Report to the Treasury Committee

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Sorry We Missed

Tuesday 30.05.17 Tuesday SORRY WE MISSED YOU →→ We called at: Reason forr non-delivery:non-delivnon delivvery:ery: Comment: Item: Depot:Depot Ref:: Trump v Underwood Who said it? Restaurant rules Lisa Markwell Ask Hadley Cute clothes ‘Squeal like a pig!’ Making Deliverance 12A Shortcuts Never order the specials: one of Gordon Ramsay’s tips for a good meal Restaurants Check the loos The golden rules of eating out and snack before you go Call, don’t click Places that show “no tables available” online may have ordon Ramsay has a new something if you take the Complain, complain, complain TV show to promote , so G trouble to telephone. They Nobody wants to leave dinner he’s effi ng and blinding will know about cancellations with a sour taste in their mouth and pronouncing like his career straight away, and if you … If the food is lousy or the depend s on it . Yesterday, we engage with the person at the table judders in time with the learn ed his rules for eating out: restaurant, you might get a dishwasher, tell them. A restau- never order the specials, haggle note on the booking that means rateur would rather fi over wine and be wary of the you’ll get a nicer table. and there (with a free xdessert, it then waiter’s boasts, such as “our or some wine, or money off famous lasagne”. He also asks for Look at the loos than have someone smile, pay a table for three when there are ) Like Bourdain, I wouldn’t the bill and then go home and only two dining – or does he mean eat somewhere that doesn’t Have lunch, not dinner savage them on TripAdvisor. -

The Colombo Bourse Re-Entered Into the Green Terrain Market Statistics 18Th Nov 15Th Nov and Closed the Trading Date on a Positive Note

- Index 18th Nov 15th Nov Change % Change The Bourse ends on positive note … ASPI 5,824.48 5,810.97 13.51 0.23% S&P SL20 3,200.31 3,174.68 25.63 0.81% The Colombo bourse re-entered into the green terrain Market Statistics 18th Nov 15th Nov and closed the trading date on a positive note. The ASPI Value of Turnover(Rs.) 936,442,175 234,292,593 gained 13.51 points or 0.23% to enter the green terrain Domestic Purchases 801,840,456 166,486,154 and settled the day at 5,824.48. The S&P SL20 gained Domestic Sales 878,381,961 196,869,291 25.63 points or 0.81% to settle at 3,200.31. A total of 49 Foreign Purchases 134,601,719 67,799,909 Foreign Sales 58,060,214 37,416,772 companies gained during the day whereas 108 companies posted drops in share prices; Singer Volume of Turnover (No.) 143,648,036 19,776,603 PER 15.26 15.22 Industries (Ceylon) PLC (10.82%) led the price gainers, on PBV 2.01 2.01 the other hand Ceylon Printers PLC (-24.57%) led the price losers. As at the daily closure, the total market capitalization as at the day’s closure moved up to LKR 7,000 2.42Tn, extending the year to date gain to 11.78%. The 5,812.84 5,816.04 5,829.05 5,810.97 5,820.46 6,000 market PER and PBV were 15.26x & 2.01x respectively. -

Complaints to the BBC

Complaints to the BBC This fortnightly report for the BBC complaints service1 shows for the periods covered: • the number of complaints about programmes and those which received more than 1002 at Stage 1 (Audience Services); • findings of subsequent investigations made at Stage 2 (by the Executive Complaints Unit)3; • the percentage of all complaints dealt with within the target periods for each stage. NB: Figures include, but are not limited to, editorial complaints, and are not comparable with complaint figures published by Ofcom about other broadcasters (which are calculated on a different basis). The number of complaints received is not an indication of how serious an issue is. Stage 1 complaints Between 12 - 25 April 2021, BBC Audience Services (Stage 1) received a total of 13,909 complaints about programmes. 21,796 complaints in total were received at Stage 1. BBC programmes which received more than 1002complaints during this period: Programme Service Date of Main Issue(s) Number of Transmission Complaints All That Glitters: BBC Two 13/04/2021 Offensive humour. 664 Britain’s Next Jewellery Star The Funeral Of BBC One 17/04/2021 Factual errors / 147 HRH The Prince offence. Philip, Duke Of Edinburgh BBC News BBC One 17/04/2021 Disrespectful to 316 (10.10pm) reference the relationship between Prince William and Prince Harry. The Andrew Marr BBC One 18/04/2021 Bias in favour of the 234 Show Royal Family. 1 Full details of the service are in the BBC Complaints Framework and Procedures document. 2 As defined in the BBC Complaints Framework and Procedures and regulated under Ofcom’s Broadcasting Code. -

Prem N Sikka Contact

CURRICULUM VITAE NAME: Prem N Sikka Contact: [email protected] EDUCATION 1) Attended Upton House Secondary School from 1966 to 1968. Left School with 5 CSE passes. This is the end of my full-time education. All of the qualifications listed below were studied for through part-time classes. 2) Various evening classes: 1969 to 1971. Passed 5 GCE 'O' Levels. 3) Evening classes 1972 to 1973. Passed two GCE 'A' Levels in Accounting and Economics. 4) Evening classes: 1972 to 1977; for the last 3 years attending as many as four nights per week: passed all professional examinations of The Association of Chartered Certified Accountants (ACCA) at the first attempt. Fellowship awarded in 1982. 5) Evening classes at the London School of Economics, 1980 to 1982: passed MSc in Accounting and Finance. This was a two-year course for part-time students and was successfully completed in the minimum prescribed period. 6) PhD from the University of Sheffield in 1991. Thesis titled "Towards an Understanding of Accounting and Society: Some Episodes in the Formulation and Development of the Going Concern Concept". 7) BA (Hons.) 1st class, in Social Sciences from the Open University in 1995. Summary ACCA 1977 FCCA 1982 MSc 1982 PhD 1991 BA (Hons.) 1995 1 CAREER INFORMATION October 1968 to January 1970: An accounts clerk with Lionel Sage & Co. Ltd (Insurance Brokers). January 1970 to February 1974: Trainee accountant, later assistant accountant with Grigsmore Ltd (Advertising Agency). February 1974 to September 1976: Financial Accountant for The City of London Real Property Co. Ltd (A major subsidiary of Land Securities Plc - Europe's largest Property Company). -

Print Digital Tv & Radio Sunday Print

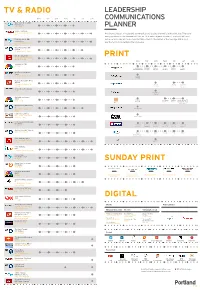

TV & RADIO LEADERSHIP MON TUE WED THUR FRI SAT SUN COMMUNICATIONS Wake Up to Money, BBC Radio 5 Live 5:15 - 6 am PLANNER Sunrise, Sky News 6 - 9 am; Sat & Sun: 6 - 10 One important part of leadership communications is using the media in the right way. There are am many opportunities to communicate live on TV or radio, in print or online. Each has a different 5 Live Breakfast, BBC audience and some will be more suited than others to the leader or the message. But a good Radio 5 Live 6 - 10 am; Sat & Sun 6 - 9 way to start is to understand the landscape. am Today Programme, BBC Radio 4 6 - 9 am; Sat: 7 - 9 am BBC Breakfast, BBC 1 PRINT 6 - 9:15 am ; Sat: 6 - 10 am, Sun: 6 - 7:40 am MON TUE WED THUR FRI SAT SUN Squawkbox, CNBC 6 - 9 am Monday Manifesto; Business Business Business Business Business Business Big Shot Big Shot Big Shot Big Shot Big Shot Big Shot Nick Ferrari Show, LBC Radio 7 - 10 am; Sat: 5 - 7 am Monday Interview Business Daily, BBC World Service 7:32 am; 14.06 pm & Fri Society Friday Saturday 7.32 am Interview Interview Interview (varies) On the Move, Bloomberg 9 am The Business Interview Worldwide Exchange, CNBC Monday 9 am - 11 pm Recruitment Business Lunch with the FT; Interview Interview Speak Person in the News; My Weekend Woman’s Hour, BBC Radio 4 Mon - Fri: 10 - 11 am; Sat: Monday View 4-5pm Daily Politics, BBC 2 Mon - Fri: 12 - 1 pm; Wed: Growth Capital 11:30 am - 1 pm In The Loop with Betty Liu, Bloomberg 1 - 3pm 60 Second 60 Second 60 Second 60 Second 60 Second 60 Second Interview Interview Interview Interview Interview -

Jon Sopel North America Correspondent, BBC Media Masters – July 16, 2020 Listen to the Podcast Online, Visit

Jon Sopel North America Correspondent, BBC Media Masters – July 16, 2020 Listen to the podcast online, visit www.mediamasters.fm Welcome to Media Masters, a series of one-to-one interviews with people at the top of the media game. Today, I'm joined down the line by John Sopel, the BBC’s North America editor. John has had a front row seat during the explosive Trump presidency reporting every twist and turn from the White House and beyond. As a member of the White House press corp, he's accompanied both President Trump and Obama on Air Force One and interviewed President Obama at the White House. He joined the BBC in 1983 and soon garnered national acclaim in his extensive reporting across UK politics. John has reported from Paris, presented the politics show Newsnight, and anchored the BBC News Channel. He's travelled extensively across the US and recently rode a Harley Davidson down the West Coast. He's the author of several books, including If Only They Didn't Speak English: Notes from Trump's America. John, thank you for joining me. A great pleasure to be with you. So with a bitter presidential election on the horizon, Coronavirus sweeping the US, have you ever known a news cycle as crazy as this? No, I've never known anything like this, but I suspect we're all in the same boat in whatever life we lead. I'm in a situation now where I'm speaking to you from Washington, DC. If my wife wanted to come out and join me here, she couldn't get into the country. -

![Full Programme, Transparency Symposium 3[…]](https://docslib.b-cdn.net/cover/5857/full-programme-transparency-symposium-3-3045857.webp)

Full Programme, Transparency Symposium 3[…]

2016. February rd 3 The London Campus of Newcastle University, London. | Page 1 ...is an informal but increasingly influential forum dedicated to encouraging greater transparency in financial services, right around the world. We are a campaigning community that believe higher levels of transparency are a prerequisite for fairer, safer and more efficient markets that deliver better value for money and better outcomes to the consumer. Because of the correlation between a lack of trust and a lack of transparency, we hope that our work on transparency will also help to rebuild trust and confidence in financial services, for the benefit of all market participants and their clients. …has a purpose; to galvanise support for the idea that there ought to be higher levels of transparency in financial services, right around the world. It is a uniquely inclusive opportunity to properly consider and the debate the keys issues, contemplate thought leadership and build consensus on the best way forward for the financial services industry and its clients, as a whole. Delegates will enjoy an environment that is conducive to candid and intelligent debate, where ideas can be exchanged in a constructive and civilised manner thereby encouraging co-operation, collaboration and collegiality, for the benefit of all. …is competed for at each of our Transparency Symposiums, by individuals and organisations that can evidence they “believe in transparency”, align with our overall objectives and want to showcase their pro-transparency credentials. There can be no doubt that the world’s financial services regulators and policymakers want greater transparency; and that asset owners, pension schemes and so on deserve it. -

Roger Mosey Master of Selwyn College, Cambridge University Media Masters – June 8, 2017 Listen to the Podcast Online, Visit

Roger Mosey Master of Selwyn College, Cambridge University Media Masters – June 8, 2017 Listen to the podcast online, visit www.mediamasters.fm Welcome to Media Masters, a series of one to one interviews with people at the top of the media game. Today, I’m joined by the former BBC executive Roger Mosey. Roger has held some of the biggest roles at the Beeb starting at Radio Lincolnshire, he went on to edit some of the country’s leading news shows including PM and, of course, the Today programme. From there he became control of Radio 5 Live, then head of BBC television news, and then director of sport. In 2008, Roger was chosen to lead the BBC coverage of the London 2012 Olympic Games, a momentous job which meant he was responsible for all of the broadcasters reporting across TV, radio and online. He left the BBC in 2013 and is now master of Selwyn College, Cambridge but remains active in debates about the broadcaster’s future, criticising it for what he called ‘liberal group think’ in his memoir, Getting Out Alive. Roger, thank you for joining me. Pleasure. Getting out alive, I think that kind of sums up the tone of the memoir, does it not? It was a joke, and my cousin said it would sound like I’d been held by the Khmer Rouge for 20 years, and actually I wasn’t intending to be like that. I mean, I loved my time in the BBC, but I think there is, when you’ve gone through BBC management, a point where you try to get out with your reputation as intact as you can make it, and that was why I put the joke in the title about getting out alive. -

Pick of the Day Radio

PICK OF THE DAY BBC1 BBC2 ITV 1 CHANNEL 4 FIVE 6.00 Breakfast (T) 20315294 6.00 CBeebies 28749 7.00 6.00 GMTV (T) 3875836 9.25 6.10 Planet Cook (T) (R) 6.00 Milkshake! 22206687 QI 9.15 Animal 24:7 (T) 1360107 CBBC 53010 8.30 CBeebies The Jeremy Kyle Show (T) 1207720 6.30 Yo Gabba 9.15 The Wright Stuff (T) 9.30pm, BBC1 10.00 Homes Under The 94752039 11.10 The 1384403 10.30 This Morning Gabba (T) (R) 43403 7.00 4020107 10.45 Trisha Hammer (T); BBC News; Flintstones Fred sneaks off to (T) 28720 12.30 Loose Freshly Squeezed 76229 7.30 Goddard (T) (R) 5685687 Weather (T) 88010 11.00 play cards. (T) (R) 2766671 Women (T) 87403 1.30 ITV Everybody Loves Raymond 11.45 Medical Investigation Living Dangerously (T) 12.00 Daily Politics (T) 97671 News; Weather (T) 79901045 (T) (R) 6186687 7.55 Frasier (T) (R) 8451478 12.35 Five 2755565 11.45 Cash In The 12.30 Working Lunch (T) 1.55 Regional News (T) (T) (R) 2180316 9.00 Will & News (T) 32130229 12.50 Attic (T); BBC News; Weather 26671 1.00 Open House (T) 89580381 2.00 Dickinson’s Grace (T) (R) 75403 9.30 Nice House, Shame About (T) 600590 12.15 Bargain (R) 73132 1.30 Live Snooker: Real Deal David Dickinson Friends (T) (R) 30039 10.30 The Garden: Revisited (T) Hunt (T) 6905652 1.00 BBC UK Championship Coverage and the team are in Bolton, The Big Bang Theory (T) (R) (R) 32633213 1.15 Cooking News; Weather (T) 75590 of the opening sessions in the Greater Manchester, where the 71687 11.00 Ugly Betty (T) The Books (T) (R) 4486381 1.30 Regional News; Weather remaining two quarter-finals at best deal of the day is a Della (R) 91584 12.00 News (T) 1.45 Neighbours (T) 4485652 (T) 59876890 1.45 Doctors the Telford International Robbia jug bought by expert 99039 12.30 Wife Swap USA 2.15 Home And Away (T) (T) 889565 2.15 Murder, She Centre, featuring a scheduled David Hakeney for £470. -

GEORGE S. YIP July 2019

GEORGE S. YIP July 2019 EDUCATION D.B.A. 1980 Harvard Business School, Business Policy (supervised by Professor Michael E. Porter) M.B.A. 1976 Cranfield School of Management (year 1) and Harvard Business School (year 2) strategy and finance (With Distinction) M.A. 1973 Cambridge University, Economics and Law B.A. 1970 Cambridge University, Economics and Law ACADEMIC APPOINTMENTS D’Amore-McKim School of Business, Northeastern University, 1 March 2020 – Distinguished Visiting Professor, International Business and Strategy Group Distinguished Visiting Fellow, Center for Emerging Markets Imperial College Business School, 1 July 2011 - 1 April 2019 – Emeritus Professor of Marketing and Strategy Teaching on campus and online electives to MBAs and EMBAs on International Business. The MBA elective was rated by the class of 2016 highly enough that Imperial was ranked 7th in the world for MBA international business by the Financial Times in 2020. 1 December 2015 – 15 March 2019 Professor of Marketing and Strategy, Associate Dean of Executive MBA, Member of Management Board. Launched one of the world’s first blended (on campus and online) EMBAs. Led initiatives to bring in evaluation of class participation in all MBA programs and to improve teaching with the case method. Taught on campus and online electives to MBAs and EMBAs on International Business. 1 July 2011 – 30 November 2015 Visiting Professor of Management Taught elective to MBAs and EMBAs on International Business. Developed a course for the online/blended Global MBA. Taught in custom executive education programs. Led development of a new open executive program. 1 China Europe International Business School, 1 July 2011 – 30 June 2016 CEIBS is the top business school in China, with campuses in Shanghai, Beijing, Shenzhen, Zurich, and Accra, Ghana. -

Meredith A. Crowley

Meredith A. Crowley Faculty of Economics, University of Cambridge Austin Robinson Building Sidgwick Avenue Cambridge, CB3 9DD, UK tel: +44 1223 335261 [email protected] http://meredithcrowley.weebly.com/ Current positions/affiliations/honors University of Cambridge Reader in International Economics, Faculty of Economics 2018 – present Keynes Fellow, University of Cambridge 2019 – present Fellow, St. John’s College 2013 – present University Lecturer, Faculty of Economics 2013 – 2018 Cambridge-INET (Institute for New Economic Thinking) Coordinator, Transmission Mechanisms and Economic Policy 2018 – present UK in a Changing Europe (UKICE), London, UK ESRC Senior Fellow 2019 – present Centre for Economic Policy Research (CEPR), London, UK Research Fellow 2016 – present UK Department for International Trade, London, UK Trade and Economy Panel (Academic Advisor) 2019 – present Freeports Advisory Panel (Academic Advisor) 2019 – present Trade and Agriculture Commission (Competitiveness Working Group Member) 2020 – present Kiel Institute for the World Economy, Kiel, Germany Member of the Scientific Advisory Council 2019 – present UK Department for Food, Agriculture and Rural Affairs, London, UK National Food Strategy Advisory Panel (Academic Advisor) 2019 – present UK Government Office for Science, Rebuilding a Resilient Britain Project 2020 – present Trade and Aid Working Group Member Previous positions/appointments/honors Bruegel, Brussels, Belgium Member of the Scientific Council 2018 – 2020 Nanjing University Visiting Professor November 2018 Shanghai University of Finance and Economics Visiting Professor, Summer School 2014, 2015 & 2019 Federal Reserve Bank of Chicago Senior Economist 2006 – 2014. Economist 2001 – 2006. American Law Institute Advisor, Principles of the Law of World Trade Project 2008 – 2012. Pew Charitable Trusts Advisory Board Member, Subsidyscope Project 2008 – 2012. -

How to Write Deadly Crime Thrillers

Table of Contents ...................................................................................................................................... 1 Copyright ....................................................................................................................... 5 Preface .......................................................................................................................... 8 PART ONE — THE SCIENCE OF STORY .................................................................... 9 Tip #1 — Understand Story ............................................................................................ 9 Tip #2 — Understand Storytelling .................................................................................. 9 Tip #3 — Understand The Crime Thriller Genre ............................................................. 9 Tip #4 — Understand Cops & Crimes .......................................................................... 11 Tip #5 — Activate Your Reader’s Brain ........................................................................ 11 Tip #7 — Balance Right & Left Brain ............................................................................ 11 Tip #8 — Study Neuro-Linguistics ................................................................................ 12 Tip #9 — Apply Neuro-Linguistics ................................................................................ 12 Tip #10 — Give Pleasure, Avoid Pain .......................................................................... 12