Chairman's Address

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Cost of Doing Business in the Province of Iloilo 2017 1

COST OF DOING BUSINESS IN THE PROVINCE OF ILOILO 2017 Cost of Doing Business in the Province of Iloilo 2017 1 2 Cost of Doing Business in the Province of Iloilo 2017 F O R E W O R D The COST OF DOING BUSINESS is Iloilo Provincial Government’s initiative that provides pertinent information to investors, researchers, and development planners on business opportunities and investment requirements of different trade and business sectors in the Province This material features rates of utilities, such as water, power and communication rates, minimum wage rates, government regulations and licenses, taxes on businesses, transportation and freight rates, directories of hotels or pension houses, and financial institutions. With this publication, we hope that investors and development planners as well as other interested individuals and groups will be able to come up with appropriate investment approaches and development strategies for their respective undertakings and as a whole for a sustainable economic growth of the Province of Iloilo. Cost of Doing Business in the Province of Iloilo 2017 3 4 Cost of Doing Business in the Province of Iloilo 2017 TABLE OF CONTENTS Foreword I. Business and Investment Opportunities 7 II. Requirements in Starting a Business 19 III. Business Taxes and Licenses 25 IV. Minimum Daily Wage Rates 45 V. Real Property 47 VI. Utilities 57 A. Power Rates 58 B. Water Rates 58 C. Communication 59 1. Communication Facilities 59 2. Land Line Rates 59 3. Cellular Phone Rates 60 4. Advertising Rates 61 5. Postal Rates 66 6. Letter/Cargo Forwarders Freight Rates 68 VII. -

Philippines: Typhoon Fengshen

Emergency appeal n° MDRPH004 Philippines: GLIDE n° TC-2008-000093-PHL Operations update n° 4 31 December 2008 Typhoon Fengshen Period covered by this Ops Update: 24 September to 15 December 2008 Appeal target (current): CHF 8,310,213 (USD 8 million or EUR 5.1 million); with this Operations Update, the appeal has been revised to CHF 1,996,287 (USD 1,878,149 or EUR 1,343,281) <click here to view the attached Revised Emergency Appeal Budget> Appeal coverage: To date, the appeal is 87%. Funds are urgently needed to enable the Philippine National Red Cross to provide assistance to those affected by the typhoon.; <click here to go directly to the updated donor response A transitional shelter house in the midst of being built in the municipality of report, or here to link to contact Santa Barbara, Ilo Ilo province. Photo: Philippine National Red Cross. details > Appeal history: • A preliminary emergency appeal was launched on 24 June 2008 for CHF 8,310,213 (USD 8 million or EUR 5.1 million) for 12 months to assist 6,000 families. • Disaster Relief Emergency Fund (DREF): CHF 200,000 was allocated from the International Federation’s DREF. Summary: The onslaught of typhoon Fengshen which hit the Philippines on 18 June 2008, followed by floods and landslides, have left in its wake urgent needs among poverty-stricken communities. According to the National Disaster Coordinating Council (NDCC), approximately four million people have been affected through out the country by typhoon Fengshen. More than 81,000 houses were totally destroyed and a further 326,321 seriously damaged. -

Iloilo Provincial Profile 2012

PROVINCE OF ILOILO 2012 Annual Provincial Profile TIUY Research and Statistics Section i Provincial Planning and Development Office PROVINCE OF ILOILO 2012 Annual Provincial Profile P R E F A C E The Annual Iloilo Provincial Profile is one of the endeavors of the Provincial Planning and Development Office. This publication provides a description of the geography, the population, and economy of the province and is designed to principally provide basic reference material as a backdrop for assessing future developments and is specifically intended to guide and provide data/information to development planners, policy makers, researchers, private individuals as well as potential investors. This publication is a compendium of secondary socio-economic indicators yearly collected and gathered from various National Government Agencies, Iloilo Provincial Government Offices and other private institutions. Emphasis is also given on providing data from a standard set of indicators which has been publish on past profiles. This is to ensure compatibility in the comparison and analysis of information found therewith. The data references contained herewith are in the form of tables, charts, graphs and maps based on the latest data gathered from different agencies. For more information, please contact the Research and Statistics Section, Provincial Planning & Development Office of the Province of Iloilo at 3rd Floor, Iloilo Provincial Capitol, and Iloilo City with telephone nos. (033) 335-1884 to 85, (033) 509-5091, (Fax) 335-8008 or e-mail us at [email protected] or [email protected]. You can also visit our website at www.iloilo.gov.ph. Research and Statistics Section ii Provincial Planning and Development Office PROVINCE OF ILOILO 2012 Annual Provincial Profile Republic of the Philippines Province of Iloilo Message of the Governor am proud to say that reform and change has become a reality in the Iloilo Provincial Government. -

REGION 6 Address: Quintin Salas, Jaro, Iloilo City Office Number: (033) 329-6307 Email: [email protected] Regional Director: Dianne A

REGION 6 Address: Quintin Salas, Jaro, Iloilo City Office Number: (033) 329-6307 Email: [email protected] Regional Director: Dianne A. Silva Mobile Number: 0917 311 5085 Asst. Regional Director: Lolita V. Paz Mobile Number: 0917 179 9234 Provincial Office : Aklan Provincial Office Address : Linabuan sur, Banga, Aklan Office Number : (036) 267 6614 Email Address : [email protected] Provincial Manager : Benilda T. Fidel Mobile Number : 0915 295 7665 Buying Station : Aklan Grains Center Location : Linabuan Sur, Banga, Aklan Warehouse Supervisor : Ruben Gerard T. Tubao Mobile Number : 0929 816 4564 Service Areas : Municipalities of New Washington, Banga, Malinao, Makato, Lezo, Kalibo Buying Station : Oliveros Warehouse Location : Makato, Aklan Warehouse Supervisor : Iris Gail S. Lauz Mobile Number : 0906 042 8833 Service Areas : Municipalities of Makato and Lezo Buying Station : Magdael Warehouse Location : Lezo, Aklan Warehouse Supervisor : Ruben Gerard T. Tubao Mobile Number : 0929 816 4564 Service Areas : Municipalities of Malinao and Lezo Buying Station : Ibajay Buying Station Location : Ibajay, Aklan Warehouse Supervisor : Iris Gail S. Laus Mobile Number : 0906 042 8833 Service Areas : Municipality of Ibajay Buying Station : Mobile Procurement Team - 5 Location : Team Leader : Cristine B. Penuela Mobile Number : 0929 530 3103 Service Areas : Municipalities of Malinao and Ibajay Provincial Office : Antique Provincial Office Address : San Fernando, San Jose, antique Office Number : (036) 540-3697 / 0927 255 8191 Email Address : [email protected] Provincial Manager : Ma. Theresa O. Alarcon Mobile Number : 0917 596 1732 Buying Station : GID Camp Fullon Location : San Fernando, San Jose, Antique Warehouse Supervisor : Judy F. Devera Mobile Number : 0916 719 8151 Service Areas : Municipalities in Cental and Southern Antique Buying Station : GID Culasi Location : Caridad, Culasi Warehouse Supervisor : Ma. -

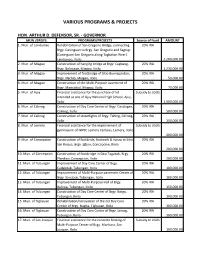

Various Programs & Projects

VARIOUS PROGRAMS & PROJECTS HON. ARTHUR D. DEFENSOR, SR. - GOVERNOR MUN./BRGYS. PROGRAMS/PROJECTS Source of Fund AMOUNT 1. Mun. of Lambunao Rehabilitation of San Gregorio Bridge, connecting 20% IRA Brgy. Caninguan to Brgy. San Gregorio and Sagcup (Caninguan-San Gregorio along Tagbakan River) Lambunao, Iloilo 2,200,000.00 2. Mun. of Miagao Construction of hanging bridge at Brgy. Cagbang- 20% IRA Brgy. Bolocaue, Miagao, Iloilo 1,230,000.00 3. Mun. of Miagao Improvement of footbridge of Sitio Buenapantao, 20% IRA Brgy. Naclub, Miagao, Iloilo 50,000.00 4. Mun. of Miagao Construction of the Multi-Purpose pavement of 20% IRA Brgy. Maricolcol, Miagao, Iloilo 70,000.00 5. Mun. of Ajuy Financial assistance for the purchase of lot Subsidy to LGUS intended as site of Ajuy National High School, Ajuy, Iloilo 1,000,000.00 6. Mun. of Calinog Construction of Day Care Center of Brgy. Caratagan, 20% IRA Calinog, Iloilo 500,000.00 7. Mun. of Calinog Construction of streetlights of Brgy. Tahing, Calinog, 20% IRA Iloilo 150,000.00 8. Mun. of Lemery Financial assistance for the improvement of Subsidy to LGUS gymnasium of NIPSC Lemery Campus, Lemery, Iloilo 400,000.00 9. Mun. of Concepcion Construction of footbride, footwalk & riprap at Sitio 20% IRA San Roque, Brgy. Igbon, Concepcion, Iloilo 200,000.00 10. Mun. of Concepcion Construction of footbridge in Sitio Tagabak, Brgy. 20% IRA Plandico, Concepcion, Iloilo 200,000.00 11. Mun. of Tubungan Improvement of Day Care Center of Brgy. 20% IRA Cadabdab, Tubungan, Iloilo 100,000.00 12. Mun. of Tubungan Improvement of Multi-Purpose pavement Center of 20% IRA Brgy. -

Last Name) (First Name)

DEPARTMENT OF LABOR AND EMPLOYMENT Regional Office No. VI Special Program for Employment of Students (SPES) List of SPES Beneficiaries CY 2018 As of DECEMBER 31, 2019 ACCOMPLISH IN CAPITAL LETTERS Name of Student No. Province Employer Address (Last Name) (First Name) 1 AKLAN LGU BALETE ARANAS CYREL KATE ARANAS, BALETE, AKLAN 2 AKLAN LGU BALETE DE JUAN MA. JOSELLE MAY MORALES, BALETE, AKLAN 3 AKLAN LGU BALETE DELA CRUZ ELIZA CORTES, BALETE, AKLAN 4 AKLAN LGU BALETE GUIBAY RESIA LYCA CALIZO, BALETE, AKLAN 5 AKLAN LGU BALETE MARAVILLA CHRISHA SEPH ALLANA POBLACION, BALETE, AKLAN 6 AKLAN LGU BALETE NAGUITA QUENNIE ANN ARCANGEL, BALETE, AKLAN 7 AKLAN LGU BALETE NERVAL ADE FULGENCIO, BALETE, AKLAN 8 AKLAN LGU BALETE QUIRINO PAULO BIANCO ARANAS, BALETE, AKLAN 9 AKLAN LGU BALETE REVESENCIO CJ POBLACION, BALETE, AKLAN 10 AKLAN LGU BALETE SAUZA LAIZEL ANNE GUANKO, BALETE, AKLAN 11 AKLAN AKLAN CATHOLIC COLLEGE AMBAY MA. JESSA CARMEN, PANDAN, ANTIQUE 12 AKLAN AKLAN CATHOLIC COLLEGE ARCEÑO SHAMARIE LYLE ANDAGAO, KALIBO, AKLAN 13 AKLAN AKLAN CATHOLIC COLLEGE BAUTISTA CATHERINE MAY BACHAO SUR, KALIBO, AKLAN 14 AKLAN AKLAN CATHOLIC COLLEGE BELINARIO JESSY ANNE LOUISE TAGAS, TANGALAN, AKLAN 15 AKLAN AKLAN CATHOLIC COLLEGE BRACAMONTE REMY CAMALIGAN, BATAN, AKLAN 16 AKLAN AKLAN CATHOLIC COLLEGE CONTRATA MA. CRISTINA ASLUM, IBAJAY, AKLAN 17 AKLAN AKLAN CATHOLIC COLLEGE CORDOVA MARVIN ANDAGAO, KALIBO, AKLAN 18 AKLAN AKLAN CATHOLIC COLLEGE DE JUAN CELESTE TAGAS, TANGALAN, AKLAN 19 AKLAN AKLAN CATHOLIC COLLEGE DELA CRUZ RALPH VINCENT BUBOG, NUMANCIA, AKLAN 20 AKLAN AKLAN CATHOLIC COLLEGE DELIMA BLESSIE JOY POBLACION, LIBACAO, AKLAN 21 AKLAN AKLAN CATHOLIC COLLEGE DESALES MA. -

Point to Point Pick Up/Drop Off Rates Kalibo to Any

POINT TO POINT PICK UP/DROP OFF RATES KALIBO TO ANY POINT OF PANAY (POINT TO POINT) RATE ORIGIN DESTINATION (VISE VERSA) KILOMETERS AUV/VAN CAR Kalibo Ajuy 4,200.00 3,900.00 Kalibo Alimodian 4,100.00 3,800.00 Kalibo Anilao 4,000.00 3,700.00 Kalibo Badiangan 3,900.00 3,600.00 Kalibo Balasan 3,800.00 3,500.00 Kalibo Banate 3,800.00 3,500.00 Kalibo Barotac Nuevo 3,900.00 3,600.00 Kalibo Barotac Viejo 3,800.00 3,500.00 Kalibo Batad 3,900.00 3,600.00 Kalibo Bingawan 3,100.00 2,900.00 Kalibo Cabatuan 3,900.00 3,600.00 Kalibo Calinog 3,200.00 3,000.00 Kalibo Carles 4,200.00 3,900.00 Kalibo Concepcion 4,200.00 3,900.00 Kalibo Dingle 3,400.00 3,100.00 Kalibo Duenas 3,300.00 3,000.00 Kalibo Dumangas 3,800.00 3,500.00 Kalibo Estancia 4,000.00 3,700.00 Kalibo Guimbal 4,300.00 4,000.00 Kalibo Igbaras 4,600.00 4,300.00 Kalibo Janiuay 3,600.00 3,300.00 Kalibo Lambunao 3,500.00 3,200.00 Kalibo Leganes 3,700.00 3,500.00 Kalibo Lemery 3,700.00 3,400.00 Kalibo Leon 4,300.00 4,000.00 Kalibo Maasin 3,900.00 3,600.00 Kalibo Miagao 4,600.00 4,300.00 Kalibo Mina 3,700.00 3,400.00 Kalibo New Lucena 3,800.00 3,500.00 Kalibo Oton 4,300.00 4,000.00 Kalibo Pavia 3,700.00 3,400.00 Kalibo Pototan 3,700.00 3,400.00 Kalibo San Dionisio 4,200.00 3,900.00 Kalibo San Enrique 3,400.00 3,100.00 Kalibo San Joaquin 4,700.00 4,400.00 Kalibo San Miguel 4,200.00 3,900.00 Kalibo San Rafael 3,500.00 3,200.00 Kalibo Santa Barbara 3,700.00 3,400.00 Kalibo Sara 4,100.00 3,800.00 Kalibo Tigbauan 4,300.00 4,000.00 Kalibo Tubungan 4,500.00 4,200.00 Kalibo Zarraga 3,700.00 3,400.00 Kalibo -

Iloilo Capiz Antique Aklan Negros Occidental

PHILIPPINES: Summary of Planned Cash Activities in REGION VI (Western Visayas) (as of 24 Feb 2014) Malay Planned Cash Activities 0 Buruanga Nabas 1 - 5 6 - 10 11 - 20 Libertad Ibajay Aklan > 20 Pandan Tangalan Numancia Makato Kalibo Lezo New Washington Malinao Banga Capiz Sebaste Roxas City Batan Panay Carles Balete Altavas Ivisan Sapi-An Madalag Pilar Balasan Estancia Panitan Mambusao Sigma Culasi Libacao Pontevedra President Roxas Batad Dao Jamindan Ma-Ayon San Dionisio Cuartero Tibiao Dumalag Sara Barbaza Tapaz Antique Dumarao Lemery Concepcion Bingawan Passi City Laua-An Calinog San Rafael Ajuy Lambunao San Enrique Bugasong Barotac Viejo Duenas Banate Negros Valderrama Dingle Occidental Janiuay Anilao Badiangan Mina Pototan Patnongon Maasin Iloilo Manapla Barotac Nuevo San Remigio Cadiz City Alimodian Cabatuan Sagay City New Lucena Victorias City Leon Enrique B. Magalona ¯ Belison Dumangas Zarraga Data Source: OCHA 3W database, Humanitarian Cluster lead organizations, GADMTubungan Santa Barbara Created 14 March 2014 San Jose Sibalom Silay City Escalante City 0 3 6 12 Km Planned Cash Activities in Region VI by Province, Municipality and Type of Activity as of 24 February 2014 Cash Grant/ Cash Grant/ Cash for Work Province Municipality Cash Voucher Transfer TOTAL (CFW) (conditional) (unconditional) BALETE 0 5 0 0 5 IBAJAY 0 0 0 1 1 AKLAN LIBACAO 0 1 0 0 1 MALINAO 0 8 0 1 9 BARBAZA 0 0 0 1 1 CULASI 0 0 0 1 1 LAUA-AN 0 0 0 1 1 ANTIQUE SEBASTE 0 0 0 1 1 TIBIAO 0 0 0 1 1 not specified 0 1 0 0 1 CUARTERO 0 0 0 1 1 DAO 0 6 0 0 6 JAMINDAN -

![Solid Waste Management Sector Project (Financed by ADB's Technical Assistance Special Fund [TASF- Other Sources])](https://docslib.b-cdn.net/cover/9882/solid-waste-management-sector-project-financed-by-adbs-technical-assistance-special-fund-tasf-other-sources-3729882.webp)

Solid Waste Management Sector Project (Financed by ADB's Technical Assistance Special Fund [TASF- Other Sources])

Technical Assistance Consultant’s Report Project Number: 45146 December 2014 Republic of the Philippines: Solid Waste Management Sector Project (Financed by ADB's Technical Assistance Special Fund [TASF- other sources]) Prepared by SEURECA and PHILKOEI International, Inc., in association with Lahmeyer IDP Consult For the Department of Environment and Natural Resources and Asian Development Bank This consultant’s report does not necessarily reflect the views of ADB or the Government concerned, and ADB and the Government cannot be held liable for its contents. All the views expressed herein may not be incorporated into the proposed project’s design. THE PHILIPPINES DEPARTMENT OF ENVIRONMENT AND NATURAL RESOURCES ASIAN DEVELOPMENT BANK SOLID WASTE MANAGEMENT SECTOR PROJECT TA-8115 PHI Final Report December 2014 In association with THE PHILIPPINES THE PHILIPPINES DEPARTMENT OF ENVIRONMENT AND NATURAL RESOURCES ASIAN DEVELOPMENT BANK SOLID WASTE MANAGEMENT SECTOR PROJECT TA-8115 PHHI SR10a Del Carmen SR12: Poverty and Social SRs to RRP from 1 to 9 SPAR Dimensions & Resettlement and IP Frameworks SR1: SR10b Janiuay SPA External Assistance to PART I: Poverty, Social Philippines Development and Gender SR2: Summary of SR10c La Trinidad PART II: Involuntary Resettlement Description of Subprojects SPAR and IPs SR3: Project Implementation SR10d Malay/ Boracay SR13 Institutional Development Final and Management Structure SPAR and Private Sector Participation Report SR4: Implementation R11a Del Carmen IEE SR14 Workshops and Field Reports Schedule and REA SR5: Capacity Development SR11b Janiuay IEEE and Plan REA SR6: Financial Management SR11c La Trinidad IEE Assessment and REAE SR7: Procurement Capacity SR11d Malay/ Boracay PAM Assessment IEE and REA SR8: Consultation and Participation Plan RRP SR9: Poverty and Social Dimensions December 2014 In association with THE PHILIPPINES EXECUTIVE SUMMARY ....................................................................................5 A. -

Province, City, Municipality Total and Barangay Population AKLAN 535,725 ALTAVAS 23,919 Cabangila 1,705 Cabugao 1,708 Catmon

2010 Census of Population and Housing Aklan Total Population by Province, City, Municipality and Barangay: as of May 1, 2010 Province, City, Municipality Total and Barangay Population AKLAN 535,725 ALTAVAS 23,919 Cabangila 1,705 Cabugao 1,708 Catmon 1,504 Dalipdip 698 Ginictan 1,527 Linayasan 1,860 Lumaynay 1,585 Lupo 2,251 Man-up 2,360 Odiong 2,961 Poblacion 2,465 Quinasay-an 459 Talon 1,587 Tibiao 1,249 BALETE 27,197 Aranas 5,083 Arcangel 3,454 Calizo 3,773 Cortes 2,872 Feliciano 2,788 Fulgencio 3,230 Guanko 1,322 Morales 2,619 Oquendo 1,226 Poblacion 830 BANGA 38,063 Agbanawan 1,458 Bacan 1,637 Badiangan 1,644 Cerrudo 1,237 Cupang 736 National Statistics Office 1 2010 Census of Population and Housing Aklan Total Population by Province, City, Municipality and Barangay: as of May 1, 2010 Province, City, Municipality Total and Barangay Population Daguitan 477 Daja Norte 1,563 Daja Sur 602 Dingle 723 Jumarap 1,744 Lapnag 594 Libas 1,662 Linabuan Sur 3,455 Mambog 1,596 Mangan 1,632 Muguing 695 Pagsanghan 1,735 Palale 599 Poblacion 2,469 Polo 1,240 Polocate 1,638 San Isidro 305 Sibalew 940 Sigcay 974 Taba-ao 1,196 Tabayon 1,454 Tinapuay 381 Torralba 1,550 Ugsod 1,426 Venturanza 701 BATAN 30,312 Ambolong 2,047 Angas 1,456 Bay-ang 2,096 Caiyang 832 Cabugao 1,948 Camaligan 2,616 Camanci 2,544 Ipil 504 Lalab 2,820 National Statistics Office 2 2010 Census of Population and Housing Aklan Total Population by Province, City, Municipality and Barangay: as of May 1, 2010 Province, City, Municipality Total and Barangay Population Lupit 1,593 Magpag-ong -

Analysis of Water Property Rights and Responsibilities of Rights Holders in Tigum-Aganan Watershed, Philippines

Philippine Journal of Science 148 (2): 289-300, June 2019 ISSN 0031 - 7683 Date Received: 17 Aug 2018 Analysis of Water Property Rights and Responsibilities of Rights Holders in Tigum-Aganan Watershed, Philippines Joy C. Lizada1*, Rosalie Arcala Hall2, Teresita S. Espinosa3, and Agnes C. Rola4 1College of Management, University of the Philippines Visayas, Miagao, Iloilo 5023 Philippines 2College of Arts and Science, Division of Social Sciences, University of the Philippines Visayas, Miagao, Iloilo 5023 Philippines 3Water Governance for Development Research, University of the Philippines Visayas, Iloilo City 5000 Philippines 4Institute for Governance and Rural Development, College of Public Affairs and Development, University of the Philippines Los Baños, College, Los Baños, Laguna 4031 Philippines The fragmentation of rights between water permit holders who exercise authority to access, exclude, and withdraw and other institutions with only shared responsibility over watershed management inhibits effective water-related decision making, resulting in conflicts that may lead to unsustainable water supply. This paper analyzes the nature and type of property rights that govern the surface water in the Philippines employing the property rights and responsibility nexus framework – using the Tigum-Aganan watershed (TAW) as a case. It explains the failure in addressing the sedimentation problem as a representation of the weak link among institutions which has adversely affected surface water supply. In addressing sustainability challenges, water property rights and the corresponding responsibilities should be clarified across the institutional hierarchy and coordinated among actors. Keywords: institutions, Philippines, property rights, surface water, Tigum-Aganan Watershed, watershed INTRODUCTION resource management. The lack of effective water right systems can create major problems in the management Water decisions and actions are products of complex of increasingly scarce water supply. -

Establishment of a Migrant Community: the Story of the Jamahs in Iloilo City ______Even Religion

Asia Pacific Journal of Multidisciplinary Research, Vol. 4, No.1, February 2016 _______________________________________________________________________________________________________________ Asia Pacific Journal of Establishment of a Migrant Community: The Multidisciplinary Research Story of the Jamahs in Iloilo City, Philippines Vol. 4 No.1,6-12 February 2016 Ronaldo F. Frufonga, Vilma S. Sulleza P-ISSN 2350-7756 West Visayas State University-Janiuay Campus, Janiuay, Iloilo, Philippines E-ISSN 2350-8442 [email protected], [email protected] www.apjmr.com Date Received: January 20, 2016; Date Revised: March 3, 2016 Abstract - This study was conceptualized to reconstruct the history of the Muslims in Iloilo City who attend worship at the San Nicolas mosque. The study employed the descriptive case study method. The in-depth and semi –structured interviews were the main tools. Other tools were informal and direct observations and focus group discussion. Inconsistencies in the narratives were straightened out in the focus group discussion. The key informants were five Maranao Muslim males from Marawi City. Reasons for migration are mostly economic and majorities are traders from Lanao Del Sur. In the 1970’s more migrants came most were single young males to avoid the then conflict between the Muslim rebels and the government troops during the Martial Law. All of the first generation migrants are males, the wives and female children followed once the males had established themselves. There were no concrete problems they have encountered as a community. The second and third generations have already adapted to the Ilonggo lifestyle. In general they encountered no resistance from the Ilonggos, instead, they feel accepted. They have no recollection of stories of resistance from the first generation migrants either.