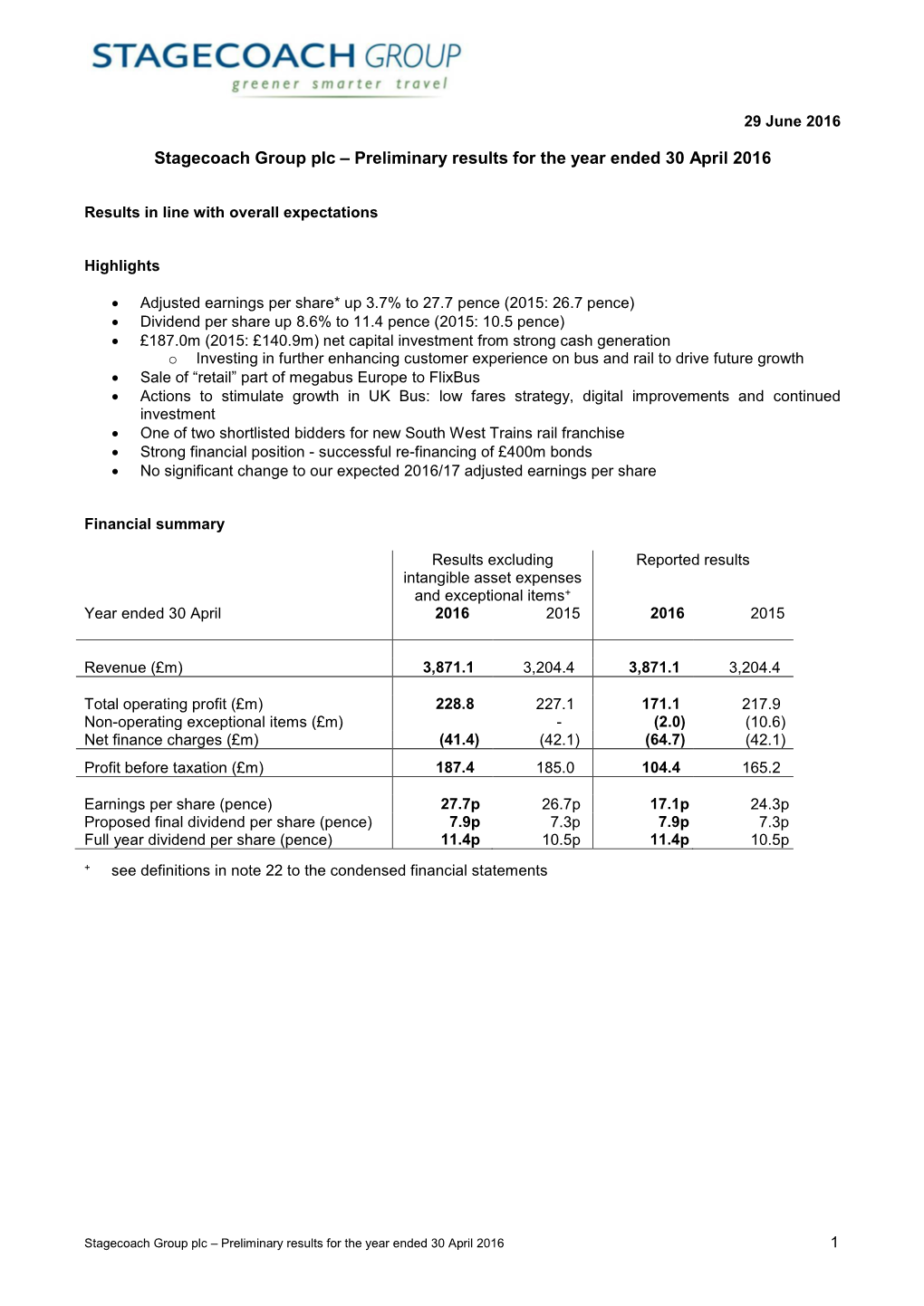

Preliminary Results for the Year Ended 30 April 2016

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Stagecoach Group Plc Response to the Joint Preliminary Consultation on Automated Vehicles

Stagecoach Group plc Response to the Joint Preliminary Consultation on Automated Vehicles Stagecoach Group plc (“Stagecoach Group”) welcomes the consultation by the Scottish and English Law Commissions on Automated Vehicles. Stagecoach Group is actively participating in trialling automated vehicles in both the depot and public transport environments, working with technology developers, vehicle manufacturers, academia and others. We welcome the consultation as another important initiative in this area. The consultation is wide – ranging in scope and some of the questions posed will be better able to be answered as more information and understanding of automated vehicles and their use in different scenarios emerges. Equally, we do not propose to respond to or comment on all questions but we offer views based on our experience to date as one of the UK’s biggest bus and coach operators, with some 8,000 buses and coaches operating in different environments across the UK. We look forward to future initiatives, particularly the planned consultation on automated vehicles in Mobility as a Service and the challenges of achieving “everything somewhere” later this year. Stagecoach Group: • Stagecoach is an international public transport group, with operations in the UK, the United States and Canada. • We are one of the UK's biggest bus and coach operators with over 8,000 buses and coaches on a network stretching from south-west England to the Highlands and Islands of Scotland. Our low-cost coach service, megabus.com, operates a network of inter-city services across the UK. • Stagecoach is a major UK rail operator, with an involvement in operating several franchised rail networks, including the East Midlands Trains network. -

Stagecoach Group out in Front for 10-Year Tram Contract Responsible for Operating Tram Services on the New Lines to Oldham, Rochdale, Droylsden and Chorlton

AquaBus New alliance Meet the Sightseeing ready to forged for megabus.com tours' bumper set sail rail bid A-Team launch The newspaper of Stagecoach Group Issue 66 Spring 07 By Steven Stewart tagecoach Group has been Sselected as the preferred bidder to operate and maintain the Manchester Metrolink tram Metrolink bid network. The announcement from Greater Manchester Passenger Transport Executive (GMPTE) will see Stagecoach Metrolink taking over the 37km system and the associated infrastructure. The contract will run for 10 years and is expected to begin within the next three months. right on track It will include managing a number of special projects sponsored by GMPTE to improve the trams and infrastructure to benefit passengers. Stagecoach Metrolink will also be Stagecoach Group out in front for 10-year tram contract responsible for operating tram services on the new lines to Oldham, Rochdale, Droylsden and Chorlton. Nearly 20 million passengers travel every year on the network, which generates an annual turnover of around £22million. ”We will build on our operational expertise to deliver a first-class service to passengers in Manchester.” Ian Dobbs Stagecoach already operates Supertram, a 29km tram system in Sheffield, incorpo- rating three routes in the city. Ian Dobbs, Chief Executive of Stagecoach Group’s Rail Division, said: “We are delighted to have been selected as preferred bidder to run Manchester’s Metrolink network, one of the UK’s premier light rail systems. “Stagecoach operates the tram system in Sheffield, where we are now carrying a record 13 million passengers a year, and we will build on our operational expertise to deliver a first-class service to passengers in Growing places: Plans are in place to tempt more people on to the tram in Manchester. -

MEDIA FACTSHEET Stagecoach Group Plc Is a Leading International Public Transport Group, with Extensive Operations in the UK

MEDIA FACTSHEET Stagecoach Group plc is a leading international public transport group, with extensive operations in the UK, United States and Canada. The company was founded by Sir Brian Souter and his sister, Ann Gloag, in Perth, Scotland, in 1980 and has been listed on the London Stock Exchange since 1993. The Group has a balanced portfolio of deregulated and contracted bus and rail businesses and a strong track-record of transport innovation. Stagecoach provides greener, smarter travel for millions of people every day, delivering vital links to employment, education, health facilities and leisure activities. Registered Office: 10 Dunkeld Road Perth PH1 5TW Scotland Registered Number: 100764 Ticker Symbol: SGC.L Our business: Stagecoach Group employs around 39,000 people in the UK and North America and runs around 13,000 buses, coaches, trains and trams. We provide greener, smarter and better value transport for around 3 million customers a day. ngers travel on Stagecoach's 8,500 buses every day on a network stretching from south-west England to the Highlands and Islands of Scotland. The company's business includes major city bus operations in London, Liverpool, Newcastle, Hull, Manchester, Oxford, Sheffield and Cambridge. networks. Stagecoach and Virgin have partnered to jointly run the East Coast and West Coast inter-city rail franchises. The Group is also a major tram operator, running a 28km system in Sheffield. -city services, tour and charter, and sightseeing operations, mainly through its Coach USA and Coach Canada brands. We operate in 40 US states and two Canadian Provinces -leading budget inter-city coach service megabus.com in around 150 locations in Europe, as well as more than 130 destinations in North America. -

Cold Calls, Cold Sweat

COLD CALLS, B y S imo n T A n , C hief E x ecutive O fficer , W est C hi n A COLD busi n ess U n it SWEAT 20 UP CLOSE WITH COMFORTDELGRO C OLD CA LL S, C OLD S W e AT Four time zones, seven countries and over 20,200 employees. ComfortDelGro is now one of the largest listed passenger land transport companies in the world with over S$1 billion invested outside of Singapore. But the road thus far has not been easy. A lot of hard work, sweat and even tears have gone into expanding the footprint in a business that is more often than not, politically sensitive and emotionally charged. Our Chief Executive Officer of West China Business Unit, Simon Tan, recalls how difficult it was to break into the Chengdu market and how true grit finally won the day. The Untold Stories 21 t was the day before I was to fly to Chengdu. I felt like a with little pockets of operations in various other coastal cities. lightweight boxer entering the ring for the first time, facing a We were not represented in any of the major provinces in the heavyweight veteran. I knew I was going to get pummelled. Southwestern and Central parts of China. I I asked: “What if I don’t deliver? What if nothing comes out I remember him saying: “The Government will have to drive of the trip?” The reply from our Managing Director/Group Chief some of the wealth created in the coastal belt inwards for society Executive Officer (MD/Group CEO), Kua Hong Pak, was resolute: as a whole.” Future economic policies, he predicted, would aim “Just go.” at moderating growth in the more developed coastal cities while That strengthened my resolve but did nothing to boost driving investments inwards towards the less developed cities my confidence. -

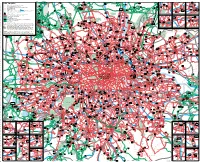

Key to Maps for Details in Central London See Overleaf

S 1 N B C 712.724 M S 2 O 9 Maldon Manor Station, The Manor Drive, Worcester Park, Dorchester Road, North Cheam, London Road, Windsor Avenue, H A C 242.C1.C2 M H 310.311 W1† 614 S 298 308.312 610 66.103.175 D 9 757 to D NE R R 2 E Cuffley 381 3 R E R A A 8 N LEY 4 1 A 5 .39 FF H U . 364 5.248 . A L N 12 A CU IL D 1 T A E P C1.C3.C4 6 621 N 615 A 3 A 380.880 L 191 W8 W10 247.294.296 O 8 - * Luton Airport E Cranborne Road . L T H 8 Stayton Road, Sutton, Cedar Road, Langley Park Road, Lind Road, Westmead Road, Carshalton, Carshalton Beeches, D R 2 9 O 1 R Breach Barns A R D Colney D * L T N 2 84 N C1 K B81 Y . O 2 648.N15 4 N S3 R 6 TI 242 I 8 E . E 0 84.302 A 365.375.575 S . A 797 D *T C T 2 S S C1 W9 O O L M B 298 B Industrial 3 RD C 382 9 . E N 7 6 G Y R . 8 CH 880 G * S S 1 T I U Street E . R R 242 211.212† 6 4 8 602 A U O R C Belmont, Royal Marsden Hospital, Sutton Hospital (Mon-Sat except evenings). Quality Line M O O O 4 398 H R 169 R T H S Shenleybury B 0 E 242 F . -

How We Support Britain's Economy and Communities

How we support Britain’s economy and communities stagecoach.com We carry We employ almost 24,000 people around 2.5 Welcome million customers a day Our transport services play a vital role in keeping Britain moving We operate 8,300 buses, coaches and trams For four decades, Stagecoach transport services have The new research carried out by Cebr has now also revealed transported billions of people, helped to build strong local the wider transport benefits associated with Stagecoach, which economies and provided a greener way to travel. As the demonstrate how we contribute towards making the nation more UK’s biggest bus and coach operator, our operations serve active, delivering cleaner air, reducing congestion on our roads communities in major cities including London, Manchester, and making our communities safer. Liverpool, Newcastle, Hull, Sheffield, Oxford and Cambridge * as well as inter-urban and rural locations, such as Cumbria Stagecoach internal data and Lincolnshire. We connect people with jobs, skills and training, bring customers to our high streets and draw families, friends For over 25 years Cebr has supplied We create vital and communities together, supporting the country’s independent economic forecasting and Jobs economic growth and reducing social deprivation. analysis to hundreds of private firms Our economic impact employment and public organisations. Cebr was This new report published by Stagecoach and the commissioned by Stagecoach Group Centre for Economics and Business Research (Cebr) to assess the economic and social contribution of its We pay our way …that’s analyses the significant impact that Stagecoach makes, not transport services to the UK economy. -

UK BUS Operating Review 2003

‘‘I’ve looked after travelling passengers for 10 years now and know that, above all, our customers value good communication. If services don’t run smoothly, they like to be kept informed. Keeping our passengers happy is crucial to our success.’’ Chris Pearce Standards Controller UK Bus Operating review 2003 UK BUS Outside London, total passenger volumes have increased by Stagecoach continues to be one of the leading UK bus operators, 0.4%. The trend in passenger volumes varies significantly by with a 16% share of a highly competitive market. Our UK Bus geographical area. We have initiatives in place to encourage business, the traditional core of the Group, remains a strong further growth and we have been particularly successful in source of cash flow. As one of the biggest bus operators in the increasing volumes in areas where congestion is causing some UK, we are at the cutting edge in developing new and innovative commuters to switch to using public transport. products and we are committed to playing a key part in Our major operation at Ferrytoll Park and Ride in Fife, Scotland, achieving the Government’s objectives of increased use of public which at peak times runs buses every five minutes into transport and greater integration. Edinburgh, has seen passenger volumes increase by 30% in the Turnover in our UK Bus division has increased by 5.4% to »598.4m past year. The Scottish Executive has approved additional (2002 ^ »567.9m). Operating profit was »67.0m,* compared to investment to double the size of the facility to 1,000 car parking »62.7m in the previous year, and this is after taking account of spaces. -

Rse Inquiry Into Facing up to Climate Change: Stagecoach Group Submission

RSE INQUIRY INTO FACING UP TO CLIMATE CHANGE: STAGECOACH GROUP SUBMISSION 1.0 Introduction 1.1 Stagecoach Group is a leading international public transport company with bus and rail operations in the UK and North America. The Group employs around 30,000 people and runs around 12,000 buses and trains. We operate more than 1,500 buses in Scotland, including the Highlands and Islands of Scotland, Aberdeenshire, Fife, Tayside, Ayrshire and West Scotland. Stagecoach is also the leading provider of inter-city coach travel in Scotland through Scottish Citylink and the budget inter-city coach service megabus.com. 1.2 We are pleased to have been invited to make a submission to the RSE’s inquiry on Facing up to Climate Change. The submission below addresses the following issues: • Transport and climate change • Risks and opportunities • Impact of the Climate Change (Scotland) Act • Transport priorities • Carbon reduction partnerships • Barriers to change • Regulation and incentives 2.0 Transport and climate change 2.1 We believe modal shift from car use to greener, smarter travel on buses and trains is central to tackling the challenge of climate change. While this may ultimately lead to increased carbon emissions from public transport, the overall benefit to society from dramatic reductions elsewhere will be enormous. Road transport accounts for around 22% of carbon emissions in the UK and it is are rising. Commuting and business travel, for example, accounts for nearly 40% of all miles driven by car in the UK. Government, local authorities, businesses, public transport operators and other stakeholders must work in partnership to encourage intelligent car use and create an environment in which it is easy for consumers to make the switch to more carbon efficient options. -

Capital Space Ltd Land South of Coldharbour Road, Gravesend

Capital Space Ltd Land South of Coldharbour Road, Gravesend Transport Assessment July 2016 Gravesham Borough Council Contents 1 INTRODUCTION .................................................................................................. 1 2 SITE AND LOCAL AREA ........................................................................................ 2 Site Location ....................................................................................................... 2 Local Road Network ............................................................................................ 2 Public Transport .................................................................................................. 3 3 POLICY ................................................................................................................ 4 National Planning Policy Framework .................................................................. 4 Supplementary Planning Guidance SPG 4 Kent Vehicle Parking Standards (July 2006) ................................................................................................................... 4 Gravesham Local Plan Core Strategy (September 2014) ................................... 5 4 BASELINE CONDITIONS ..................................................................................... 6 Existing Traffic Conditions .................................................................................. 6 5 PROPOSED DEVELOPMENT ................................................................................. 7 Overview -

On Stage, Stagecoach Group, Stagecoach South West Mark Whittle 01392 889747 Operating Companies

Going topless Reaching a in New new level York of control The newspaper of Stagecoach Group Issue 54 Spring 2004 Stagecoach joins Danes in bid for rail franchise tagecoach Group has linked up with Danish State SRailways (DSB) to bid for a major UK rail franchise. Carry on The Group has taken a 29.9% majority of passenger rail services in stake in South Eastern Railways Ltd, a Denmark and has further franchise company set up by DSB, to bid for operations in other Scandinavian the new Integrated Kent franchise in countries. logging on south-east England. It is an independent Public Three other companies – GNER, Corporation, owned by the Danish Carry on megabus.com! First Group and a consortium of Go- Government, and is managed by a That was the message Ahead and Keolis, of France – have Board of Directors and an Executive from bubbly actress been shortlisted for the seven to 10- Committee, who are responsible for Barbara Windsor when year franchise. the day-to-day business. she helped launch Integrated Kent, which will be let Executive Vice President and CFO Britain’s first low-cost from early 2005, of DSB, Søren internet bus service. will include routes Eriksen said: And, with tickets on the national rail ‘Both Stagecoach “Stagecoach has available from just £1 network throug- extensive through megabus.com, the hout Kent, parts of and DSB share a experience with initiative is catching the Sussex and South- train operations in public’s imagination for East London. It will commitment to the UK and DSB is catching a bus. -

On Stage Issue

The newsletter of Stagecoach Group Issue 110 | July 2015 STAGE ON page 2 page 6 INSIDE Memorial award | Greener together megabus.com continues European expansion megabus.com has revealed record advance ticket sales on its new network of domestic coach services in Italy as well as launching two new international routes. More than 30,000 customers purchased tickets during the first week of sales in Italy – higher than the initial sales on any of the company’s other networks in Europe. megabus.com services now link 13 destinations across Italy and passengers have been snapping up bargain fares from just €1 (plus 50 cents booking fee). The major new network of inter-city coach services covers Rome, Milan, Florence, Venice, Naples, Turin, Bologna, Verona, Padua, Siena, Genoa, Sarzana (La Spezia) and Pisa. megabus.com has also created around 100 new jobs through the opening of new bases near Milan megabus.com vehicles at the launch of the new Italian domestic network in Florence and in Florence. In addition, megabus.com recently launched its first base in France, where it has created 35 jobs between London and Milan via Lille, Paris, Lyon from customers has been fantastic. at a depot located near Lyon, from which a new and Turin. “The new routes between London and Milan, and international route now operates between megabus.com Managing Director Edward between Barcelona and Cologne are great news Barcelona, Perpignan, Montpellier, Avignon, Lyon, Hodgson said: “These latest routes mark even for our customers who now have access to even Mulhouse, Freiburg, Karlsruhe, Heidelberg, more expansion of our services in Europe. -

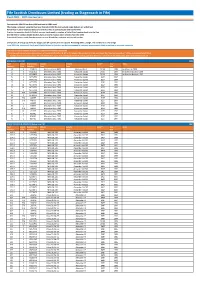

Historic Fleetlists.Xlsx

Fife Scottish Omnibuses Limited (trading as Stagecoach in Fife) Fleet 2001… 40th Anniversary Fleet strength 294 (25 less than 1996 and back to 1991 level) After being a constant since the fleet was formed in 1961 the last Leyland single deckers are withdrawn 30 low floor 'Loliner' branded buses are now in service at Cowdenbeath and Dunfermline A return to operating Scottish Citylink services has brought a number of toilet fitted coaches back into the fleet Over 50 former London double deckers have arrived to replace older vehicles from the 1970s Stagecoach Express coach fleet has grown to over 40 vehicles, including articulated coaches Livery notes; A new group livery for Stagecoach UK operations is introduced. Retaining white, orange, red and blue in a new design From 2000 Fife, Stagecoach Perth and Bluebird Buses in Aberdeen are being managed by common management albeit remaining as separate companies * LF next to a fleet number indicates it is low floor/wheelchair accessible ** Seating code shows a bus, dual purpose or coach (starts with a B, DP or C) followed by number of seats and then F (for front entranced) a 't' at the end means toilet fitted *** Double decker seating is shown 'H' followed by the upper deck seating/lower deck seating and then the door code (F for front entranced). Open top vehicles start 'O' MINIBUSES (Total 20) 2001 Fleet Depot Registration Chassis Vehicle Seats** Year Notes Number* Alloc Number Type Type New 16 K F234NLS Mercedes Benz 609D Mercedes Benz DP18F 1988 ex Alisons in 2000 17 K M317RSO Mercedes Benz