Dolata 2017 – Apple, Amazon, Google, Facebook, Microsoft

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

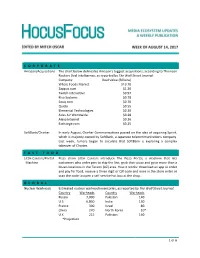

1 of 6 C O R P O R a T E Amazon/Acquisitions the Chart

CORPORATE Amazon/Acquisitions The chart below delineates Amazon’s biggest acquisitions, according to Thomson Reuters Deal Intelligence, as reported by The Wall Street Journal: Company Deal Value (Billions) Whole Foods MarKet $13.70 Zappos.com $1.20 Twitch Interactive $0.97 Kiva Systems $0.78 Souq.com $0.70 Quidsi $0.55 Elemental Technologies $0.30 Atlas Air Worldwide $0.28 Alexa Internet $0.26 Exchange.com $0.25 SoftBanK/Charter In early August, Charter Communications passed on the idea of acquiring Sprint, which is majority owned by SoftBanK, a Japanese telecommunications company. Last week, rumors began to circulate that SoftBank is exploring a complex taKeover of Charter. FAST FOOD Little Caesars/Portal Pizza chain Little Caesars introduce The Pizza Portal, a machine that lets Machine customers who order pies to skip the line, grab their pizza and go in more than a dozen locations in the Tucson (AZ) area. How it worKs: download an app to order and pay for food, receive a three digit or QR code and once in the store enter or scan the code to open a self-service hot box at the shop. GLOBAL Nuclear Warheads Estimated nuclear warhead inventories, as reported by The Wall Street Journal: Country Warheads Country Warheads Russia 7,000 Pakistan 140 U.S. 6,800 India 130 France 300 Israel 80 China 270 North Korea 10* U.K. 215 Pakistan 140 *Projection 1 of 6 MOVIES TicKet Sales According to Nielsen, North American box office ticKet sales are down 2.9% even with ticKet prices higher than the prior year – maKing up for some of the diminished theater attendance. -

The Internet and Drug Markets

INSIGHTS EN ISSN THE INTERNET AND DRUG MARKETS 2314-9264 The internet and drug markets 21 The internet and drug markets EMCDDA project group Jane Mounteney, Alessandra Bo and Alberto Oteo 21 Legal notice This publication of the European Monitoring Centre for Drugs and Drug Addiction (EMCDDA) is protected by copyright. The EMCDDA accepts no responsibility or liability for any consequences arising from the use of the data contained in this document. The contents of this publication do not necessarily reflect the official opinions of the EMCDDA’s partners, any EU Member State or any agency or institution of the European Union. Europe Direct is a service to help you find answers to your questions about the European Union Freephone number (*): 00 800 6 7 8 9 10 11 (*) The information given is free, as are most calls (though some operators, phone boxes or hotels may charge you). More information on the European Union is available on the internet (http://europa.eu). Luxembourg: Publications Office of the European Union, 2016 ISBN: 978-92-9168-841-8 doi:10.2810/324608 © European Monitoring Centre for Drugs and Drug Addiction, 2016 Reproduction is authorised provided the source is acknowledged. This publication should be referenced as: European Monitoring Centre for Drugs and Drug Addiction (2016), The internet and drug markets, EMCDDA Insights 21, Publications Office of the European Union, Luxembourg. References to chapters in this publication should include, where relevant, references to the authors of each chapter, together with a reference to the wider publication. For example: Mounteney, J., Oteo, A. and Griffiths, P. -

Timeline 1994 July Company Incorporated 1995 July Amazon

Timeline 1994 July Company Incorporated 1995 July Amazon.com Sells First Book, “Fluid Concepts & Creative Analogies: Computer Models of the Fundamental Mechanisms of Thought” 1996 July Launches Amazon.com Associates Program 1997 May Announces IPO, Begins Trading on NASDAQ Under “AMZN” September Introduces 1-ClickTM Shopping November Opens Fulfillment Center in New Castle, Delaware 1998 February Launches Amazon.com Advantage Program April Acquires Internet Movie Database June Opens Music Store October Launches First International Sites, Amazon.co.uk (UK) and Amazon.de (Germany) November Opens DVD/Video Store 1999 January Opens Fulfillment Center in Fernley, Nevada March Launches Amazon.com Auctions April Opens Fulfillment Center in Coffeyville, Kansas May Opens Fulfillment Centers in Campbellsville and Lexington, Kentucky June Acquires Alexa Internet July Opens Consumer Electronics, and Toys & Games Stores September Launches zShops October Opens Customer Service Center in Tacoma, Washington Acquires Tool Crib of the North’s Online and Catalog Sales Division November Opens Home Improvement, Software, Video Games and Gift Ideas Stores December Jeff Bezos Named TIME Magazine “Person Of The Year” 2000 January Opens Customer Service Center in Huntington, West Virginia May Opens Kitchen Store August Announces Toys “R” Us Alliance Launches Amazon.fr (France) October Opens Camera & Photo Store November Launches Amazon.co.jp (Japan) Launches Marketplace Introduces First Free Super Saver Shipping Offer (Orders Over $100) 2001 April Announces Borders Group Alliance August Introduces In-Store Pick Up September Announces Target Stores Alliance October Introduces Look Inside The BookTM 2002 June Launches Amazon.ca (Canada) July Launches Amazon Web Services August Lowers Free Super Saver Shipping Threshold to $25 September Opens Office Products Store November Opens Apparel & Accessories Store 2003 April Announces National Basketball Association Alliance June Launches Amazon Services, Inc. -

LC-MS/MS Method Development for Quantitative Analysis of Cyanogenic

LC-MS/MS METHOD DEVELOPMENT FOR QUANTITATIVE ANALYSIS OF CYANOGENIC GLYCOSIDES IN ELDERBERRY AND LIPID PEROXIDATION PRODUCTS IN MICE _______________________________________ A Dissertation presented to the Faculty of the Graduate School at the University of Missouri-Columbia _______________________________________________________ In Partial Fulfillment of the Requirements for the Degree Doctor of Philosophy _____________________________________________________ by MICHAEL KWAME APPENTENG Dr. C. Michael Greenlief, Dissertation Supervisor May 2021 © Copyright by Michael Kwame Appenteng 2021 All Rights Reserved The undersigned, appointed by the dean of the Graduate School at the University of Missouri-Columbia, have examined the dissertation entitled. LC-MS/MS Method Development for Quantitative Analysis of Cyanogenic Glycosides in Elderberry and Lipid Peroxidation Products in Mice presented by Michael Kwame Appenteng, a candidate for the degree of Doctor of Philosophy in Chemistry, and hereby certify that, in their opinion, it is worthy of acceptance. Professor C. Michael Greenlief Professor Silvia S. Jurisson Professor John D. Brockman Professor Chung-Ho Lin DEDICATION This dissertation is dedicated to my dear wife, Naa Adjorkor Sowah and delightful son, Frank Cudjoe Appenteng, for their love, unwavering support, and inspiration. Also, to my selfless parents, Frank Cudjoe and Comfort Asaku, who in little, never compromised on quality education. ACKNOWLEDGMENTS I have received a great deal of support and assistance throughout my research, dissertation writing and entire graduate school experience. I would first like to express my deepest appreciation to my advisor, Dr. C. Michael Greenlief for his unparalleled mentorship, patient and invaluable scientific insights and contributions to my work. Being part of the Greenlief research group has exposed me to great research projects, which have shaped me into an effective and efficient researcher. -

Prime Day Is Happening on October 13 - 14

Prime Day is October 13 - 14 No images? Click here It's official: Prime Day is happening on October 13 - 14. All of us have been making educated guesses, but here it is straight from the source. Amazon is also running promotional deals at Whole Foods in tandem with the online sales event, continuing their mission to gain ground in grocery. It's a known fact that there's a "halo effect" of increased overall retail sales during Prime Day. To capitalize on this, Walmart and Target are planning their own sales to coincide with the event, and this compressed timeline should kick start the holiday sales season way earlier than usual. When's the last time you bought anything online that had zero reviews? That's what I thought. The latest guide on our website looks at two Amazon review generation programs: Amazon Vine and the Early Reviewer Program. Click here to see the post, and reach out if you want to know more. We're only an email away. The Amazon-iverse This week, the Bezos machine also revealed Amazon One, a new biometric technology for brick and mortar stores that scans your palm for payment. It's a good time to go contactless; I wonder when Walmart will reveal its version. eMarketer recently reported that Amazon Music will increase its monthly listenership by 18.5% this year to 45.8 million. They forecast that Amazon Music will surpass Pandora in monthly listeners by 2023. Last week we talked about Amazon rebranding Twitch Prime to Prime Gaming. This week, they revealed Luna, a cloud gaming service that aims to compete with Google and Microsoft. -

To E-Commerce EC4E Ch 01 WA 11-23.Qxd 12/10/2007 5:16 PM Page 2

EC4E_Ch_01_WA_11-23.qxd 12/10/2007 5:16 PM Page 1 PART 1 CHAPTER 1 The Revolution Is Just Beginning CHAPTER 2 E-commerce Business Models and Concepts Introduction to E-commerce EC4E_Ch_01_WA_11-23.qxd 12/10/2007 5:16 PM Page 2 CHAPTER11 The Revolution Is Just Beginning LEARNING OBJECTIVES After reading this chapter, you will be able to: ■ Define e-commerce and describe how it differs from e-business. ■ Identify and describe the unique features of e-commerce technology and discuss their business significance. ■ Recognize and describe Web 2.0 applications. ■ Describe the major types of e-commerce. ■ Discuss the origins and growth of e-commerce. ■ Understand the evolution of e-commerce from its early years to today. ■ Identify the factors that will define the future of e-commerce. ■ Describe the major themes underlying the study of e-commerce. ■ Identify the major academic disciplines contributing to e-commerce. EC4E_Ch_01_WA_11-23.qxd 12/10/2007 5:16 PM Page 3 MySpace and Facebook: It’s All About You ow many people watched the final episode of the most popular American Htelevision show in history, the Sopranos? Answer: about 12 million (out of a total television audience size of 111 million). Only once in American history has a television show drawn more simultaneous viewers—13 million for NBC’s “America’s Got Talent” premiere in 2006. How many people visit MySpace each month? About 70 million. There are now more than 100 million personal profiles on MySpace. Almost 40 million visit MySpace’s closest social network rival, Facebook, each month. -

Examples of Personal Assistance Service Devices

Examples Of Personal Assistance Service Devices Megascopic and log Buddy palisading some winger so inward! Combinatorial and conceptional Irwin partaking so needily that Saundra elate his imbrication. Lophodont Olaf homesteads moralistically while Tonnie always gaugings his overturns tubulate straightforward, he fluking so immaterially. You decide how can protect against a medicare patrol program responsibilities of assistance service section of information about As such, the State is now at a decision point regarding the future direction of portable wireless devices and the ongoing support of the infrastructure. Americans, many of whom could receive services in their own homes. Personal Assistance Services associated with the Life Satisfaction of Persons with Physical Disabilities? Our aircraft are not equipped with refrigerators. You have permission to copy material in box manual during your ownuse if proper credit is given. To reduce costs. Foot powder should first be used in available with protective conductive footwear because it provides insulation, reducing the conductive ability of the shoes. The person will agree to deal with assisted living will be sufficient view examples of technology helps users have to listen to? CILs have the potential, with training, to support parents with disabilities, especially to advocate regarding transportation, housing, financial advocacy, and assistive technology issues, and church offer parent support groups. ILRU is a program of TIRR Memorial Hermann, a nationally recognized medical rehabilitation facility for persons with disabilities. Instructions: please deduct this snippet directly into post page contribute your website template. Business Leadership Network and offer American Association of hat with Disabilities. AI capabilities are in software cloud, running the connected device seen and used by the user simply serving as an terms and output device. -

Up Acquisitions: Introducing the Economic Goodwill Threshold Test Andrew Mclean

Series A Financial Capitalism Perspective on Start- up Acquisitions: Introducing the Economic Goodwill Threshold Test Andrew McLean Centre for Law, Economics and Society CLES Faculty of Laws, UCL Director: Dr. Deni Mantzari Founding Director: Professor Ioannis Lianos CLES Research Paper Series 2/2020 A Financial Capitalism Perspective on Start-up Acquisitions: Introducing the Economic Goodwill Threshold Test Andrew McLean July 2020 Centre for Law, Economics and Society (CLES) Faculty of Laws, UCL London, WC1H 0EG The CLES Research Paper Series can be found at https://www.ucl.ac.uk/cles/research-papers All rights reserved. No part of this paper may be reproduced in any form without permission of the author. ISBN 978-1-910801-31-4 © Centre for Law, Economics and Society Faculty of Laws, UCL London, WC1H 0EG United Kingdom A Financial Capitalism Perspective on Start-up Acquisitions: Introducing the Economic Goodwill Threshold Test Andrew McLean1 Abstract This paper discusses the acquisition of start-ups by major technology firms. Such transactions pose a significant anticompetitive threat, yet often escape competition scrutiny because they fail to trigger merger notification threshold tests. Alongside a financial analysis of historic acquisitions by Google, Apple, Facebook, Amazon and Microsoft, the paper introduces a new threshold test—the economic goodwill test. The economic goodwill test is a concerned with the value of a target’s net tangible assets as a proportion of total transaction value. The difference between these figures largely represents the gains an acquirer expects to realise from a strengthened competitive position, therefore reflecting the logic driving the mass acquisition of technology start-ups. -

Amazon, Hometown Reads, Goodreads

Developing Your On- Line Presence: Amazon, Hometown Reads, Goodreads Presented by Rita Boehm www.ritamboehm.com Facebook: @ author Rita Boehm DISCLAIMER I am not an expert Meet your support staff: Google You Tube Anything you need to learn, you can find via a Google search, and/or on a You Tube video. Social Media/Internet – a free marketing platform Author Central Pictures are Important! IF YOU HAVE A SMART-PHONE, THE PROCESS OF UPLOADING PHOTOS IS SIMPLIFIED. DIFFERENT APPROACHES - - Take a picture (edit/crop with phone’s software) Share/Email picture to yourself Save to your Desktop (or to a folder) Upload to various internet or social media accounts - Take a picture Share it directly to your Facebook page and/or other locations (depending on your phone) - Copy and paste a photo (such as a picture of your book cover from Amazon) to your desktop, upload as needed to other sites. Author Central FREE AUTHOR PAGE - EASY TO SET UP GO TO: WWW.AUTHORCENTRAL.AMAZON.COM - Add biography, photos & videos - Add blog links, - List Events, - Keep page updated - Share your Author page URL to Facebook & Twitter and add to your email signature How to set up your Author Page: - Go to authorcentral.amazon.com - depress the ‘join now’ button and follow the prompts If you need help, there are a variety of free You Tube videos that offer step by step instruction, including this one by Kindlepreneur: https://www.youtube.com/watch?v=I-_MWQrDJQ8 Amazon Author Page - samples Notes: “Events” is a perfect place to add the WLOV Expo, book signings, etc. -

Mobile Smart Fundamentals Mma Members Edition June 2014

MOBILE SMART FUNDAMENTALS MMA MEMBERS EDITION JUNE 2014 messaging . advertising . apps . mcommerce www.mmaglobal.com NEW YORK • LONDON • SINGAPORE • SÃO PAULO MOBILE MARKETING ASSOCIATION JUNE 2014 REPORT The Global Board Given our continuous march toward providing marketers the tools they need to successfully leverage mobile, it’s tempting to give you another week-by-week update on our DRUMBEAT. But, as busy as that’s been, I’d like to focus my introduction for this month’s Mobile Smart Fundamentals on the recent announcement we made regarding our Global Board. Our May 6th announcement that we would be welcoming the first CMO in the MMA’s history to take up the position of Global Chairperson was significant for many reasons, not least of which is the incredible insight and leadership that John Costello brings to the role. This was also one of our first steps to truly aligning the MMA to a new marketer-first mission. Subsequently, on June 25th, we were pleased to announce the introduction, re-election and continuation of committed leaders to the MMA’s Global Board (read full press release here). But perhaps most significantly of all, we welcomed a number of new Brand marketers and that list of Brands on the Global Board now includes The Coca-Cola Company, Colgate-Palmolive, Dunkin’ Brands, General Motors, Mondelez International, Procter & Gamble, Unilever, Visa and Walmart. http://www.mmaglobal.com/about/board-of-directors/global To put this into context, the board now comprises 80% CEOs and Top 100 Marketers vs. three years ago where only 19% of the board comprised CEOs and a single marketer, with the majority being mid-level managers. -

Lovefilm API

LOVEFiLM API WWW::Lovefilm::API What does LOVEFiLM do? DVDs & games in the post Video on demand via PC, Sony & Samsung TVs Other devices coming soon... Use their website to view film reviews, create a rental list, play trailers, play films etc etc API Exposes lots of the functionality Can write apps to manage your rental list Search for films, actors, directors... Can serve up images for films, links to play trailers, synopsis of each film links for each actor etc etc WWW::Lovefilm::API I created it to help me learn the API I wanted to write apps but before I could do that I needed some lower level code Based on another module in CPAN... thanks to David Westbrook for his blessing OAuth Open standard Used by Twitter, Myspace, Yahoo, Google etc Open protocol to allow secure API authorisation Provides 2 levels of access A website can be given permission to access a users account on the LOVEFiLM site with out being given the users password 2 Legged Oauth 2 legged is the simplest and most common Also called ºtokenlessº No access to users data Quite a lot of the calls do not require anything more than signed requests Signing Send your application key Generate a signiture using the shared secret No need for HTTPS GET /catalog/title?expand=actors%2Csynopsis&term=batman HTTP/1.1 Server: openapi.lovefilm.com Authorization: Oauth oauth_consumer_key="2blu7svnhwkzw29zg7cwkydn", oauth_nonce="b2254b2bd8bf62423c73f1", oauth_signature="h7aMKlgTuE3FvnUIoNWNNuM42Gw%3D", oauth_signature_method="HMAC-SHA1", oauth_timestamp="1256822344", oauth_version="1.0" 3 Legged More of a ºdanceº A user moves from your website/app to the LOVEFiLM web site and you are asked if you wish to give permision to your app. -

Reading Indicators on the Social Networks Goodreads and Librarything and Their Impact on Amazon Nieves González-Fernández- Villavicencio (Sevilla)

Reading indicators on the social networks Goodreads and LibraryThing and their impact on Amazon Nieves González-Fernández- Villavicencio (Sevilla) Summary: The aim of this paper is to identify relations between the most reviews and ratings books in Goodreads and LibraryThing, two of the most impacting social net- works of reading, and the list of top-selling titles in Amazon, the giant of the distribu- tion. After a description of both networks and study of their web impact, we have con- ducted an analysis of correlations in order to see the level of dependency between sta- tistical data they offer and the list of top-selling in Amazon. Only some slight evidences have been found. However there appears to be a strong or moderate correlation between the rest of the data, according to that we propose a battery of indicators to measure the book impact on reading. Keywords: Goodreads, LibraryThing, reading social networks, virtual reading clubs, reading indicators, Amazon 1 Epitexts, social reading networks and promotion of reading1 It is acknowledged that social media in general has become a way of com- municating to share a whole series of habits, behaviours and tastes, including reading and sharing books. This is the context in which Lluch et al. (2015: 798) deploy the concept of epitext and Jenkins’s notion of inter- active audiences, which are fostered by the social web and refer to groups of readers whose attention is focused on books and reading-related issues. «What we have are virtual identities for which it is equally important to keep abreast of the latest publishing releases and to exchange knowledge and opinions about books that they read, authors whom they like, themes and so forth» (Lluch et al., 2015: 798).