Chronology of the Financial Crisis

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Directive 94/19/EC on Deposit-Guarantee Schemes – Obligation of Result – Emanation of the State – Discrimination)

JUDGMENT OF THE COURT 28 January 2013 (Directive 94/19/EC on deposit-guarantee schemes – Obligation of result – Emanation of the State – Discrimination) In Case E-16/11, EFTA Surveillance Authority, represented by Xavier Lewis, Director, and Gjermund Mathisen, Officer, Department of Legal & Executive Affairs, acting as Agents, applicant, supported by the European Commission, represented by its Agents Enrico Traversa, Albert Nijenhuis and Karl-Philipp Wojcik, intervener, v Iceland, represented by Kristján Andri Stefánsson, Agent, Tim Ward QC, Lead counsel, Jóhannes Karl Sveinsson, Co-counsel, defendant, APPLICATION for a declaration that by failing to ensure payment of the minimum amount of compensation to Icesave depositors in the Netherlands and in the United Kingdom provided for in Article 7(1) of the Act referred to at point 19a of Annex IX to the Agreement on the European Economic Area (Directive 94/19/EC of the European Parliament and of the Council of 30 May 1994 on deposit-guarantee schemes) within the time limits laid down in Article 10 of the Act, Iceland has failed to comply with the obligations resulting from that Act, in particular its Articles 3, 4, 7 and 10, and/or Article 4 of the Agreement on the European Economic Area. – 2 – THE COURT, composed of: Carl Baudenbacher, President and Judge Rapporteur, Páll Hreinsson, and Ola Mestad (ad hoc), Judges, Registrar: Gunnar Selvik, - having regard to the written pleadings of the parties and the intervener and the written observations of the Principality of Liechtenstein, represented -

SC13-2384 Exhibit D (Lavalle)

EXHIBIT D REPORT ON NYE LAVALLE’S INVESTIGATIONS, RESEARCH BACKGROUND, BONA FIDES, EXPERTISE, & EXPERIENCE IN PREDATORY MORTGAGE SECURITIZATION, SERVICING, FORECLOSURE & ROBO-SIGNING PRACTICES INTRODUCTION 1. My name is Aneurin Adlai Lavalle. I am most commonly referred to as Nye Lavalle. I am a resident of the State of Florida. 2. I provide this report based upon facts and information personally known by me and to me and gathered from my research and investigation over a period of more than twenty-years. 3. I have a research background and as a consumer and shareholder advocate, I have developed a series of skills, procedures, and protocols over 20-years that has led me to be an expert in predatory mortgage securitization, servicing, and foreclosure fraud issues with a specialty in robo-signing.1 4. I have been accepted by Courts as an expert in matters relating to predatory mortgage securitization, servicing, and foreclosure fraud issues. 5. My findings, analyses, opinions, and many of my protocols, opinions, and conclusions have been reviewed, corroborated, and adopted by state and Federal regulatory agencies such as the Federal Reserve, Office of Comptroller of the Currency; Federal Deposit Insurance Corporation, Federal Housing Financing Agency, U.S. Attorney General and Attorneys General from all 50 states, FILED, 02/04/2015 12:11 am, JOHN A. TOMASINO, CLERK, SUPREME COURT including Florida, but especially by those in New York, Delaware, Nevada, and California. 1 http://en.wikipedia.org/wiki/Nye_Lavalle 1 6. In addition, numerous state and federal courts, including the Supreme and highest courts of the states of Massachusetts,2 Maryland,3 and Kansas4 have agreed with some of my opinions, findings, conclusions, and analyses I have developed over the last twenty-years. -

Iceland's Financial Crisis

Iceland’s Financial Crisis A Global Crisis • The current economic turmoil in Iceland is part of a complex global financial crisis and is by no means an isolated event. • Governments around the world have introduced emergency measures to protect their financial system and rescue their banks, as they suffer from a severe liquidity shortage. • Thus far, Iceland has been hit particularly hard by this unprecedented financial storm due to the large size of the banking sector in comparison to the overall economy. • The Icelandic Government has taken measures and is working hard to resolve the situation, both independently and in cooperation with other parties. • Iceland is cooperating with its Nordic and European partners and is currently consulting with the IMF on measures toward further stabilization of the Icelandic economy. 1 Bank Liquidity Tightens • The liquidity position of Icelandic banks tightened significantly in late September and early October as interbank markets froze following the collapse of Lehman Brothers. • The nationalization of Glitnir, one of Iceland’s three major banks, on Sept. 29 th , led to a credit rating downgrade on sovereign debt and that of all the major banks. • This led to further deterioration of liquidity. • Early October, all three banks were suffering from a severe liquidity shortage and in dire need for Central Bank emergency funding. Negative coverage on the Icelandic economy, particularly in the U.K, did not help either. • By mid-October, all three banks, Glitnir, Landsbanki and Kaupthing, had been taken over by the government on the basis of a new emergency law. • The banks had become too large to rescue. -

Housing and the Financial Crisis

This PDF is a selection from a published volume from the National Bureau of Economic Research Volume Title: Housing and the Financial Crisis Volume Author/Editor: Edward L. Glaeser and Todd Sinai, editors Volume Publisher: University of Chicago Press Volume ISBN: 978-0-226-03058-6 Volume URL: http://www.nber.org/books/glae11-1 Conference Date: November 17-18, 2011 Publication Date: August 2013 Chapter Title: The Future of the Government-Sponsored Enterprises: The Role for Government in the U.S. Mortgage Market Chapter Author(s): Dwight Jaffee, John M. Quigley Chapter URL: http://www.nber.org/chapters/c12625 Chapter pages in book: (p. 361 - 417) 8 The Future of the Government- Sponsored Enterprises The Role for Government in the US Mortgage Market Dwight Jaffee and John M. Quigley 8.1 Introduction The two large government- sponsored housing enterprises (GSEs),1 the Federal National Mortgage Association (“Fannie Mae”) and the Federal Home Loan Mortgage Corporation (“Freddie Mac”), evolved over three- quarters of a century from a single small government agency, to a large and powerful duopoly, and ultimately to insolvent institutions protected from bankruptcy only by the full faith and credit of the US government. From the beginning of 2008 to the end of 2011, the two GSEs lost capital of $266 billion, requiring draws of $188 billion under the Treasured Preferred Stock Purchase Agreements to remain in operation; see Federal Housing Finance Agency (2011). This downfall of the two GSEs was primarily a question of “when,” not “if,” given that their structure as a public/private Dwight Jaffee is the Willis Booth Professor of Banking, Finance, and Real Estate at the University of California, Berkeley. -

Primers Federal Home Loan Banks Feb. 8, 2021

The NAIC’s Capital Markets Bureau monitors developments in the capital markets globally and analyzes their potential impact on the investment portfolios of U.S. insurance companies. Please see the Capital Markets Bureau website at INDEX. Federal Home Loan Banks Analyst: Jennifer Johnson Executive Summary • The Federal Home Loan Bank (FHLB) system was established in 1932 for the purpose of providing liquidity and transparency to the capital markets. • It is comprised of 11 regional banks that are government-sponsored entities (GSEs) and support the market for homes. These FHLB regional banks provide low-cost financing to member financial institutions, which in turn make loans to individuals. • Each FHLB regional bank is structured as a cooperative of mortgage lenders, or members, which sets its credit standards and lending policies. To become a member, a financial institution must purchase shares of the regional bank. • FHLB regional bank members may apply for a loan or “advance” based on required credit limits and borrowing capacity. Each loan or advance is secured by eligible collateral, and lending capacity is based on applicable discount rates on the eligible collateral. The more liquid and easily valued the collateral, the lower the discount rate. • Eligible collateral may include U.S. government or government agency securities; residential mortgage loans; residential mortgage-backed securities (RMBS); multifamily mortgage loans; cash; deposits in an FHLB regional bank; and other real estate-related assets such as commercial What is thereal FHLB estate? loans. • U.S. insurers interact with the FHLB system via borrowing, investing in FHLB debt and owning stock in FHLB regional banks. -

Financial Freak Show

Financial freak show September 15, 2008 – The S&P/TSX Capped Financials Index has not retested its mid- July low of 154. In fact, the index, which tracks Canada’s major financial services companies, closed last Friday at 184, up 19.5% from July’s low. It’s a sign that investors believe that the worst could well be over for the big Canadian banks, most of which have taken sizable writedowns of US subprime mortgage-related debt. A price floor seems to have developed for the financials, and compared with the financial freak show unfolding south of the border, Canadian banks now appear as bastions of financial probity. But that’s no reason to gloat. Most Canadian banks’ balance sheets were fouled with the same sort of junk that’s bedevilling much of the US financial sector just now, but not to the same degree. They cleaned it up in a hurry, but let’s not forget that with one or two exceptions – Scotiabank and Toronto-Dominion Bank leap to mind – Canadian banks fell into the same trap that their US counterparts did. So no kudos for these guys – at least not until they restore shareholder value and demonstrate a return to the principles of solid bank management. On the other hand, the financial drama that continues to unfold in the south 49 has taken on the epic proportions of high Shakespearean tragedy. With much rending of garments and falling on swords the fourth-largest US investment bank, Lehman Brothers Holdings, descended into the banker’s hell of non-confidence last week, as the Korea Development Bank abandoned a possible deal that would have kept Lehman afloat. -

Special Report

September 2014 turnarounds & Workouts 7 Special Report European Restructuring Practices of Major U.S. Law Firms, page 1 Firm Senior Professionals Representative Clients Bingham McCutchen James Roome Elisabeth Baltay Creditors of: Arcapita Bank, Bulgaria Telecommunications/Vivacom, Crest +44.20.7661.5300 Barry G. Russell Liz Osborne Nicholson, Dannemora Minerals, DEPFA Bank, Findus Foods, Gala Coral, www.bingham.com James Terry Neil Devaney Icelandic Banks (Kaupthing, Glitnir and Landsbanki), Invitel, Klöckner Stephen Peppiatt Emma Simmonds Pentaplast, Media Works, Northland Resources, Oceanografia, OSX3 Leasing Tom Bannister B.V., Petromena, Petroplus, Preem, Punch Taverns, Royal Imtech, Selecta, Sevan Marine, Skeie Drilling, Straumur, Technicolor S.A. (Thomson S.A.), Terreal, The Quinn Group, Uralita, Wind Hellas, Xcite, and others. Cadwalader, Wickersham Gregory Petrick Louisa Watt Centerbridge Partners, Avenue Capital Group, GSO Capital Partners, & Taft Richard Nevins Paul Dunbar Oaktree Capital Management, Varde Partners, Golden Tree Asset +44 (0) 20 7170 8700 Yushan Ng Karen McMaster Management, Bluebay Asset Management, MBIA, Davidson Kempner, www.cadwalader.com Holly Neavill Alexis Kay Outrider Management, GLG Partners, Warwick Capital, Alchemy, Finnisterre Capital. Davis Polk Donald S. Bernstein Timothy Graulich Lehman Brothers International (Europe) and its U.K. Lehman affiliates, +44 20 7418 1300 Karen E. Wagner Elliot Moskowitz Sterling Equities in Madoff SIPA liquidation, Technicolor S.A., Royal www.davispolk.com Andrés V. Gil Thomas J. Reid Imtech, Carrefour, major global banks and financial institutions in Arnaud Pérès Christophe Perchet connection with several monoline insurance company restructurings, Marshall S. Huebner John Banes Goldman Sachs in connection with exposures to BP, Castle HoldCo 4, Benjamin S. Kaminetzky Reuven B. -

Financial Crises and Policy Responses

Financial Crises and Policy Responses A MARKET-BASED VIEW FROM THE SHADOW FINANCIAL REGULATORY COMMITTEE, 1986–2015 ROBERT LITAN NOVEMBER 2016 AMERICAN ENTERPRISE INSTITUTE Financial Crises and Policy Responses A MARKET-BASED VIEW FROM THE SHADOW FINANCIAL REGULATORY COMMITTEE, 1986–2015 ROBERT LITAN NOVEMBER 2016 AMERICAN ENTERPRISE INSTITUTE © 2016 by the American Enterprise Institute. All rights reserved. The American Enterprise Institute (AEI) is a nonpartisan, nonprofit, 501(c)(3) educational organization and does not take institutional posi- tions on any issues. The views expressed here are those of the author(s). Table of Contents Preface ................................................................................................................................................................................... v I. Financial Crises and Challenges: The Origins of the Shadow Financial Regulatory Committee ..... 1 II. A Brief 30-Year History of Finance ..................................................................................................................... 5 III. The S&L Crises of the 1980s ................................................................................................................................. 7 IV. The Banking Crises of the 1980s and Policy Responses .............................................................................. 11 V. Deposit Insurance and Safety-Net Reform .................................................................................................... 17 VI. Banking Regulation -

World Bank Document

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized IN TiUS ISSUE The Great American Motor Rallye •...............•... Meet a Foreigner . .. Christma~ Cocktail Party Pictures. ............... Public Disclosure Authorized The following statement was made by Mr. Andrew N. Overby at the last Executive Directors' meeting in 1955. We think his words are most fitting as a thought for the New Year. "Mr. Chairman: "This, I believe. will be the last meeting of the year. and I think it is appropriate at this time not only to extend to the management and staff of the Bank the Board's Christmas greetings. but also their deep appreciation. of the work and able and efficient discharge of duty on behalf of the staff• . They wish also to pay tribute to the leadership of the management of the Bank which has taken us through another difficult year and. we think, without running afoul of too many rocks, and has taken us into some new and perhaps even interesting horizons lying ahead of us. "So with those words. we expres~ our appreciation, as well as our Christmas greetings to you and all the members of the staff, sir." CHRISTMAS CARDS RE<:;EIVED BY THE BANK, 1955 The First National Ciiy Bank of Caisse d'Epargne de L 'Etat, New York Luxembourg Amsterdamsche Bank The Workers' Bank Ltd., Israel Governor of the Bank of Greece Landsbanki Islands La Asociacion Mexicana de Caminos Central Hidroelectrica del Rio Federal Reserve Bank of New York Anchicaya, Limitada,. Colombia Bank of the Ryukyus Comptoir National d'Escompte de Banque de France Paris Industrial Development Bank of The Trust Company of Cuba Turkey Central Office of Information, Malta Nederlandsche Handel-Maatschappij. -

Elizabeth a Duke: a Framework for Analyzing Bank Lending

Elizabeth A Duke: A framework for analyzing bank lending Speech by Ms Elizabeth A Duke, Member of the Board of Governors of the US Federal Reserve System, at the 13th Annual University of North Carolina Banking Institute, Charlotte, North Carolina, 30 March 2009. The original speech, which contains figures and various links to the documents mentioned, can be found on the US Federal Reserve System’s website. * * * In August 2008 I joined the Board of Governors of the Federal Reserve System, leaving behind a 30-year career as a commercial banker to become a central banker. My time as a commercial banker spanned numerous business cycles. It also encompassed at least one severe financial system crisis, in the late 1980s through the early 1990s, albeit one that was not as severe as the current one. From my time as a commercial banker, I already understood the factors considered by bankers in the initial lending decision as well as those in loss mitigation when collecting those same loans. As a central banker, I have come to appreciate even more fully the role of credit in our economic well-being. So I thought it would be appropriate for me to provide my perspective on credit conditions in our economy and the current crisis. Today, I would like to discuss a three-dimensional view of the flow of credit to households and businesses and describe the evolving role of banks in the U.S. economy. I will begin by taking a look at recent trends in aggregate borrowing by households and by the nonfinancial business sector. -

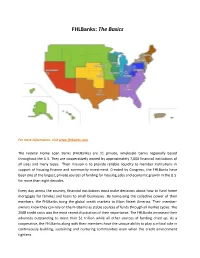

Fhlbanks: the Basics

FHLBanks: The Basics For more information, visit www.fhlbanks.com. The Federal Home Loan Banks (FHLBanks) are 11 private, wholesale banks regionally based throughout the U.S. They are cooperatively owned by approximately 7,000 financial institutions of all sizes and many types. Their mission is to provide reliable liquidity to member institutions in support of housing finance and community investment. Created by Congress, the FHLBanks have been one of the largest, private sources of funding for housing, jobs and economic growth in the U.S. for more than eight decades. Every day across the country, financial institutions must make decisions about how to fund home mortgages for families and loans to small businesses. By harnessing the collective power of their members, the FHLBanks bring the global credit markets to Main Street America. Their member- owners know they can rely on the FHLBanks as stable sources of funds through all market cycles. The 2008 credit crisis was the most recent illustration of their importance. The FHLBanks increased their advances outstanding to more than $1 trillion while all other sources of funding dried up. As a cooperative, the FHLBanks along with their members have the unique ability to play a critical role in continuously building, sustaining and nurturing communities even when the credit environment tightens. 2 FHLBanks are regionally focused and controlled. This structure allows each FHLBank to be responsive to the specific community credit needs in its geography. At the same time, the FHLBanks collectively use their combined size and strength to obtain funding at the lowest possible cost for their members. -

POLICY INSIGHT No. 44 JANUJANUARY 2010

abcd a POLICY INSIGHT No. 44 JANUJANUARY 2010 The saga of Icesave Jon Danielsson London School of Economics The President of Iceland has refused to sign a parlia- • Strong likelihood of state support in the event of mentary bill agreeing to compensate the governments systemic shock of the UK and Netherlands for deposit insurance pay- • Good financial fundamentals outs because of Icesave. This does not mean a rejection • Good efficiency levels of the country's obligations, nor any form of default. • Diversification of income On the contrary, the decision by the president stems • Capable credit risk management and good qual- from the fact that over 70% of Icelanders find the terms ity loan portfolios of the current deal unreasonable. • Adequate capitalisation • Prudent liquidity management Origin of the problem This coincided with one of the biggest asset bubbles the Iceland has traditionally had limited experience with world has ever seen, where anybody taking a highly international banking (Buiter and Sibert 2008). The leveraged bet was assured outsized profits. Eventually, financial system was highly regulated and politicised, the balance sheet of the banks swelled to 10 times the with the bulk of the system in government hands and GDP of Iceland. (See Danielsson and Zoega 2009). insulated from the outside world with capital controls until 1994. This all changed with the deregulation and So what is Icesave? privatisation of the financial system. Iceland adopted a new regulatory structure, in line with EU regulations, The Iceland banks started experiencing increasing prob- because of its European Economic Area membership. lems raising funds in international capital markets in Importantly, this meant that Icelandic banks could 2006.