VIETNAM Data Collection Survey on E-Money and Transport Smart Card

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Trang 1/ 13 TERMS and CONDITIONS

“REFER CITI CARD, GET PREMIUM GIFTS – PERIOD 3/2021” PROGRAM (Effective from Sep 16th, 2021) TERMS AND CONDITIONS 1. Program Scope The “Refer Citi Card, Get Premium Gifts – Period 3/2021” Program (“the Program”) is applicable at Ha Noi and Ho Chi Minh City for existing primary card members of Citi PremierMiles card or Citi Cash Back card or Citi Rewards card or Citi Simplicity+ card or Lazada Citi Platinum card who refer their friends to apply for a Citi PremierMiles card or Citi Cash Back card or Citi Rewards card or Citi Simplicity+ card during the Program Period. 2. Program Period Sep 16th, 2021 to Jan 15th, 2022 (both days inclusive). 3. Promotion scheme 3.1. Within the program period, Eligible referrer will receive Cash Back and Tier rewards for each and multiple successful referrals, details as following: Successful Cash Back Tier Rewards Referrals 1 500,000 VND 2 1,000,000 VND 3 1,500,000 VND Tier 1: GotIt e-voucher valued VND 4 2,000,000 VND 2,000,000 5 2,500,000 VND 6 3,000,000 VND 7 3,500,000 VND Tier 2: AccorPlus Explorer 8 4,000,000 VND membership valued VND 6,000,000 9 4,500,000 VND 10 5,000,000 VND 11 5,500,000 VND Issued by Citibank Vietnam Page 1 of 6 12 6,000,000 VND Tier 3: Apple Watch SE 44mm GPS 13 6,500,000 VND valued VND 9,990,000 14 7,000,000 VND 15+ 7,500,000 VND Special: Apple 11-inch iPad Pro Wi-Fi 128GB valued VND 21,990,000 Caps 7,500,000 VND Tier 1: 100 gifts Tier 2: 50 gifts Tier 3: 30 gifts Special: 20 gifts Note: In all situations, a Referrer who satisfies all the terms and conditions of the program will receive maximum VND 7,500,000 cash back. -

Bradley C Resume

BRADLEY C. LALONDE Co-Founder and Managing Partner Vietnam Partners LLC Hanoi, Vietnam email: [email protected] mobile: +84-90-810-6518 (Vietnam) +1-917-991-9109 (global) PROFESSIONAL EXPERIENCE: Over 25 year career in investment and corporate banking in multiple countries, spanning the United States, Europe, Middle East, Africa and Asia. Over 15 years experience in general management of Citibank franchises encompassing credit, marketing, operations and technology and treasury activities. Built start up franchises into profitable and well controlled businesses in Turkey, Tunisia and Vietnam. Key competences are marketing, credit and risk management , people management, particularly hiring, training and developing staff in marketing and risk management skills. A frequent guest lecturer in selling skills, marketing and risk management in Citibank training programs. In addition, significant professional experience in strategic planning, developing a business model to service the non-bank financial institutions industry, corporate audit for commercial lending and leasing in the United States, and Private Equity. Senior Credit Officer of Citigroup. Awarded distinguished order of the Republic from President of Tunisia for contributions to banking system(1993). Chairman of the American Chamber of Commerce in Hanoi, Vietnam(1996-1998). Numerous board seats on various trade and community organizations. PRESENT: Partner and Co-Founder of Vietnam Partners, New York. Since October 03 to present. An Investment Bank serving the Vietnamese government and businesses in Vietnam. Investing capital, raising capital and providing financial advise. Head office in New York City and representative office in Hanoi, Vietnam. Notable achievements over the last 5 years. Established 50:50 joint venture fund management company with Bank for Development and Investment in Vietnam( BIDV). -

Causality in Vietnam's Parallel Exchange Rate System During

economies Article Causality in Vietnam’s Parallel Exchange Rate System during 2005–2011: Policy Implications for Macroeconomic Stability Minh Tam Bui Faculty of Economics, Srinakharinwirot University, Bangkok 10110, Thailand; [email protected] Received: 5 October 2018; Accepted: 21 November 2018; Published: 12 December 2018 Abstract: As in many transition economies, Vietnam has experienced a multiple exchange rate system with three exchange rates having co-existed. This paper uses the Vector-Error-Correction model and the Granger tests to investigate the relationship between the official and black market exchange rates from January 2005 to April 2011. The results confirm a long-run relationship between the official and parallel market rates of the Vietnam dong against the U.S. dollar. The short-run dynamics of two exchange rates suggest that the official exchange rate causes the black exchange rate, but not vice versa. This conclusion is valid for both a sub-period of stability and a sub-period of vibrant fluctuations, with February 2008 as the cut-off. The findings also reject the efficiency hypothesis of the black market for foreign exchange and support the policy choice of the State Bank of Vietnam not to follow black market signals in managing official exchange rates for macroeconomic stability. Keywords: parallel market; exchange rate dynamics; black market; causality; inflation JEL Classification: F31; E52; E58; C32 1. Introduction The exchange rate system in Vietnam has experienced different episodes due to macroeconomic fluctuations and changes in exchange rate policy following the economic reforms in the late 1980s. This includes a period of free floating in early 1990s, and a pegging system during 1993–1996. -

The Unintended Consequences of Successful Resource Mobilization: Financing Development in Vietnam

The Unintended Consequences of Successful Resource Mobilization: Financing Development in Vietnam Jay K. Rosengard, Trần Thị Quế Giang, Đinh Vũ Trang Ngân, Huỳnh Thế Du, and Juan Pablo Chauvin 2011 M-RCBG Faculty Working Paper No. 2011-01 Mossavar-Rahmani Center for Business & Government Weil Hall | Harvard Kennedy School | www.hks.harvard.edu/mrcbg The views expressed in the M-RCBG Working Paper Series are those of the author(s) and do not necessarily reflect those of the Mossavar-Rahmani Center for Business & Government or of Harvard University. M-RCBG Working Papers have not undergone formal review and approval. Papers are included in this series to elicit feedback and encourage debate on important public policy challenges. Copyright belongs to the author(s). Papers may be downloaded for personal use only. The Unintended Consequences of Successful Resource Mobilization: Financing Development in Vietnam Jay K. Rosengard, Trần Thị Quế Giang, Đinh Vũ Trang Ngân, Huỳnh Thế Du, and Juan Pablo Chauvin Executive Summary The total amount of development finance generated by Vietnam has been exceptionally high from all significant sources using all standard measures of comparison. However, there are many potential unintended consequences of Vietnam’s successful resource mobilization, with significant implications for the future financing of development. There are several steps the government can take to mitigate these risks. The principal vulnerabilities created by Vietnam’s mobilization of substantial resources for development finance fall into two main categories: threats to macroeconomic stability caused by imbalances in the composition of funding; and risks for microeconomic management arising from imprudent financing structures. The most serious macroeconomic threats are: public sector funds crowding out both access to and utilization of private sector funds; overleveraging of insufficient equity for unsustainable levels of debt; financial exclusion of low-income households and family enterprises; and flight of hot capital. -

Driving Growth Through Innovation in Vietnam Keeping an Eye on the Prize and an Open Mind

Driving growth through innovation in Vietnam Keeping an eye on the prize and an open mind In association with In mid-December 2017 in Hanoi, more than a dozen leaders of Vietnam’s banking, finance and FinTech industry joined a roundtable luncheon hosted by EY to discuss developments in the sector and how competing interests can be aligned to drive future growth. Finding synergies between legacy financial institutions and the more disruptive FinTech start-up players was a key part of the discussion, as was how these new developments in the financial services industry are facing the challenge of being ahead of a more conservative regulatory environment. Finally, the discussion also addressed ways in which technology could be used to streamline services and drive down the cost of service provision using automation and other technological advances. Competition and Cooperation He said banks have generally not welcomed the emergence of the FinTech companies. Like many industries in Vietnam, the FinTech sector “The partnership between FinTech players and has seen rapid growth in recent years. While it is the traditional finance industry has always difficult to gauge the exact amount of investment been a struggle in the early days”. new FinTechs have attracted, an estimate published in Vietnam Investment Review from the Topica “We have seen similar struggles in recent years, Founder Institute put the total investment in particularly in the payment business. And then Vietnamese FinTech start-ups in 2016 at $129 we moved to the lending business and we are million dollars, accounting for 63 per cent of all facing similar difficulties.” start-up contract value, with companies such as Binh related his experience with establishing Payoo, VNPT E-pay, M_Service (Momo), and F88 an online loan platform in which the entire process leading in terms of deal value. -

Vietnam Global Depositary Notes (Gdns) Issuance & Cancellation Guide GDN List / Vietnamese Bonds

Depositary Receipt Services August 2015 Vietnam Global Depositary Notes (GDNs) Issuance & Cancellation Guide GDN List / Vietnamese Bonds Coupon Maturity Date Local ISIN GDN ISIN 144A GDN ISIN REGS 12.300% 6/20/2016 VNTD11160403 US92670LAH24 XS1247495903 12.50% 7/25/2016 VNTD11160502 US92670LAJ89 XS1247502377 12.40% 9/6/2016 VNTD11160544 US92670LAK52 XS1247503268 7.60% 10/31/2016 VNTD13160195 US92670LAL36 XS1247505396 10.80% 4/15/2017 VNTD12170369 US92670LBA61 XS1247507095 9.50% 6/15/2017 VNTD12170385 US92670LAM19 XS1247509034 9.30% 1/15/2018 VNTD13180219 US92670LAN91 XS1247509620 8.20% 1/15/2019 VNTD14190811 US92670LAP40 XS1247511014 7.90% 2/15/2019 VNTD14190829 US92670LAQ23 XS1247511527 6.00% 1/15/2020 VNTD15202565 US92670LAR06 XS1247512681 5.40% 1/31/2020 VNTD15202599 US92670LAS88 XS1247513499 5.30% 2/15/2020 VNTD15202607 US92670LAT61 XS1247514208 5.20% 2/28/2020 VNTD15202615 US92670LAU35 XS1247515601 8.70% 5/31/2024 VNTD14240921 US92670LAV18 XS1247516328 8.80% 3/15/2029 VNTD14290942 US92670LAW90 XS1247516674 7.60% 1/31/2030 VNTD15302589 US92670LAX73 XS1247517219 7.50% 2/28/2030 VNTD15302878 US92670LAY56 XS1247517565 7.20% 3/15/2030 VNTD15302886 US92670LAZ22 XS1247518530 Ratio for GDN Trading & Settlement Purposes • 1 Vietnam GDN = VND 100,000 nominal amount of Local Vietnamese Government Bonds 1 Vietnam GDN Issuance Process 1. On S/D, International Broker-Dealer sends instructs its local custodian (MT542 - DF Instruction) for the delivery of Vietnamese bonds to “Citibank NY GDN safekeeping account” at Citibank Vietnam including the following information: International Investor a) Counterparty: Citibank, N.A. – GDN depositary b) Local Vietnamese Bonds quantity & ISIN, c) GDN quantity & ISIN International Broker-Dealer d) GDN settlement instructions (DTC participant+ any sub-account # or other relevant reference). -

APEC Meeting Documents

Participant List (GFPN 03/2009A) APEC Workshop: Best Practices in Microfinance 7-8 April 2011, Hanoi, Vietnam PARTICIPANTS LIST Economy: BRUNEI DARUSSALAM S/N Title Name Position Organization Contacts ( Tel / HP / Fax / Email ) Rogayah binti Abdullah Community Development Officer Ministry of Culture, Youth and [email protected] Sports Norzaridah binti Haji Community Development Officer Ministry of Culture, Youth and [email protected] Zainal Sports Economy: CHILE S/N Title Name Position Organization Contacts ( Tel / HP / Fax / Email ) Ms. Katia Makhlouf Advisor in SMEs Division Ministry of Economy [email protected] Ms. Viviana Paredes Head of Women work Area Women’s National Service of Chile (SERNAM) [email protected] Economy: CHINA S/N Title Name Position Organization Contacts ( Tel / HP / Fax / Email ) Mr. ZHANG Haiying Division director Department of Small and Medium T: 861.0682.05316 Enterprises, Ministry of Industry and F: 861.0660.17331 Information Technology [email protected] 4 S/N Title Name Position Organization Contacts ( Tel / HP / Fax / Email ) Mr. ZHANG Baiyin Expert Ministry of Industry and Information T: 861.0682.05325 Technology Software and Integrated F: 861.0660.17331 circuit Promotion Center [email protected] Economy: INDONESIA S/N Title Name Position Organization Contacts ( Tel / HP / Fax / Email ) Mrs. Ika Tejaningrum Senior Analyst, Head of Research & Central Bank of Indonesia T: 622.1381.7991 Development on Credit and SMEs F: 622.1351.8951 [email protected] Ms. Caroline Mangowal Research Unit Manager Microfinance Innovation Center for [email protected] Resources and Alternatives (MICRA) Economy: MALAYSIA S/N Title Name Position Organization Contacts ( Tel / HP / Fax / Email ) Mrs. -

Strengthening Trade Capacity for Development

© OECD, 2001. © Software: 1987-1996, Acrobat is a trademark of ADOBE. All rights reserved. OECD grants you the right to use one copy of this Program for your personal use only. Unauthorised reproduction, lending, hiring, transmission or distribution of any data or software is prohibited. You must treat the Program and associated materials and any elements thereof like any other copyrighted material. All requests should be made to: Head of Publications Service, OECD Publications Service, 2, rue André-Pascal, 75775 Paris Cedex 16, France. 43 2001 07 1 P 18/10/01 19:10 Page 1 The DAC Guidelines Strengthening Trade Capacity for Development ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT histo.fm Page 1 Monday, October 1, 2001 3:38 PM ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT Pursuant to Article 1 of the Convention signed in Paris on 14th December 1960, and which came into force on 30th September 1961, the Organisation for Economic Co-operation and Development (OECD) shall promote policies designed: – to achieve the highest sustainable economic growth and employment and a rising standard of living in Member countries, while maintaining financial stability, and thus to contribute to the development of the world economy; – to contribute to sound economic expansion in Member as well as non-member countries in the process of economic development; and – to contribute to the expansion of world trade on a multilateral, non-discriminatory basis in accordance with international obligations. The original Member countries of the OECD are Austria, Belgium, Canada, Denmark, France, Germany, Greece, Iceland, Ireland, Italy, Luxembourg, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland, Turkey, the United Kingdom and the United States. -

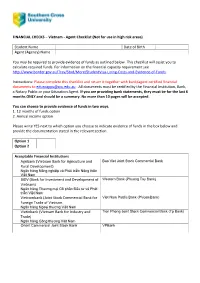

FINANCIAL CHECKS – Vietnam - Agent Checklist (Not for Use in High Risk Areas)

FINANCIAL CHECKS – Vietnam - Agent Checklist (Not for use in high risk areas) Student Name Date of Birth Agent (Agency) Name You may be required to provide evidence of funds as outlined below. This checklist will assist you to calculate required funds. For information on the financial capacity requirement see http://www.border.gov.au/Trav/Stud/More/StudentVisa-Living-Costs-and-Evidence-of-Funds. Instructions: Please complete this checklist and return it together with bank/agent certified financial documents to [email protected] . All documents must be certified by the Financial Institution, Bank, a Notary Public or your Education Agent. If you are providing bank statements, they must be for the last 6 months ONLY and should be a summary. No more than 10 pages will be accepted. You can choose to provide evidence of funds in two ways. 1. 12 months of funds option 2. Annual income option Please write YES next to which option you choose to indicate evidence of funds in the box below and provide the documentation stated in the relevant section. Option 1 Option 2 Acceptable Financial Institutions Agribank (Vietnam Bank for Agriculture and Bao Viet Joint Stock Commercial Bank Rural Development) Ngân hàng Nông nghiệp và Phát triển Nông thôn Việt Nam BIDV (Bank for Investment and Development of Western Bank (Phuong Tay Bank) Vietnam) Ngân hàng Thương mại Cổ phần Đầu tư và Phát triển Việt Nam Vietcombank (Joint Stock Commercial Bank for Viet Nam Public Bank (PVcomBank) Foreign Trade of Vietnam. Ngân hàng Ngoại thương Việt Nam Vietinbank (Vietnam -

Responsible Finance in Vietnam

Responsible Finance in Vietnam IN PARTNERSHIP WITH Schweizerische Eidgenossenschaft Federal Department of Economic Affairs, Confédération suisse Education and Research EAER Confederazione Svizzera State Secretariat for Economic Affairs SECO Confederaziun svizra Swiss Confederation PB 1 About IFC IFC, a member of the World Bank Group, is the largest global development institution focused exclusively on the private sector. Working with private enterprises in about 100 countries, we use our capital, expertise, and influence to help eliminate extreme poverty and boost shared prosperity. In FY14, we provided more than $22 billion in financing to improve lives in developing countries and tackle the most urgent challenges of development. For more information, visit www.ifc.org Disclaimer “IFC, a member of the World Bank Group, creates opportunity for people to escape poverty and improve their lives. We foster sustainable economic growth in developing countries by supporting private sector development, mobilizing private capital, and providing advisory and risk mitigation services to businesses and governments. This report was commissioned by IFC within the Vietnam Microfinance Sector Capacity Building Project, financedy b the Swiss State Secretariat for Economic Affairs (SECO).” “The conclusions and judgments contained in this report should not be attributed to, and do not necessarily represent the views of, IFC or its Board of Directors or the World Bank or its Executive Directors, or the countries they represent. IFC and the World Bank do -

Connected and Disconnected in Viet Nam : Remaking Social Relations in a Post-Socialist Nation / Editor Philip Taylor

CONNECTED & DISCONNECTED IN VIET NAM Remaking Social Relations in a Post-socialist Nation CONNECTED & DISCONNECTED IN VIET NAM Remaking Social Relations in a Post-socialist Nation EDITED BY PHILIP TAYLOR VIETNAM SERIES Published by ANU Press The Australian National University Acton ACT 2601, Australia Email: [email protected] This title is also available online at press.anu.edu.au National Library of Australia Cataloguing-in-Publication entry Title: Connected and disconnected in Viet Nam : remaking social relations in a post-socialist nation / editor Philip Taylor. ISBN: 9781925022926 (paperback) 9781760460006 (ebook) Subjects: Social interaction--Vietnam. Vietnam--Social conditions--21st century. Vietnam--Social life and customs--21st century. Other Creators/Contributors: Taylor, Philip, 1962- editor. Dewey Number: 959.7044 All rights reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying or otherwise, without the prior permission of the publisher. Cover design and layout by ANU Press. Cover photograph: Monk on Sam Mountain with iPad by Philip Taylor. This edition © 2016 ANU Press Contents Preface . vii Introduction: An Overture to New Ethnographic Research on Connection and Disconnection in Vietnam . 1 Philip Taylor 1 . Social Relations, Regional Variation, and Economic Inequality in Contemporary Vietnam: A View from Two Vietnamese Rural Communities . 41 Hy V . Luong 2 . The Dynamics of Return Migration in Vietnam’s Rural North: Charity, Community and Contestation . 73 Nguyen Thi Thanh Binh 3 . Women as Fish: Rural Migration and Displacement in Vietnam . 109 Linh Khanh Nguyen 4 . ‘Here, Everyone is Like Everyone Else!’: Exile and Re-emplacement in a Vietnamese Leprosy Village . -

Vietnamese Cuisine Provides an Interesting Experience for Most Tourists and Foodies Because of Its Subtle Flavours and Outstanding Diversity

Publisher Dr KKJohan Editor in Chief Chew Bee Peng Editorial Team Francis Leong Ian Gregory Edward Masselamani Nur’Ain MC Nurilya Anis Rahim Gerald Chuah Creative Manager Ibtisam Basri Assistant Creative Manager Mohd Shahril Hassan Senior Creative Designer Mohd Zaidi Yusof Multimedia Designer Zulhelmi Yarabi Project Manager Lau Swee Ching Secretariat Kalwant Kaur accept nothing less The BrandLaureate Special Edition World Awards 2017 1st Edition : March 2018 it’s the brandlaureate awards Published by: TBL Brand Awards Sdn Bhd 39A, SS21/60, Damansara Utama, 47400 Petaling Jaya, Selangor Tel: 603-77100348 Fax: 603-77100350 Email: [email protected] or nothing Printed by: Percetakan Skyline Sdn Bhd 35 & 37, Jalan 12/32B, TSI Business Industrial Park, - DR. KKJOHAN Batu 6 1/2, Off Jalan Kepong, 52000 Kuala Lumpur Tel: 03-6257 4824 / 1217 Fax: 03-6257 7525 / 1216 Email: [email protected] 3 THE ASIA PACIFIC BRANDS FOUNDATION Founded in 2005, the Asia Pacific Brands Foundation (APBF) is a non-profit organization dedicated to developing brands in a myriad of business backdrops. Led by its Patron, H.E. Tun Dr. Mahathir Mohamad, Malaysia’s fourth Prime Minister, together with a Board of Governors who are experienced captains of industries and established brand icons. The power of branding is a visual, auditory and sensory experience which is undoubtedly vital to the success of brands. Brands are catalysts that transcend achieving objectives, making profits or establishing one’s status so that it appeals to consumers. In reality, consumers’ buying preferences are determined by the way brands attract and engage them. It is crucial that organizations realize the significance of brands and branding.