Barley/Malt/Beer

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

RELATÓRIO DA ADMINISTRAÇÃO O Ano De 2019 Foi Marcado Por

RELATÓRIO DA ADMINISTRAÇÃO O ano de 2019 foi marcado por investimentos transformadores em nosso portfólio, com novos líquidos e novas embalagens, inovações que buscam o crescimento sustentável da Companhia no longo prazo, alcançando um crescimento orgânico da receita líquida de 7,9%. Por outro lado, enfrentamos pressões significativas sobre o custo devido ao aumento do preço de matérias-primas denominadas em dólar, levando a um crescimento orgânico moderado do EBITDA de 1,5%, com contração orgânica da margem em 260 pontos-base. Estamos comprometidos a entregar melhores resultados em 2020, fortalecendo os fundamentos que temos construído nos últimos anos para gerar crescimento no longo prazo: (i) uma abordagem centrada no consumidor; (ii) nosso portfólio excepcional de marcas; (iii) nossa inigualável capacidade de distribuição; (iv) inovações animadoras; (v) iniciativas em tecnologia; e (vi) nossa gente. No segmento de cervejas no Brasil, introduzimos inovações em todos os segmentos de mercado e continuamos a realizar investimentos estruturais direcionados ao consumidor. Lançamos e consolidamos a marca Skol Puro Malte, que fortalece a família Skol de cervejas, e avançamos com o bom momento da marca Brahma, que manteve sua conexão com paixões brasileiras – futebol e música sertaneja. Nosso portfólio de cervejas premium manteve o forte ritmo de crescimento, de dois dígitos. O excelente desempenho das marcas globais, Budweiser, Corona e Stella Artois, assim como da cerveja Original, foi reforçado pelo lançamento de Beck’s, uma legítima cerveja puro malte alemã com sabor amargo único, e da marca Colorado Ribeirão Lager, que em poucos meses se tornou líder do segmento de cervejas artesanais no Brasil. As cervejas Nossa, Magnífica e Legítima, produzidas com mandioca de produtores locais, apresentaram resultados surpreendentes, fomentando, assim, a economia e a cultura dos estados do Nordeste onde são produzidas e vendidas. -

The Deity's Beer List.Xls

Page 1 The Deity's Beer List.xls 1 #9 Not Quite Pale Ale Magic Hat Brewing Co Burlington, VT 2 1837 Unibroue Chambly,QC 7% 3 10th Anniversary Ale Granville Island Brewing Co. Vancouver,BC 5.5% 4 1664 de Kronenbourg Kronenbourg Brasseries Stasbourg,France 6% 5 16th Avenue Pilsner Big River Grille & Brewing Works Nashville, TN 6 1889 Lager Walkerville Brewing Co Windsor 5% 7 1892 Traditional Ale Quidi Vidi Brewing St. John,NF 5% 8 3 Monts St.Syvestre Cappel,France 8% 9 3 Peat Wheat Beer Hops Brewery Scottsdale, AZ 10 32 Inning Ale Uno Pizzeria Chicago 11 3C Extreme Double IPA Nodding Head Brewery Philadelphia, Pa. 12 46'er IPA Lake Placid Pub & Brewery Plattsburg , NY 13 55 Lager Beer Northern Breweries Ltd Sault Ste.Marie,ON 5% 14 60 Minute IPA Dogfishhead Brewing Lewes, DE 15 700 Level Beer Nodding Head Brewery Philadelphia, Pa. 16 8.6 Speciaal Bier BierBrouwerij Lieshout Statiegeld, Holland 8.6% 17 80 Shilling Ale Caledonian Brewing Edinburgh, Scotland 18 90 Minute IPA Dogfishhead Brewing Lewes, DE 19 Abbaye de Bonne-Esperance Brasserie Lefebvre SA Quenast,Belgium 8.3% 20 Abbaye de Leffe S.A. Interbrew Brussels, Belgium 6.5% 21 Abbaye de Leffe Blonde S.A. Interbrew Brussels, Belgium 6.6% 22 AbBIBCbKE Lvivske Premium Lager Lvivska Brewery, Ukraine 5.2% 23 Acadian Pilsener Acadian Brewing Co. LLC New Orleans, LA 24 Acme Brown Ale North Coast Brewing Co. Fort Bragg, CA 25 Actien~Alt-Dortmunder Actien Brauerei Dortmund,Germany 5.6% 26 Adnam's Bitter Sole Bay Brewery Southwold UK 27 Adnams Suffolk Strong Bitter (SSB) Sole Bay Brewery Southwold UK 28 Aecht Ochlenferla Rauchbier Brauerei Heller Bamberg Bamberg, Germany 4.5% 29 Aegean Hellas Beer Atalanti Brewery Atalanti,Greece 4.8% 30 Affligem Dobbel Abbey Ale N.V. -

Blue Moon Belgian White Witbier / 5.4% ABV / 9 IBU / 170 CAL / Denver, CO Anheuser-Busch Bud Light Lager

BEER DRAFT Blue Moon Belgian White Pint 6 Witbier / 5.4% ABV / 9 IBU / 170 CAL / Denver, CO Pitcher 22 Blue Moon Belgian White, Belgian-style wheat ale, is a refreshing, medium-bodied, unfiltered Belgian-style wheat ale spiced with fresh coriander and orange peel for a uniquely complex taste and an uncommonly... Anheuser-Busch Bud Light Pint 6 Lager - American Light / 4.2% ABV / 6 IBU / 110 CAL / St. Louis, Pitcher 22 MO Bud Light is brewed using a blend of premium aroma hop varieties, both American-grown and imported, and a combination of barley malts and rice. Its superior drinkability and refreshing flavor... Coors Coors Light Pint 5 Lager - American Light / 4.2% ABV / 10 IBU / 100 CAL / Pitcher 18 Golden, CO Coors Light is Coors Brewing Company's largest-selling brand and the fourth best-selling beer in the U.S. Introduced in 1978, Coors Light has been a favorite in delivering the ultimate in... Deschutes Fresh Squeezed IPA Pint 7 IPA - American / 6.4% ABV / 60 IBU / 192 CAL / Bend, OR Pitcher 26 Bond Street Series- this mouthwatering lay delicious IPA gets its flavor from a heavy helping of citra and mosaic hops. Don't worry, no fruit was harmed in the making of... 7/2/2019 DRAFT Ballast Point Grapefruit Sculpin Pint 7 IPA - American / 7% ABV / 70 IBU / 210 CAL / San Diego, CA Pitcher 26 Our Grapefruit Sculpin is the latest take on our signature IPA. Some may say there are few ways to improve Sculpin’s unique flavor, but the tart freshness of grapefruit perfectly.. -

L & F to Purchase Desert Eagle Dist

Modern Brewery Age Weekly E-Newsletter •Volume 58, Number 51• December 17, 2007 Miller Brewing Co. to test “lite” craft beers Miller Brewing Co. has announced that it will test the ‘‘Miller Lite Brewers Collection,’’ a portfolio of craft-style beers that are lower in calories and carbohydrates. Miller will test the collection in four markets— Minneapolis, Charlotte, San Diego and Baltimore, beginning in February 2008. The Brewers Collection will feature three beers—Blonde Ale, an Amber and a Wheat—each with fewer calories and carbs than a typical craft beer for that style. Miller Chief Marketing Officer Randy Ransom said “Miller is seeking to again establish a whole new category for the beer industry—craft-style-light. “The brewer who can provide a more refreshing and drinkable craft style can stake out a whole new niche in the market. (Continued on Page 10) L & F to purchase Desert Eagle Dist. Desert Eagle Distributing, which controls 76 percent of El Paso's beer market is sell- ing the company to L&F Distributors, a larger McAllen, TX-based, family-owned distributor, the El Paso Times reports. "The future of the business will be large, Jim Sloan, vice president, Star Brand Imports, pours the first draft beer from a rare keg of Affligem mega wholesalers. We either had to grow Noel tapped at the Ginger Man in New York City this past week. Star Brands is importing 61 20-liter the business or sell out. In our case we had kegs of the celebrated Belgian seasonal, to be sold on draft in select accounts in the New York, no acquisition possibilities," J. -

DEPARTMENT of BUSINESS and PROFESSIONAL REGULATION DBPR Form AB&T DIVISION of ALCOHOLIC BEVERAGES and TOBACCO 4000A-032E Rev

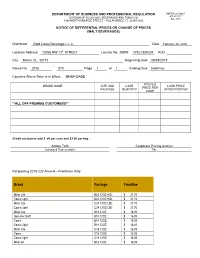

DEPARTMENT OF BUSINESS AND PROFESSIONAL REGULATION DBPR Form AB&T DIVISION OF ALCOHOLIC BEVERAGES AND TOBACCO 4000A-032E Rev. 5/04 1940 NORTH MONROE STREET • TALLAHASSEE, FL 32399-1022 NOTICE OF DIFFERENTIAL PRICES OR CHANGE OF PRICES (MALT BEVERAGES) Distributor Gold Coast Beverage L.L.C. Date February 26, 2016 Location Address 10055 NW 12th STREET License No. JDBW WSL2300224 KLD City Miami, FL 33172 Beginning Date 09/28/2015 - Notice No. 2016 074 Page 1 of 1 Ending Date Indefinite Counties Where Price is in Effect: MIAMI-DADE POSTED BRAND NAME SIZE AND CASE CASH PRICE PRICE PER PACKAGE QUANTITY AFTER POSTING CASE **ALL OFF PREMISE CUSTOMERS** Credit customers add $ .40 per case and $2.00 per keg. Amber Toth Corporate Pricing Analyst Authorized Representative Title Ref posting 2015-222 Amend – Frontlines Only Brand Package Frontline Miller Lite B24 12OZ HGL $ 21.70 Coors Light B24 12OZ HGL $ 21.70 Miller Lite C24 12OZ LSE $ 21.70 Coors Light C24 12OZ LSE $ 21.70 Miller Lite B18 12OZ $ 16.05 Genuine Draft B18 12OZ $ 16.05 Coors B18 12OZ $ 16.05 Coors Light B18 12OZ $ 16.05 Miller Lite C18 12OZ $ 16.05 Coors C18 12OZ $ 16.05 Coors Light C18 12OZ $ 16.05 Miller 64 B18 12OZ $ 16.05 Miller 64 C18 12OZ $ 16.05 Lite B24 12OZ 12P $ 21.80 Genuine Draft B24 12OZ 12P $ 21.80 Coors Light B24 12OZ 12P $ 21.80 Miller Lite C24 12OZ 12P $ 21.80 Coors Light C24 12OZ 12P $ 21.80 Coors Banquet C24 12OZ 12P $ 21.80 Coors Banquet Stubby B24 12OZ 12STB $ 21.80 Coors LT Citrus Radler C24 12OZ 12P $ 21.80 Miller Lite B24 12OZ 6P $ 22.40 Coors Light B24 12OZ -

Crc - Liquor List

2701 W Howard Street Chicago, IL 60645-1303 PH: 773.465.3900 Fax: 773.465.6632 Rabbi Sholem Fishbane Kashruth Administrator Items listed as "Recommended" do not require a kosher symbol unless they are marked with a star (*) This list is updated regularly and should be considered accurate until December 31, 2013 cRc - Liquor List Bar Stock Items Bar Stock Items Bar equipment (strainers, shot measures, blenders, stir Other rods, shakers, etc.) used with non-kosher products Olives - Green should be properly cleaned and/or kashered prior to Require Certification use with kosher products. Onions - Pearl Canned or jarred require certification Recommended Coco Lopez OU* Beer Daily's OU* All unflavored beers with no additives are acceptable, OU* Holland House even without Kosher certification. This applies to both Jamaica John cRc* American and imported beers, light, dark and non- Jero OK* alcoholic beers. Mr & Mrs T OU or OK* Many breweries produce specialty brews that have Rose's - Grenadine OU* additives; please check the label and do not assume Rose's - Lime OU* that all varieties are acceptable. Furthermore, beers known to be produced at microbreweries, pub K* Tabasco - Hot Pepper Sauce breweries, or craft breweries require certification. Underberg - Herb Mix for Underberg OU* Natural Herb Bitters Recommended Other 800 - Ice Beer OU Bitters Anheuser-Busch - Redbridge Gluten Require Certification Free Coconut Milk Aspen Edge - Lager OU Requires Certification Blue Moon - Belgian White Ale OU* Cream of Coconut Blue Moon - Full Moon Winter Ale -

View Presentation

WORLD BREWING CONGRESS 2016 World Brewing Congress August 13-17, 2016 Prospective demand for malting barley and malt quality for the global brewing industry Sheraton Downtown Denver 159 Peter Watts1, Dr. Yueshu Li1 and Dr. Jessica Yu2 Denver, CO 80202, U.S.A. 1. Canadian Malting Barley Technical Centre, Winnipeg, Manitoba, Canada R3C 3G7 2. Tsingtao Brewery Co. Ltd, Qingdao, China 266100 Introduction China Beer Market Evolving Quality Requirements Rapid changes in the world brewing industry including the boom in craft brewing, diversification in In addition to international brewing groups such as Carlsberg and AB-InBev, China Resource Snow Brewery, Tsingtao Brewery, and Beijing Yangjing Beer are dominant Rising beer production in China and the rapid development of craft brewing in the US beer brand/style as well as changing ownership present both challenges and opportunities for the players in China accounting for 71% of beer output. Increasingly Chinese beer manufacturers are strengthening their brand positioning. In 2014 China Resources Snow are driving increased demand for malting barley and malt, and are also shifting quality malting barley industry. In this presentation, trends in global malting and brewing sectors, Breweries produced 107 million hectolitres of Snow beer making it the world’s largest beer brand at 5.4% of the global market. Its total volume is higher than the requirements. In China, brewers are demanding barley with higher grain protein and specifically in China and the United States, and changing quality requirements for malting barley combined volume of Budweiser (4.6 billion liters) and Budlight (5.0 billion liters). Together with Tsingtao Brewery and Beijing Yangjing Beer, these three Chinese brewers very high enzyme potential to compensate for large adjunct incorporation. -

Our Imprint Report 2020

OUR IMPRINT OUR IMPRINT IMPRINT OUR REPORT 2020 REPORT A r o u OU n R d I o M f P g o R o I d N n T e s s OUR IMPRINT REPORT 2020 Contents INTRODUCTION 03 SUSTAINABLY BREWING 18 CEO Letter 03 Safeguarding Our About Molson Coors Most Precious Resource 20 Beverage Company 04 On the Road to 1.5°C 22 Building a Business With On a Loop: Moving Toward a Positive Imprint 06 a Circular Economy 24 Our Imprint 2025 07 The Future of Farming 28 RESPONSIBLY REFRESHING 08 COLLECTIVELY CRAFTED 30 Responsible Refreshment 10 Supporting Our People Talking to the Right Audience 13 Through Challenging Times 32 Understanding What Goes Into Every Sip 15 Lifting Up Our Communities 36 Options to Satisfy Every Taste 16 Building an Ethical Supply Chain 38 About This Report Welcome to the Molson Coors Our Imprint We have continued our commitment to Report 2020. This report contains updates report against international frameworks, on Our Imprint 2025 goals, including such as the Global Reporting Initiative key stories and relevant highlights of our (GRI) Standards, the Ten Principles of performance against our sustainability the UN Global Compact (UNGC), the focus areas. Sustainability Accounting Standards Board (SASB) and alignment with the United Following the initiation of a revitalization Nations (UN) Sustainable Development plan in the fourth quarter of 2019, in Goals (SDGs). January 2020 the newly named Molson Coors Beverage Company restructured Full details of our 2019 performance, to comprise two operating business units: aligned to these global frameworks, are North America and Europe. -

Tsingtao Brewery Company Case Study Tsingtao Brewery Co., Ltd

Tsingtao Brewery Company Case Study Tsingtao Brewery Co., Ltd., one of the oldest beer makers in China, was founded in 1903 by German and British merchants under the name Nordic Brewery Co., Ltd. Tsingtao Branch. Today, Tsingtao Brewery is China’s largest brewery and was also an Official Sponsor of the Beijing 2008 Olympic Games. On July 15, 1993, Tsingtao Brewery became the first-ever Chinese company to be listed on the Hong Kong Stock Exchange (stock code 0168). On August 27, 1993, it listed on the Shanghai Stock Exchange (stock code: 600600), making Tsingtao Brewery the first Chinese company to be listed in both Mainland China and Hong Kong. China now has about 500 breweries, nearly one for every three counties, but 80 per cent have an annual production capacity of less than 50,000 tons and most have operational difficulties. This has spelled opportunities for the three heavyweights, Tsingtao, Yanjing and China Resources. They have all pursued a domestic expansion plan through numerous strategic mergers, purchasing insolvent companies, reorganization, and joint-venture partnerships. Still, in spite of its having the second largest market in the world, China still has a long way to go because per capita beer consumption annually is only about 15 liters, compared to 84 liters in the United States. In 2007, Tsingtao Brewery achieved a total sales volume of 5.05 million kiloliters globally, with the market share of Tsingtao Beer in China reaching 13% . In that same year, World Brand Lab valued the brand at RMB 25.827 billion, placing it first in China’s brewing industry. -

Annual Report 2013 Management Financial Review Statements

Annual Report 2013 Management Financial review statements 3 The Carlsberg Group at a glance 54 Consolidated financial statements 8 Letter from the Chairman 140 Parent Company 9 Statement from the CEO 160 Management statement 12 In the spotlight: Supply chain 161 Auditors’ report 13 Our regions 19 In the spotlight: China 20 Our business model and Strategy Wheel 21 KPIs 22 Strategy 28 CSR in the value chain 29 CSR targets 30 In the spotlight: Self-regulation 31 Risk management 35 In the spotlight: Sponsorships 36 Corporate governance 43 Remuneration report 49 Executive Committee 50 Shareholder information 52 Financial review 162 Supervisory Board DISCLAIMER This Annual Report contains forward-looking may contain the words “believe, anticipate, then current expectations or forecasts. Such actual results to differ materially from those distribution-related issues, information tech- not be possible for management to predict all statements, including statements about the expect, estimate, intend, plan, project, will be, information is subject to the risk that such expressed in its forward-looking statements nology failures, breach or unexpected termina- such risk factors, nor to assess the impact of Group’s sales, revenues, earnings, spending, will continue, will result, could, may, might”, expectations or forecasts, or the assumptions include, but are not limited to: economic and tion of contracts, price reductions resulting all such risk factors on the Group’s business or margins, cash flow, inventory, products, or any variations of such words or other words underlying such expectations or forecasts, may political uncertainty (including interest rates from market-driven price reductions, market the extent to which any individual risk factor, actions, plans, strategies, objectives and with similar meanings. -

FIC Guide 2009/10

Guide to the Foreign Investors Council / 3 SPECIAL EDITION CONTENTS Guide to the STABLE BANKING SECTOR PHARMACEUTICALS RECESSION RESISTANT COMMENT - Radovan Jelašić, Gover- MARKET ANALYSIS FOREIGN by Erste Group 6 nor of the National Bank of Serbia 50 PREPARING FOR THE END OF THE CRISIS INVESTORS INTERVIEW - Aleksandar BUSINESS NEWS 8 Radosavljević, FIC President and 53 COUNCIL CEO of Carlsberg Srbija ADVANTAGES IN CRISIS 2009/2010 INVESTING IN SCIENTIFIC INFRASTRUC- INTERVIEW TURE 54 - Michael Kefalopoulos, General INTERVIEW - Božidar Đelić, Deputy Director of Mellon d.o.o. FASTER REFORMS REQUIRED IMPRESSUM 14 Serbian Prime Minister and Minister of Science & Technology INTERVIEW - Nenad Vuković, EDITOR IN CHIEF LEADERS 56 Member of the FIC Board of Direc- Tatjana Ostojić 20 tors, President of Henkel Serbia [email protected] SEEKING CONSISTENCY BUSINESS NEWS EDITOR INTERVIEW - Kjell-Morten Johnsen, 59 EU-STANDARD LAWS Mark R. Pullen 22 FIC Vice President, CEO of Telenor YEAR OF CRISIS & REFORM BUSINESS - Jelena Pejčinović ART DIRECTOR INTERVIEW - Nebojša Ćirić, 60 (FIC), Executive Secretary of the Tamara Ivljanin ADCPI Committee [email protected] 26 State Secretary in the Serbian Economy and Regional BUSINESS EDITORIAL Development Ministry 61 NEWS CONTRIBUTORS WORLD ECONOMIC FORUM REGULATING A CHANGING INDUSTRY Mark R. Pullen, Ana Stojanović Switzerland INTERVIEW - Vera Nikolić Dimić (Vip Mobile), Head of the FIC Tel- PHOTO 30 on top 62 Slobodan Jotić NEW FIXED-LINE OPERATORS ecommunications Committee and INTERVIEW - Jasna Matić, Serbian -

Monitoring Branżowy Analizy Sektorowe

Monitoring Branżowy Analizy Sektorowe 10 kwietnia 2017 Rynek piwa1 w Polsce zdominowany przez firmy zagraniczne Trendy bieżące Departament Analiz Ekonomicznych W 2016 r. produkcja piwa w Polsce wzrosła o 0,5% r/r (wobec spadku o 1,1% r/r w 2015 r.), sięgając 40,7 mln hl. Polska jest trzecim producentem Zespół Analiz Sektorowych piwa w UE. [email protected] W 2016 r. sytuacja ekonomiczno-finansowa producentów piwa nieznacznie pogorszyła się r/r, choć rentowność sprzedaży pozostała na poziomie Anna Senderowicz wyższym niż średnio w przetwórstwie przemysłowym. tel. 22 521 81 24 Od kilku lat spożycie piwa w Polsce utrzymuje się na stabilnym poziomie, oscylując w granicach 98-99 litrów na osobę. Udział podatku akcyzowego i VAT w cenie detalicznej piwa kształtuje się w granicach 35-37%. Dochody budżetu z akcyzy w 2015 r. wyniosły 3,6 mld zł. W siedmiu spośród 26 średnich i dużych firm wytwarzających piwo dominuje kapitał zagraniczny, ich udział w przychodach ogółem w 2016 r. sięgał 87%, a w zysku netto 93%. Ponad 80% rynku piwa należy do trzech producentów: Kompanii Piwowarskiej (właścicielem jest japońska grupa Asahi), Grupy Żywiec (grupa Heineken) oraz Carlsberg Polska (grupa Carlsberg). Perspektywy krótkoterminowe W krótkiej perspektywie sytuacja branży może się nieco poprawić z uwagi na wzrost wartości sprzedaży pod wpływem spodziewanych wyższych cen piwa oraz wzrostu popytu piwa markowe (efekt lepszej sytuacji gospodarstw domowych). Z drugiej strony wysokie nasycenie rynku i silna konkurencja między browarami będzie czynnikiem ograniczającym wzrost branży. Szanse to tendencja częstszego spożywania posiłków poza domem (podczas których zamawia się piwo), rozwój browarów rzemieślniczych, a także rozwijający się eksport piwa do krajów UE.