WINGX Analysis

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

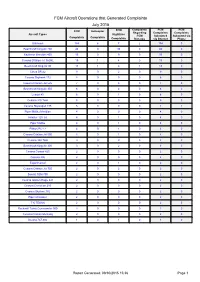

FCM Aircraft Operations That Generated Complaints July 2015

FCM Aircraft Operations that Generated Complaints July 2015 Complaints FCM FCM FCM Helicopter FCM Regarding Complaints Complaints Aircraft Types Nighttime FCM Submitted Submitted via Complaints Complaints Complaints Run-ups via Internet Phone Unknown 184 6 7 2 184 0 Beechcraft King Air 200 46 0 30 0 46 0 Raytheon Beechjet 400 15 0 9 0 15 0 Cessna Citation Jet 560XL 15 1 4 0 15 0 Beechcraft King Air 90 13 1 6 1 13 0 Cirrus SR-22 9 0 2 0 9 0 Cessna Skyhawk 172 8 0 0 0 8 0 Cessna Citation Jet 525 7 0 3 0 7 0 Beechcraft King Air 350 6 0 2 0 6 0 Learjet 45 6 0 1 0 6 0 Cessna 310 Twin 5 0 0 0 5 0 Cessna Skywagon 185 5 0 0 0 4 1 Piper Malibu Meridian 4 0 0 0 4 0 Hawker 125 Jet 4 0 1 0 4 0 Piper Malibu 4 0 1 0 4 0 Pilatus PC-12 4 0 1 0 4 0 Cessna Citation Jet 560 4 0 1 0 4 0 Cessna 340 Twin 3 0 0 0 3 0 Beechcraft King Air 300 3 0 2 0 3 0 Cessna Corsair 425 2 0 0 0 2 0 Cessna 206 2 0 0 0 2 0 Experimental 2 0 1 0 2 0 Cessna Citation Jet 750 2 0 2 0 2 0 Socata TBM 700 2 0 0 0 2 0 Cessna Golden Eagle 421 2 0 0 0 2 0 Cessna Centurion 210 2 0 0 0 2 0 Cessna Skylane 182 2 0 0 0 2 0 Piper Cherokee 2 0 0 0 2 0 T-6 TEXAN 2 0 0 0 2 0 Rockwell Turbo Commander 900 2 0 0 0 2 0 Cessna Citation Mustang 2 0 0 0 2 0 Boeing 737-900 1 0 1 0 1 0 Report Generated: 09/30/2015 15:36 Page 1 Complaints FCM FCM FCM Helicopter FCM Regarding Complaints Complaints Aircraft Types Nighttime FCM Submitted Submitted via Complaints Complaints Complaints Run-ups via Internet Phone Piper Navajo Twin 1 0 0 0 1 0 Mitsubishi MU-2 1 0 0 0 1 0 Beechcraft Debonair/Bonanza 1 0 1 0 1 0 -

ATP® Libraries Catalog

2 ATP® Libraries Catalog Revision Date May 24 2016 ATP 101 South Hill Drive Brisbane, CA 94005 (+1) 415-330-9500 www.atp.com ATP® Policies and Legal www.atp.com/policy © Copyright 2016, ATP. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form by any means, electronic, mechanical, photocopying, recording or otherwise, without prior written permission of ATP. The information in this catalog is subject to change without notice.ATP, ATP Knowledge, ATP Aviation Hub, HubConnect, NavigatorV, and their respective logos, are among the registered trademarks or trademarks of ATP. All third-party trademarks used herein are the property of their respective owners and ATP asserts no ownership rights to these items. iPad and iPhone are trademarks of Apple Inc., registered in the U.S. and other countries. App Store is a service mark of Apple Inc. All original authorship of ATP is protected under U.S. and foreign copyrights and is subject to written license agreements between ATP and its subscribers. Visit www.atp.com/policy for more information ATP Customer Support Please visit www.atp.com/support for customer support information ATP® Libraries Catalog – Revision Date: May 24 2016 3 CONTENTS CONTENTS ...................................................................................................................................................................... 3 REGULATORY LIBRARIES ............................................................................................................................................. -

Textron: Action & Results

130124 5/14/03 2:16 PM Page FC1 Textron: Action & Results 2002 Fact Book 130124 5/14/03 2:16 PM Page IFC2 Textron is an $11 billion multi-industry company with approximately 49,000 employees in 40 countries. We leverage our global network of businesses to provide customers with innovative solutions and services in industries such as aircraft, fastening systems, industrial products and components, and finance. Textron is known around the world for its powerful brands, such as Bell Helicopter, Cessna Aircraft, Kautex, Lycoming, E-Z-GO and Greenlee, among others. Stock and Contact Information Stock Exchange Listings General Information Ticker Symbol – TXT This Fact Book is one of several sources of information available to Textron Inc. shareholders and the investment community. To receive Annual Common Stock Reports, 10-K, 10-Q reports and/or press releases, please call (888) TXT- New York, Chicago and Pacific Stock Exchanges LINE or visit our website at www.textron.com Preferred Stock ($2.08 and $1.40) New York Stock Exchange Contacts Investors Mandatorily Redeemable Preferred Securities of Subsidiary Trust (7.92%) Douglas R. Wilburne New York Stock Exchange Vice President, Communications & Investor Relations [email protected] Capital Stock (401) 457-2353 (as of December 28, 2002) (401) 457-3598 (fax) Common stock: par value $0.125; 500,000,000 shares authorized; Marc Kaplan 136,499,608 shares outstanding. Director, Investor Relations $2.08 Cumulative Convertible Preferred stock, Series A: [email protected] 120,515 shares outstanding. (401) 457-2502 (401) 457-3598 (fax) $1.40 Convertible Preferred Dividend stock, Series B: 56,394 shares outstanding. -

Memscap Pressure Sensor Systems Fly to Success

MEMSCAP PRESSURE SENSOR SYSTEMS FLY TO SUCCESS Cessna Citation Mustang Equipped with 8 MEMSCAP Sensors Accomplishes Successful First Flight Grenoble, France and Durham, North Carolina, May 11, 2005 – MEMSCAP (Euronext: MEN), the leading provider of innovative solutions based on MEMS (micro-electro-mechanical systems) technology, today announced its pressure sensor technology has taken to the sky along with Cessna new Citation Mustang. Cessna, the subsidiary of multi-billion dollar company Textron (NYSE: TXT), has namely recently announced the successful first flight of its Citation Mustang - the company's newest entry-level business jet. It is equipped with MEMSCAP transducers for new lines of microprocessor-based instruments including a standby altimeter and airspeed that have been specially designed for Cessna together with 3 Cessna direct suppliers. This new Cessna Mustang that will be certified as a FAR Part 23 aircraft, with a maximum operating altitude of 41,000 feet, is embedded with 8 MEMSCAP sensors that Company provides to 3 major North American Cessna Suppliers, such as Aerosonic (cf. Press release June 16-2004). This flight is of great importance for MEMSCAP whose business in aeronautics is gaining a strong momentum as the company is providing more and more key products to major players in this industry. The new Cessna Mustang thus contains 8 MEMSCAP new technology sensors, including TP 3100 pressure module transducers and SP82 sensors family, when the former aircrafts only were equipped with 2 to 4 SP 82 sensors. " MEMSCAP sensors technology for highly demanding applications is selected today because we provide the accuracy and stability needed to exceed the end customers expectations," explains Jan Hallenstvedt, GM of MEMSCAP Sensor Solutions business unit. -

3 Minutes in the Private Jet Market

Issue 5 FLY-BY 3 Minutes in the Private Jet Market Factors Affecting Resale Prices Large, Medium & Small Cabin Market Summaries Post-Brexit Private Aviation Advice What to Know About Aircraft Financing +44 (0) 203 551 8007 ∙ www.colibriaircraft.com ∙ [email protected] Jets delivered by Gulfstream from 61 January to June - their lowest first half deliveries 127 since 2012. Minutes saved per flight using Business Aviation rather than fastest com- mercial counterpart according to a recent EBAA Study. €98 BILLION Honda Jets delivered in the first half of 2016. Economic output of Business 10 Aviation in Europe. $6,002,712 Decrease in the average 240 asking price of the Gulf- stream G550 since August Cubic feet of interior bag- 2015. gage compartment in the Embraer Legacy 600 & 650 - the largest in private jets. BREXIT & BUSINESS JETS What’s Happened Since the Vote Without question, the United Kingdom’s narrow de- The operating question gets more complicated. The cision on June 23 to leave the European Union will short answer is that it is too soon to tell any long term be one of the more significant election outcomes ramifications. But in the near term, operations of in decades. Since the referendum, our clients have UK registered aircraft into the EU and EU registered asked us: How will this affect the private jet mar- aircraft into the UK should not be affected.T he ref- ket? What does this mean for aircraft pricing? Do we erendum was a non-binding vote that merely high- need to change how we operate? Here is what we’ve lighted a narrow decision of voters. -

SPECIAL CITATION JET OWNERS SECTION! EDITOR Leroy Cook

FOR THE PILOTS OF OWNER-FLOWN, CABIN-CLASS AIRCRAFT SEPTEMBER 2015 $3.95 US VOLUME 19 NUMBER 9 Transitioning from a Single to a Citation The Prickly Parts Of Ownership Avoiding Overloading SPECIAL CITATION JET OWNERS SECTION! EDITOR LeRoy Cook EDITORIAL OFFICE 2779 Aero Park Drive Traverse City, MI 49686 Phone: (660) 679-5650 E-mail: [email protected] PUBLISHERS J. Scott Lizenby Dave Moore PRESIDENT Dave Moore CFO J. Scott Lizenby PRODUCTION MANAGER Mike Revard PUBLICATIONS DIRECTOR Steve Smith GRAPHIC DESIGN Michael McCatty ADVERTISING DIRECTOR John Shoemaker Twin & Turbine 2779 Aero Park Drive Traverse City, MI 49686 Phone: 1-800-773-7798 Garmin International Fax: (231) 946-9588 [email protected] Full Page REPRINT SALES DIRECTOR MEDIA COORDINATOR 4/C Ad ADVERTISING ADMINISTRATIVE ASSISTANT Betsy Beaudoin Phone: 1-800-773-7798 [email protected] SUBSCRIBER SERVICES Rhonda Kelly San Juana Fisher Diane Chauvin P.O. Box 968 Traverse City, MI 49685 1-800-447-7367 COVER PHOTO Photo Courtesy of Textron Aviation TWIN & TURBINE WEBSITE www.twinandturbine.com Search for the MediaWire app on your iPad. Issues of Twin & Turbine are available for free www.twinandturbine.com 2 • TWIN & TURBINE SEPTEMBER 2015 Contents SEPTEMBER 2015 • VOL. 19, NO. 9 EDITOR FEATURES LeRoy Cook 2 Editorial EDITORIAL OFFICE 2779 Aero Park Drive Avoiding Ambivalence Traverse City, MI 49686 Phone: (660) 679-5650 E-mail: [email protected] 4 In The Belly Of The Blob – Gary “Waldo” Peppers PUBLISHERS J. Scott Lizenby Dave Moore 14 Why Do Pilots Overload? 4 PRESIDENT Dave Moore Twin Proficiency CFO 16 Confident Go J. Scott Lizenby – Thomas Turner PRODUCTION MANAGER Mike Revard 20 Winning The Medical Game, Part II Cardiovascular Tips PUBLICATIONS DIRECTOR Steve Smith John Loughmiller GRAPHIC DESIGN 16 Michael McCatty From The Flight Deck 26 Cholla Airplanes ADVERTISING DIRECTOR John Shoemaker – Kevin R. -

Staying Proficient in Cessna's Mustang

| TURBINE PILOT | Staying proficient in Cessna’s Mustang IT’S THAT TIME OF YEAR AGAIN: time to go through my Cessna Citation Mustang annual proficiency check, better known as the FAR 61.58 ride. But this time there’s a twist. Well, a couple, actually. The first is that I went to Simcom’s Scottsdale, Arizona, training center, where I’d be flying a Simcom Level C, full-motion sim- ulator for the first time. The second was a biggie: I hadn’t been behind the yoke of a real live Mustang in almost a year. If expe- rienced Mustang pilots—like my classmate, John Hinshaw of Frankfort, Indiana, with 900 hours in his 2014 Mustang—dread the annual check, then I had much more to worry about. BY THOMAS A. HORNE PHOTOGRAPHY BY MIKE FIZER For a light jet under 10,000 pounds max- controls firmly, then disconnect the autopi- failure is rare, but better battery capacity my instructor, Clovis Jones Jr. Steep turns, Level C simulators have a 75-degree-wide landings (half of them day, half night). My imum gross takeoff weight, the Mustang is lot and pull the associated circuit breaker). would also be nice, especially if an instru- approaches to stalls—clean, takeoff, and field of view; Level Ds have 150-degree big challenges centered on staying ahead of pretty full-featured. It has full-authority But some memory items make you ment approach is in the offing. landing configuration, with and without fields of view. And as with Level D simula- the airplane in such fast-paced situations (it digital engine controls (FADEC) to prevent think. -

FCM Aircraft Operations That Generated Complaints August 2016

FCM Aircraft Operations that Generated Complaints August 2016 Table 1 Complaints FCM FCM Regarding Aircraft Types Nighttime FCM Complaints Complaints Run-ups Unknown 236 87 9 Beechcraft King Air 200 24 21 0 Raytheon Beechjet 400 9 9 0 Cessna Citation Jet 525 9 3 0 Aerospace 695 Jetprop Commander 7 6 0 Bombardier Challenger 300 6 6 0 Beechcraft King Air 90 6 5 2 Cessna Skyhawk 172 6 3 0 Cessna Citation Jet 560XL 6 3 0 Cirrus SR-22 6 1 0 Beechcraft Bonanza 36 5 3 0 Cessna 340 Twin 5 5 0 Pilatus PC-12 3 0 0 Beechcraft King Air 350 3 1 0 Dassault Falcon 900 3 3 0 Cessna Citation Jet 560 2 0 0 Dassault Falcon 10 2 0 0 Cessna Conquest 441 2 2 0 Cessna 208 2 0 0 Piper Malibu 2 2 0 Cirrus SR-20 2 0 0 Learjet 45 2 1 0 Mooney M-20P 2 0 0 Cessna Citation Mustang 2 2 0 Cessna Citation CJ3 1 0 0 Cessna Citation Jet 750 1 1 0 Socata TBM-850 1 0 0 Beechcraft King Air 300 1 1 0 Cessna 310 Twin 1 0 0 Cessna 206 1 0 0 Cessna Citation Jet 680 Sovereign 1 1 0 Embraer Phenom 300 1 0 0 Report Generated: 10/20/2016 13:50 Page 1 Complaints FCM FCM Regarding Aircraft Types Nighttime FCM Complaints Complaints Run-ups Piper Warrior 1 1 0 Gulfstream III* 1 0 0 Beechcraft Debonair/Bonanza 1 0 0 Beechcraft Bonanza 35 1 0 0 Floatplane 1 0 0 Embraer 135 1 1 0 Socata TBM 1 0 0 Helicopter 1 1 1 Experimental 1 0 0 Total Complaints 369 169 12 Table 2 Table 3 August August Nature of Other Totals Count* 2016 2015 Complaint Description Early/Late 165 FCM Complaints 369 424 Engine Run-up 12 Complainants (Households) 22 25 Excessive Noise 312 Frequency 234 FCM Nighttime Complaints -

FCM Aircraft Operations That Generated Complaints April 2016

FCM Aircraft Operations that Generated Complaints April 2016 Table 1 Complaints FCM FCM FCM Helicopter FCM Regarding Complaints Complaints Aircraft Types Nighttime FCM Submitted Submitted via Complaints Complaints Complaints Run-ups via Internet Phone Unknown 166 0 8 10 166 0 Beechcraft King Air 200 20 0 19 0 20 0 Cessna Citation Jet 560 10 0 6 2 10 0 Rockwell Aero Commander 500 7 0 2 0 7 0 Cessna Citation Jet 525 5 0 5 0 5 0 Raytheon Beechjet 400 5 0 3 1 5 0 Piper Malibu 4 0 1 2 4 0 Cessna Citation Jet 560XL 4 0 1 0 4 0 Beechcraft King Air 90 4 0 2 0 4 0 Cessna Skylane 182 4 0 0 0 4 0 Beechcraft Bonanza 36 3 0 0 1 3 0 Cessna Citation Jet 680 Sovereign 3 0 0 0 3 0 Cirrus SR-22 3 0 0 0 3 0 Cessna Skyhawk 172 3 0 0 0 3 0 Beechcraft King Air 350 2 0 0 0 2 0 Cessna 210T 2 0 0 0 2 0 Learjet 45 2 0 0 1 2 0 Mooney M-20P 2 0 0 0 2 0 Socata TBM-850 1 0 0 1 1 0 Hawker 125 Jet 1 0 1 0 1 0 Piper Cherokee 1 0 0 0 1 0 Beechcraft King Air 300 1 0 0 0 1 0 Beechcraft King Air 100 1 0 0 0 1 0 P-51 Mustang 1 0 0 0 0 1 Cessna Citation Mustang 1 0 0 0 1 0 Cessna Conquest 441 1 0 0 0 1 0 Cessna Centurion 210 1 0 1 0 1 0 Embraer Phenom 300 1 0 0 0 1 0 Cessna Citation CJ3 1 0 0 0 1 0 Rockwell Aero Commander 112 1 0 0 0 1 0 Cessna 340 Twin 1 0 0 0 1 0 Piper Cheyenne III Twin 1 0 0 0 1 0 Report Generated: 06/28/2016 13:01 Page 1 Complaints FCM FCM FCM Helicopter FCM Regarding Complaints Complaints Aircraft Types Nighttime FCM Submitted Submitted via Complaints Complaints Complaints Run-ups via Internet Phone Overflights (Non-FCM Operations) 16 0 1 2 16 0 Uncorrelated -

SUBJECT: February 2, 2017 Mark Reichin Propeller Airports LLC Paul

DATE: February 2, 2017 TO: Mark Reichin Propeller Airports LLC FROM: Paul Dunholter, P.E. BridgeNet International SUBJECT: Snohomish County Airport Commercial Service EA Noise Assessment - Response to Comments BACKGROUND The following memo is a response to the comments outlined in the memo “Recommended revisions to noise analysis in EA/FONSI to support incorporation into SEPA” prepared by Jason Volt on September 16, 2016. The memo listed 12 comments that are addressed below. In addition to the response to the comments, the noise contours from the Environmental Assessment (EA) were updated using the FAA’s new AEDT noise model. The results of contour updates are presented in a separate memo report dated February 1, 2017, “Snohomish County Airport (Paine Field) AEDT Noise Contour Update.” The contour update included modeling the original commercial aircraft studied in the NEPA EA as well as alternative commercial aircraft. The “original commercial aircraft” refers to the Q400 regional turbo prop aircraft and MD83 commercial aircraft assumed in the EA, while “Current Generation” refers to the EMB175 regional aircraft and 737800 commercial aircraft that reflect common aircraft used today and assumed to be in service within the planning horizon of the NEPA EA. The Maximum Throughput was also evaluated in that memo for both the assumptions presented in the EA and with an assumed higher level of activity. February 2, 2017 RESPONSE TO COMMENTS 1. Why are counts of operations in the base case (2008) higher than future year 2013 or future year 2018 operations? This is not intuitive. Existing operations numbers should be explained when the report is updated with the base case of 2016 or 2017. -

UNCLASSIFIED Washington, DC 2059 1 ACTION: PRIORITY

TELEGRAPHIC MESSAGE PRECEDENCE: SECURITY CLASSIFICATION Federal Aviation Administration PRIORITY 800 Independence Avenue, SW UNCLASSIFIED Washington, DC 2059 1 ACTION: PRIORITY ACCOUNTING CLASSIFICATION DATE PREPARED: FILE: 29 APRIL 2016 FOR INFORMATION CALL NAME PHONE NUMBER TYPE OF MESSAGE LARRY BECK (202) 267-0862 _ SINGLE _ BOOK _X_ MULTI ADDRESS MESSAGE TO BE TRANSMITTED (Use double spacing and all capital letters) TO: KRWA NOUS2 092020Z GENOT RWA 16/12 N JO 7360.001 FF ALRGNS 1/500/530 AMC-1 AMA-500 ACT-1 ALATFO XVM EFFECTIVE: 04/29/2016 SUBJECT: CHANGE TO FAA ORDER JO 7360.1, APPENDIX A, APPENDIX B, AND APPENDIX C, AIRCRAFT TYPE DESIGNATORS REVISE LAHSO GROUP NUMBERS TO THE FOLLOWING AIRCRAFT: GULFSTREAM, ROCKWELL, NORTH AMERICAN ROCKWELL -TURBO COMMANDER (ALL MODELS) AC90: LAHSO GROUP 4 LEARJET 45 LJ45: LAHSO GROUP 6 ADD LAHSO GROUP NUMBERS TO THE FOLLOWING AIRCRAFT: BEECHCRAFT, RAYTHEON- BONANZA (TURBINE) B36T: LAHSO GROUP 1 BEECHCRAFT BARON (TURBO) BE56: LAHSO GROUP 2 BEECHCRAFT QUEEN AIR BE70: LAHSO GROUP 1 BEECHCRAFT, EXCALIBUR, SWEARINGEN QUEEN AIR (ALL MODELS) BE80: LAHSO GROUP 5 BEECHCRAFT QUEEN AIR BE88: LAHSO GROUP 5 BEECHCRAFT, RAYTHEON- PREMIER PRM1: LAHSO GROUP 7 CESSNA, AJI, SCENIC 402 (TURBINE) C02T: LAHSO GROUP 6 CESSNA, OMNI 404 (TURBINE) C04T: LAHSO GROUP 4 CESSNA, SOLOY 206 (TURBINE) C06T: LAHSO GROUP 2 CESSNA, SOLOY 207 (TURBINE) C07T: LAHSO GROUP 2 CESSNA, AJI, SCENIC 414 (TURBINE) C14T: LAHSO GROUP 5 CESSNA 195 C195: LAHSO GROUP 2 CESSNA, RILEY 421 (TURBINE) C21T: LAHSO GROUP 5 CESSNA CITATION CJ2 525A C25A: -

2,000 Citationjet Takes Flight

FOR THE PILOTS OF OWNER-FLOWN, CABIN-CLASS AIRCRAFT AUGUST 2017 $3.95 US VOLUME 21 NUMBER 8 2,000th CitationJet Takes Flight Watching a New CJ3+ Come to Life Radar Guidance: Understanding the Math Flying by the Rule of 10's Miller: Meet My New Plane August 2017 Advent Aircraft Systems Inc. Full Page 4/C Ad 3 4 2 3 www.aircraftsystems.aero 2 • TWIN & TURBINE August 2017 Contents August 2017 • VOL. 21, NO. 8 2 Editor’s Briefing by Dianne White 4 3 Airmail Jet Journal 4 Three Decades of the CitationJet 2,000th CJ Takes Flight by Dianne White 8 8 Meet My New Citation CJ3+ Owner-pilot Watches His New Jet Come to Life by Marc Dulude 16 Beam Me Up Scotty! A discussion on radar 16 beam geometry by Joe Ratterman 20 Five on the Fly Meet CJP's Andrew Broom by Rebecca Groom Jacobs 20 Twin Proficiency 22 Rules of 10's Technique for Hand-Flying Precision by Thomas P. Turner From the Flight Deck 26 26 Altered States by Kevin R. Dingman On Final 32 Meet N416DM 32 by David Miller Twin & Turbine (ISSN 1945-6514), USPS 24432 is published monthly by Village Press, Inc. with advertising offices located at 2779 EDITOR ADVERTISING DIRECTOR Aero Park Drive, Traverse City, Michigan Dianne White John Shoemaker 49686. Telephone (231) 946-3712. Printed (316) 213-9626 Twin & Turbine in the United States of America. All rights [email protected] 2779 Aero Park Drive reserved. Copyright 2016, Village Press, Inc. Traverse City, MI 49686 Periodical Postage Paid at Traverse City, MI.