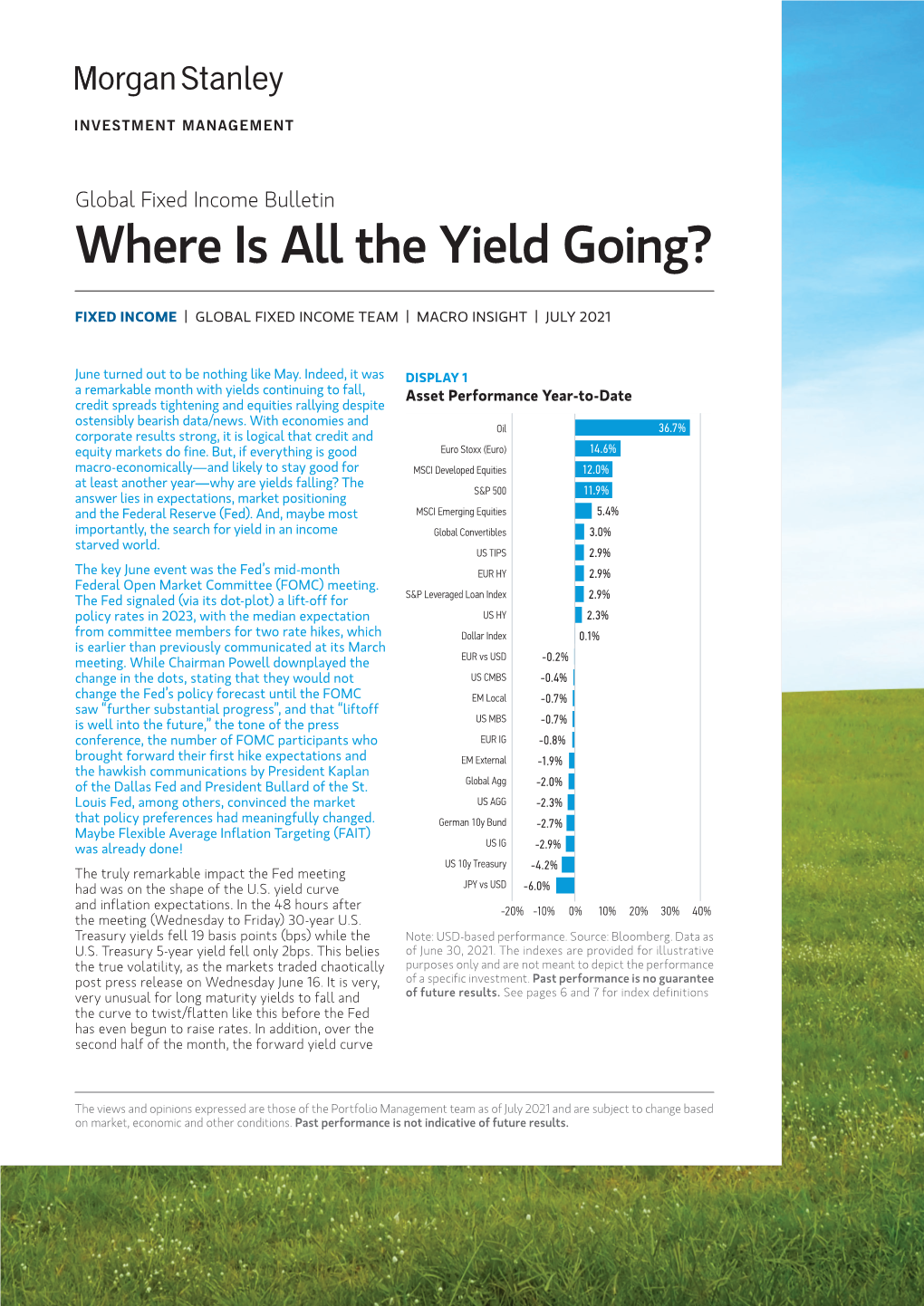

Where Is All the Yield Going?

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Performing Shakespeare in Contemporary Taiwan

Performing Shakespeare in Contemporary Taiwan by Ya-hui Huang A thesis submitted in partial fulfilment for the requirements of the degree of Doctor of Philosophy at the University of Central Lancashire Jan 2012 Abstract Since the 1980s, Taiwan has been subjected to heavy foreign and global influences, leading to a marked erosion of its traditional cultural forms. Indigenous traditions have had to struggle to hold their own and to strike out into new territory, adopt or adapt to Western models. For most theatres in Taiwan, Shakespeare has inevitably served as a model to be imitated and a touchstone of quality. Such Taiwanese Shakespeare performances prove to be much more than merely a combination of Shakespeare and Taiwan, constituting a new fusion which shows Taiwan as hospitable to foreign influences and unafraid to modify them for its own purposes. Nonetheless, Shakespeare performances in contemporary Taiwan are not only a demonstration of hybridity of Westernisation but also Sinification influences. Since the 1945 Kuomintang (Chinese Nationalist Party, or KMT) takeover of Taiwan, the KMT’s one-party state has established Chinese identity over a Taiwan identity by imposing cultural assimilation through such practices as the Mandarin-only policy during the Chinese Cultural Renaissance in Taiwan. Both Taiwan and Mainland China are on the margin of a “metropolitan bank of Shakespeare knowledge” (Orkin, 2005, p. 1), but it is this negotiation of identity that makes the Taiwanese interpretation of Shakespeare much different from that of a Mainlanders’ approach, while they share certain commonalities that inextricably link them. This study thus examines the interrelation between Taiwan and Mainland China operatic cultural forms and how negotiation of their different identities constitutes a singular different Taiwanese Shakespeare from Chinese Shakespeare. -

An Energetic Example of Bidirectional Sino-Japanese Esoteric Buddhist Transmission

religions Article From China to Japan and Back Again: An Energetic Example of Bidirectional Sino-Japanese Esoteric Buddhist Transmission Cody R. Bahir Independent Researcher, Palo Alto, CA 94303, USA; [email protected] Abstract: Sino-Japanese religious discourse, more often than not, is treated as a unidirectional phe- nomenon. Academic treatments of pre-modern East Asian religion usually portray Japan as the pas- sive recipient of Chinese Buddhist traditions, while explorations of Buddhist modernization efforts focus on how Chinese Buddhists utilized Japanese adoptions of Western understandings of religion. This paper explores a case where Japan was simultaneously the receptor and agent by exploring the Chinese revival of Tang-dynasty Zhenyan. This revival—which I refer to as Neo-Zhenyan—was actualized by Chinese Buddhist who received empowerment (Skt. abhis.eka) under Shingon priests in Japan in order to claim the authority to found “Zhenyan” centers in China, Hong Kong, Taiwan, Malaysia, and even the USA. Moreover, in addition to utilizing Japanese Buddhist sectarianism to root their lineage in the past, the first known architect of Neo-Zhenyan, Wuguang (1918–2000), used energeticism, the thermodynamic theory propagated by the German chemist Freidrich Wilhelm Ost- wald (1853–1932; 1919 Nobel Prize for Chemistry) that was popular among early Japanese Buddhist modernists, such as Inoue Enryo¯ (1858–1919), to portray his resurrected form of Zhenyan as the most suitable form of Buddhism for the future. Based upon the circular nature of esoteric trans- mission from China to Japan and back to the greater Sinosphere and the use of energeticism within Neo-Zhenyan doctrine, this paper reveals the sometimes cyclical nature of Sino-Japanese religious influence. -

Sayyids and Shiʽi Islam in Pakistan

Legalised Pedigrees: Sayyids and Shiʽi Islam in Pakistan SIMON WOLFGANG FUCHS Abstract This article draws on a wide range of Shiʽi periodicals and monographs from the s until the pre- sent day to investigate debates on the status of Sayyids in Pakistan. I argue that the discussion by reform- ist and traditionalist Shiʽi scholars (ʽulama) and popular preachers has remained remarkably stable over this time period. Both ‘camps’ have avoided talking about any theological or miracle-working role of the Prophet’s kin. This phenomenon is remarkable, given the fact that Sayyids share their pedigree with the Shiʽi Imams, who are credited with superhuman qualities. Instead, Shiʽi reformists and traditionalists have discussed Sayyids predominantly as a specific legal category. They are merely entitled to a distinct treatment as far as their claims to charity, patterns of marriage, and deference in daily life is concerned. I hold that this reductionist and largely legalising reading of Sayyids has to do with the intense competition over religious authority in post-Partition Pakistan. For both traditionalist and reformist Shiʽi authors, ʽulama, and preachers, there was no room to acknowledge Sayyids as potential further competitors in their efforts to convince the Shiʽi public about the proper ‘orthodoxy’ of their specific views. Keywords: status of Sayyids; religious authority in post-Partition Pakistan; ahl al-bait; Shiʻi Islam Bashir Husain Najafi is an oddity. Today’s most prominent Pakistani Shiʽi scholar is counted among Najaf’s four leading Grand Ayatollahs.1 Yet, when he left Pakistan for Iraq in in order to pursue higher religious education, the deck was heavily stacked against him. -

Explored Countless Lab- Oratories, Interviewed a Myriad of Scientists, and Prepared Thousands of News Releases, Feature Articles, Web Sites, and Multimedia Packages

Explaining Research This page intentionally left blank Explaining Research How to Reach Key Audiences to Advance Your Work Dennis Meredith 1 2010 3 Oxford University Press, Inc., publishes works that further Oxford University’s objective of excellence in research, scholarship, and education. Oxford New York Auckland Cape Town Dar es Salaam Hong Kong Karachi Kuala Lumpur Madrid Melbourne Mexico City Nairobi New Delhi Shanghai Taipei Toronto With offi ces in Argentina Austria Brazil Chile Czech Republic France Greece Guatemala Hungary Italy Japan Poland Portugal Singapore South Korea Switzerland Thailand Turkey Ukraine Vietnam Copyright © 2010 by Dennis Meredith Published by Oxford University Press, Inc. 198 Madison Avenue, New York, New York 10016 www.oup.com Oxford is a registered trademark of Oxford University Press. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior permission of Oxford University Press. Library of Congress Cataloging-in-Publication Data Meredith, Dennis. Explaining research : how to reach key audiences to advance your work / Dennis Meredith. p. cm. Includes bibliographical references and index. ISBN 978-0-19-973205-0 (pbk.) 1. Communication in science. 2. Research. I. Title. Q223.M399 2010 507.2–dc22 2009031328 9 8 7 6 5 4 3 2 1 Printed in the United States of America on acid-free paper To my mother, Mary Gurvis Meredith. She gave me the words. This page intentionally left blank You do not really understand something unless you can explain it to your grandmother. -

Happy Purim! RABBANIT SHANI TARAGIN on Why Purim Is the Most Zionistic Holiday

ADAR SHEINI 5779 MARCH 2019 TORAT ERETZ YISRAEL • PUBLISHED IN SHUSHAN • DISTRIBUTED AROUND THE WORLD ISRAEL EDITION RABBI BEREL WEIN פורים שמח! living our own purim story PAGE 24 Happy Purim! RABBANIT SHANI TARAGIN on why purim is the most zionistic holiday PAGE 5 RABBI JONATHAN SACKS invites us to be alert to G-d's messages PAGE 14 SIVAN RAHAV-MEIR with advice for a noisy world PAGE 23 RABBI CHAIM NAVON analyzes binge relationships PAGE 22 RABBANIT YEMIMA MIZRACHI with some magical moments for women this issue is dedicated in loving memory of PAGE 21 professor cyril domb by his wife and children Torat HaMizrachi HITLER, HAMAN & HAMAS A Parashat Zachor and Purim Primer bsolute evil has existed for minute. Thousands of years later, Individuals and societies possess both millennia. It constitutes a Hitler declared the same intentions. the passion for altruistic good and single-minded, systematic Tragically, he succeeded in murdering the impulse for self-destructive evil. focusA to destroy all good in the world. one third of the Jewish people, and Israel's mission is chiefly the former; According to Torah tradition, it has a if not for the hand of Providence Amalek's the latter. name. Amalek. The Torah commands guiding the actions of the Allied It was not by chance that Amalek was us to always remember and never Forces, he would have gone much 1 the first nation to attack Israel, as forget what Amalek represents. further. Unstopped and unchecked, this type of evil would, G-d forbid, soon as we came out of Egypt. -

Climate Wars Science and Its Disputers Oprah's Gullibility How

SI M/A 2010 Cover V1:SI JF 10 V1 1/22/10 12:59 PM Page 1 MARTIN GARDNER ON JAMES ARTHUR RAY | JOE NICKELL ON JOHN EDWARD | 16 NEW CSI FELLOWS THE MAG A ZINE FOR SCI ENCE AND REA SON Vol ume 34, No. 2 • March / April 2010 • INTRODUCTORY PRICE U.S. and Canada $4.95 Climate Wars Science and Its Disputers Oprah’s Gullibility How Should Skeptics Deal with Cranks? Why Witchcraft Persists SI March April 2010 pgs_SI J A 2009 1/22/10 4:19 PM Page 2 Formerly the Committee For the SCientiFiC inveStigation oF ClaimS oF the Paranormal (CSiCoP) at the Cen ter For in quiry/tranSnational A Paul Kurtz, Founder and Chairman Emeritus Joe Nickell, Senior Research Fellow Richard Schroeder, Chairman Massimo Polidoro, Research Fellow Ronald A. Lindsay, President and CEO Benjamin Radford, Research Fellow Bar ry Karr, Ex ec u tive Di rect or Richard Wiseman, Research Fellow James E. Al cock, psy chol o gist, York Univ., Tor on to David J. Helfand, professor of astronomy, John Pau los, math e ma ti cian, Tem ple Univ. Mar cia An gell, M.D., former ed i tor-in-chief, New Columbia Univ. Stev en Pink er, cog ni tive sci en tist, Harvard Eng land Jour nal of Med i cine Doug las R. Hof stad ter, pro fes sor of hu man un der - Mas si mo Pol id oro, sci ence writer, au thor, Steph en Bar rett, M.D., psy chi a trist, au thor, stand ing and cog ni tive sci ence, In di ana Univ. -

|||GET||| Curse of Strahd a Dungeons & Dragons Sourcebook 1St Edition

CURSE OF STRAHD A DUNGEONS & DRAGONS SOURCEBOOK 1ST EDITION DOWNLOAD FREE none | 9780786965984 | | | | | Curse of Strahd: A Dungeons & Dragons Sourcebook Read full review. Compared to the other adventures this one has a lot of talking and declensions you have to make compared to combat. Popular Features. Thanks for telling us about the problem. Related Searches. Published by Wizards of the Coast, United States A plethora of useful tips, hints and information is provided here the level of which is rarely found in other published adventures. That all said, there's a ton of cool content in here. The book is gorgeous and retains all the feeling of horror and helplessness plus a rich setting that the original had with the addition of new personalities to meet and fight and new places to explore. Rumbling thunder pounds the castle spires. Strahd is more menacing than ever. Full RTC once I've finished running it for the players, but: Initial thoughts: A lot of very fun material here, but I wouldn't recommend this one for beginner DMs -- it's collections of plothooks in every possible locations, with a very high level only set of suggestions of reasons to send people to each one. Lots of neat adventure sites throughout Barovia, with interesting plot hooks and NPCs, many of which would be easily exported to other settings. Look out for a podcast of our game in early Curse of Strahd A Dungeons & Dragons Sourcebook 1st edition Verified purchase: Yes Condition: Pre-owned. The adventure has a lot of varying elements that will touch base on a variety of players interests. -

The Situation of Religious Minorities

writenet is a network of researchers and writers on human rights, forced migration, ethnic and political conflict WRITENET writenet is the resource base of practical management (uk) e-mail: [email protected] independent analysis PAKISTAN: THE SITUATION OF RELIGIOUS MINORITIES A Writenet Report by Shaun R. Gregory and Simon R. Valentine commissioned by United Nations High Commissioner for Refugees, Status Determination and Protection Information Section May 2009 Caveat: Writenet papers are prepared mainly on the basis of publicly available information, analysis and comment. All sources are cited. The papers are not, and do not purport to be, either exhaustive with regard to conditions in the country surveyed, or conclusive as to the merits of any particular claim to refugee status or asylum. The views expressed in the paper are those of the author and are not necessarily those of Writenet or UNHCR. TABLE OF CONTENTS Acronyms ................................................................................................... i Executive Summary ................................................................................. ii 1 Introduction........................................................................................1 2 Background.........................................................................................4 3 Religious Minorities in Pakistan: Understanding the Context......6 3.1 The Constitutional-Legal Context..............................................................6 3.2 The Socio-Religious Context .......................................................................8 -

Monday, 08. 04. 2013 SUBSCRIPTION

Monday, 08. 04. 2013 SUBSCRIPTION MONDAY, APRIL 7, 2013 JAMADA ALAWWAL 27, 1434 AH www.kuwaittimes.net Clashes after New fears in Burgan Bank Lorenzo funeral of Lanka amid CEO spells wins Qatar Egypt Coptic anti-Muslim out growth MotoGP Christians7 campaign14 strategy22 18 MPs want amendments to Max 33º Min 19º residency law for expats High Tide 10:57 & 23:08 Govt rebuffs Abu Ghaith relatives ‘Peninsula Lions’ may be freed Low Tide • 04:44 & 17:01 40 PAGES NO: 15772 150 FILS By B Izzak conspiracy theories KUWAIT: Five MPs yesterday proposed amendments to the residency law that call to allow foreign residents to Menopause!!! stay outside Kuwait as long as their residence permit is valid and also call to make it easier to grant certain cate- gories of expats with residencies. The five MPs - Nabeel Al-Fadhl, Abdulhameed Dashti, Hani Shams, Faisal Al- Kandari and Abdullah Al-Mayouf - also proposed in the amendments to make it mandatory for the immigration department to grant residence permits and renew them By Badrya Darwish in a number of cases, especially when the foreigners are relatives of Kuwaitis. These cases include foreigners married to Kuwaiti women and that their permits cannot be cancelled if the relationship is severed if they have children. These [email protected] also include foreign wives of Kuwaitis and their resi- dence permits cannot be cancelled if she has children from the Kuwaiti husband. Other beneficiaries of the uys, you are going to hear the most amazing amendments include foreign men or women whose story of 2013. -

Jack Parsons on Human Population Competition

JACK PARSONS ON HUMAN POPULATION COMPETITION A short synopsis of his major work by Edmund Davey Chairman of the United Kingdom Optimum Population Trust Finally edited and rounded off by the author ISBN 0-9541978-3-6 (CD version of this text) Published and printed by Population Policy Press © Copyright 2002 Jack Parsons The moral right of the authors and editors has been asserted DataCrítica: International Journal of Critical Statistics publishes this synopsis thanks to the courtesy of Edmund Davey DataCrítica: International Journal of Critical Statistics , Vol.1, No.1, Supplement 1-71, 2007 © DataCrítica Creative Commons, 2007 2 DataCrítica: International Journal of Critical Statistics , Vol.1, No.1 Supplement Table of Contents Synopsis only Foreword by Professor James P Duguid CBE, MD, BSc, FRC Path.......................................................... .6 Introduction by Edmund Davey, Chairman of the Optimum Population Trust .............................. ..9 A brief history of the various editions of this book. .................................................................................... 9 Original table of contents (with both Synopsis and original page number in brackets) Volume 1 Part I The population/resources/quality of life problem 1) A brief introduction ..................................................................................................................................12 [1] Part II Introduction to competition in general 2) Environments, plants, and animals versus each other ............................................................................14 -

CBD First National Report

Contents ACKNOWLEDGEMENTS ................................................................................................................... 5 GLOSSARY ............................................................................................................................................ 6 LIST OF TABLES .................................................................................................................................. 8 LIST OF FIGURES ................................................................................................................................ 9 LIST OF BOXES .................................................................................................................................. 10 PAKISTAN FACT SHEET ................................................................................................................. 11 EXECUTIVE SUMMARY .................................................................................................................. 12 1. PREPARATION OF THIS REPORT ........................................................................................ 15 1.1 Background ....................................................................................................... 16 1.1.1 What is Biodiversity? ...................................................................................................... 16 1.1.2 The Convention on Biological Diversity ......................................................................... 17 1.1.3 Pakistan’s Obligations................................................................................................... -

A Performance Genealogy of "Etchings of Debutantes" Melanie A

Louisiana State University LSU Digital Commons LSU Master's Theses Graduate School 2004 A performance genealogy of "Etchings of Debutantes" Melanie A. Kitchens Louisiana State University and Agricultural and Mechanical College, [email protected] Follow this and additional works at: https://digitalcommons.lsu.edu/gradschool_theses Part of the Communication Commons Recommended Citation Kitchens, Melanie A., "A performance genealogy of "Etchings of Debutantes"" (2004). LSU Master's Theses. 4011. https://digitalcommons.lsu.edu/gradschool_theses/4011 This Thesis is brought to you for free and open access by the Graduate School at LSU Digital Commons. It has been accepted for inclusion in LSU Master's Theses by an authorized graduate school editor of LSU Digital Commons. For more information, please contact [email protected]. A PERFORMANCE GENEALOGY OF ETCHINGS OF DEBUTANTES A Thesis Submitted to the Graduate Faculty of the Louisiana State University and the School of Arts and Sciences in partial fulfillment of the requirements for the degree of Master of Arts in The Department of Communication Studies by Melanie Kitchens B.A. Theatre, Georgia Southern University, 2001 December 2004 Acknowledgements My humblest thanks to all those involved in this process. Namely, Alice, Amy, Andy, Angela, Anne, Andrew, Bella, Ben, Bridgette, Brittany, Bruce, Carlton, Caroline, Carrie, Connie, Danielle, Danny, Dianne, Doris, Drew, Dan Paul, David, Don, Doug, Dudley, Eric, Gary, Ginger, Gretchen, Holly, Ivy, Jane, Jessica, Jim, Jimbo, Jim, Joan, Joe, Joey, Joseph, Jon, Josh, Justin, Kristen, Lisa, Linda, Mabel, Madison, Maggie, Marie, Mary Grace, Michael, Miles, Miron, Missy, Molly, Nancy, Necie, Nick, Odessa, Pam, Patti, Ralph, Rob, Ruth, Sarah, Scott, Suzanna, Tom, Tracy, Trish, and Tyler.