Economic Bulletin Economic Bulletin December 2009

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

FOR TRAUMA and TORTURE of Honor

Decorated by the President THE ALBANIAN REHABILITATION CENTRE ofRepublic ofAlbania with the FOR TRAUMA AND TORTURE of Honor ALTERNATIVE REPORT To the list of issues (CAT / C ALB / 2 ), dated 15 December 2011 Prepared by the UN Committee against Torture to be considered in connection with the consideration of the second periodic report of ALBANIA AlbanianRehabilitationCentrefor Trauma and Torture(ARCT) April 2012 Contents INTRODUCTORYREMARKS 2 WITHREGARDSTO ARTICLES1 AND4 2 WITH REGARDSTO ARTICLE 2 : 2 WITH REGARDSTO ARTICLES 5-9 9 WITH REGARDSTO ARTICLE 10 ...... 10 WITH REGARDSTO ARTICLE 11: ..... ......... WITH REGARDSTO ARTICLE 14:. 11 OTHERISSUESOFCONCERN: 12 DISABLED PERSONS ...... 12 CHILDREN AND JUVENILES . 12 LEGAL AID SCHEMES 13 RECOMMENDATIONS : 13 ANNEX 1 - CASES IDENTIFIED DURING REGULAR AND AD - HOC VISITS , LETTERS AND MEDIA MONITORING 14 ANNEX 2 - COURT REPRESENTATIONOF A SELECTION OF CASES AS OF 2011:. 26 ANNEX 3 - PREVALENCEOF TORTURE AND ILL TREATMENT IN POLICE, PRE-TRIAL AND DETENTION, RESULTS FROM THE NATIONAL SURVEY BASED ON THE ARCT & SCREENING INSTRUMENT 36 1 Introductory remarks Coming from one of the most difficult and atrocious dictatorial regime, Albania is representing a challenge for the political, social and cultural developments of the Balkans, and more widely of the Europe. Since early 90s, significant legal reforms have been made hereby establishing a legal framework in the area of human rights and setting up key institutions, such as the Ombudsman's Office (People's Advocate). However, serious problems from the communist era prevail and Albania is still a society governed by weak state institutions, lack of the Rule ofLaw and widespread corruption; receiving criticisms on the implementation oflaws. -

Ftese Per Oferte

Invitation to quote INVITATION TO QUOTE Dear Sir/Madam, 1. You are invited to present your price quotation(s) for Property Insurance services. Please see attached Annex A “Financial Quotation”. Annex B “List of Tirana Bank Branches and ATM Networks”. Annex C “List of Tirana Bank Properties”. 2. You can provide to us an estimation cost for the mentioned services which will be subject of a separate review procedure and signature of the respective contract by parties included, for the best offers. Based on the “Invitation to Quote” you should present your offer, after you have read carefully each articles specified, as parts of your assessment. 3. Your quotation(s) should be addressed in a closed envelope, and submitted to: Procurement Unit Tirana Bank, Head Office Rr. "Ibrahim Rugova", Envelope should be superscribed with “Quotation for Tender” 4. THE DEADLINE The deadline for receipt your quotation (s) by the Purchaser at the address indicated above is: 24.01.2020 -12:00 a.m. 5. TECHNICAL SPECIFICATIONS - Your offer should include: a- Financial Offer (Price) b- Technical Offer c- Legal documentations - Contract duration will be for 1 year -Deductibles: 500,000All 6. PRICE You should deliver a financial quotation for: Your are requested to give your financial offer as described in Annex A. Price (% per Sum Insured ) should be VAT and every other taxes or expenses included. - 1 - Invitation to quote 7. Technical Offer Your offer should Include: a- Details on the reinsurance agreement i.e.: -reinsurance company, -minimum amount reinsured, -duration of the reinsurance agreement, - risk coverage of the reinsurance agreement, - Premium Return Policy (Policy Cancellations and Return Premiums/refund of premiums paid), in cases of cancelation of property insurance. -

Cultural Tourism Goes Virtual: Audience Development in Southeast European Countries

CULTURAL TOURISM GOES VIRTUAL: AUDIENCE DEVELOPMENT IN SOUTHEAST EUROPEAN COUNTRIES 1 ddioio FFOREWORD.inddOREWORD.indd 1 44/7/09/7/09 11:32:47:32:47 PPMM This book has been published with the fi nancial support of the UNESCO Offi ce in Venice – UNESCO Regional Bureau for Science and Culture in Europe, City of Zagreb – City Offi ce for Education, Culture and Sports and Ministry of Science, Education and Sports The designations employed and the presentation of the material throughout this publication do not imply the expressing of any opinion whatsoever on the part of the UNESCO Secretariat concerning the legal status of any country or territory, city or area or of its authorities, the delimitations of its frontiers or boundaries. The authors are responsible for the choice and the presentation of the facts contained in this book and for the opinions expressed therein, which are not necessarily those of UNESCO and do not commit the organization. This book is a result of the research which has fi nancially been supported by the UNESCO Offi ce in Venice – UNESCO Regional Bureau for Science and Culture in Europe and Ministry of Culture of the Republic of Croatia 1 ddioio FFOREWORD.inddOREWORD.indd 2 44/7/09/7/09 11:32:50:32:50 PPMM Cultural Tourism Goes Virtual: Audience Development in Southeast European Countries Edited by Daniela Angelina Jelinčić Institute for International Relations Zagreb, 2009 1 ddioio FFOREWORD.inddOREWORD.indd 3 44/7/09/7/09 11:32:51:32:51 PPMM Culturelink Joint Publication Series No 13 Series editor Biserka Cvjetičanin Reviewers Nada Zgrabljić Rotar Nikša Alfi rević Language editing Charlotte Huntly Cover design Dragana Markanović Layout MEANDARMEDIA/Marina Belčić Printed and bound by KIKA GRAF, Zagreb Publisher Institute for International Relations Lj. -

Response of the Albanian Government

CPT/Inf (2006) 25 Response of the Albanian Government to the report of the European Committee for the Prevention of Torture and Inhuman or Degrading Treatment or Punishment (CPT) on its visit to Albania from 23 May to 3 June 2005 The Albanian Government has requested the publication of this response. The report of the CPT on its May/June 2005 visit to Albania is set out in document CPT/Inf (2006) 24. Strasbourg, 12 July 2006 Response of the Albanian Government to the report of the European Committee for the Prevention of Torture and Inhuman or Degrading Treatment or Punishment (CPT) on its visit to Albania from 23 May to 3 June 2005 - 5 - REPUBLIC OF ALBANIA MINISTRY OF FOREIGN AFFAIRS Legal Representative Office No.______ Tirana, on 20.03.2006 Subject: The Albanian Authority’s Responses on the Report of the European Committee for the Prevention of Torture and other Inhuman or Degrading Treatment (CPT) The Committee for the Prevention of Torture and other Inhuman or Degrading Treatment (CPT) Mrs. Silvia CASALE - President Council of Europe - Strasbourg Dear Madam, Referring to your letter date 21 December 2005 in the report of 2005 of CPT for Albania, we inform that our state authorities are thoroughly engaged to realize the demands and recommendations made by the CPT and express their readiness to cooperate for the implementation and to take the concrete measures for the resolution of the evidenced problems in this report. Responding to your request for information as regards to the implementation of the submitted recommendations provided in the paragraphs 68, 70, 98, 131, 156 of the report within three months deadline, we inform that we have taken a response form the Ministry of Justice and the Ministry of Health meanwhile the Ministry of interior will give a response as soon as possible. -

Albania 2020 Report

EUROPEAN COMMISSION Brussels, 6.10.2020 SWD(2020) 354 final COMMISSION STAFF WORKING DOCUMENT Albania 2020 Report Accompanying the Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions 2020 Communication on EU Enlargement Policy {COM(2020) 660 final} - {SWD(2020) 350 final} - {SWD(2020) 351 final} - {SWD(2020) 352 final} - {SWD(2020) 353 final} - {SWD(2020) 355 final} - {SWD(2020) 356 final} EN EN Table of Contents 1. INTRODUCTION 3 1.1. Context 3 1.2. Summary of the report 4 2. FUNDAMENTALS FIRST: POLITICAL CRITERIA AND RULE OF LAW CHAPTERS 8 2.1. Functioning of democratic institutions and public administration reform 8 2.1.1 Democracy 8 2.1.2. Public administration reform 14 2.2.1. Chapter 23: Judiciary and fundamental rights 18 2.2.2. Chapter 24: Justice, freedom and security 37 3. FUNDAMENTALS FIRST: ECONOMIC DEVELOPMENT AND COMPETITIVENESS 51 3.1. The existence of a functioning market economy 51 3.2. The capacity to cope with competitive pressure and market forces within the Union 57 4. GOOD NEIGHBOURLY RELATIONS AND REGIONAL COOPERATION 59 5. ABILITY TO ASSUME THE OBLIGATIONS OF MEMBERSHIP 62 5.1. Chapter 1: Free movement of goods 62 5.2. Chapter 2: Freedom of movement of workers 64 5.3. Chapter 3: Right of establishment and freedom to provide services 64 5.4. Chapter 4: Free movement of capital 65 5.5. Chapter 5: Public procurement 67 5.6. Chapter 6: Company law 69 5.7. Chapter 7: Intellectual property law 70 5.8. -

Directory of Development Organizations

EDITION 2010 VOLUME III.A / EUROPE DIRECTORY OF DEVELOPMENT ORGANIZATIONS GUIDE TO INTERNATIONAL ORGANIZATIONS, GOVERNMENTS, PRIVATE SECTOR DEVELOPMENT AGENCIES, CIVIL SOCIETY, UNIVERSITIES, GRANTMAKERS, BANKS, MICROFINANCE INSTITUTIONS AND DEVELOPMENT CONSULTING FIRMS Resource Guide to Development Organizations and the Internet Introduction Welcome to the directory of development organizations 2010, Volume III: Europe The directory of development organizations, listing 63.350 development organizations, has been prepared to facilitate international cooperation and knowledge sharing in development work, both among civil society organizations, research institutions, governments and the private sector. The directory aims to promote interaction and active partnerships among key development organisations in civil society, including NGOs, trade unions, faith-based organizations, indigenous peoples movements, foundations and research centres. In creating opportunities for dialogue with governments and private sector, civil society organizations are helping to amplify the voices of the poorest people in the decisions that affect their lives, improve development effectiveness and sustainability and hold governments and policymakers publicly accountable. In particular, the directory is intended to provide a comprehensive source of reference for development practitioners, researchers, donor employees, and policymakers who are committed to good governance, sustainable development and poverty reduction, through: the financial sector and microfinance, -

Missing Segments of Ring Roads in Tirana

Missing Segments of Ring Roads in Tirana about project PROJECT DESCRIPTION The completion of the ring roads of Tirana requires a number of investments in several missing segments that are listed below: • Komuna e Parisit & Medar Shtylla Road development Project is 1.66 Km long. A new section M07 of 0.6 Km from the Outer Ring Road up to the Medar shtylla Road (Tish Daia Road) is yet to be built. The remaining existing section of 1.06 Km long from Outer Ring Road up to Bajram Curri Boulevard needs to be reconstructed; Budget -Komuna e Parisit & Medar • The Intermediate Ring Road Project is 2.16 Km long in total. A new section of 1.54 Km from Shtylla Road Development Zhan D’Ark Boulevard up to Qemal Stafa Road, from Dibra Road up to Zogu I Boulevard and ALL 1.482.000.000 -Intermediate Ring Road from Durres Road up to Myslym Shyri Road is yet to be built. The remaining existing section ALL 4.317.500.000 of 0.62 Km long stretching from Qemal Stafa Road to Dibra Road needs to be reconstructed; -Middle Ring Road ALL 2.037.600.000 • The Middle Ring Road Project is 1.36 Km long in total. A New section of 0.80 Km from Ali Demi -North section of the Outer Ring Road Road up to Qamil Guranjaku Road is yet to be built. The remaining existing section of 0.56 ALL 13.630.050.000 Km including the north section of Qemal Guranjaku Road and Asim Zeneli Road needs to be - North section of the Outer reconstructed. -

INVEST in TIRANA I TABLE of CONTENTS

INVEST in TIRANA I TABLE OF CONTENTS 01 GENERAL DATA 4 08 FIND OPPORTUNITIES IN TIRANA 19 02 EDUCATED AND PRODUCTIVE LABOR FORCE 5 09 A GREAT ENVIRONMENT FOR START UPS 23 03 A GATEWAY TO SOUTH EAST EUROPE 7 10 BOOSTING FOREIGN INVESTMENT – A STRATEGIC 25 04 TIRANA METROPOLITAN AREA - PROPITIOUS 9 LAW BUSINESS LOCATION 11 BUSINESS LICENSING 27 05 NATIONAL INCENTIVES FOR FDI 13 12 REAL ESTATE IN TIRANA 30 06 INTERNATIONAL TRADE 14 13 TIRANA AT A GLANCE 32 International Relations 07 IMPORT AND EXPORT PERMITS 16 Picture credit © Tirana Municipality 1. GENERAL DATA 2. EDUCATED AND PRODUCTIVE LABOR FORCE Tirana, the capital of Albania is a flamboyant city that is flourishing with enormous steps. It has 811 649 inhabitants and an average age of 32. The Literacy rate for adults is 96.85% (INSTAT, 2011) GENERAL DATA The economy of Tirana Metropolitan Area benefits considerably from the concentration of the largest Population 2’886’026 (INSTAT 2016) universities and schools of all levels and types in the country and also numerous research and scientific institutes, including the Academy of Sciences with its 13 institutes and the scientific research centers. Population growth rate -1% Tirana has about 180 educational institutions among which there are: Medicine, Law, Economic GDP 11.46 Billion USD Science, Engineering Science, Social Science. The Literacy rate for Youth is 98.7% (INSTAT, 2011) GDP per Capita 4’541 USD GDP growth rate 3% Tirana currently accommodates up to 100,000 students at levels 5 and 6 (undergraduate and postgraduate), gaining not only a vibrant, young population from all over Albania and neighboring Currency Albanian LEK (ALL) countries, but also a relatively well-educated labor force as many of the students stay Inflation rate 2% afterwards in Tirana. -

Terms and Conditions for Individuals

TERMS AND CONDITIONS FOR INDIVIDUALS 1 TIRANA BANK Rr. Ibrahim Rugova, K. Postare 2400/1, Tiranë - Shqipëri TEL: +355 4 22 77 700 / FAX: +355 4 22 63 022 E-MAIL: [email protected] TERMS AND CONDITIONS FOR INDIVIDUALS A. ACCOUNTS 1. Current Accounts Individuals ALL, EUR, USD, GBP, CHF 1.1 Account Opening Free of Charge 1.2 Initial deposited amount / minimum balance required ALL 1,000, EUR10, GBP10, USD10,CHF10 1.3 Monthly Account Maintenance Fee ALL 150, EUR 2, USD 2, GBP 2, CHF 2, 1.4 Account Reactivation ALL 200, EUR 1.5, GBP 1.5, USD 1.5, CHF 1.5 1.5 Debit Interest ALL 12%, EUR 10%, USD 8%, GBP 10%, CHF 10% 1.6 Account Closing ALL 700, EUR 5, GBP 5, USD 7, CHF 7 1.7 Account Statement 1.7.1 Once per month (Actual month) Free of Charge 1.7.2 More frequently EUR 1/ ALL 150 / Equivalent of 1 EUR for other currencies 1.8 Cash Deposits 1.8.1 Tirana Bank Customers 1.8.1.1 Personal Accounts Free of Charge 1.8.1.2 Third Parties Accounts (Individuals + Companies) ALL 150, EUR 1, USD 1.5, GBP 1, CHF 1.5 1.8.1.3 Utility Payments (Electricity, Water, Phone, Internet, etc.) ALL 200 1.8.1.4 Public Institutions (Tax, Fine, Customs Duty, Students Fee) ALL 200 1.8.2 Non Customers 1.8.2.1 Third Parties Accounts (Individuals + Companies) ALL 250, EUR 2, USD 2.5, GBP 2, CHF 2.5 1.8.2.2 Utility Payments (Electricity, Water, Phone, Internet, etc.) ALL 500 1.8.2.3 Public Institutions (Tax, Fine, Customs Duty, Students Fee) ALL 500 1.9 Value Date 1.9.1 Cash deposit in ALL, EUR, USD, GBP, and CHF Same Value Date 1.10 Cash withdrawal 1.10.1 Amount up to daily maximum cash withdrawal limit in ATM ALL 100 1.10.2 One working day notification Free of charge 1.10.3 without prior notification - Withdrawals up to 5,000 EUR/ USD/ GBP/ CHF, 1 Mio ALL Free of charge - Withdrawals over 5,001 EUR, USD, GBP, CHF 0.1% Max EUR 100, USD 100, GBP 100 - Withdrawals over 1 Mio ALL 0.05% Max ALL 10,000 * Availability of funds upon Treasury approval Note: Future incoming funds in NOK, DKK, SEK, JPY, AUD and CAD for the existing customers will be converted in ALL, USD, EUR. -

Annual Report

BRANCHES 2 12 ANNUAL REPORT CREDIT DIVISION INTERNAL AUDIT CORPORATE DIVISION TABLE OF CONTENTS 1. MESSAGE FROM CEO E. TREASURY 2. PIRAEUS BANK GROUP F. TECHNOLOGY DEVELOPMENTS 3. TIRANA BANK OVERVIEW G. RISK A. GENERAL INFORMATION H. COMPLIANCE B. BRANCH NETWORK: MAP AND ADDRESSES I. FUNDS TRANSFER C. MAIN HIGHLIGHTS (TIMELINE) 7. CORPORATE SOCIAL RESPONSIBILITY 4. ECONOMIC OUTLOOK A. ENVIRONMENT A. INTERNATIONAL ECONOMY B. SOCIETY B. ALBANIAN ECONOMY C. CULTURE C. ALBANIAN BANKING SECTOR 8. HUMAN RESOURCES 5. TIRANA BANK MAIN RESULTs – 2012 9. FINANCIAL STATEMENTS (TABLES AND GRAPHS) A. MAIN FINANCIAL AND BUSINESS RESULTS A. CONTENTS OF THE FINANCIAL STATEMENTS B. TABLE OF FINANCIAL STATEMENTS B. INDEPENDENT AUDITor’s REPORT 6. TIRANA BANK During 2012 – PRODUCTS, PERFORMANCE & OTHERS C. INCOME STATEMENT A. RETAIL BANKING D. BALANCE SHEET B. SMEs BANKING E. StATEMENT OF CHANGES IN EQUITY C. CORPORATE BANKING F. CASH FLOW STATEMENT D. BRANCHES G. NOTES TO THE FINANCIAL STATEMENTS ANNUAL REPORT 2012 PAGE 2 01 Message from CEO In this period of challenge and uncertainty, role towards the society, economy, customers, Dear Stakeholders, Tirana Bank aimed to predominantly standby employees, and the shareholders of the Bank, and support its clients. Accordingly, it is fulfilled if we conduct our business with induced readiness of its staff towards the new transparency and integrity. Hence, adding challenges through guidance, empowerment value to the greater society and its well being and appropriate supervision. At the same time through contributing to a sound financial the core objective of protecting the interests of system, a healthy and growing economy and its shareholders was streamlined towards: a human oriented community. -

Final Monitoring Report Final Monitoring Report

ELECTIONS FOR THE ASSEMBLY OF ALBANIA 25 JUNE 2017 FINAL MONITORING REPORT FINAL MONITORING REPORT uesv zhg e Ve Vë nd i o i r n e io c i l www.zgjedhje.al a ISBN: o K THE COALITION OF DOMESTIC OBSERVERS GRUPIM I 34 ORGANIZATAVE JOFITIMPRURËSE VENDASE, LOKALE APO QENDRORE, QË VEPROJNË NË FUSHËN E DEMOKRACISË DHE TË 9 789992 786833 DREJTAVE TË NJERIUT THE COALITION OF DOMESTIC OBSERVERS ABOUT CDO The Coalition of Domestic Observers is an alliance of non-governmental and non-partisan organizations, the core of activity of which is the development of democracy in Albania and defense for human rights, especially the observation of electoral processes. Since its establishment in 2005, the network of organizations in CDO has grown to include dozens of members. CDO considers the observation of electoral processes by citizen groups as the most appropriate instrument for ensuring transparency, integrity and credibility of elections. CDO strongly believes that engaging citizens in following electoral processes does more than just promote good elections. Empowering citizens to observe the electoral process, among other things, helps to ensure greater accountability of public officials. The leading organizations of CDO - the Society for Democratic Culture, KRIIK Albania and the For Women and Children Association - are three of the most experienced domestic groups. In fulfillment of the philosophy of action, these organizations announce relevant actions depending on the electoral or institutional process to be followed. All interested civil society organizations are invited to join the action, thus CDO re-assesses periodically, openly, and in a transparent manner the best values of network functioning. -

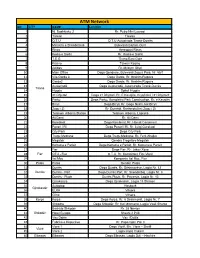

ATM Network NO CITY NAME Location 1 Nj

ATM Network NO CITY NAME Location 1 Nj. Bashkiake 2 Rr. Petro Nini Luarasi 2 Taiwan Taiwan 3 Q.T.U Q.T.U Autostrada Tiranë-Durrës 4 Ministria e Shëndetsisë Bulevardi Bajram Curri 5 Rinas Aereoport Rinas 6 Kodra e Diellit Rr. Kodra e Diellit 7 T.E.G Tirana East Gate 8 Kasino Taiwan Kasino 9 Adidas Rr. Myslym Shyri 10 Main Office Dega Qendrore, Bulevardi Zogu i Parë, Nr. 55/1 11 Vila Garda 3 Dega Garda, Rr. Ibrahim Rugova 12 Garda2 Dega Garda, Rr. Ibrahim Rugova 13 Autostradë Dega Autostradë, Autorstrada Tiranë-Durrës Tiranë 14 Hygeia Spitali Hygeia 15 21 Dhjetori Dega 21 Dhjetori, Rr. E Kavajës, Kryqëzimi i 21 Dhjetorit 16 Parku Dega Parku, Kompleksi Park Construction, Rr. e Kavajës 17 Brryli Dega Brryli, Rr. Gogo Nushi, tek Brryli 18 Zogu i Zi Rr. Durrësit, Rrethrrotullimi Zogu i Zi 19 Telekom Albania Station Telekom Albania, Laprakë 20 Ali Demi Rr. Ali Demi 21 Kombinat Dega Kombinat, Rr. Hamdi Cenoimeri 22 Pazari i Ri Dega Pazari i Ri, Rr. Luigj Gurakuqi 23 City Park Dega City Park 24 Tregu Medrese Dega Tregu Medrese, Rr. Ferit Xhajko 25 Megatek Qendra Tregëtare Megatek 26 Komuna e Parisit Dega Komuna e Parisit, Rr. Komuna e Parisit 27 Fier Dega Fier, Rr. Jakov Xoxe 28 Fier QTU - Fier Q.T.U, Rr. Kombëtare Fier-Vlorë 29 Ital Mec Kompania Ital Mec, Fier 30 Patos Patos Qendër Patos 31 Durrës Dega Durrës, Rr. Dëshmorëve, Lagjia Nr. 12 32 Durrës Durrës - Port Dega Durrës Port, Rr. Skendërbej, Lagjia Nr. 3 33 Durrës - Plazh Durrës Plazh, Rr.