BF-Sept-2018-Main-So

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

List of Candidates for Refund 2020-21

List of Candidates for Refund ( Round of I, II, III & Additional) Online Counselling 2020-21 S. Roll No Name Bank Name Branch Name IFSC Account No Name of Account Holder Refundable NO. Amount 1 200310043131 NALIN VERMA HDFC bank Lakhimpur kheri HDFC0001914 50100368464565 NALIN VERMA 15000 2 200310053526 RAUNAK KUMAR Union Bank Of India Lucknow main UBIN0530221 302202010704968 RAJENDER PRASAD 7000 3 200310062010 ADITYA JAIN BANK OF INDIA Indira nagar, lucknow BKID0006852 685210110000863 ADITYA JAIN 15000 4 200310070835 SANYA SENGAR STATE BANK OF INDIA Azad nagar, kalyanpur SBIN0001962 30091238739 SANYA SENGAR 15000 5 200310076008 NAMAN SINGH Kotak mahindra bank Civil lines bareilly KKBK0005294 619010016953 KEYERROR 7000 6 200310139507 MAYANK GARG Union Bank Shamli UBIN0541125 411202010991520 KEYERROR 15000 7 200310141073 SHUBHNEET TIWARI STATE BANK OF INDIA Manik chowk SBIN0003759 38563010993 NAVNEET TIWARI 15000 8 200310164372 DIVYANSH BAJPAI State Bank of India Karrhi SBIN0015624 32978606681 DIVYANSH BAJPAI 15000 9 200310169615 GEETIKA SINGH BANK OF INDIA Lohatia BKID0006915 691510100007669 KEYERROR 15000 10 200310181526 SAKSHAM GAUTAM Prathama U.P. Gramin Bank Kachaharii road bulandshahr PUNB0SUPGB5 91681500003267 SAKSHAM GAUTAM 15000 11 200310185397 MAYANK GUPTA STATE BANK OF INDIA Ashok nagar kanpur SBIN0006218 10417761378 AMBARISH GUPTA 15000 12 200310208513 PUNIT KUMAR PUNJAB NATIONAL BANK Afzalgarh PUNB0051500 0515000105712115 PUNIT KUMAR 7000 13 200310212525 ANKITA SINGH STATE BANK OF INDIA Jankipuram, lucknow SBIN0051291 30057228891 KEYERROR 15000 14 200310363207 SHIVANSH GUPTA BANK OF BARODA K-block kidwai nagar kanpur BARB0KIDKAN 19640100024438 SHIVANSH GUPTA 15000 SANTOSH KUMAR 15 200310395766 MANISH SRIVASTAVA State Bank Of India Industrial estate SBIN0000219 10890252471 15000 SRIVASTAVA 16 200310571706 ANURAG MISHRA Canara Bank Shyamnagar, kanpur CNRB0004964 4964101000209 PRIYANKA MISHRA 15000 17 200310620392 APARNA DUBEY State Bank of India Sbi-kannauj sarai miran p.o. -

India Financial Checks

INDIAN FINANCIAL CHECKLIST Student name Date of Birth Agent (Agency) Business Name You should provide evidence of funds as outlined below. This checklist will assist you to calculate required funds. For information on the financial capacity requirement see http://www.border.gov.au/Trav/Stud/More/Student-Visa-Living-Costs- and-Evidence-of-Funds. Instructions: Please complete this checklist and return it together with your financial documents requested to [email protected] All documents must be certified by the Financial Institution, Bank, a Notary Public or your Education Agent. If you are providing bank statements, they must be for the last 6 months ONLY and should be a summary. No more than 10 pages will be accepted. Expenses Required funds (AUD) Funds available (Please specify in AUD) Funds required for your 12 months’ tuition and living costs AUD $55,000 Add for accompanying dependants Spouse or partner Please add $7,362 Children Please add $3,152 per child TOTAL (AUD) Evidence of Financial Capacity – You must provide one of the following Sufficient funds to cover your travel costs and 12 months of living and tuition fees for you (as above AUD $55,000) plusplusplus accompanying and your family members and school costs for any school aged dependents . Source of funds Acceptable evidence includes: • Your bank statements or deposit certificates from a recognised financial institution • A signed undertaking from a private sponsor that includes an explanation of the relationship between the applicant and sponsor and evidence of financial capacity as above (maximum of 2 sponsors). Note: For married couples, if main applicant is male, funds must be from male side of the family. -

List of Banks for the Purpose of Proof of Address and Photo Identity for Passport Application

ANNEXURE List of Banks for the purpose of proof of Address and Photo identity for Passport Application A. PUBLIC SECTOR BANKS 1. AIlahabad Bank 31. Gramin Bank of Aryavart 2. Andhra Bank 32. Assam Gramin Vikash Bank 3. Bank of Baroda 33. Bangiya Gramin Vikash Bank 4. Bank of India 34. Baroda Gujarat Gramin Bank 5. Bank of Maharashtra 35. Baroda Rajasthan Kshetriya Gramin 6. Canara Bank Bank 7. Central Bank of India 36. Baroda. U P Gramin Bank 8. Corporation Bank 37. Bihar Gramin Bank 9. Dena Bank 38. Central Madhya Pradesh Gramin 10. Indian Bank Bank 11. Indian Overseas Bank 39. Chaitanya Godavari Grameena Bank 12. Oriental Bank of Commerce 40. Chhattisgarh Rajya Gramin Bank 13. Punjab National Bank 41. Deccan Grameena Bank 14. Punjab & Sind Bank 42. Dena Gujarat Gramin Bank 15. Syndicate Bank 43. Ellaquai Dehati Bank 16. Union Bank of India 44. Himachal Pradesh Gramin Bank 17. United Bank of India 45. Jharkhand Gramin Bank 18. UCO Bank 46. Jammu And Kashmir Gramin Bank 19. Vijaya Bank 47. Karnataka Vikas Grameena Bank 20. IDBI Bank Ltd 48. Kashi Gomti Samyut Gramin Bank 21. State Bank of India 49. Kaveri Grameena Bank 22. State Bank of Bikaner & Jaipur 50. Kerala Gramin Bank 23. State Bank of Patiala 51. Langpi Dehangi Rural Bank 24. State Bank of Hyderabad 52. Madhyanchal Gramin Bank 25. State Bank of Mysore 53. Maharashtra Gramin Bank 26. State Bank of Travancore 54. Malwa Gramin Bank 55. Manipur Rural Bank B. LIST OF REGIONAL RURAL BANKS 56. Marudhara Rajasthan Gramin Bank 57. Meghalaya Rural Bank 27. -

Government of India Ministry of Finance Department of Financial Services Lok Sabha Unstarred Question No

GOVERNMENT OF INDIA MINISTRY OF FINANCE DEPARTMENT OF FINANCIAL SERVICES LOK SABHA UNSTARRED QUESTION NO. 152 TO BE ANSWERED ON THE 02ND FEBRUARY, 2018 / 13 MEGHA, 1939 (SAKA) Banking and Insurance Ombudsman QUESTION 152. SHRI SHER SINGH GHUBAYA: DR. RAVINDRA KUMAR RAY: Will the Minister of FINANCE be pleased to state: (a) whether the banking and insurance ombudsman have a large number of pending claims; (b) if so, the details of the number of claims that are pending before Banking Ombudsman and Insurance Ombudsman till date, Bank/Insurance company-wise; and (c) the steps being taken by the Government to redress the claims immediately that have been pending for a long time? ANSWER THE MINISTER OF STATE IN THE MINISTRY OF FINANCE (SHRI SHIV PRATAP SHUKLA) (a) to (c): The Bank / Insurance company-wise details regarding number of complaints that are pending before Banking Ombudsman and Insurance Ombudsman as on 31.12.2017 are given in Annexure-I and Annexure-II respectively. Offices of the Banking Ombudsman have to resolve the complaints within a period of two months. However, in some cases due to delay in receipt of information / documents / clarifications, the resolution gets delayed. In case of insurance sector, the Redressal of Public Grievances Rules, 1998 have been revamped and replaced by the Insurance Ombudsman Rules, 2017. The object of these Rules is to resolve all complaints of insurance policies taken in an individual capacity, group insurance policies, policies issued to sole proprietorship and micro enterprises on the part of insurance companies and their agents and intermediaries in a cost effective and impartial manner. -

Pradhan Mantri Awas Yojana (Urban) – Housing for All Mission

PRADHAN MANTRI AWAS YOJANA (URBAN) – HOUSING FOR ALL MISSION :: CREDIT LINKED SUBSIDY SCHEME FOR EWS/LIG :: (CLSS for EWS/LIG) List of Primary Lending Institutions (PLIs) who have signed MoUs with Central Nodal Agencies1 (CNAs) (Status as on 31.10.2017) Category of PLI NHB HUDCO TOTAL Public Sector Banks 19 2 21 Private Sector Banks 14 6 20 Regional Rural Banks 38 16 54 Co-Operative Banks 19 41 60 Housing Finance Companies 79 - 79 Small Finance Bank 7 1 8 Non Banking Finance Company – Micro Finance Institution 7 1 8 Total 183 67 250 Sl. PLI Website Address Associated CNA PUBLIC SECTOR BANKS* 1. Allahabad Bank www.allahabadbank.in NHB 2. Andhra Bank www.andhrabank.in NHB 3. Bank of Baroda www.bankofbaroda.co.in NHB 4. Bank of India www.bankofindia.com NHB 5. Bank of Maharashtra www.bankofmaharashtra.in NHB 1 List sourced from Central Nodal Agencies (CNAs) i.e. National Housing Bank (NHB) & Housing and Urban Development Corporation Ltd. (HUDCO) CLSS Toll-Free Helpline Numbers: NHB: 1800-11-3377 / 1800-11-3388 and HUDCO: 1800-11-6163 Sl. PLI Website Address Associated CNA 6. Canara Bank www.canarabank.in NHB 7. Central Bank of India www.centralbankofindia.co.in HUDCO 8. Corporation Bank www.corpbank.com NHB 9. Dena Bank www.denabank.co.in NHB 10. IDBI Bank Ltd. www.idbi.com NHB 11. Indian Bank www.indian-bank.com NHB 12. Indian Overseas Bank www.iob.in NHB 13. Oriental Bank of Commerce www.obcindia.co.in NHB 14. Punjab & Sind Bank www.psbindia.com NHB 15. -

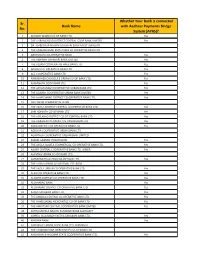

Sr. No. Bank Name Whether Your Bank Is Connected with Aadhaar

Whether Your Bank is connected Sr. Bank Name with Aadhaar Payments Bridge No. System (APBS)? 1 AKHAND ANAND CO.OP BANK LTD. Yes 2 THE AURANGABAD DISTRICT CENTRAL COOP BANK LIMITED Yes 3 DR. AMBEDKAR NAGRIK SAHAKARI BANK MYDT GWALIOR 4 THE ANDHRA BANK EMPLOYEES CO OPERATIVE BANK LTD. 5 ABHYUDAYA CO-OPERATIVE BANK Yes 6 THE ABHINAV SAHAKARI BANK LIMITED Yes 7 THE ASSAM COOPERATIVE APEX BANK LTD. Yes 8 ADARSH CO-OPERATIVE BANK LTD. Yes 9 ACE COOPERATIVE BANK LTD. Yes 10 ANNASAHEB CHOUGULE URBAN CO-OP BANK LTD. Yes 11 AMARNATH COOP BANK LTD. Yes 12 THE ARYAPURAM COOPERATIVE URBAN BANK LTD. Yes 13 THE ADARSH COOPERATIVE URBAN BANK LIMITED Yes 14 THE AHMEDABAD DISTRICT CO-OPERATIVE BANK LTD. Yes 15 ABU DHABI COMMERCIAL BANK 16 THE AKOLA DISTRICT CENTRAL COOPERATIVE BANK LTD. Yes 17 SHRI ADINATH CO-OP.BANK LTD. Yes 18 THE ADILABAD DISTRICT CO-OP CENTRAL BANK LTD. Yes 19 THE AGRASEN CO-OPERATIVE URBAN BANK LTD. Yes 20 AGRA DISTRICT CO OPERATIVE BANK LTD. Yes 21 AGROHA COOPERATIVE URBAN BANK LTD. 22 AGARTALA COOPERATIVE URBAN BANK LIMITED 23 ASSAM GRAMIN VIKASH BANK Yes 24 THE AKOLA JANATA COMMERCIAL CO-OPERATIVE BANK LTD. Yes 25 AJMER CENTRAL COOPERATIVE BANK LTD. AJMER Yes 26 AJANTHA URBAN CO-OP BANK LTD. 27 AMBARNATH JAI-HIND CO-OP.BANK LTD. Yes 28 THE AJARA URBAN CO-OP BANK LTD. BOM 29 THE AKOLA URBAN CO OPERATIVE BANK LTD. Yes 30 ALAVI CO OPERATIVE BANK LTD. Yes 31 ALIGARH DISTRICT CO OPERATIVE BANK LTD. Yes 32 ALLAHABAD BANK Yes 33 ALLAHABAD DISTRICT CO OPERATIVE BANK LTD. -

DIGITAL PAYMENTS BOOK Part1

DIGITAL PAYMENTS Trends, Issues And Opportunities July 2018 FOREWORD A Committee on Digital Payments was growth figures for both volume and value. constituted by Department of Economic Notwithstanding this the analysis finds that Affairs, Ministry of Finance in August 2016 both the data are relevant and equally under my Chairmanship to inter-alia important. They are complementary. In recommend medium term measures of addition to this the underlying growth trends promotion of Digital Payments Ecosystem in Digital Payments over the last seven in the country. The Committee submitted its years are also covered in this booklet. final report to Hon’ble Finance Minister in December 2016. One of the key This booklet has some new chapters which recommendations of the Committee related cover the areas of policy developments, to development of a metric for Digital global trends and opportunities in Digital Payments. As a follow-up on this a group of Payments. In the policy space the important Stakeholders from Different Departments of developments with respect to the Government of India and RBI was amendment of the Payment and Settlement constituted in NITI Aayog under my Act 2007 are covered. chairmanship to facilitate the work relating I am grateful to Governor, RBI, Secretary to development of the metric. This group MeitY and CEO, NPCI for their support in prepared a document on the measurement preparing this booklet. Shri. B.N. Satpathy, issues of Digital Payments. Accordingly, a Senior Consultant, EAC-PM and Shri. booklet titled “Digital Payments: Trends, Suneet Mohan, Young Professional, NITI Issues and Challenges” was prepared in Aayog have played a key role in compiling May 2017 and was released by me in July this booklet. -

Master Circular on Various Schemes on Financial Inclusion and Banking Technology

K@) \li ,/ N;\8ARl] Ref. No. NB.DFIBT/ 7981,-8459 / DFIBT - 23 / 2or8-a9 16 July zorS circular No. i 8+ / DFIBT -ztl zors The Chairman and Managing Director / Chairman / Chief Executive Officer Scheduled Commercial Banks (including Scheduled Small Finance Banks) Regional Rural Banks State Co-operative Banks and District Central Co-operative Banks Dear Sir Master Circular on various schemes on Financial Inclusion and Bankins Technolog.v NABARD has, from time to time, issued a number of guidelines/instructions to banks on various schemes that are supported out of Financial Inclusion Fund (FIF). In order to enable the banks to have instructions at one place, a Master Circular incorporating the existing guidelines/instructions on various schemes (gs indicated in Appendix) have been updated till the date of this circular and are enclosed for ready reference. z. As per the revised policy regarding Memorandum of Agreement (MoA), henceforth only one-time agreement, viz., General Agreement for Grant Assistance, may be executed by banks, which will be valid for ail the projects sanctioned to the respective bank. The bank need not sign General Agreement (GA) each time a new project is sanctioned to the bank. 3. All claims for grant assistance from FIF shoutd be submitted in accordance with the Circular No. B7/DFIBT-7112c18 dated z5 April zorS issued on the subject "Applicability of GST and Treatement of Input Tax Credit (ITC) while seitling the claims". machandran) Chief General Manager Encl.: As above Appendix Table of Contents 1. Rating of NGOs (for Commercial Banks, RRBs & RCBs) ................................................................. 1 2. Financial Literacy Centres (for RRBs & Rural Cooperative Banks) ........................................... -

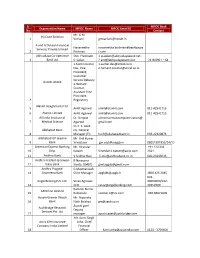

(N) Code Solution Mr. G M. Varliani [email protected] 2

Sr. MPOC Desk Organization Name MPOC Name MPOC Email ID No. Contact Mr. G M. (n) Code Solution 1 Varliani [email protected] A and A Dukaan Financial Navaneetha navaneetha.krishnan@bankbazaa Services Private Limited 2 Krishnan r.com Abhyudaya Co-operative Shri. Premnath [email protected] 3 Bank Ltd S. Salian [email protected] 2418 0961 – 64 1.Sachin Kumar [email protected] Das, Vice [email protected] President, Customer Service Delivery Aircel Limited 2.Hemant Coomar, Assistant Vice President, 4 Regulatory Alankit Assignments Ltd. 5 Ankit Agarwal [email protected] 011-42541713 6 Alankit Limited Ankit Agarwal [email protected] 011-42541713 All India Institute of Dr. Deepak aiimschairmancomputerization@ 7 Medical Science Agarwal gmail.com Sri P. S. Azad Allahabad Bank Dy. General 8 Manager (FI) [email protected] 033-22420874 Allahabad UP Gramin Mr. Anil Kumar 9 Bank Srivastava [email protected] 08052302953/54/55 American Express Banking Mr. Virender +91 124 336 10 Corp. Katoch [email protected] 2561 11 Andhra Bank V.Sridhar Rao [email protected] 040-23243033 Andhra Pradesh Grameen B Narayana 12 Vikas Bank Sresty, GM(IT) [email protected] Andhra Pragathi G.Masthanaiah 13 Grameena Bank Chief Manager [email protected] 1800 425 2045 022- Angel Broking Pvt. Ltd. Vinay Agrawal 40003600/022- 14 CEO [email protected] 39357600 Ramesh Kumar APOnline Limited 15 Kokkonda [email protected] 040-66671635 Assam Gramin Vikash Mr. Nipendra 16 Bank Nath Baishya [email protected] Ayushi goel AuthBridge Research Deputy Services Pvt. -

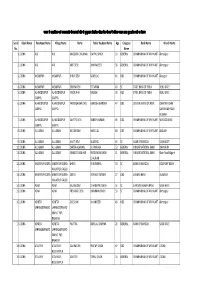

Rural List of Labharthi Parakh.Xlsx

tuin es ykHkkFkhZijd ,oa dY;k.kdkjh ;kstukUrxrZ ifr dh eqR;qijkUr fujkfJr efgyk isaku ;kstuk esa loZs{k.k mijkUr izkIr gq, izkFkZuk i=ksa dk fooj.k Serial Block Name Panchayat Name Village Name Name father husband Name Age Category Bank Name Branch Name No. Name 1 LODHA AISI AISI ANGOORI CHAUHAN OM PAL SINGH 59 GENERAL GRAMIN BANK OF ARYAVART Ahmedpur 2 LODHA AISI AISI ARTI DEVI DHARMVEER 38 GENERAL GRAMIN BANK OF ARYAVART Ahmedpur 3 LODHA AKBARPUR AKBARPUR BHURI DEVI RAMJILAL 64 OBC GRAMIN BANK OF ARYAVART Akbarpur 4 LODHA AKBARPUR AKBARPUR DROPA DEVI TOTARAM 49 SC STATE BANK OF INDIA DEHLI GATE 5 LODHA ALHADDADPUR ALHADDADPUR NOORJAHA SALEEM 39 OBC STATE BANK OF INDIA DEHLI GATE GARIYA GARIYA 6 LODHA ALHADDADPUR ALHADDADPUR PANVESHWARI DEVI RAMESH CHANDRA 47 OBC CENTRAL BANK OF INDIA KSHETRIYA SHRI GARIYA GARIYA GANDHI ASHRAM ALIGARH 7 LODHA ALHADDADPUR ALHADDADPUR SAVETRI DEVI NARESH KUMAR 46 OBC GRAMIN BANK OF ARYAVART MASOODABAD GARIYA GARIYA 8 LODHA ALL GRAM ALL GRAM KATORI DEVI NAND LAL 60 OBC GRAMIN BANK OF ARYAVART ALIGARH 9 LODHA ALL GRAM ALL GRAM MALTI DEVI VIJAY PAL 44 SC BANK OF BARODA SASNI GATE 10 LODHA ALL GRAM ALL GRAM SARITA AGARWAL JAI PRAKASH 53 GENERAL PUNJAB NATIONAL BANK DHANIPUR 11 LODHA ALL GRAM ALL GRAM SUMATI CHAUHAN PRADUMAN SINGH 51 GENERAL PUNJAB NATIONAL BANK Khair Road Aligarh CHAUHAN 12 LODHA AMARPUR KODRA AMARPUR KODRA- BHURI KUNWARPAL 53 SC BANK OF BARODA COMPANY BAGH HAVATPUR FAGOI 13 LODHA AMARPUR KODRA AMARPUR KODRA- GEETA INDRAJEET SINGH 27 OBC CANARA BANK JALALPUR HAVATPUR FAGOI 14 LODHA ASNA ASNA -

State Sponsor Bank Name of New Names of Amalgamated Sr

TABLE B17 : LIST OF AMALGAMATED REGIONAL RURAL BANKS (As on September 02, 2013) State Sponsor Bank Name of new Names of amalgamated Sr. No. Regional Rural Bank Regional Rural Banks (1) (2) (3) (4) 1. Andhra Pradesh Andhra Bank Chaitanya Godavari GB Chaitanya GB Godavari GB 2. ---------do---------- Indian Bank Saptagiri GB Kanakdurga GB Shri Venkateswara GB 3. ---------do---------- State Bank of Hyderabad Deccan GB Golconda GB Sri Rama GB Sri Saraswathi GB Sri Sathavahana GB 4. ---------do---------- State Bank of India Andhra Pradesh Grameena Kakathiya GB Vikas Bank Manjira GB Nagarjuna GB Sangameshwara GB Sri Visakha GB 5. ---------do---------- Syndicate Bank Andhra Pragathi GB Pinakini GB Rayalseema GB Sree Anantha GB 6. Assam United Bank of India Assam Gramin Vikash Bank Cachar GB Lakhimi Gaonlia GB Pragjyotish Gaonlia GB Subansiri Gaonlia GB 7. Bihar Central Bank of India Uttar Bihar KGB Champaran KGB Gopalganj KGB Madhubani KGB Mithila KGB Saran KGB Siwan KGB Vaishali KGB 8. ---------do---------- Punjab National Bank Madhya Bihar GB Bhojpur Rohtas GB Magadh GB Nalanda GB Patliputra GB 9. ---------do---------- UCO Bank Bihar KGB Begusarai KGB Bhagalpur-Banka KGB Monghyr KGB 10. ---------do---------- Central Bank of India Uttar Bihar GB Kosi KGB Uttar Bihar KGB 11. ---------do---------- State Bank of India Bihar GB Samastipur KGB UCO Bank Bihar KGB 12. Chhattisgarh State Bank of India Chhattisgarh GB Bastar KGB Bilaspur Raipur GB Raigarh KGB 13 ---------do---------- Dena Bank Chhattisgarh Rajya GB Chhattisgarh GB Surguja KGB Durg Rajnandgaon GB 14. Chennai Indian Bank Puduvai Bharathiar GB New RRB 15. Gujarat Bank of Baroda Baroda Gujarat GB Panchmahal Vadodara GB Surat Bharuch GB Valsad Dangs GB 16 ---------do---------- Dena Bank Dena Gujarat GB Banaskantha-Mehsana GB Kutch GB Sabarkantha Gandhinagar GB 17 ---------do---------- State Bank of Saurashtra Saurashtra GB Jamnagar Rajkot GB Junagadh Amreli GB Surendranagar Bhavnagar GB 18. -

IBPS RRB Bank IBPS RRB Bank Wise Language

B_w[r_ of Dupli][t_ W_\sit_ with S[rk[ri R_sult Simil[r N[m_s @lw[ys Op_n WWW.S[rk[riR_sult.Com IBPS RRB Bank Wise Language List A. PARTICIPATING RRBs Desired Local Sr. Name of the RRB Present Head State / UT Language Proficiency as No. Office prescribed by the Participating RRBs Hindi, Urdu, 1 Allahabad UP Gramin Bank Banda Uttar Pradesh Sanskrit 2 Andhra Pradesh Grameena Vikas Bank Warangal Telangana Telugu 3 Andhra Pragathi Grameena Bank Kadapa Andhra Pradesh Telugu 4 Arunachal Pradesh Rural Bank Naharlagun Arunachal Pradesh English (Papumpare) Assamese, Bengali, 5 Assam Gramin Vikash Bank Guwahati Assam Bodo 6 Bangiya Gramin Vikash Bank Murshidabad West Bengal Bengali 7 Baroda Gujarat Gramin Bank Bharuch Gujarat Gujarati 8 Baroda Rajasthan Kshetriya Gramin Ajmer Rajasthan Hindi Bank Hindi, Urdu, 9 Baroda UP Gramin Bank Raibareilly Uttar Pradesh Sanskrit 10 Bihar Gramin Bank Begusarai Bihar Hindi 11 Central Madhya Pradesh Gramin Bank Chhindwara Madhya Pradesh Hindi 12 Chaitanya Godavari Grameena Bank Guntur Andhra Pradesh Telugu 13 Chhattisgarh Rajya Gramin Bank Raipur Chhattisgarh Hindi 14 Dena Gujarat Gramin Bank Gandhinagar Gujarat Gujarati Dogri, Kashmiri, 15 Ellaquai Dehati Bank Srinagar Jammu & Kashmir Punjabi, Urdu, Gojri, Pahari, Ladakhi, Balti (Palli), Dardi, Hindi 16 Gramin Bank of Aryavart Lucknow Uttar Pradesh Hindi 17 Himachal Pradesh Gramin Bank Mandi Himachal Pradesh Hindi Dogri, Kashmiri, 18 J & K Grameen Bank Jammu Jammu & Kashmir Pahari, Gojri, Punjabi, Ladakhi, Balti (Palli), Dardi 19 Jharkhand Gramin Bank Ranchi