Morning Highlight

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

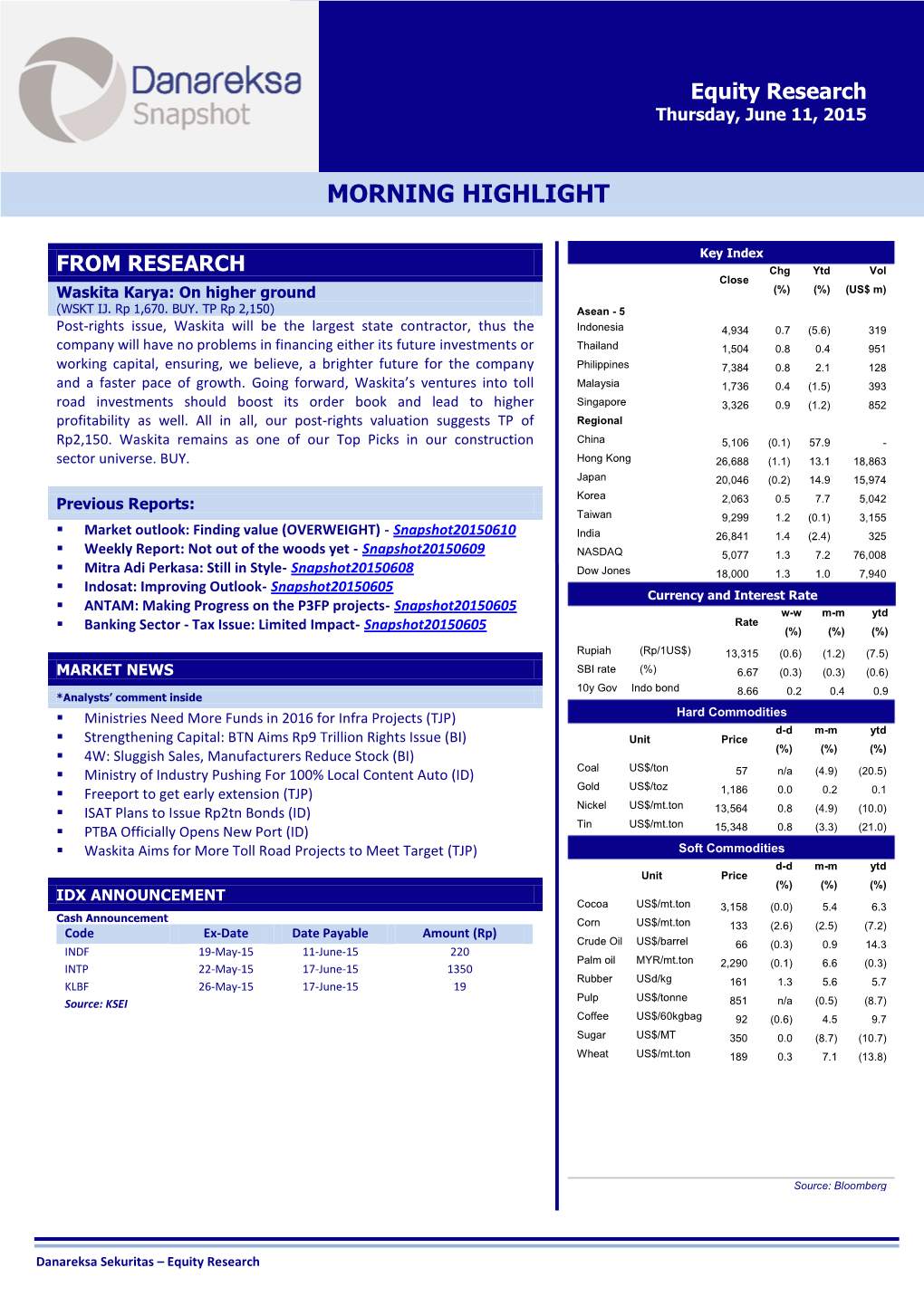

-

JM Update FY 2016

Jasa Marga Update FY 2016 1 List of Content 3 Company in Brief 9 Toll Road Industry in Indonesia 12 Jasa Marga’s Strategic Projects 18 Funding Strategy 22 Financial Highlights 2 I COMPANY IN BRIEF Proven Track Record in Indonesian Toll Road Business Leading toll road operator in Indonesia with 38 years of experience. Start 1978 1983 1984 1986 1987 1988 1990 1991 1998 2001 2003 2009 2011 2013 2014 2015 2016 Operation BORR (Section 2 & 3)(2) Jagorawi Cipularang JORR W2 North Surabaya- Padaleunyi Palikanci (4) (Section 1-4)(2) Gempol- Gempol (2) Jakarta- Surabaya- Pasuruan Ulujami- Bogor Outer Semarang Cikampek Ring Road Mojokerto Pondok Aren (Section 4)(2) Semarang- Belmera BORR Semarang-Solo Solo(2) Jakarta Outer (Section 1)(2) (Section 2)(2) Ring Road Cengkareng- Jakarta-Tangerang (2) (JORR) Gempol- Kunciran (2) Surabaya-Mojokerto Pandaan Kunciran-Serpong(2) Prof. Dr. Ir. (Section 1A)(2) Sedyatmo Jakarta Inner Surabaya-Mojokerto(2) Ring Road (JIRR) Toll Road (1) Semarang-Solo BORR Medan-Kualanamu- Concessions (2) Tebing Tinggi(2) (Section 1)(2) (Section 2A) Solo-Ngawi(2) Ngawi-Kertosono(2) Nusa Dua-Ngurah Rai-Benoa(2) Cinere-Serpong(2) Semarang-Batang(2) Pandaan-Malang(2) Balikpapan-Samarinda(2) Manado-Bitung(2) Jakarta-Cikampek II Elevated(2) Number of 1 2 4 6 7 8 9 10 11 12 13 14 16 17 18 19 19 31 Concessions Total Length (km) under Corresponding 59 84 131 223 246 329 394 437 463 469 527 531 544 554 576 590 593 1.260 Concessions(3) Note: (1) Jakarta Inner Ring Road (JIRR) is comprised of the Cawang-Tomang-Pluit concession granted to Jasa Marga and Cawang-Tanjung Priok-Pluit concession granted to CMNP. -

Indonesian Toll Roads NEUTRAL (Unchanged)

Alpha Asiamoney's 2014 Asiamoney’s Southeast Asia 2013 Finance Asia's Sector flash 2013 2014 Best Best Domestic Best Best Domestic Research Call Equity House Equity House Equity House FMCG Sector 7 April 2015 Indonesian toll roads NEUTRAL (Unchanged) Bob Setiadi E-mail: [email protected] Phone: +6221 250 5081 ext. 3605 Policy updates Exhibit 1. Sector summary Code Ratings Share price +/- P/E EPS grwth . 4 SOEs to construct Trans-Sumatra toll-road sections: Upon obtaining CP TP (%) (x) (%) IDR3.6tn capital injection, Hutama Karya, a non-listed construction SOE, JSMR BUY 7,125 8,000 12.3 30.0 14.9 recently signed a toll-road concession agreement (PPJT) for the 17km Source: Bloomberg, Bahana estimates Based on closing prices on 7 April 2015 Medan-Binjai toll road, one of four Trans Sumatra toll-road sections (exhibit 8), assigned to Hutama Karya based on Presidential Decree No.100/2014. Exhibit 2. Inflation sensitivity to toll revenue Effect on toll-road revenue Inflation rate (%) The government plans to issue a new decree to form a consortium between 2015F 2016F Hutama Karya and three other listed SOEs (Jasa Marga, Waskita Karya and 11.0 2.0% 8.4% 12.0 2.2% 9.1% Wijaya Karya) to develop the Trans-Sumatra toll roads, utilizing the same 13.0 (base case) 2.4% 9.8% scheme that was successful in constructing the Bali Mandara toll road. While 14.0 2.6% 10.5% 15.0 2.8% 11.2% we support government’s plan to accelerate the Trans-Sumatra project, we Source: Bahana estimates; Note: Based on 2-year inflation are awaiting the announcement of the consortium agreements, as the adjustment Trans-Sumatra offers a relatively low IRR (7-17%) which could result in Exhibit 3. -

Mapping and Payment on Tangerang to West Jakarta's Toll Road's Gate Using Non-Determenistic Finite State Automata

Mapping and Payment on Tangerang to West Jakarta’s Toll Road’s Gate Using Non-Determenistic Finite State Automata Deka Primatio D.1, Farrel Irsyad F.2, Kharansyah Tawaddu S.3, M. Rizky Zaldi4, Raul Andrian5 {[email protected], [email protected] 2, [email protected], [email protected] 4, [email protected]} Faculty of Information and Technology, Universitas Multimedia Nusantara, Jl. Scientia Boulevard, Gading Serpong, Tangerang, Banten, Indonesia 15527 1,2,3,4,5 Abstract. In this research, the concept of Non-Deterministic Finite Automata is used for mapping and simulating the payment system for the Tangerang - West Jakarta toll road. Currently, toll road construction is being intensively developed, because it is one of the government's flagship programs, namely infrastructure development. Tolls in Indonesia apply a uniform fare system without priorit izing the calculation of vehicle mileage, the main disadvantage of this system is that it does not take into account the possibility of attracting users who travel short distances by making toll rate differences. Therefore, this study designed a mapping with payment system based on the calculation of the distance traveled by the vehicle from the toll gate in to the toll gate out. The implementation in the form of simulations is carried out using a raptor in the form of a conceptual and systematic flowchart program, and the simulation works effectively, starting from the balance scan to the suitability of the toll gate exit output and the distance traveled. The concept of Non -Deterministic Finite Automata can be a method for creating payment systems and mapping toll gate. -

Review of Developments in Transport in Asia and the Pacific 2005

REVIEW OF DEVELOPMENTS IN TRANSPORT IN ASIA AND THE PACIFIC 2005 United Nations E S C A P ECONOMIC AND SOCIAL COMMISSION FOR ASIA AND THE PACIFIC ESCAP is the regional development arm of the United Nations and serves as the main economic and social development centre for the United Nations in Asia and the Pacific. Its mandate is to foster cooperation between its 53 members and 9 associate members. ESCAP provides the strategic link between global and country-level programmes and issues. It supports Governments of the region in consolidating regional positions and advocates regional approaches to meeting the region’s unique socio-economic challenges in a globalizing world. The ESCAP office is located in Bangkok, Thailand. Please visit our website at www.unescap.org for further information. The shaded areas of the map represent ESCAP members and associate members. REVIEW OF DEVELOPMENTS IN TRANSPORT IN ASIA AND THE PACIFIC 2005 United Nations New York, 2005 ECONOMIC AND SOCIAL COMMISSION FOR ASIA AND THE PACIFIC REVIEW OF DEVELOPMENTS IN TRANSPORT IN ASIA AND THE PACIFIC 2005 United Nations publication Sales No. E.06.II.F.9 Copyright United Nations 2005 All rights reserved Manufactured in Thailand ISBN: 92-1-120461-5 ST/ESCAP/2392 ESCAP WORKS TOWARDS REDUCING POVERTY AND MANAGING GLOBALIZATION Acknowledgements: This document was prepared by the Transport and Tourism Division (TTD), ESCAP, led by the Transport Policy and Tourism Section. Assistance and consultancy inputs were provided by Meyrick and Associates Pty., Limited (www.meyrick.com.au). The Chapter on Air Transport was graciously provided by the International Civil Aviation Organization (ICAO), Bangkok, Thailand. -

Townland Consultants

EXAMPLES OF PROJECTS IN INDONESIA Project TCL Project Description Client Lead Duration Completed Ref. Consultant of Project (year) (months) Master Planning for IP9 TOWNLAND was commissioned to PT. Sumber TOWNLAND 1997 Town Centre undertake the Master Planning of an Mitrarealtindo Development (43 ha) in Innovative Commercial Mixed-Use Complex Kelapa Gading on a 43 ha Site. Post Evaluation of the IP10 Post-Evaluation of a Master Layout Plan for PT. Sumber TOWNLAND 1997 Master Layout Plan and Mitra Gading Apartments and preparation Mitrarealtindo Preparation of a of an alternative Concept Plan for a 12 Concept Plan for storey residential development on a 7 ha Residential Site. Development (7 ha) at Kelapa Gading, Jakarta Urban Design and IP13 TOWNLAND was commissioned to PT. Bakrieland TOWNLAND 1999 Coordination of Master undertake the Urban Design and Master Development, Planning for a 200 ha Planning for the Project, comprising a 200 Tbk New Town Development ha Site about 100 km from Jakarta. The New in Purwakarta Town comprises predominantly residential uses and supporting facilities. Future development includes a business park and a tertiary education facility. Landscape Design for IP4/4 TOWNLAND prepared an Innovative Golf PT. Pulo Mas TOWNLAND 2 2000 Golf Courts Proposal, Court Concept and Framework Landscaping Jaya Pulo Mas, East Jakarta to Golf Court, Driving Range and Ancillary Facilities. Master Layout Planning IP21 TOWNLAND prepared the Master Layout PT. Waringin TOWNLAND 5 2000 for Warehouse and Plan for a 13.5 ha Site within the 100 ha Pluit Multicipta Commercial District Distribution Centre in Northwest Jakarta. Master Plan (13.5 ha) in Uses include light industrial, warehousing Kapuk Kamal Raya, and supporting commercial facilities. -

Annual Report 2018

20 18 Laporan Tahunan Annual Report TOLL INTEGRATION FOR THE BETTER FUTURE PT Marga Lingkar Jakarta PENDAHULUAN PREFACE 01 PT MARGA LINGKAR JAKARTA ANNUAL REPORT 2018 2 IKHTISAR KEUANGAN & PENDAHULUAN OPERASIONAL LAPORAN MANAJEMEN PROFIL PERUSAHAAN PREFACE FINANCIAL & OPERATIONAL MANAGEMENT REPORT COMPANY PROFILE HIGHLIGHTS TOLL INTEGRATION FOR THE BETTER FUTURE Integrasi tarif jalan tol Jakarta Outer Ring Road The Jakarta Outing Ring Road (JORR) toll tariff (JORR) yang mulai diimplementasikan pada integration which has been implemented since 29 tanggal 29 September 2018 adalah tahapan September 2018 is a stage towards a multilane menuju transaksi tol menerus atau multilane free free flow (MLFF) that will take effect in 2019. The flow (MLFF) yang akan diberlakukan dalam waktu integration is also aimed at improving services yang tidak lama lagi. Integrasi transaksi tol JORR and supporting the national logistics system to be ini juga bertujuan meningkatkan pelayanan dan more efficient and competitive. mendukung sistem logistik nasional agar lebih efisien dan berdaya saing. Dengan integrasi tarif jalan tol ini, pengguna tol The toll integration makes the payment system hanya melakukan satu kali transaksi pada gerbang becomes open in which toll users will only have tol masuk (on-ramp payment) atau jauh-dekat satu to make one transaction on the toll gate (on-ramp tarif. Sebelumnya, pengguna tol harus melakukan payment) at one tariff. Previously, toll users were 2-3 kali transaksi untuk menggunakan tol JORR charged a closed transaction system by having sepanjang 76,85 km yang dikelola oleh 4 badan to conduct 2-3 transactions to use the 76.85 km usaha jalan tol (BUJT) berbeda. -

Jasa Marga Update Fy2020holders Meeting 1 August 2019 Company Overview

Jasa Marga Update FY2020holders Meeting 1 August 2019 Company Overview 2 Company Highlights Brief Snapshot Company Highlights • Leading toll road operator in Indonesia with more than 40 years of • Largest toll road operator in Indonesia with 67% market share in experience. term of operated commercial toll roads lengths (± 1,191 km). • 34 toll road concessions with total length of 1,603 km. • The longest concession period holder in Asia reflecting stable • 70% shares owned by the Government of Indonesia. income. • Listed on the Indonesia Stock Exchange since 2007, with a market cap • Strategically important with strong government ownership. Rp33.6 trillion as of 30th December 2020. • Resilient industry with strong government focus. • Key business • Strong financial profile with promising growth going forward. • Construction, operation and maintenance of toll road • Supporting business / other business • Toll Road Operation Services (Provides operation services for Jasa Marga Group and other toll road investors) Vision & Mission • Toll Road Maintenance Services (Provides maintenance services for Jasa Marga Group and other toll road investor) To be the largest, trusted and sustainable national toll Vision road network company. • Prospective Business (Manages rest areas and other properties on toll road corridors) FY2020 Revenue Breakdown 1. Lead toll road business along the end-to-end value chain professionally and continuously to improve National connectivity Toll Revenue – Other Business Subsidiaries Revenue 2. Optimize regional development for community 17% 9% progress Mission 3. Increase value for shareholders.. 4. Enhance customer satisfaction through service excellence Toll Revenue – Jasa 5. Encourage the development and enhancement of Marga employee performance in a harmonious (13 old concessions environment. -

Transformation for Sustainability

PT JASA MARGA (Persero) Tbk TRANSFORMATION FOR SUSTAINABILITY 2017 SUSTAINABILITY REPORT Highlights of Company Message from the Board Message from the Board Concerning Sustainability Profile of Commissioners of Directors Sustainability Report Performance 2017 HIGHLIGHTS OF SUSTAINABILITY 5 COMPANY PROFILE 20 PERFORMANCE REPORT OF THE BOARD OF 37 REPORT OF THE BOARD OF 43 COMMISSIONERS DIRECTORS 49 57 CONCERNING SUSTAINABLE SUSTAINABILITY REPORT GOVERNANCE 2017 2 PT Jasa Marga (Persero) Tbk. 2017 Sustainability Report Sustainable Sustainability GRI Standards POJK No. 51 of 2017 Indeks GRI Governance Performance Application Statement Reference Standards Opsi “Core” TABLE OF CONTENTS THEME 3 HIGHLIGHTS OF SUSTAINABILITY PERFORMANCE 6 Economic Aspect 6 Environmental Aspect 8 Social Aspect 10 AWARD AND CERTIFICATIONS 12 IMPORTANT EVENTS 14 SUSTAINABILITY PERFORMANCE ASPECTS OVERVIEW 17 A COMPANY PROFILE 20 Vision, Mission, and Sustainability Values 21 Brief Profile 24 Scale of Business 26 Employee Profile 27 Policy in Employment Opportunities 31 Share Ownership Information 32 Operation Area 32 Business Field 33 Membership of the Association 35 Significant Changes 35 B MANAJEMENT REPORT 36 Message from the Board of Commissioners 37 Message from the Board of Director 43 C ABOUT SUSTAINABILITY REPORT 2017 49 D SUSTAINABILITY GOVERNANCE 57 Structure of Governance 58 Position of GMS, Board of Commissioners and Directors 60 Risk Management Control 75 Stakeholders Management 77 Supply Chain 80 The Problems Encountered 81 E SUSTAINABILITY PERFORMANCE 84 Economic Aspect 84 Social Aspect 85 Environmental Aspect 98 Product Responsibility 102 FEED BACK SHEET 106 STATEMENTS OF GRI STANDARDS APPLICATION 107 INDEX OF FINANCIAL SERVICES AUTHORITY REGULATION (FSA) NO.51 108 INDEX OF GRI STANDARDS IN OPTION “CORE” 109 PT Jasa Marga (Persero) Tbk. -

Jasa Marga Update 1Q2021olders Meeting 1 August 2019 Company Overview

Jasa Marga Update 1Q2021olders Meeting 1 August 2019 Company Overview 2 Company Highlights Brief Snapshot Company Highlights • Leading toll road operator in Indonesia with more than 40 years of • Largest toll road operator in Indonesia with 67% market share in experience. term of operated commercial toll roads lengths (± 1,214 km). • 34 toll road concessions with total length of 1,603 km. • The longest concession period holder in Asia reflecting stable • 70% shares owned by the Government of Indonesia. income. • Listed on the Indonesia Stock Exchange since 2007, with a market cap • Strategically important with strong government ownership. Rp29.3 trillion as of 31st March 2021. • Resilient industry with strong government focus. • Key business • Strong financial profile with promising growth going forward. • Construction, operation and maintenance of toll road • Supporting business / other business • Toll Road Operation Services (Provides operation services for Jasa Marga Group and other toll road investors) Vision & Mission • Toll Road Maintenance Services (Provides maintenance services for Jasa Marga Group and other toll road investor) To be the largest, trusted and sustainable national toll Vision road network company. • Prospective Business (Manages rest areas and other properties on toll road corridors) 1Q2021 Revenue Breakdown 1. Lead toll road business along the end-to-end value chain professionally and continuously to improve National connectivity. 2. Optimize regional development for community progress. Mission 3. Increase value for shareholders. 4. Enhance customer satisfaction through service excellence. 5. Encourage the development and enhancement of employee performance in a harmonious environment. 3 Company Key Development Milestone ✓Government offered the opportunities ✓Jasa Marga was established with for the private sector to participate in focus on business management, toll road business through Build, maintenance and procurement of Jasa Marga became a public Operate and Transfer (BOT) system the toll road network. -

Along with Indonesia's Rapid Economic Growth of About 8 Percent Annually

TRANSPORTATION AND LAND USE DYNAMICS IN METROPOLITAN JAKARTA Bambang Susantono This article is an attempt to build an understanding of current interactions between land development and transportation infrastructure in the Jakarta Metropolitan Area. The in tention is to pro vide a basis for further research in transportation and land use planning in megacities in the developing world. Four issues are revealed by the discussion. Firs t, transportation infrastructure development has promoted urban sprawl in Jakarta 's peripheries. Second, the in creased accessibility of suburbs, combined with poor land management and corrup t public servants have resulted in uncontrolled development in Jakarta 's urban fringes. Third, the curren t situation of Jakarta's organic growth has resulted from the informal development practices which dominate the land development in Jakarta 's suburbs. Fourth, the government should .be more consistent in following their own plans and regulations. Otherwise, the uncontrolled development which has reached an alarming position will be far more difficult to handle. Introduction Along with Indonesia's rapid economic growth of about 8 percent annually in the last decade, the city of Jakarta has been experiencing some dramatic changes in its landscape. As the dominating economic and political center of the country, Jakarta has been growing economically and demographically at least twice as fast as the nation as a whole. Yet the planning and management responses to those changes have been inadequate because of various limitations. As a consequence, land use changes often do not conform with the plans, employment centers are located regardless of the traffic impacts in the surrounding areas, and traffic congestion is found in almost every corner of the city. -

Journal Template

GSJ: Volume 8, Issue 1, January 2020 ISSN 2320-9186 2058 GSJ: Volume 8, Issue 1, January 2020, Online: ISSN 2320-9186 www.globalscientificjournal.com THE EFFECT OF SEDIMENT DEPOSITION RATE ON COMMUNITY STRUCTURE OF MACROZOOBENTHOS IN SITU GUNUNG PUTRI, INDONESIA 1 2 3 2 Mochammad Faisal Rapsanjani , Isni Nurruhwati , Aiman Ibrahim , Zahidah Hasan 1Student at Faculty of Fisheries and Marine Scicence, Padjadjaran University, Bandung – Sumedang KM 21 Jatinangor 45363, Indonesia E-mail address: [email protected] 2Lecturer at Faculty of Fisheries and Marine Science, Padjadjaran University, Bandung – Sumedang KM 21 Jatinangor 45363, Indonesia E-mail address: [email protected] 3Researcher at Research Center for Limnology, Indonesian Institute of Sciences, Jakarta – Bogor KM 46 Cibinong 16911, Indonesia KeyWords Sediment Deposition Rate, Abundance, Diversity, Macrozoobenthos, Situ Gunung Putri ABSTRACT Situ Gunung Putri is a small lake located in Bogor Regency, West Java. The purpose of this research is to determine the sediment deposition rate that occurs in Situ Gunung Putri and its effect on community structure of macrozoobenthos. The research method was using survey method and samples determined by using purposive sampling method. This research was conducted from March to June 2019 in five observation stations once two week and three times for each stations. The measurement of sediment deposition rate was conducted using sediments traps, while macrozoobenthos sampling is conducted by using Eckman Grab. The result shows that the sediment deposition rate in Situ Gunung Putri ranged from 76.95 to 1264 grams/m2/day. Abundance of macrozoobenthos ranged from 89 to 1321 individuals/m2. Shanon-Wiener Diversity Index ranged from 0.62 to 1.78. -

Jasa Marga Update 1Q2019 Company Overview Company Overview

Jasa Marga Update 1Q2019 Company Overview Company overview Brief Snapshot Company Highlights • Leading toll road operator in Indonesia with 40 years of experience ✓ Largest toll road operator in Indonesia with 66% market share in • 33 toll road concessions with total length of 1,527 km terms of commercial toll roads lengths (±1.000 km) and 80% • 70% owned by the Government of Indonesia market share of toll road transaction volume • Publically listed on the Indonesia Stock Exchange since 2007, with a ✓ The longest concession period holder in Asia reflecting stable market cap IDR 43 trillion as of March 31st, 2019 income • Key business ✓ Strategically important with strong government ownership – Construction, operation and maintenance of toll road ✓ Resilient industry with strong government focus • Supporting business / other business ✓ Strong financial profile with promising growth going forward – Toll Road Operation Services (Provides operation services for Jasa Marga Group and other toll road investors) – Toll Road Maintenance Services (Provides maintenance services for Jasa Marga Group Vision & Mission and other toll road investor) – Property (Manages rest areas and other properties on toll road corridors) To be the largest, trusted and sustainable national toll 1Q2019 Segmental Revenue Breakdown Vision road network company. Other Business Toll Revenue – Revenue 1. Lead toll road business along the end-to-end value 8% Subsidiaries chain professionally and continuously to improve 13% National connectivity 2. Optimize regional development for community progress Mission 3. Increase value for shareholders.. Toll Revenue – Jasa Marga 4. Enhance customer satisfaction through service (13 old excellence concessions in balance sheet) 5. Encourage the development and enhancement of 79% employee performance in a harmonious environment.