Audiovisual Content Streaming: Setting the Scene

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

LIVA - a Software Live Video & Audio Production Framework Team’S Presentation

Presentation of the Stars4Media Initiative: LIVA - a software live video & audio production framework Team’s presentation Video Snackbar Hub: exchanging knowledge on new technologies, ideas and workflows to support content creators and part of the Future Media Hubs. An international network of media companies that strengthen each other and collaborate on innovative and/or strategic topics. Chosen representatives for the Stars4Media-project were: ● Morten Brandstrup, Head of news technology – TV2 Denmark ● Hugo Ortiz, IP Broadcast Coach – RTBF ● Floris Daelemans, Innovation Researcher – VRT ● Henrik Vandeput, Software developer (freelancer) – VRT ● Sarah Geeroms, Strategic partnerships and Head of FMH – VRT ● Coralie Villeret, Software engineer and UX designer – RTBF [email protected] Initiative’s summary ● To explore the boundaries of standard broadcast technology ● Building custom components in a creative software (TouchDesigner) ● Exploring the significant profit of a new workflow (both financially and creatively) ● Learning some interesting insights and different approaches from junior profiles ● Expanding our skill-sets https://www.videosnackbarhub.com [email protected] Initiative’s results ● Added experience to the junior profiles within our media organizations ● Resourced our community of like-minded media players ● Resulting components with lots of possibilities ● Helped us explore Github and TouchDesigner in-depth ● Applied new and creative software to our broadcast ● Received constructive feedback from our international -

Contribution of Public Service Media in Promoting Social Cohesion

COUNCIL CONSEIL OF EUROPE DE L’EUROPE Contribution of public service media in promoting social cohesion and integrating all communities and generations Implementation of Committee of Ministers Recommendation Rec (97) 21 on media and the promotion of a culture of tolerance Group of Specialists on Public Service Media in the Information Society (MC-S-PSM) H/Inf (2009) 5 Contribution of public service media in promoting social cohesion and integrating all communities and generations Implementation of Committee of Ministers’ Recommendation Rec (97) 21 on media and the promotion of a culture of tolerance Report prepared by the Group of Specialists on Public Service Media in the Information Society (MC-S-PSM), November 2008 Directorate General of Human Rights and Legal Affairs Council of Europe Strasbourg, June 2009 Édition française : La contribution des médias de service public à la promotion de la cohésion sociale et a l’intégration de toutes les communautés et générations Directorate General of Human Rights and Legal Affairs Council of Europe F-67075 Strasbourg Cedex http://www.coe.int/ © Council of Europe 2009 Printed at the Council of Europe Contents Executive summary . .5 Introduction . .5 Key developments . .6 Workforce . 6 Requirements . .11 Content and services . 13 Conclusions, recommendations and proposals for further action . 18 Conclusions . .18 Recommendations and proposals for further action . .20 Appendix A. Recommendation No. R (97) 21 . 22 Recommendation No. R (97) 21 on Appendix to Recommendation No. R the media and the promotion of a (97) 21 . .22 culture of tolerance . .22 Appendix B. Questionnaire on public service media and the promotion of a culture of tolerance . -

The Rai Studio Di Fonologia (1954–83)

ELECTRONIC MUSIC HISTORY THROUGH THE EVERYDAY: THE RAI STUDIO DI FONOLOGIA (1954–83) Joanna Evelyn Helms A dissertation submitted to the faculty at the University of North Carolina at Chapel Hill in partial fulfillment of the requirements for the degree of Doctor of Philosophy in the Department of Music. Chapel Hill 2020 Approved by: Andrea F. Bohlman Mark Evan Bonds Tim Carter Mark Katz Lee Weisert © 2020 Joanna Evelyn Helms ALL RIGHTS RESERVED ii ABSTRACT Joanna Evelyn Helms: Electronic Music History through the Everyday: The RAI Studio di Fonologia (1954–83) (Under the direction of Andrea F. Bohlman) My dissertation analyzes cultural production at the Studio di Fonologia (SdF), an electronic music studio operated by Italian state media network Radiotelevisione Italiana (RAI) in Milan from 1955 to 1983. At the SdF, composers produced music and sound effects for radio dramas, television documentaries, stage and film operas, and musical works for concert audiences. Much research on the SdF centers on the art-music outputs of a select group of internationally prestigious Italian composers (namely Luciano Berio, Bruno Maderna, and Luigi Nono), offering limited windows into the social life, technological everyday, and collaborative discourse that characterized the institution during its nearly three decades of continuous operation. This preference reflects a larger trend within postwar electronic music histories to emphasize the production of a core group of intellectuals—mostly art-music composers—at a few key sites such as Paris, Cologne, and New York. Through close archival reading, I reconstruct the social conditions of work in the SdF, as well as ways in which changes in its output over time reflected changes in institutional priorities at RAI. -

Increased Transparency and Efficiency in Public Service Broadcasting

Competition Policy Newsletter Increased transparency and efficiency in public service AID STATE broadcasting. Recent cases in Spain and Germany (1) Pedro Dias and Alexandra Antoniadis Introduction The annual contribution granted to RTVE was made dependent upon the adoption of measures Since the adoption of the Broadcasting Communi- to increase efficiency. The Spanish authorities cation in 200, the Commission followed a struc- commissioned a study on the financial situation tured and consistent approach in dealing with of RTVE which revealed that the — at the time numerous complaints lodged against the financ- — existing workforce exceeded what was neces- ing of public service broadcasters in Europe. It sary for the fulfilment of the public service tasks. reviewed in particular the existing financing Agreement could be reached between the Span- regimes and discussed with Member States meas- ish authorities, RTVE and trade unions on a sig- ures to ensure full compliance with the EU State nificant reduction of the workforce through early aid rules. The experience has been positive: Sev- retirement measures. The Spanish State decided to eral Member States have either already changed or finance these measures, thus alleviating RTVE of committed themselves to changing the financing costs it would normally have to bear. The savings rules for public service broadcasters to implement in terms of labour costs and consequently pub- fundamental principles of transparency and pro- lic service costs of RTVE exceeded the financial portionality (2). burden of the Spanish State due to the financing of the workforce reduction measures. The Com- The present article reviews the two most recent mission approved the aid under Article 86 (2) EC decisions in this field which are examples of Treaty, also considering the overall reduction of increased efficiency and transparency in public State aid to the public service broadcaster (). -

Press Release Potsdam Declaration

Press Release Potsdam 19.10.2018 Potsdam Declaration signed by 21 public broadcasters from Europe “In times such as ours, with increased polarization, populism and fixed positions, public broadcasters have a vital role to play across Europe.” A joint statement, emphasizing the inclusive rather than divisive mission of public broadcasting, will be signed on Friday 19th October 2018 in Potsdam. Cilla Benkö, Director General of Sveriges Radio and President of PRIX EUROPA, and representatives from 20 other European broadcasters are making their appeal: “The time to stand up for media freedom and strong public service media is now. Our countries need good quality journalism and the audiences need strong collective platforms”. The act of signing is taking place just before the Awards Ceremony of this year’s PRIX EUROPA, hosted by rbb in Berlin and Potsdam from 13-19 October under the slogan “Reflecting all voices”. The joint declaration was initiated by the Steering Committee of PRIX EUROPA, which unites the 21 broadcasters. Potsdam Declaration, 19 October 2018 (full wording) by the 21 broadcasters from the PRIX EUROPA Steering Committee: In times such as ours, with increased polarization, populism and fixed positions, public broadcasters have a vital role to play across Europe. It has never been more important to carry on offering audiences a wide variety of voices and opinions and to look at complex processes from different angles. Impartial news and information that everyone can trust, content that reaches all audiences, that offers all views and brings communities together. Equally important: Public broadcasters make the joys of culture and learning available to everyone, regardless of income or background. -

European Public Service Broadcasting Online

UNIVERSITY OF HELSINKI, COMMUNICATIONS RESEARCH CENTRE (CRC) European Public Service Broadcasting Online Services and Regulation JockumHildén,M.Soc.Sci. 30November2013 ThisstudyiscommissionedbytheFinnishBroadcastingCompanyǡYle.Theresearch wascarriedoutfromAugusttoNovember2013. Table of Contents PublicServiceBroadcasters.......................................................................................1 ListofAbbreviations.....................................................................................................3 Foreword..........................................................................................................................4 Executivesummary.......................................................................................................5 ͳIntroduction...............................................................................................................11 ʹPre-evaluationofnewservices.............................................................................15 2.1TheCommission’sexantetest...................................................................................16 2.2Legalbasisofthepublicvaluetest...........................................................................18 2.3Institutionalresponsibility.........................................................................................24 2.4Themarketimpactassessment.................................................................................31 2.5Thequestionofnewservices.....................................................................................36 -

The Public Service Broadcasting Culture

The Series Published by the European Audiovisual Observatory What can you IRIS Special is a series of publications from the European Audiovisual Observatory that provides you comprehensive factual information coupled with in-depth analysis. The expect from themes chosen for IRIS Special are all topical issues in media law, which we explore for IRIS Special in you from a legal perspective. IRIS Special’s approach to its content is tri-dimensional, with overlap in some cases, depending on the theme. terms of content? It offers: 1. a detailed survey of relevant national legislation to facilitate comparison of the legal position in different countries, for example IRIS Special: Broadcasters’ Obligations to Invest in Cinematographic Production describes the rules applied by 34 European states; 2. identifi cation and analysis of highly relevant issues, covering legal developments and trends as well as suggested solutions: for example IRIS Special, Audiovisual Media Services without Frontiers – Implementing the Rules offers a forward-looking analysis that will continue to be relevant long after the adoption of the EC Directive; 3. an outline of the European or international legal context infl uencing the national legislation, for example IRIS Special: To Have or Not to Have – Must-carry Rules explains the European model and compares it with the American approach. What is the source Every edition of IRIS Special is produced by the European Audiovisual Observatory’s legal information department in cooperation with its partner organisations and an extensive The Public of the IRIS Special network of experts in media law. The themes are either discussed at invitation-only expertise? workshops or tackled by selected guest authors. -

Minority-Language Related Broadcasting and Legislation in the OSCE

University of Pennsylvania ScholarlyCommons Other Publications from the Center for Global Center for Global Communication Studies Communication Studies (CGCS) 4-2003 Minority-Language Related Broadcasting and Legislation in the OSCE Tarlach McGonagle Bethany Davis Noll Monroe Price University of Pennsylvania, [email protected] Follow this and additional works at: https://repository.upenn.edu/cgcs_publications Part of the Critical and Cultural Studies Commons Recommended Citation McGonagle, Tarlach; Davis Noll, Bethany; and Price, Monroe. (2003). Minority-Language Related Broadcasting and Legislation in the OSCE. Other Publications from the Center for Global Communication Studies. Retrieved from https://repository.upenn.edu/cgcs_publications/3 This paper is posted at ScholarlyCommons. https://repository.upenn.edu/cgcs_publications/3 For more information, please contact [email protected]. Minority-Language Related Broadcasting and Legislation in the OSCE Abstract There are a large number of language-related regulations (both prescriptive and proscriptive) that affect the shape of the broadcasting media and therefore have an impact on the life of persons belonging to minorities. Of course, language has been and remains an important instrument in State-building and maintenance. In this context, requirements have also been put in place to accommodate national minorities. In some settings, there is legislation to assure availability of programming in minority languages.1 Language rules have also been manipulated for restrictive, sometimes punitive ends. A language can become or be made a focus of loyalty for a minority community that thinks itself suppressed, persecuted, or subjected to discrimination. Regulations relating to broadcasting may make language a target for attack or suppression if the authorities associate it with what they consider a disaffected or secessionist group or even just a culturally inferior one. -

Mediaset España Sets New Historical Record with 18,5 Million Unique Users in May

Madrid, 12th June, 2013 According to the monthly report of OJD MEDIASET ESPAÑA SETS NEW HISTORICAL RECORD WITH 18,5 MILLION UNIQUE USERS IN MAY • In one year, the media group has increased its traffic by 11.2% compared to May 2012. Telecinco.es has grown by 9.2%, and Cuatro.com 20.6% and Divinity.es has registered an excellent growth of 44.5% • Exceeding Grupo RTVE, by almost 1.8 million monthly unique users • Telecinco.es the third most watched national media in the overall ranking of digital media audited by OJD, surpassed only by Marca.com and Elmundo.es • In addition, Telecinco is a leading in social share in May and became the first channel to exceed 4 million comments a month Once again, Mediaset España sets new record Internet audience to record 18.5 million unique users in May, the month in which Telecinco.es and Divinity.es have also beaten their own record highs with 15.8 million and 1.5 million unique users, respectively, according to the audited report of OJD. In one year, the audiovisual group preferred by users has increased Internet traffic (monthly unique visitors) by 11.2% compared to May 2012. Per site, the growth was 9.2% for Telecinco.es, Cuatro.com 20.6% and an excellent 44.5% for Divinity.es. Mediaset España continues to be absolute leader in Internet among Spanish television operators, both monthly unique browsers (18,483,679 users) and daily traffic (1,487,468 users), ahead of its nearest competitor (*), RTVE Group, which includes all RTVE and RNE sites - by almost 1.8 million monthly unique browsers and 337 808 unique visitors per day. -

Rightstrade Partners with RTVE and Movistar+ to Become Leading Spanish- Language Content Marketplace

RightsTrade 12001 Ventura Pl, #500 Studio City, CA 91604 +1 (818) 762-5811 [email protected] RightsTrade partners with RTVE and Movistar+ to become leading Spanish- language content marketplace The online platform will make thousands of hours of Spanish-language content available to its 5,000 registered buyers in 140 countries RightsTrade, the largest online B2B marketplace for film and television rights, has been making 2018 a year for international growth. By adding over 25,000 hours of film and TV programming from RTVE (Spain’s public broadcasting corporation), Movistar+ (a Telefonica company) and other key Hispanic content providers, RightsTrade has solidified itself as the leading content hub for Spanish-language content. RTVE will make its most well-known programs available to Rightstrade’s wide variety of international content buyers. This agreement offers greater visibility and international exposure to RTVE’s catalog, while further expanding RightsTrade’s international offerings. RTVE programming comprises the public corporation's most recent prime time series, such as 'El Continental', A Different View ('La otra mirada'), 'Detectives' (‘Sabuesos’), ‘Vintage’ ('Gran Reserva'), and 'Treason' (‘Traición’). Documentaries shot in 4K are also available, such as ‘El Prado, a passion for painting’ ('La Pasión del Prado'), and 'Spanish Cities, World Heritage Sites', along with feature films, entertainment and musical programming, among others. According to María Jesús Pérez, RTVE's Director of International Sales, "at a time when Spanish audiovisual content is experiencing an increase in global demand, our alliance with RightsTrade represents a unique opportunity to enhance the international sales of our titles and optimize distribution through its innovative online tools." Movistar+ also joins RightsTrade at this pivotal period of global growth. -

List of Public Broadcasting Decisions

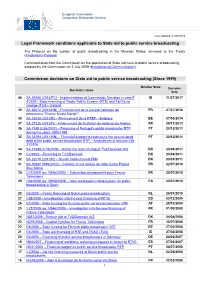

European Commission Competition Directorate-General Last updated: 01/07/2019 Legal Framework conditions applicable to State aid to public service broadcasting The Protocol on the system of public broadcasting in the Member States, annexed to the Treaty (Amsterdam Protocol). Communication from the Commission on the application of State aid rules to public service broadcasting, adopted by the Commission on 2 July 2009 (Broadcasting Communication). Commission decisions on State aid to public service broadcasting (Since 1999) Member State Decision Decision name date 40 SA.39346 (2014/FC) - Implementation of Commission Decision in case E IE 11/07/2017 4/2005 - State financing of Radio Teilifís Éireann (RTÉ) and Teilifís na Gaeilge (TG4) - Ireland 39 SA.36672 (2013/NN) - Financement de la société nationale de FR 27/07/2016 programme "France Media Monde" 38 SA.32635 (2012/E) – Financement de la RTBF – Belgique BE 07/05/2014 37 SA.37136 (2013/N) - Financement de la station de radio locale France FR 08/11/2013 36 SA.7149 (C85/2001) – Financing of Portugal's public broadcaster RTP PT 20/12/2011 during the years 1992-1998 35 SA.33294 (2011/NN) – Financial support to restructure the accumulated PT 20/12/2011 debt of the public service broadcaster RTP – Amendment of decision NN 31/2006 34 SA.27688 (C19/2009) - Aid for the restructuring of TV2/Danmark A/S DK 20/04/2011 33 C2/2003 – Financing of TV2/Danmark DK 20/04/2011 32 SA.32019 (2010/N) – Danish radio channel FM4 DK 23/03/2011 31 SA.30587 (N95/2010) – Création d’une station de radio locale France FR 22/07/2010 Bleu Maine 30 C27/2009 (ex. -

Eurodoc Executive Meeting – an Exclusive Meeting Platform for Documentary Executives and Commissioning Editors

EURODOC EXECUTIVE MEETING – AN EXCLUSIVE MEETING PLATFORM FOR DOCUMENTARY EXECUTIVES AND COMMISSIONING EDITORS Tuesday, 2nd of October 2018 Geneva, Eurodoc for Executives CHANGE IN PUBLIC SERVICE PLATFORM CURATING – MORE THAN ALGORHYTHM ? With Jeroen Depraetere, Head of Television and Future, EBU Curation and algorithms as ways of enhancing our service are definitely something public service should take up (have taken up…), but it seems to be developing very slowly almost everywhere. The news of the planned "Alliance" of France Televisions, ZDF and RAI, or the planned joint streaming service of BBC, Channel4 and ITV make it very clear that also the European public service media have understood that the media landscape will be dominated by big international or global players. The survival for documentary programs and smaller players in this landscape will require co-operation and high quality of not only the content but also the service. We may find ourselves having to create and defend a position not within one national public service broadcaster but a conglomerate of many. LUNCH for Executives only 2.30 PM – 5 PM WELCOME & INTRODUCTION INPUT by Jeroen Depraetere, Head of Television and Future, European Broadcasting Union EBU, Geneva, introducing to the « Alliance » of France Télévision, ZDF and RAI and other public initiatives followed by a discussion INTERNATIONAL CASE STUDYS by our participants from the different services such as ARTE, SRF, HBO etc. THE EURODOC EXECUTIVE’S MEETING Since 2013, Eurodoc also offers an exclusive opportunity to meet amongst Documentary Executives and Commissioning Editors only. This exclusive meeting always takes place on the first day of the Eurodoc session and is curated by Anita Hugi (SRF) for Eurodoc.