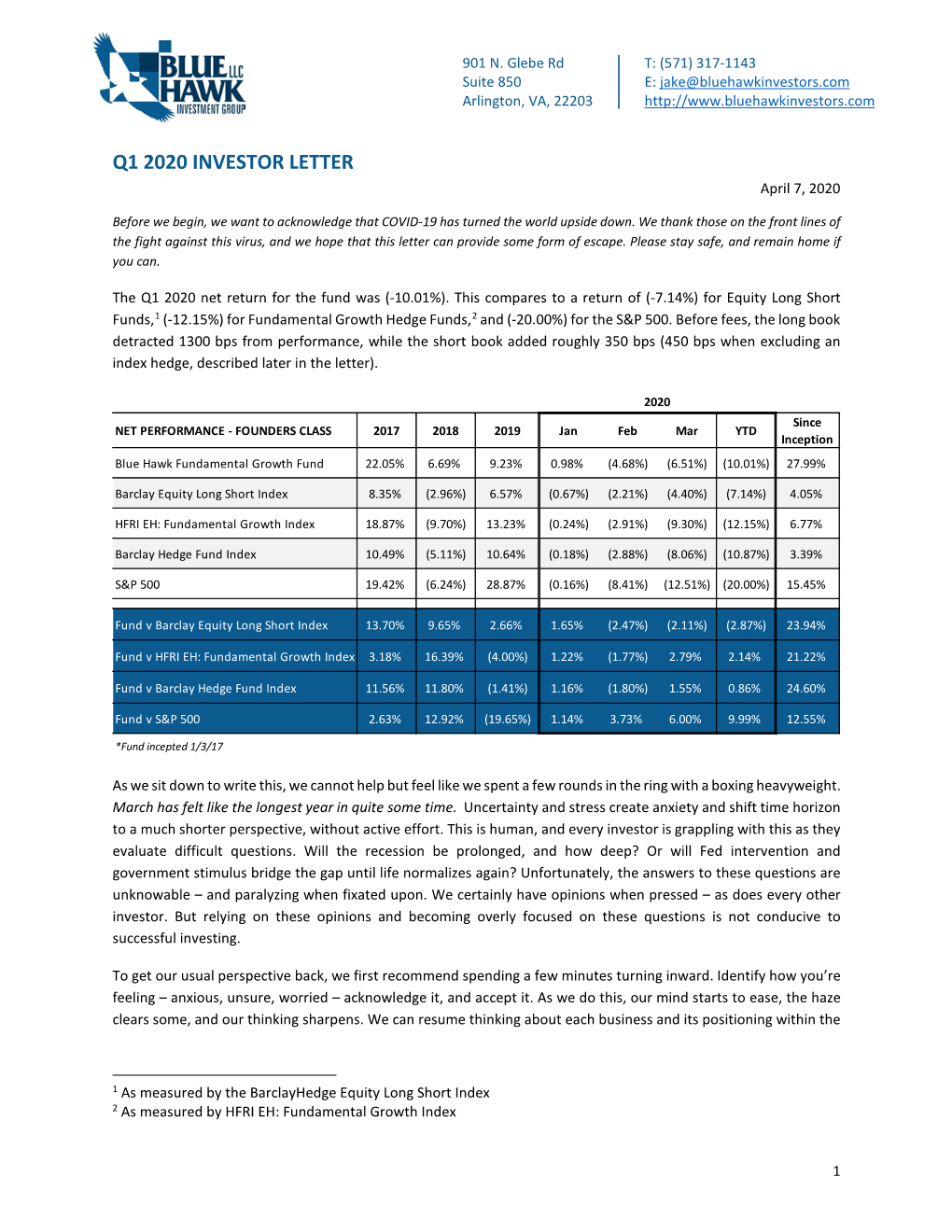

Q1 2020 INVESTOR LETTER April 7, 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

288666055.Pdf

The Official ‘Love is Blind’ Interactive eBook eBook Written by Limus Woods All Rights Reserved © 2016 Table of Contents Section One Episode I: The Setup The Character Crill Gates Haitian Water Episode II: Arrangements Why The Character Robert Should Stay Off Facebook Real Pakistani Culture in Brooklyn Fatimah Being Forced into a Planned Marriage Love is Blind Character Rivalries: Meeka vs Linda The Dirty Pimp Casper Episode III: The Proposal The Reality of Cocaine in American Life Love is Blind Character Rivalries: Rodney vs Crill Gates Section Two Episode IV: The Shake When Arguing Helps Fatimah’s Perverted Uncle Episode V: The Harassment Racial Profiling on Love is Blind Love is Blind Character Rivalries: Anna vs Mary Episode VI: Mr. Walker Another Side of Mr. Walker G Money Has a Girlfriend Love is Blind Character Rivalries: Mercy vs G Section Three Episode VII: Foot is Still At It Foot & Flossy…Always Sippin! Episode VIII: The Closet Monster Love is Blind Character Rivalries: Robert vs Rodney Will Robert Lose His Virginity? Is Sexual Immorality Worse than Emotional? Episode IX: G Money’s Luck May Have Just Ran Out The Beautiful Tai Chi Boxing Scene Love is Blind Character Rivalries: Ralphie vs Adolf Section One Episode One: The Setup It seems that when there is money involved, there is a sense of being able to coexist among the characters, at least in the first scene of Love is Blind (2015), the new series from Flo X Films on You Tube at . But, the true colors of people always eventually shine through, like for example when the Mr. -

A Love Knowing Nothing: Zen Meets Kierkegaard

Journal of Buddhist Ethics ISSN 1076-9005 http://blogs.dickinson.edu/buddhistethics/ Volume 22, 2015 A Love Knowing Nothing: Zen Meets Kierkegaard Mary Jeanne Larrabee DePaul University Copyright Notice: Digital copies of this work may be made and distributed provided no change is made and no alteration is made to the content. Reproduction in any other format, with the exception of a single copy for private study, requires the written permission of the author. All en- quiries to: [email protected]. A Love Knowing Nothing: Zen Meets Kierkegaard Mary Jeanne Larrabee 1 Abstract I present a case for a love that has a wisdom knowing nothing. How this nothing functions underlies what Kier- kegaard urges in Works of Love and how Zen compassion moves us to action. In each there is an ethical call to love in action. I investigate how Kierkegaard’s “religiousness B” is a “second immediacy” in relation to God, one spring- ing from a nothing between human and God. This imme- diacy clarifies what Kierkegaard takes to be the Christian call to love. I draw a parallel between Kierkegaard’s im- mediacy and the expression of immediacy within a Zen- influenced life, particularly the way in which it calls the Zen practitioner to act toward the specific needs of the person standing before one. In my understanding of both Kierkegaard and Zen life, there is also an ethics of re- sponse to the circumstances that put the person in need, such as entrenched poverty or other injustices. 1 Department of Philosophy, DePaul University. Email: [email protected]. -

MIAMI UNIVERSITY the Graduate School

MIAMI UNIVERSITY The Graduate School Certificate for Approving the Dissertation We hereby approve the Dissertation of Daniel J. Ciamarra Candidate for the Degree Doctor of Philosophy ______________________________ Director (Tom S. Poetter) ______________________________ Reader (Richard A. Quantz) ______________________________ Reader (Denise Baszile) _____________________________ Graduate School Representative (Bob Burke) ABSTRACT SPEAKING UP: USING A PEDAGOGY OF LOVE TO DEBUNK TECHNICAL TEACHING AND LEARNING PRACTICES by Daniel J. Ciamarra At present, our students are valued for their capacities to thoughtlessly absorb and regurgitate standardized facts and figures. Meanwhile, the affective facets of schooling, such as love, relationality, compassion, acceptance, integrity, and altruism are overlooked by politicians and educational decision makers, who claim these elements lack academic rigor. In this study, I use the dominant views of the educational elect to accentuate the current push for a more standardized, accountable, and scientific approach to schooling. Then, I employ the counternarrative as a methodological tool for talking back, offering up personal stories and experiences that frame the power of agapic love to demystify the normative views of schooling. More specifically, I employ personal narrative as means for providing teachers a voice, one which aims to debunk confounding generalizations or refute common claims about what education is or ought to be. Finally, I analyze the divergent stories through multiple theoretic and practical lenses in order to make meaning of my experiences. Moreover, the counternarratives in this study focus on how agapic love can be utilized in pedagogical and curricular efforts to transcend the present conditions that hinder many students and teachers from being and becoming who they really are. -

Love Is Blind: Books on Relationships Between Persons with Vision Loss and the Sighted

Love is Blind: Books on Relationships Between Persons with Vision Loss and the Sighted Beyond the Bear: How I Learned to Live and Love Again After Being Blinded by a Bear – DB 76560 Author: Dan Bigley Narrator: Jeff Allin Length: 9 hours, 28 minutes Author recounts being blinded during a near-fatal grizzly bear attack in Alaska in 2003 at age twenty-five. Details his recovery and his attendance at a center for the visually impaired. Discusses earning a master degree, changing careers, and reuniting with--and marrying--his girlfriend. Beyond the Blindness: My Story of Losing Sight and Living Life – DBC 12204 & BR 22492 Author: Ted Hinson Narrator: not listed Length: 3 hours, 45 minutes As a young parent, Ted Hinson was on top of everything. He was an active father, basketball coach, and worked in the oil and gas industry. And he accomplished all of this while completely blind. In this book he has an important message for anyone coping with adversity: strive to change obstacles into opportunities, and don't let challenges limit your life. Blind Ambition: One Woman's Journey to Greatness Despite Her Blindness – DBC 1886 Author: Ever Lee Hairston Narrator: Paul Georgiou Length: 6 hours, 28 minutes Growing up, Ever Lee Hairston didn’t tell anyone she was losing her sight. Through two troubled marriages and much turmoil, she emerged as a woman with a powerful, inspirational story of ambition and helping others overcome obstacles to realize the purpose of their lives. Blind Curve – DB 59915 & BR 15929 Author: Annie Solomon Narrator: Michele Schaeffer Length: 9 hours, 29 minutes Detective Danny Sinofsky loses his sight in an undercover operation. -

FILE 1 – Body Shaming Document 2 Document 3 - "Love Is Blind" Highlights Reality TV's Fatphobia Problem Teen Vogue, March 5, 2020, by Mathew Rodriguez

FILE 1 – Body shaming Document 2 Document 3 - "Love Is Blind" Highlights Reality TV's Fatphobia Problem Teen Vogue, March 5, 2020, by Mathew Rodriguez Not having any plus-size people as part of the experiment undercuts any thesis the show purports to test. In this op-ed, writer Mathew Rodriguez unpacks how Netflix’s dating reality show "Love Is Blind" purports to test whether sparks can fly between people who have never seen each other before — yet doesn’t include fat people. Within the first few minutes of Love Is Blind on Netflix, host Vanessa Lachey, standing next to her husband, 98 Degrees frontman Nick Lachey, delivers the show’s premise. She says to the participating women, “Everyone wants to be loved for who they are. Not for their looks, their race, their background or their income.” To counteract the world of Tinder, Grindr, and other dating apps, which give users the chance to reject or accept a person based solely on a photo, Blind challenges people to fall in love without ever having seen their potential partners. Couples will date and forge connections in furnished pods from opposite sides of a wall. The show does make good on at least three of those promises: It does have couples that are from different economic backgrounds, different upbringings, and across races. But, for all the differences the show derives drama from, it leaves one notable exception to its experiment: weight. Love Is Blind features all average-bodied people. And while it does want to test how people find love regardless of race and class, it never even nods to people’s size. -

MILWAUKEE PUBLIC LIBRARY Rshakespeare

MILWAUKEE PUBLIC LIBRARY EADE Events Books Services RApril 2016 Vol. 74 No. 4 R Shakespeare 400 Searching for “Shakespeare 400” on the web this month will result in a plethora of events, programs, books, and even ideas in London and around the world on how to celebrate the 400th anniversary of William Shakespeare’s death in 1616. But if you can’t make that “leap over the pond,” you can celebrate at the Milwaukee Public Library with Optimist Theatre’s To Be! Shakespeare Here and Now presentation in the Richard E. and Lucile Krug Rare Books Room of the Central Library on Saturday, April 23 at 2 p.m. The show is a one-person interac- tive presentation, featuring actor Ron Fry as William Shakespeare. Dynamic inter- pretations of excerpts from some of Shakespeare’s most famous works combine with a humorous look at life in Renaissance England with plenty of opportunities You could be quoting for audience members to star alongside The Bard. Shakespeare without knowing it! The newly renovated Tippecanoe Branch offers Powerful Rhyme: The Art of “As good luck would have it” William Shakespeare on Tuesday, April 12 from noon to 7:30 p.m. A day full The Merry Wives of Windsor of entertainment will include a sonnet slam, Hidden Treasures of the Library: Rarities of Shakespeare presentation (2-4 p.m.), performances, discussion, music “Be-all and the end-all” and more. Macbeth Milwaukee Public Library has a large number of Shakespeare-related rari- “Break the ice” The Taming of ties including The Works of Mr. -

The Canterbury Tales

The Canterbury Tales The Merchant, his Prologue and his Tale 1 The Merchant is apparently a prosperous exporter who likes to TALK of his prosperity; he is concerned about pirates and profits, he is skillful in managing exchange rates, but tightlipped about business details. The portrait of the Merchant from the General Prologue A MERCHANT was there with a fork•d beard, In motley,1 and high on horse he sat, Upon his head a Flandrish beaver hat, from Flanders His boots clasp•d fair and fetisly. neatly His reasons he spoke full solémpn•ly, solemnly 275 Sounding always the increase of his winning. profits He would the sea were kept for anything 2 He wished Betwixt Middleburgh and Or•well. Well could he in Exchang• shield•s sell.3 sell currency This worthy man full well his wit beset — used his brains 280 There wist• no wight that he was in debt, no person knew So stately was he of his governance astute in management With his bargains and with his chevissance. money dealings Forsooth he was a worthy man withal, Truly / indeed But sooth to say, I n'ot how men him call. truth / I don't know 1 271: "(dressed in) motley": probably not the loud mixed colors of the jester, but possibly tweed. 2 276-7: "He wished above all that the stretch of sea between Middleburgh (in Flanders) and Orwell (in England) were guarded (kept) against pirates." 3 278: He knew the intricacies of foreign exchange. Scholars have charged the Merchant with gold smuggling or even coin clipping; but, although "shields" were units of money, they were neither gold nor coins. -

House Md S06 Swesub

House md s06 swesub House M.D.. Season 8 | Season 7 | Season 6 | Season 5 | Season 4 | Season 3 | Season 2 | Season 1. #, Episode, Amount, Subtitles. 6x21, Help Me, 11, en · es. Greek subtitles for House M.D. Season 6 [S06] - The series follows the life of anti-social, pain killer addict, witty and arrogant medical docto. Hugh Laurie plays the title role in this unusual new detective series. Gregory House is an introvert, antisocial doctor any time avoid having any contact with their. House M.D. - 6x12 - Moving the Chainsp English. · House M.D. - 6x20 - English. · House M.D. House returns home to Princeton where he continues to focus on hi Sep 28, Harsh Lighting. Episode 3: The Tyrant. When a. Home >House M.D.. Share this video: House treats a patient on death row while Dr. Cameron avoids Sep 13, 44 Season 6 Show All Episodes. 20 House returns home to House M.D. Season 08 ﻣﺴﺤﻮﺑﺔ ﻣﻦ اﻟﻨﺖ" ,Princeton where he continues to focus Sep Arabic · House, M.D. Season 6 (p x Joy), 6 months ago, 1, B COMPLETE p BluRay x MB Pahe. House m d s06 swesub. No-registration upload files up MB claims there victim dying, but not from accident. House m d s06 swesub. Amd radeon hd g драйвер. House M.D. - Season 6: In this season, House finds himself in an And when House returns more obstinate. «House, M.D.» – Season 6, Episode 13 watch in HD quality with subtitles in different languages for free and without registration! «House, M.D.» – Season 6, Episode 2 watch in HD quality with subtitles in different languages for free and without registration! -Sabelma Romanian Subtitle. -

A New Hip Hop Musical Featuring Jack & Annie

A NEW HIP HOP MUSICAL FEATURING JACK & ANNIE JANUARY 12-14, 2020 THE MAGIC TREE HOUSE BOOKS Mary Pope Osborne is an American author of children’s books. She is best known as the author of the Magic Tree House series, which includes over 50 titles and has sold more than 134 million copies worldwide. In every book in the series, the Magic Tree House whisks siblings, Jack and Annie, on new adventures in different time periods and different places all over the world! The show you experienced today, is adapted from Magic Tree House #25: Stage Fright on a Summer Night. The show you saw today was created by NJPAC (New Jersey Performing Arts Center) from Newark, New Jersey. Learn more about them at njpac.org. DISCUSSION QUESTIONS Talk with your class or family after the show: How do Annie and Jack feel when they first arrive in London in the 1600s? How would you feel if you were suddenly transported to Shakespeare’s time? You saw a portrayal of William Shakespeare on stage today. Did the actor portray Shakespeare the way you envisioned him? How was he similar? How was he different? Why do you think there was a law that prevented women from performing on stage during Shakespeare’s time? Do you think this was a just law? What do you want to know about Shakespeare that you haven’t learned today? Where can you find the answers to your questions? SHAKESPEARE’S WORDS SHAKESPEARE’S DRESS RHYMING VERSE William Shakespeare was a wordsmith, meaning he was a In Shakespeare’s day, the actors would wear popular clothing. -

Happy Birthday!

Resident Newsletter Garden Life April 2021 Happy Birthday! In This issue: Page Ed Rand 2-3 James Hale 03 Jim Pendleton 4 Bill Stewart * 06 Marketing 5 Jeanne Harrell* 08 From Legacy 6 Al Johnson * 11 Monthly Outings 7-8 Bob Rudisill 15 Special Events 9 Sue Ruehlen 15 10-12 Edna Duren 16 This & That Lillian Swan 17 Hooks and Needles 13 Harold McGuire 21 Gardening Outlook ‘21 14 Nancy Chambliss 22 Nifty Nineties* 15 Dick Crom* 23 Captured Moments 16 Roger Long 26 Dot Masters 26 Come visit our Facebook page, The Gardens of Taylor Glen-BRH Or visit our website www.taylorglencommunity.org Tom & Joyce Suggs April 3rd Page 1 Garden Life A Monkey of a Time Ed Rand Friday morning after his escape from The Charlotte Metro Zoo, Sydney, the chimpanzee on the loose, arrived in Mt. Sandy, up in Rowan County. He was incredibly hungry and no doubt was having some serious misgivings about his ad- venture when he caught a whiff of Amy Louise Watterson’s breakfast sitting on a table on her unscreened back porch. Amy Louise was in the house, only a few feet away, talking to her sister from Charlotte on the phone. Amy Louise remembered that her late husband, Cleaver, had once said she would rather talk than eat, and here she was proving him right again. Sydney, seeing his opportunity, swung up on the porch, lapped up a plate of scrambled eggs, bacon, and grits and was on his way just as he heard Amy Louise hang up the phone and head in his direction. -

Isolation / Quarantine Daily Plan General Tips

MICHIGAN TECHNOLOGICAL UNIVERSITY ISOLATION / QUARANTINE DAILY PLAN GENERAL TIPS So, you're in a 10-day isolation period after testing positive, or you're quarantining for 14 days after being exposed to someone with COVID-19, but you're feeling fine (or had some symptoms, but are ready for some action)... what do you do? Here are some tips and a 14-day schedule from the center for student mental health and well-being to keep yourself balanced, even when you're stuck at home. Pick and choose from our Be Well menu of daily activities to keep every day new and exciting. GENERAL TIPS Stick to a schedule. Attend your classes daily - even if they're recorded. Create a routine for completing your work, try scheduling things at specific times in Google Calendar or your planner. Utilize the resources available to you (we'll tell you all about them!). Connect with others virtually as much as you can. Alone time is something you might not have normally, try to focus on the positives and enjoy some time to yourself. 14 days may seem like a long time right now, but it will be over before you know it! If you're in quarantine, not isolation, remember, you can get outside for 2 hours a day to get some fresh air - just ask your REC or campus contact for guidelines! RESOURCES If you live on-campus, you should already have a professional staff member assigned to you. If you don't have one, contact [email protected]. If you live off-campus and need something, please contact [email protected]. -

MALVERN COLLISION Krohn 181 Lancaster Ave

Feast of the Baptism of the Lord St. Patrick Catholic Church 126 Woodland Avenue Malvern, PA 19355 www.stpatrickmalvern.org Contact Information Parish Staff Office: 610-647-2345 Fax: 610-647-4997 Rev. T. Christopher Redcay, Pastor School: 610-644-5797 Rev. James J. Ambrogi, Pastor Emeritus PREP: 610-296-8899 Music Ministry: 610-647-2348 Rev. Arul Amalraj, O. Praem, Parochial Vicar Rev. Kevin P. McCabe , Resident Liturgy Schedule Rev. Dennis O’Donnell, Sunday Assistant Daily 6:30AM & 9:00AM Deacon Lawrence Froio, Retired Permanent Deacon Saturday Vigil: 5:00PM Deacon Louis Libbi, Permanent Deacon Sunday: 7:30AM, 9:00AM, Deacon Matthew Windle , Transitional Deacon 10:30AM, 12 Noon Ms. Patricia O’Donnell, Principal Sister Eileen Tiernan, IHM , Director of Religious Education Reconciliation Mrs. Katey Engel, Liturgical Music Director Saturday: 3:30PM - 4:30PM Mr. Daniel Milani, Director of Adult Faith Formation Confessional is located behind the Church Sanctuary ST. PATRICK PARISH ! So faith, hope, love remain, these three; but the great- est of these is love. ! St. Valenne’s Day is just a few weeks away now. Do you find yourself spending me reading all the variety of cards in !"" the card shop because you have to find just the right one that carries just the right senment? The messages in these cards run from simple beauty to sappy and senmental as they eloquently describe what LOVE is. All throughout histo- ! ! ry, many poets, writers and musicians have aempted to ! " describe for us what “love is.” A favorite line of Shake- #$ # ! speare, o en quoted by many, is “love is blind.” The Beatles ! ! gave us “love is all you need.” For those who remember the ! %& 1970 movie Love Story we have the famous “love means ' " "& (&)* ! never having to say you’re sorry.” And we could go on and " ! ! on.