you discover that the sellers weren’t the real owners, but people posing as the owners. They searched the public records for a home with out-of-state owners, forged and recorded a fictitious deed, then sold the property to you before the real owners (or you) discovered the scam. Sound farfetched? Both of these scenarios really happened. To protect your investment from these and other serious problems, make sure you have title insurance. Title Insurance 101 Title insurance insures that the title to your property is clear, with no known liens or encumbrances, such as unpaid property taxes, recorded liens, or street and sewer easements. -

Scope of Work for Closing and Title Search Services

SCOPE OF WORK FOR CLOSING AND TITLE SEARCH SERVICES FOR THE NATURAL RESOURCES CONSERVATION SERVICE GENERAL I. OBJECTIVE The objective of this contract is to retain closing and title search services for acquisitions of wetland easements on behalf of the United States of America, acting by and through the Natural Resources Conservation Service (NRCS), United States Department of Agriculture, pursuant to Title XII of the Food Security Act of 1985, as amended, 16 USC. 3837. II. BACKGROUND The Wetlands Reserve Program (WRP) authorizes the acquisition of easement rights for willing landowners for the purpose of restoring and protecting wetlands. The NRCS is the lead agency within the United States Department of Agriculture charged with administering the program. IV. STANDARDS AND RESPONSIBILITIES The Contractor is responsible for having a current knowledge of the requirements of New Hampshire State law in connection with title searches, closing real estate transactions, and title clearance. The title insurance company must be on the United States Attorney General’s list of approved companies and must comply with all New Hampshire State laws, including title insurance reserves requirements. The Contractor must be an approved agent licensed to do title insurance business in the State of New Hampshire. The title insurance company must be approved by the State Insurance Commissioner. The Contractor will provide evidence of liability insurance coverage for errors and omissions in the amount of at least $1,000,000 and fidelity coverage of at least $500,000 on each individual who will have access to the WRP funds or provide an indemnification agreement from the title insurance for which the Contractor will close the transaction(s) satisfactory to the NRCS providing for reimbursement to NRCS for any loss caused by fraud or dishonesty, or failure by the attorneys, agents, or employees of the Contractor to comply with NRCS’ written closing instructions. -

Step 1 Starting the Process

Step 1 Starting the Process A sales contract is signed by the buyer and seller, and delivered to the title company of their choosing, usually accompanying an earnest money check. The escrow is accepted by the escrow agent and often confirmed with an earnest money receipt upon request. The escrow agent starts the closing process by opening a title order. The file begins to be processed with the collection of data including but not limited to obtaining loan payoff information, marital status of parties, legal documentation for corporate entities & ordering inspections. Step 2 Title Search and Examination This search is made of the public records. Records searched include deeds, mortgages, easements, assessments, liens, judgments, wills, probate court, divorce settlements and other documents affecting title to the property. Title examination is the examination of the documents found during the title search that affect the title to the property. This step verifies who the legal owner is and the debts owed against the property are determined. Upon completion of the search and examination, a title commitment/preliminary report is prepared and reviewed and sent out to interested parties including the realtor, broker, lender, attorney, seller or purchaser. Step 3 Document Preparation The closing agent will review the lender’s documents & instructions, types the appropriate documents, follow the real estate contract terms and agreements, review instructions from other parties involved in the transaction and insert closing fees into the settlement statement. The escrow agent acts as a key communicator with all parties involved throughout process until file is ready to schedule and close. -

PDF(Brochure Format)

ROLL FOLD... DOUBLE CHECK ADJUSTMENTS FOR ROLL FOLD... 1/16" creep. MAKE ADJUSTMENTS FOR DOT GAIN. note, deed of trust, tax forms, and other disclosures). associated with the loan, title search and closing. These Q: The closing attorney is asking me to remit • create a false gift letter for down payment funds. the other party may terminate the contract. If you are not A seller will be asked to sign a deed conveying the costs include the appraisal fee, survey, pest inspection, funds via wire transfer. How can I protect myself • make it appear you made a deposit when, in fact, using the standard form Offer to Purchase and Contract property to the buyer. If a buyer has not already lender fees, fees to establish an escrow balance for from wire transfer fraud? you did not. in your transaction, you should consult an attorney received and reviewed copies of the termite report, homeowner’s insurance, taxes and any required private A: Before transferring any funds via wire transfer, • give the seller a secret or even false or “forgivable” regarding the impact of a possible delay in closing. Questions and Answers on: survey and repair invoice(s), he/she should do that at mortgage insurance, attorney fees, title insurance, and contact the closing attorney’s office by telephone using second mortgage. the closing. recording fees. The seller normally pays the balance a publicly verified phone number and speak directly • make payments outside of closing which are not Related reading available from the Real Estate due on any existing loans, his portion of the taxes, to the closing attorney or a member of his/her staff disclosed on the closing disclosure or closing/ Commission: REAL ESTATE commissions to real estate brokers, fees for deed to obtain the correct wire transfer information. -

Title Insurance 101: a Guide for Realtors, Home Buyers, & Lenders

Title Insurance 101: A Guide for Realtors, Home Buyers, & Lenders TABLE OF CONTENTS • Introduction • The History Behind Title Insurance in the United States • Why Do You Need Title Insurance? • What Is Lender’s Title Insurance? • What Is Owner’s Title Insurance? • What Is a Title Commitment and Why Is It Important? • What Does a Title Insurance Underwriter Do? • How Much Does Title Insurance Cost? • What Are Title Policy Endorsements? • What Are Title Insurance Vesting Issues? • What Should You Look for in a Title Insurance Company? • What Should You Expect From the Title Policy Process? Don’t Think You Own. Be Sure. www.BNTC.com Call us at 727.449.8733 INTRODUCTION One of the most important steps to take before closing the deal on the purchase of a new home is to obtain title insurance. But what is it? Why do you need it? And where can you get it? We created this eBook to answer those questions and many others and to help realtors, home buyers, and mortgage lenders better understand the ins and outs of title insurance. Don’t Think You Own. Be Sure. www.BNTC.com Call us at 727.449.8733 THE HISTORY BEHIND TITLE INSURANCE IN THE UNITED STATES In layperson’s terms, a title to a piece of property provides evidence of lawful ownership. And title insurance is a type of policy that insures a property owner or mortgage lender against loss by reason of defects in the title to a piece of real estate. But up until the 1870s in the United States, there was no title insurance. -

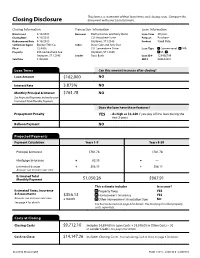

Closing Disclosure Document with Your Loan Estimate

This form is a statement of final loan terms and closing costs. Compare this Closing Disclosure document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued 4/15/2013 Borrower Michael Jones and Mary Stone Loan Term 30 years Closing Date 4/15/2013 123 Anywhere Street Purpose Purchase Disbursement Date 4/15/2013 Anytown, ST 12345 Product Fixed Rate Settlement Agent Epsilon Title Co. Seller Steve Cole and Amy Doe File # 12-3456 321 Somewhere Drive Loan Type x Conventional FHA Property 456 Somewhere Ave Anytown, ST 12345 VA _____________ Anytown, ST 12345 Lender Ficus Bank Loan ID # 123456789 Sale Price $180,000 MIC # 000654321 Loan Terms Can this amount increase after closing? Loan Amount $162,000 NO Interest Rate 3.875% NO Monthly Principal & Interest $761.78 NO See Projected Payments below for your Estimated Total Monthly Payment Does the loan have these features? Prepayment Penalty YES • As high as $3,240 if you pay off the loan during the first 2 years Balloon Payment NO Projected Payments Payment Calculation Years 1-7 Years 8-30 Principal & Interest $761.78 $761.78 Mortgage Insurance + 82.35 + — Estimated Escrow + 206.13 + 206.13 Amount can increase over time Estimated Total Monthly Payment $1,050.26 $967.91 This estimate includes In escrow? Estimated Taxes, Insurance x Property Taxes YES & Assessments $356.13 x Homeowner’s Insurance YES Amount can increase over time a month x Other: Homeowner’s Association Dues NO See page 4 for details See Escrow Account on page 4 for details. You must pay for other property costs separately.