Tirana Bank 2013 Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Ftese Per Oferte

Invitation to quote INVITATION TO QUOTE Dear Sir/Madam, 1. You are invited to present your price quotation(s) for Property Insurance services. Please see attached Annex A “Financial Quotation”. Annex B “List of Tirana Bank Branches and ATM Networks”. Annex C “List of Tirana Bank Properties”. 2. You can provide to us an estimation cost for the mentioned services which will be subject of a separate review procedure and signature of the respective contract by parties included, for the best offers. Based on the “Invitation to Quote” you should present your offer, after you have read carefully each articles specified, as parts of your assessment. 3. Your quotation(s) should be addressed in a closed envelope, and submitted to: Procurement Unit Tirana Bank, Head Office Rr. "Ibrahim Rugova", Envelope should be superscribed with “Quotation for Tender” 4. THE DEADLINE The deadline for receipt your quotation (s) by the Purchaser at the address indicated above is: 24.01.2020 -12:00 a.m. 5. TECHNICAL SPECIFICATIONS - Your offer should include: a- Financial Offer (Price) b- Technical Offer c- Legal documentations - Contract duration will be for 1 year -Deductibles: 500,000All 6. PRICE You should deliver a financial quotation for: Your are requested to give your financial offer as described in Annex A. Price (% per Sum Insured ) should be VAT and every other taxes or expenses included. - 1 - Invitation to quote 7. Technical Offer Your offer should Include: a- Details on the reinsurance agreement i.e.: -reinsurance company, -minimum amount reinsured, -duration of the reinsurance agreement, - risk coverage of the reinsurance agreement, - Premium Return Policy (Policy Cancellations and Return Premiums/refund of premiums paid), in cases of cancelation of property insurance. -

Cultural Tourism Goes Virtual: Audience Development in Southeast European Countries

CULTURAL TOURISM GOES VIRTUAL: AUDIENCE DEVELOPMENT IN SOUTHEAST EUROPEAN COUNTRIES 1 ddioio FFOREWORD.inddOREWORD.indd 1 44/7/09/7/09 11:32:47:32:47 PPMM This book has been published with the fi nancial support of the UNESCO Offi ce in Venice – UNESCO Regional Bureau for Science and Culture in Europe, City of Zagreb – City Offi ce for Education, Culture and Sports and Ministry of Science, Education and Sports The designations employed and the presentation of the material throughout this publication do not imply the expressing of any opinion whatsoever on the part of the UNESCO Secretariat concerning the legal status of any country or territory, city or area or of its authorities, the delimitations of its frontiers or boundaries. The authors are responsible for the choice and the presentation of the facts contained in this book and for the opinions expressed therein, which are not necessarily those of UNESCO and do not commit the organization. This book is a result of the research which has fi nancially been supported by the UNESCO Offi ce in Venice – UNESCO Regional Bureau for Science and Culture in Europe and Ministry of Culture of the Republic of Croatia 1 ddioio FFOREWORD.inddOREWORD.indd 2 44/7/09/7/09 11:32:50:32:50 PPMM Cultural Tourism Goes Virtual: Audience Development in Southeast European Countries Edited by Daniela Angelina Jelinčić Institute for International Relations Zagreb, 2009 1 ddioio FFOREWORD.inddOREWORD.indd 3 44/7/09/7/09 11:32:51:32:51 PPMM Culturelink Joint Publication Series No 13 Series editor Biserka Cvjetičanin Reviewers Nada Zgrabljić Rotar Nikša Alfi rević Language editing Charlotte Huntly Cover design Dragana Markanović Layout MEANDARMEDIA/Marina Belčić Printed and bound by KIKA GRAF, Zagreb Publisher Institute for International Relations Lj. -

Directory of Development Organizations

EDITION 2010 VOLUME III.A / EUROPE DIRECTORY OF DEVELOPMENT ORGANIZATIONS GUIDE TO INTERNATIONAL ORGANIZATIONS, GOVERNMENTS, PRIVATE SECTOR DEVELOPMENT AGENCIES, CIVIL SOCIETY, UNIVERSITIES, GRANTMAKERS, BANKS, MICROFINANCE INSTITUTIONS AND DEVELOPMENT CONSULTING FIRMS Resource Guide to Development Organizations and the Internet Introduction Welcome to the directory of development organizations 2010, Volume III: Europe The directory of development organizations, listing 63.350 development organizations, has been prepared to facilitate international cooperation and knowledge sharing in development work, both among civil society organizations, research institutions, governments and the private sector. The directory aims to promote interaction and active partnerships among key development organisations in civil society, including NGOs, trade unions, faith-based organizations, indigenous peoples movements, foundations and research centres. In creating opportunities for dialogue with governments and private sector, civil society organizations are helping to amplify the voices of the poorest people in the decisions that affect their lives, improve development effectiveness and sustainability and hold governments and policymakers publicly accountable. In particular, the directory is intended to provide a comprehensive source of reference for development practitioners, researchers, donor employees, and policymakers who are committed to good governance, sustainable development and poverty reduction, through: the financial sector and microfinance, -

Terms and Conditions for Individuals

TERMS AND CONDITIONS FOR INDIVIDUALS 1 TIRANA BANK Rr. Ibrahim Rugova, K. Postare 2400/1, Tiranë - Shqipëri TEL: +355 4 22 77 700 / FAX: +355 4 22 63 022 E-MAIL: [email protected] TERMS AND CONDITIONS FOR INDIVIDUALS A. ACCOUNTS 1. Current Accounts Individuals ALL, EUR, USD, GBP, CHF 1.1 Account Opening Free of Charge 1.2 Initial deposited amount / minimum balance required ALL 1,000, EUR10, GBP10, USD10,CHF10 1.3 Monthly Account Maintenance Fee ALL 150, EUR 2, USD 2, GBP 2, CHF 2, 1.4 Account Reactivation ALL 200, EUR 1.5, GBP 1.5, USD 1.5, CHF 1.5 1.5 Debit Interest ALL 12%, EUR 10%, USD 8%, GBP 10%, CHF 10% 1.6 Account Closing ALL 700, EUR 5, GBP 5, USD 7, CHF 7 1.7 Account Statement 1.7.1 Once per month (Actual month) Free of Charge 1.7.2 More frequently EUR 1/ ALL 150 / Equivalent of 1 EUR for other currencies 1.8 Cash Deposits 1.8.1 Tirana Bank Customers 1.8.1.1 Personal Accounts Free of Charge 1.8.1.2 Third Parties Accounts (Individuals + Companies) ALL 150, EUR 1, USD 1.5, GBP 1, CHF 1.5 1.8.1.3 Utility Payments (Electricity, Water, Phone, Internet, etc.) ALL 200 1.8.1.4 Public Institutions (Tax, Fine, Customs Duty, Students Fee) ALL 200 1.8.2 Non Customers 1.8.2.1 Third Parties Accounts (Individuals + Companies) ALL 250, EUR 2, USD 2.5, GBP 2, CHF 2.5 1.8.2.2 Utility Payments (Electricity, Water, Phone, Internet, etc.) ALL 500 1.8.2.3 Public Institutions (Tax, Fine, Customs Duty, Students Fee) ALL 500 1.9 Value Date 1.9.1 Cash deposit in ALL, EUR, USD, GBP, and CHF Same Value Date 1.10 Cash withdrawal 1.10.1 Amount up to daily maximum cash withdrawal limit in ATM ALL 100 1.10.2 One working day notification Free of charge 1.10.3 without prior notification - Withdrawals up to 5,000 EUR/ USD/ GBP/ CHF, 1 Mio ALL Free of charge - Withdrawals over 5,001 EUR, USD, GBP, CHF 0.1% Max EUR 100, USD 100, GBP 100 - Withdrawals over 1 Mio ALL 0.05% Max ALL 10,000 * Availability of funds upon Treasury approval Note: Future incoming funds in NOK, DKK, SEK, JPY, AUD and CAD for the existing customers will be converted in ALL, USD, EUR. -

Economic Bulletin Economic Bulletin December 2009

volume 12 volume 12 number 4 number 4 December 2009 Economic Bulletin Economic Bulletin December 2009 E C O N O M I C December B U L L E T I N 2 0 0 9 B a n k o f A l b a n i a PB Bank of Albania Bank of Albania 1 volume 12 volume 12 number 4 number 4 December 2009 Economic Bulletin Economic Bulletin December 2009 If you use data from this publication, you are requested to cite the source. Published by: Bank of Albania, Sheshi “Skënderbej”, Nr.1, Tirana, Albania Tel.: 55-4-222220; 225568; 225569 Fax.: 55-4-222558 E-mail: [email protected] www.bankofalbania.org Printed in: 70 copies Printed by Adel PRINT 2 Bank of Albania Bank of Albania volume 12 volume 12 number 4 number 4 December 2009 Economic Bulletin Economic Bulletin December 2009 content S MONETARY POLICY REPORT FOR THE SECOND HALF OF 2009 7 I. GOVERNOR’S SPEECH 7 II. DEVELOPMENTS IN THE WORLD ECONOMY 11 II.1 Economic growth and macroeconomic balances 11 II.2 Monetary Policy, Financial Markets and the Exchange rate 14 II. Oil and commodity price development 15 III. PRICE STABILITY AND BANK OF ALBANIA TARGET 16 III.1 Consumer price, inflation target and monetary policy 17 III.2 Price performance of Main CPI Basket Items 19 III. Main inflation trends 21 IV. MACROECONOMIC DEVELOPMENTS AND THEIR EFFECTS ON INFLATION 22 IV.1 Gross Domestic Product and performance of aggregate demand 2 IV.2 Labour market and wage 49 IV. -

Annual Report

BRANCHES 2 12 ANNUAL REPORT CREDIT DIVISION INTERNAL AUDIT CORPORATE DIVISION TABLE OF CONTENTS 1. MESSAGE FROM CEO E. TREASURY 2. PIRAEUS BANK GROUP F. TECHNOLOGY DEVELOPMENTS 3. TIRANA BANK OVERVIEW G. RISK A. GENERAL INFORMATION H. COMPLIANCE B. BRANCH NETWORK: MAP AND ADDRESSES I. FUNDS TRANSFER C. MAIN HIGHLIGHTS (TIMELINE) 7. CORPORATE SOCIAL RESPONSIBILITY 4. ECONOMIC OUTLOOK A. ENVIRONMENT A. INTERNATIONAL ECONOMY B. SOCIETY B. ALBANIAN ECONOMY C. CULTURE C. ALBANIAN BANKING SECTOR 8. HUMAN RESOURCES 5. TIRANA BANK MAIN RESULTs – 2012 9. FINANCIAL STATEMENTS (TABLES AND GRAPHS) A. MAIN FINANCIAL AND BUSINESS RESULTS A. CONTENTS OF THE FINANCIAL STATEMENTS B. TABLE OF FINANCIAL STATEMENTS B. INDEPENDENT AUDITor’s REPORT 6. TIRANA BANK During 2012 – PRODUCTS, PERFORMANCE & OTHERS C. INCOME STATEMENT A. RETAIL BANKING D. BALANCE SHEET B. SMEs BANKING E. StATEMENT OF CHANGES IN EQUITY C. CORPORATE BANKING F. CASH FLOW STATEMENT D. BRANCHES G. NOTES TO THE FINANCIAL STATEMENTS ANNUAL REPORT 2012 PAGE 2 01 Message from CEO In this period of challenge and uncertainty, role towards the society, economy, customers, Dear Stakeholders, Tirana Bank aimed to predominantly standby employees, and the shareholders of the Bank, and support its clients. Accordingly, it is fulfilled if we conduct our business with induced readiness of its staff towards the new transparency and integrity. Hence, adding challenges through guidance, empowerment value to the greater society and its well being and appropriate supervision. At the same time through contributing to a sound financial the core objective of protecting the interests of system, a healthy and growing economy and its shareholders was streamlined towards: a human oriented community. -

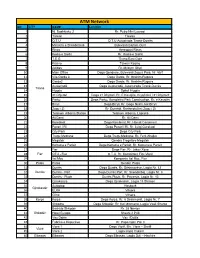

ATM Network NO CITY NAME Location 1 Nj

ATM Network NO CITY NAME Location 1 Nj. Bashkiake 2 Rr. Petro Nini Luarasi 2 Taiwan Taiwan 3 Q.T.U Q.T.U Autostrada Tiranë-Durrës 4 Ministria e Shëndetsisë Bulevardi Bajram Curri 5 Rinas Aereoport Rinas 6 Kodra e Diellit Rr. Kodra e Diellit 7 T.E.G Tirana East Gate 8 Kasino Taiwan Kasino 9 Adidas Rr. Myslym Shyri 10 Main Office Dega Qendrore, Bulevardi Zogu i Parë, Nr. 55/1 11 Vila Garda 3 Dega Garda, Rr. Ibrahim Rugova 12 Garda2 Dega Garda, Rr. Ibrahim Rugova 13 Autostradë Dega Autostradë, Autorstrada Tiranë-Durrës Tiranë 14 Hygeia Spitali Hygeia 15 21 Dhjetori Dega 21 Dhjetori, Rr. E Kavajës, Kryqëzimi i 21 Dhjetorit 16 Parku Dega Parku, Kompleksi Park Construction, Rr. e Kavajës 17 Brryli Dega Brryli, Rr. Gogo Nushi, tek Brryli 18 Zogu i Zi Rr. Durrësit, Rrethrrotullimi Zogu i Zi 19 Telekom Albania Station Telekom Albania, Laprakë 20 Ali Demi Rr. Ali Demi 21 Kombinat Dega Kombinat, Rr. Hamdi Cenoimeri 22 Pazari i Ri Dega Pazari i Ri, Rr. Luigj Gurakuqi 23 City Park Dega City Park 24 Tregu Medrese Dega Tregu Medrese, Rr. Ferit Xhajko 25 Megatek Qendra Tregëtare Megatek 26 Komuna e Parisit Dega Komuna e Parisit, Rr. Komuna e Parisit 27 Fier Dega Fier, Rr. Jakov Xoxe 28 Fier QTU - Fier Q.T.U, Rr. Kombëtare Fier-Vlorë 29 Ital Mec Kompania Ital Mec, Fier 30 Patos Patos Qendër Patos 31 Durrës Dega Durrës, Rr. Dëshmorëve, Lagjia Nr. 12 32 Durrës Durrës - Port Dega Durrës Port, Rr. Skendërbej, Lagjia Nr. 3 33 Durrës - Plazh Durrës Plazh, Rr. -

Payment Revolution in Albania - the "Creative Destruction" for a New Business Model in Banking Prof

No. 37 Publication Bankieri October 2020 PAYMENT REVOLUTION AAB MEMBERS www.aab.al CONTENT Editorial Payment revolution in Albania - The "creative destruction" for a new business model in banking Prof. Asoc. Dr. Elvin MEKA 5 Bankieri No. 37, October 2020 Frontline Publication of Albanian Association of Banks The new law on payment services - An important and welcomed development Prof.Dr. Luljeta MINXHOZI 6 The new Law on Payment Services - Challenges and opportunities for the Albanian banking sector Kerem PAMUK No. 37 Publication October 2020 Ardian HASA Bankieri Gentian CAPO 9 New developments in the field of payments - An open market for competition and quality services Geis ÇEKU, MSc. Jonida KËLLEZI Perlat SULAJ 12 Seven Systems for Smooth and Efficient Payment Operations Vladimir VASIĆ 17 Special Pandemic, public debt and the economy Anila DENAJ, Minister 19 Intervista UNION BANK – dedicated to automatization and modernization of banking services PAYMENT Flutura VEIPI 24 REVOLUTION Banking System Banks - a indispensable reality for the economy and society Dr. Spiro BRUMBULLI 26 Beyond loan holiday/moratorium - Issues to be addressed and managed by the banking sector Admira LLAZARI 28 EDITORIAL TEAM: Experts's Forum The new legislation on capital market - the right investment for developing and deepening Elvin Meka the Albanian financial system Editor-in-Chief Eftali Peçi Niko KOTONIKA 31 Coordinator Moving towards a digital-first mindset Dorina Zarka Vladimir DJORDJEVIC 33 Photographer Digital Renminbi - a technical inevitability Design & Layout: FCB Afirma Dr. Genti BEQIRI 35 Printed by: CSR 38 News From Banking Sector 42 AAB: Activities - Trainings 43 Bankieri is the official publication of EDITORIAL BOARD: the Albanian Association of Banks which mainly focuses on the Albanian Silvio PEDRAZZI Georgios PAPANASTASIOU Adrian CIVICI AAB Chairman & CEO AAB Executive Committee Dean, Faculty of banking industry. -

Positive Financial Results, in Line with the Activity Growth Strategy

special Finance POSITIVE FINANCIAL RESULTS, IN LINE WITH THE ACTIVITY GROWTH STRATEGY ritan Musatafa, General steps between the Government of Director of Tirana Bank, Albania, the Bank of Albania and Dsays for “Monitor”, that his the Banking System, in terms of bank grew in 2020 with a higher the financial support provided, the growth rate than the banking system temporary easing of the financial average. Although some branches burden for borrowers (in accordance of the economy, mainly trade and with loan moratoriums), together services, were significantly affected with the possibilities for restructuring by the consequences of the crisis, Mr. of loan obligations (in accordance Mustafa says that Tirana Bank does with the facilitations provided in the not expect a worrying increase in the implementation of the regulatory non-performing loan ratio. According framework), we estimate that they to him, Tirana Bank continues to have enabled easier coping with the adhere to the strategic objective of financial difficulties caused by the further growth of activity during 2021, pandemic, guaranteeing economic including the expansion of activity life, as well as support for gradual in Kosovo, through a representative revitalization of consumption and office. investment. alternative channels (eg: ATM investments have also affected the What are your main expectations DRITAN transactions, debit / credit cards, as decline in trade and services volumes, and objectives for business How would you assess the In your view, what were the most well as digital platforms, etc.). Debit which are the main reason that Gross performance in 2021? performance of your bank in MUSTAFA important changes brought about / credit card transactions of Tirana National Product (GNP) marked Tirana Bank continues to adhere to the 2020? What would you single by the pandemic in the way it Bank customers marked an increase negative levels in 2020. -

Student Handbook

Master of Science in Business Administration STUDENT HANDBOOK ACADEMIC YEAR 2014-2016 Contents 1. CONTACT INFORMATION .........................................................................................................4 2. UNYT ACADEMIC CALENDAR .................................................................................................5 3. UNIVERSITY INFORMATION.....................................................................................................6 MISSION STATEMENT ................................................................................................................... 6 INSTITUTIONAL GOALS ................................................................................................................ 6 VALUES.............................................................................................................................................7 UNIVERSITY HISTORY................................................................................................................... 8 ADMINISTRATION........................................................................................................................... 9 ACADEMIC DECISION AND POLICY-MAKING BODIES.......................................................... 10 GRADUATE FACULTY.................................................................................................................. 11 ACCREDITATION .......................................................................................................................... 13 PARTNERSHIPS/ -

Formulari I Fteses Per Oferte

FORMULARI I FTESES PER OFERTE FTESE PER OFERTE 1. Ju jeni te lutur te paraqitni oferten tuaj per “Sherbimin e Pastrimit te ambienteve te Tirana Bank dhe blerjen e materialeve te nevojshem per kete qellim per Zyrat Qendrore dhe Rrjetin e degeve te Tirana Bank, ne te gjithe Republiken e Shqiperise.” Per informacion me te detajuar shikoni Anekset Bashkangjitur kesaj Ftese per Oferte. 2. Ju mund te jepni oferten Tuaj per sherbimin e lartpermendur, per te cilat do te kete proçedure vleresimi dhe do te lidhet kontrate me ofertuesin me te mire. {Ju mund te paraqisni oferten tuaj duke u bazuar ne FTESEN PER OFERTE}. 3. Oferta Juaj duhet te dergohet ne adresen: Njesia e Prokurimeve Tirana Bank, Head Office Rr. "Ibrahim Rugova", Kutia Postare 2400/1. Duke Shenuar edhe subjektin e dergeses “Pjesemarrje ne tender”. 4. Afati i fundit i pranimit te ofertave eshte: 28.05.2021 ora 12 00 5. Detajet e sherbimeve te kerkuara: Sherbimi i pastrimit, i cili do te perfshije: - Pastrim ditor i te gjithe ambienteve te Bankes (zyrat qendrore dhe cdo dege), - Pastrim çdo jave i te gjitha ATM-ve Off site te Tiranes & parkingut te brendshem te zyrave qendrore . - Pastrim çdo muaj i xhamave te degeve, reklamave, ATM-ve Off site jashte Tiranes, etj. - Pastrim gjeneral çdo 3-muaj i i zyrave qendrore pastrim i fasadave te zyrave qendrore me vinc. - Sherbim çdo 6-muaj: 3D dezinfektim-deratizim-dezinsketim ne dege dhe zyrat qendrore. Pershkrim i detajuar i sherbimeve te kerkuara jepet ne Aneksin B - 1 - FORMULARI I FTESES PER OFERTE Furnizimi çdo tre muaj te Zyrave Qendrore dhe degeve me Materialet e nevojshem per sherbimin e pastrimit dhe sasite e nevojitura. -

Albania 2019

Albania 2019 1 Table of Contents Doing Business in Albania ______________________________________________ 5 Market Overview _____________________________________________________________ 5 Market Challenges ___________________________________________________________ 6 Market Opportunities _________________________________________________________ 6 Market Entry Strategy _________________________________________________________ 7 Political Environment __________________________________________________ 8 Selling US Products & Services __________________________________________ 9 Using an Agent to Sell US Products and Services _________________________________ 9 Establishing an Office ________________________________________________________ 9 Franchising ________________________________________________________________ 11 Direct Marketing ____________________________________________________________ 11 Joint Ventures/Licensing _____________________________________________________ 11 Selling to the Government ____________________________________________________ 11 Distribution & Sales Channels _________________________________________________ 12 Express Delivery ____________________________________________________________ 12 Selling Factors & Techniques _________________________________________________ 13 eCommerce ________________________________________________________________ 13 Trade Promotion & Advertising ________________________________________________ 13 Pricing ____________________________________________________________________ 13 Sales