Parliamentary Debates House of Commons Official Report General Committees

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

PSG Website Report 24 Nov 2020

Summary of Background to Haven Hotel planning application Quick Read ● A planning application to demolish the Haven Hotel and replace it with blocks of flats will likely soon be decided by BCP Council ● The current proposal envisages three, six-storey blocks of flats totalling 119 apartments in place of the existing hotel ● Over 3 ½ years after application first filed, BCP planning committee likely to decide it in the first three months of next year (2021) ● An exact date for the BCP planning committee to make a final decision is not yet clear ● SCG oppose the current Haven plans for reasons explained below ● The National Trust, Natural England and Dorset AONB still oppose the plans ● Over 3000 people have filed formal objections against the plans ● The developers have sought to downplay the public's objections on grounds plans have changed since people filed many of those objections ● SCG has launched a new campaign to raise public awareness & encourage people to object, even if they have already opposed - watch this space What is happening to the Haven? BCP Council is getting close to deciding on whether to approve plans to demolish the Haven Hotel and replace it with blocks of flats. This note prepared by Sandbanks Community Group (SCG) explains the background and the issues in more detail. What is history? In April 2017, owners FJB Hotels (owned by the Butterworth family - John Butterworth is CEO) and their planning adviser, Richard Carr, filed plans to demolish the Haven Hotel, the Sandbanks Hotel and the Harbour Heights Hotel. The original plans envisaged that two completely new hotels would replace Harbour Heights and Sandbanks Hotels with a contemporary design. -

THE 422 Mps WHO BACKED the MOTION Conservative 1. Bim

THE 422 MPs WHO BACKED THE MOTION Conservative 1. Bim Afolami 2. Peter Aldous 3. Edward Argar 4. Victoria Atkins 5. Harriett Baldwin 6. Steve Barclay 7. Henry Bellingham 8. Guto Bebb 9. Richard Benyon 10. Paul Beresford 11. Peter Bottomley 12. Andrew Bowie 13. Karen Bradley 14. Steve Brine 15. James Brokenshire 16. Robert Buckland 17. Alex Burghart 18. Alistair Burt 19. Alun Cairns 20. James Cartlidge 21. Alex Chalk 22. Jo Churchill 23. Greg Clark 24. Colin Clark 25. Ken Clarke 26. James Cleverly 27. Thérèse Coffey 28. Alberto Costa 29. Glyn Davies 30. Jonathan Djanogly 31. Leo Docherty 32. Oliver Dowden 33. David Duguid 34. Alan Duncan 35. Philip Dunne 36. Michael Ellis 37. Tobias Ellwood 38. Mark Field 39. Vicky Ford 40. Kevin Foster 41. Lucy Frazer 42. George Freeman 43. Mike Freer 44. Mark Garnier 45. David Gauke 46. Nick Gibb 47. John Glen 48. Robert Goodwill 49. Michael Gove 50. Luke Graham 51. Richard Graham 52. Bill Grant 53. Helen Grant 54. Damian Green 55. Justine Greening 56. Dominic Grieve 57. Sam Gyimah 58. Kirstene Hair 59. Luke Hall 60. Philip Hammond 61. Stephen Hammond 62. Matt Hancock 63. Richard Harrington 64. Simon Hart 65. Oliver Heald 66. Peter Heaton-Jones 67. Damian Hinds 68. Simon Hoare 69. George Hollingbery 70. Kevin Hollinrake 71. Nigel Huddleston 72. Jeremy Hunt 73. Nick Hurd 74. Alister Jack (Teller) 75. Margot James 76. Sajid Javid 77. Robert Jenrick 78. Jo Johnson 79. Andrew Jones 80. Gillian Keegan 81. Seema Kennedy 82. Stephen Kerr 83. Mark Lancaster 84. -

Members of the House of Commons December 2019 Diane ABBOTT MP

Members of the House of Commons December 2019 A Labour Conservative Diane ABBOTT MP Adam AFRIYIE MP Hackney North and Stoke Windsor Newington Labour Conservative Debbie ABRAHAMS MP Imran AHMAD-KHAN Oldham East and MP Saddleworth Wakefield Conservative Conservative Nigel ADAMS MP Nickie AIKEN MP Selby and Ainsty Cities of London and Westminster Conservative Conservative Bim AFOLAMI MP Peter ALDOUS MP Hitchin and Harpenden Waveney A Labour Labour Rushanara ALI MP Mike AMESBURY MP Bethnal Green and Bow Weaver Vale Labour Conservative Tahir ALI MP Sir David AMESS MP Birmingham, Hall Green Southend West Conservative Labour Lucy ALLAN MP Fleur ANDERSON MP Telford Putney Labour Conservative Dr Rosena ALLIN-KHAN Lee ANDERSON MP MP Ashfield Tooting Members of the House of Commons December 2019 A Conservative Conservative Stuart ANDERSON MP Edward ARGAR MP Wolverhampton South Charnwood West Conservative Labour Stuart ANDREW MP Jonathan ASHWORTH Pudsey MP Leicester South Conservative Conservative Caroline ANSELL MP Sarah ATHERTON MP Eastbourne Wrexham Labour Conservative Tonia ANTONIAZZI MP Victoria ATKINS MP Gower Louth and Horncastle B Conservative Conservative Gareth BACON MP Siobhan BAILLIE MP Orpington Stroud Conservative Conservative Richard BACON MP Duncan BAKER MP South Norfolk North Norfolk Conservative Conservative Kemi BADENOCH MP Steve BAKER MP Saffron Walden Wycombe Conservative Conservative Shaun BAILEY MP Harriett BALDWIN MP West Bromwich West West Worcestershire Members of the House of Commons December 2019 B Conservative Conservative -

Stephen Kinnock MP Aberav

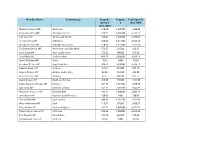

Member Name Constituency Bespoke Postage Total Spend £ Spend £ £ (Incl. VAT) (Incl. VAT) Stephen Kinnock MP Aberavon 318.43 1,220.00 1,538.43 Kirsty Blackman MP Aberdeen North 328.11 6,405.00 6,733.11 Neil Gray MP Airdrie and Shotts 436.97 1,670.00 2,106.97 Leo Docherty MP Aldershot 348.25 3,214.50 3,562.75 Wendy Morton MP Aldridge-Brownhills 220.33 1,535.00 1,755.33 Sir Graham Brady MP Altrincham and Sale West 173.37 225.00 398.37 Mark Tami MP Alyn and Deeside 176.28 700.00 876.28 Nigel Mills MP Amber Valley 489.19 3,050.00 3,539.19 Hywel Williams MP Arfon 18.84 0.00 18.84 Brendan O'Hara MP Argyll and Bute 834.12 5,930.00 6,764.12 Damian Green MP Ashford 32.18 525.00 557.18 Angela Rayner MP Ashton-under-Lyne 82.38 152.50 234.88 Victoria Prentis MP Banbury 67.17 805.00 872.17 David Duguid MP Banff and Buchan 279.65 915.00 1,194.65 Dame Margaret Hodge MP Barking 251.79 1,677.50 1,929.29 Dan Jarvis MP Barnsley Central 542.31 7,102.50 7,644.81 Stephanie Peacock MP Barnsley East 132.14 1,900.00 2,032.14 John Baron MP Basildon and Billericay 130.03 0.00 130.03 Maria Miller MP Basingstoke 209.83 1,187.50 1,397.33 Wera Hobhouse MP Bath 113.57 976.00 1,089.57 Tracy Brabin MP Batley and Spen 262.72 3,050.00 3,312.72 Marsha De Cordova MP Battersea 763.95 7,850.00 8,613.95 Bob Stewart MP Beckenham 157.19 562.50 719.69 Mohammad Yasin MP Bedford 43.34 0.00 43.34 Gavin Robinson MP Belfast East 0.00 0.00 0.00 Paul Maskey MP Belfast West 0.00 0.00 0.00 Neil Coyle MP Bermondsey and Old Southwark 1,114.18 7,622.50 8,736.68 John Lamont MP Berwickshire Roxburgh -

Letter to Ms Saxby: Cummings

North Devon Dear Ms Saxby, RE: Dominic Cummings I hope you're keeping well at this turbulent time. The British people have been trying to come to grips with the restrictions imposed by lockdown in an effort to contain the virus. Although these measures have led to hardship for some and heartbreaking separation for others, we have seen an extraordinary resilience in the belief that 'we are all in this together'. This has generated an expectation by everyone to stay at home in order to save lives - it was that simple. The groundswell of disbelief and disgust at the news of Dominic Cummings flouting the rules he has been so involved in developing is therefore quite understandable. You will be aware, of course, that these feelings are shared across North Devon. Many people have been left wondering why it is one rule for the entire nation and another one for Cummings and Johnson's top team. In a recent tweet, North Devon Liberal Democrats summed up the mood of North Devon, we said 'we're especially sorry to those who haven't been able to hold the hands of their loved ones as they passed, whilst Cummings thinks he's above the rules". I echo the point that many people have made immense sacrifices to protect the NHS and save lives, but this hasn't been repaid by Cummings in flouting the rules, or indeed the new 'stay alert' message which has seen tourists flock to Devon and Cornwall. A number of Conservative Members of Parliament have put constituents above party to denounce Dominic Cummings for breaking lockdown. -

House of Commons Wednesday 31 October 2012 Votes and Proceedings

No. 59 451 House of Commons Wednesday 31 October 2012 Votes and Proceedings The House met at 11.30 am. PRAYERS. 1 Questions to (1) the Secretary of State for International Development (2) the Prime Minister 2 European Union Free Movement Directive 2004 (Disapplication): Motion for leave to bring in a Bill (Standing Order No. 23) Motion made and Question proposed, That leave be given to bring in a Bill to disapply the European Union Free Movement Directive 2004/38/EC; and for connected purposes.—(Mr Stewart Jackson.) Motion opposed (Standing Order No. 23(1)). Question put, and agreed to. Ordered, That Mr Stewart Jackson, Heather Wheeler, Mr Frank Field, Priti Patel, Mr Philip Hollobone, Gordon Henderson, Henry Smith, Mr Andrew Turner, Zac Goldsmith, Caroline Nokes, Kate Hoey and Mr James Clappison present the Bill. Mr Stewart Jackson accordingly presented the Bill. Bill read the first time; to be read a second time on Friday 14 December, and to be printed (Bill 86). 3 Local Government Finance Bill (Programme) (No. 3) Motion made and Question put forthwith (Standing Order No. 83A(7)), That the following provisions shall apply to the Local Government Finance Bill for the purpose of supplementing the Orders of 10 January 2012 in the last session (Local Government Finance Bill (Programme)) and 21 May 2012 (Local Government Finance Bill (Programme) (No. 2)): Consideration of Lords Amendments 1. Proceedings on consideration of Lords Amendments shall (so far as not previously concluded) be brought to a conclusion three hours after their commencement at today’s sitting. Subsequent stages 2. -

Our Ref : 0241

Our ref : 0241 January 2017 Dear Parents / Carers Following my letter yesterday regarding the Fairer Funding Formula consultation I have been overwhelmed by your support. Thank you, this means an awful lot! You may have seen this story in the national press this morning. It has been sensibly suggested that I write a model letter for you to send to your MP or to the Minister(s) and I include this along with names and contact details below. Secretary of State for Education – Justine Greening MP [email protected] House of Commons, London, SW1A 0AA Minister for Schools – Nick Gibb MP [email protected] House of Commons, London, SW1A 0AA Mid Dorset and North Poole – Michael Tomlinson MP [email protected] House of Commons, London, SW1A 0AA Poole BC – Robert Syms MP [email protected] Poole Conservative Association, 38 Sandbanks Road, Poole, BH14 8BX Thank you for your support – I hope that with our combined efforts we can change the Ministers’ approach. Yours sincerely Tracy Harris Address Address Address Date Dear I write to outline my very serious concerns about the impact of the proposed National Fair Funding Formula on my daughter’s school, Parkstone Grammar School in Poole. Let us be clear that we do not disagree with many of the principles of which the National Fair Funding Formula is based. It is not morally acceptable for a family’s post code to dictate how much funding a school receives to educate a child and we agree that more resources are needed to help a disadvantaged child and a child with low prior attainment make good progress. -

Whole Day Download the Hansard

Monday Volume 691 15 March 2021 No. 190 HOUSE OF COMMONS OFFICIAL REPORT PARLIAMENTARY DEBATES (HANSARD) Monday 15 March 2021 © Parliamentary Copyright House of Commons 2021 This publication may be reproduced under the terms of the Open Parliament licence, which is published at www.parliament.uk/site-information/copyright/. HER MAJESTY’S GOVERNMENT MEMBERS OF THE CABINET (FORMED BY THE RT HON. BORIS JOHNSON, MP, DECEMBER 2019) PRIME MINISTER,FIRST LORD OF THE TREASURY,MINISTER FOR THE CIVIL SERVICE AND MINISTER FOR THE UNION— The Rt Hon. Boris Johnson, MP CHANCELLOR OF THE EXCHEQUER—The Rt Hon. Rishi Sunak, MP SECRETARY OF STATE FOR FOREIGN,COMMONWEALTH AND DEVELOPMENT AFFAIRS AND FIRST SECRETARY OF STATE— The Rt Hon. Dominic Raab, MP SECRETARY OF STATE FOR THE HOME DEPARTMENT—The Rt Hon. Priti Patel, MP CHANCELLOR OF THE DUCHY OF LANCASTER AND MINISTER FOR THE CABINET OFFICE—The Rt Hon. Michael Gove, MP LORD CHANCELLOR AND SECRETARY OF STATE FOR JUSTICE—The Rt Hon. Robert Buckland, QC, MP SECRETARY OF STATE FOR DEFENCE—The Rt Hon. Ben Wallace, MP SECRETARY OF STATE FOR HEALTH AND SOCIAL CARE—The Rt Hon. Matt Hancock, MP COP26 PRESIDENT—The Rt Hon. Alok Sharma, MP SECRETARY OF STATE FOR BUSINESS,ENERGY AND INDUSTRIAL STRATEGY—The Rt Hon. Kwasi Kwarteng, MP SECRETARY OF STATE FOR INTERNATIONAL TRADE AND PRESIDENT OF THE BOARD OF TRADE, AND MINISTER FOR WOMEN AND EQUALITIES—The Rt Hon. Elizabeth Truss, MP SECRETARY OF STATE FOR WORK AND PENSIONS—The Rt Hon. Dr Thérèse Coffey, MP SECRETARY OF STATE FOR EDUCATION—The Rt Hon. -

Urgent Open Letter to Jesse Norman Mp on the Loan Charge

URGENT OPEN LETTER TO JESSE NORMAN MP ON THE LOAN CHARGE Dear Minister, We are writing an urgent letter to you in your new position as the Financial Secretary to the Treasury. On the 11th April at the conclusion of the Loan Charge Debate the House voted in favour of the motion. The Will of the House is clearly for an immediate suspension of the Loan Charge and an independent review of this legislation. Many Conservative MPs have criticised the Loan Charge as well as MPs from other parties. As you will be aware, there have been suicides of people affected by the Loan Charge. With the huge anxiety thousands of people are facing, we believe that a pause and a review is vital and the right and responsible thing to do. You must take notice of the huge weight of concern amongst MPs, including many in your own party. It was clear in the debate on the 4th and the 11th April, that the Loan Charge in its current form is not supported by a majority of MPs. We urge you, as the Rt Hon Cheryl Gillan MP said, to listen to and act upon the Will of the House. It is clear from their debate on 29th April that the House of Lords takes the same view. We urge you to announce a 6-month delay today to give peace of mind to thousands of people and their families and to allow for a proper review. Ross Thomson MP John Woodcock MP Rt Hon Sir Edward Davey MP Jonathan Edwards MP Ruth Cadbury MP Tulip Siddiq MP Baroness Kramer Nigel Evans MP Richard Harrington MP Rt Hon Sir Vince Cable MP Philip Davies MP Lady Sylvia Hermon MP Catherine West MP Rt Hon Dame Caroline -

Arts Lottery Funding Recipient Constituencies Per Capita, 2015 & 2016 Combined

Arts Lottery funding recipient constituencies per capita, 2015 & 2016 combined Published 25 May 2017 Following on from The Stage article ‘Revealed: Which UK constituencies get the most – and least – Lottery cash for the arts’ below is the full list of Arts Lottery funding across 659 UK Parliamentary Constituencies per capita. DCMS publishes details of all lottery grant recipients on their website. If you combine all ‘Arts’ awards across the UK in 2015 and 2016 and then divide by the overall size of the electorate, the average per capita amount per constituent across the UK is £13.10, excluding the 1,928 grants worth £101 million that were not designated to a constituency (16% of the total amount of grants awarded). £ Total Arts Lottery £ Per UK Constituency MP Grants Capita 2014 & 2015 1 Leeds Central Hilary Benn (L) 46,596,403 569.65 2 Cities of London and Westminster Mark Field (C) 34,290,940 562.22 3 Birmingham, Ladywood Shabana Mahmood (L) 33,109,864 485.99 4 Cardiff South and Penarth Stephen Doughty (L Co-op) 25,727,041 338.49 5 Islington South and Finsbury Emily Thornberry (L) 14,673,010 215.38 6 Glasgow Central Alison Thewliss (SNP) 12,337,293 173.9 7 Hackney South and Shoreditch Meg Hillier (L Co-op) 10,926,061 128.59 8 Manchester Central Lucy Powell (L Co-op) 10,701,760 124.33 9 Vauxhall Kate Hoey (L) 10,020,186 121.85 10 Bristol West Thangam Debbonaire (L) 10,427,938 114.3 11 Edinburgh East Tommy Sheppard (SNP) 7,375,694 109.85 12 Poole Robert Syms (C) 7,904,345 108.94 13 Bermondsey and Old Southwark Neil Coyle (L) 8,514,689 -

Invest, Don't Cut the Predicted Impact of Government Policy on Funding For

Invest, Don’t Cut The predicted impact of Government policy on funding for schools and academies by 2020 A report by NUT and ATL This report presents findings from an NUT / ATL interactive website which demonstrates the likely impact on schools and academies of the Government’s current school funding policies and its plan to redistribute existing funding between schools in England - www.schoolcuts.org.uk The interactive website allows users to access detailed predictions for every school’s funding per pupil in real terms, as affected by the Government’s proposal to implement a new funding formula for schools alongside a freeze in funding per pupil and cost increases imposed by Government. The predictions are based on publicly available government data and the most robustly constructed proposed funding formula for schools currently available. With schools already struggling to cope, the Government plans what the Institute for Fiscal Studies has described as the largest real terms cut in school funding in a generation. We know that children are already suffering – class sizes are rising, curriculum choices are being cut, pupils with special educational needs and disabilities are losing vital support and school staff are losing their jobs. Instead of investing more money in education to address the funding shortages already hitting schools and academies, the Government plans only to move existing money around the country through a new funding formula. For every school which gains from this, others will lose – and almost every school will lose when the impact of inflation and other cost increases, against which the funding freeze offers no protection, are also taken into account. -

THE UNIVERSITY of HULL Do Committees Make A

THE UNIVERSITY OF HULL Do Committees Make a Difference? An Examination of the Viscosity of Legislative Committees in the British House of Commons being a Thesis submitted for the Degree of Doctor of Philosophy in the University of Hull by Louise Thompson, BA (Hons), MA May 2013 Acknowledgements The submission of this thesis brings my time as a student in the Department of Politics and International Studies to an end. The ten years I have spent as a student here have been the very happiest and the most enjoyable. There was only ever one university at which I wanted to study, hence why I stayed so long. I have always found the department and its staff to be extremely warm, welcoming and supportive. I will always look back on these years in the department with much affection and will be incredibly sad to leave. Whilst I owe a debt of gratitude to all of the academic and administrative staff for making my time here so memorable; very special thanks must go to two people in particular. Firstly, to Professor the Lord Norton of Louth. From my very first day as an undergraduate student, through my undergraduate dissertation, a Master’s degree and now the submission of this thesis he has acted as my academic supervisor. I therefore thank him for a decade of advice and guidance. His supervision and counsel in preparing this thesis has been invaluable and has kept me on the right path whenever I have started to wander. Secondly to Dr Cristina Leston-Bandeira; my supervisor, mentor and friend, for her never ending supply of advice and words of wisdom.