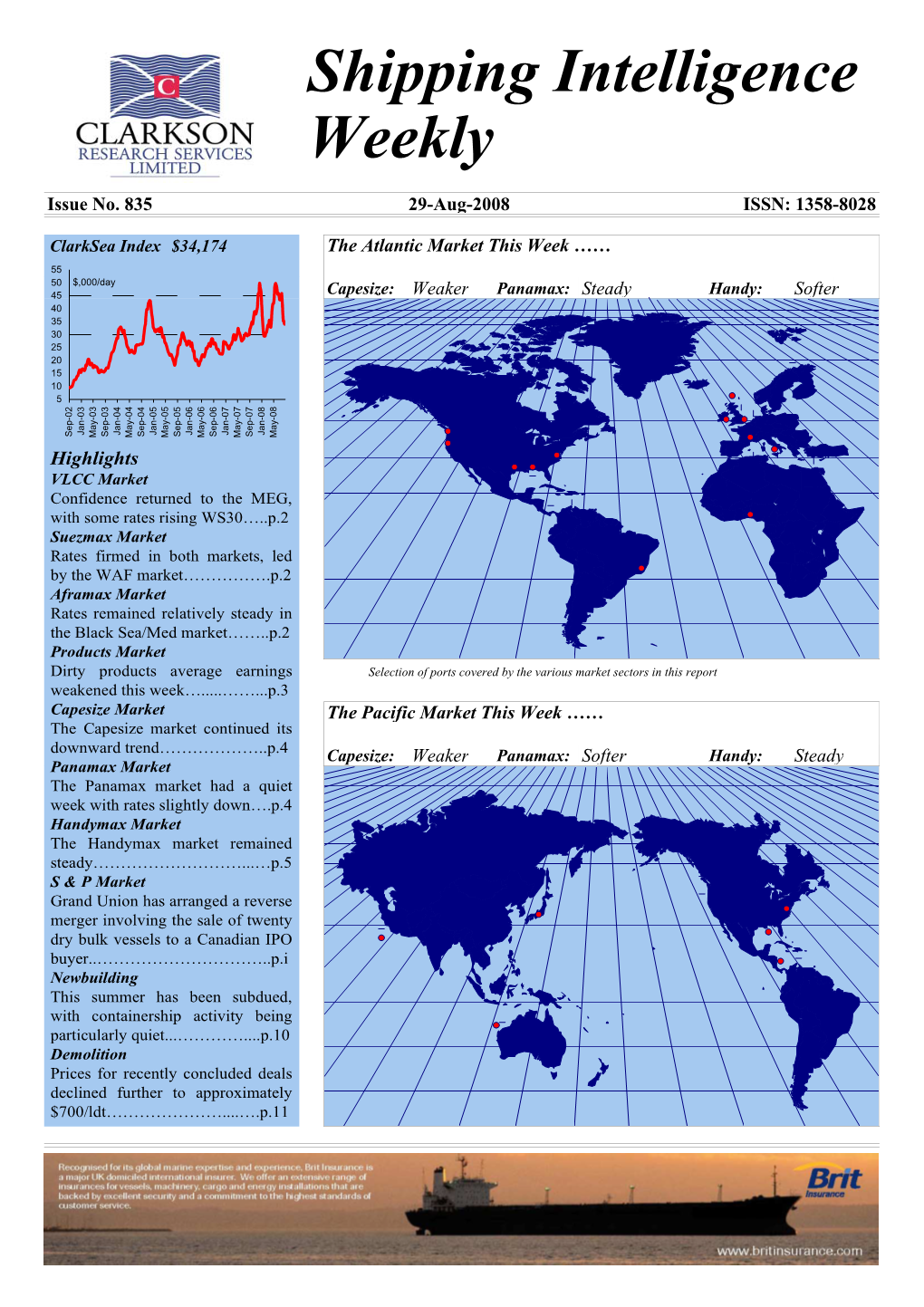

Shipping Intelligence Weekly

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

BILL ANALYSIS and FISCAL IMPACT STATEMENT (This Document Is Based on the Provisions Contained in the Legislation As of the Latest Date Listed Below.)

The Florida Senate BILL ANALYSIS AND FISCAL IMPACT STATEMENT (This document is based on the provisions contained in the legislation as of the latest date listed below.) Prepared By: The Professional Staff of the Environmental Preservation and Conservation Committee BILL: CS/SB’s 1094 & 326 INTRODUCER: Environmental Preservation and Conservation Committee and Senators Haridopolis and Constantine SUBJECT: Regulation of releases from gambling vessels DATE: March 25, 2008 REVISED: ANALYST STAFF DIRECTOR REFERENCE ACTION 1. Branning Kiger EP Fav/Combined CS 2. MS 3. RI 4. GA 5. 6. Please see Section VIII. for Additional Information: A. COMMITTEE SUBSTITUTE..... X Statement of Substantial Changes B. AMENDMENTS........................ Technical amendments were recommended Amendments were recommended Significant amendments were recommended I. Summary: The committee substitute creates the “Clean Ocean Act”. Provides definitions. Requires the owner or operator of a gambling vessel to register with the DEP. The registration shall be executed under oath and transmitted electronically. Requires each waterfront-landing facility that is registered as a gambling vessel’s berth to establish procedures for the release of waste from gambling vessels at the facility; make available a waste-management service; and collect a fee for the costs associated with making a waste-management service available for gambling vessels. Specifies that the DEP shall consider certain information when estimating a facility’s minimum waste-service demand. Requires a gambling vessel to report releases immediately. Provides penalties for violations of the act. Requires the DEP to establish and collect fees to cover the costs associated with administering the Clean Ocean Act. Provides that certain releases are exempt from the act’s provisions. -

Palm Beach and West Palm Beach Attractions

09_595369_ch05.qxd 10/24/05 12:11 PM Page 285 PART FIVE PALM BEACH COUNTY WELCOME to PALM BEACH TRUMP AND THE BREAKERS, TRUMPETS AT the Philharmonic, and breaking the bank are people and things associated with mostly rar- efied, sometimes vilified, but always fascinating Palm Beach. Palm Beach County is larger than Delaware, but most visitors are aware only of the opulent “Gold Coast,” from Palm Beach to Boca Raton. But there are 37 other municipalities and unincorporated areas, and the county includes 47 miles of beaches on the east, and Lake Okeechobee and the Everglades on the west. Delray Beach, between Boca and Palm Beach, has become a lively, desirable place to play and live. West Palm Beach is becoming a shop- ping and entertainment destination in itself, far less stuffy than its rich neighbor across Lake Worth. And west of the coast, past the suburban communities, are citrus groves, ranches, and wildlife refuges. A BRIEF HISTORY THE COUNTY’S EARLIEST KNOWN RESIDENTS were Native Ameri- cans, but the region was claimed for Spain in 1513. The nascent United States purchased the territory of Florida three centuries later. The Seminole Indian tribe’s famous resistance to forced relocation promptedCOPYRIGHTED three wars. The third, fought MATERIAL between 1835 and 1842, ended Indian control of the area. The county’s oldest nonnative set- tlement, Jupiter, was founded as a wartime fort in 1836. The Jupiter Lighthouse began operating in 1860 and continues to the present. In the 1890s, visionary Henry Flagler, a founding partner of Stan- dard Oil, built the Florida East Coast Railway system from Jacksonville to Key West to open the state as a winter paradise. -

Nieuwsbrief 165 8 Mei 2010

Nieuwsbrief 165 8 mei 2010 ALDABI 7600823 (NB-164), 12-2-1977 te water gelaten, 5-1977 opgeleverd door Van der Giessen-De Noord B.V., Krimpen a/d IJssel (909) als ALDABI aan Van Nievelt, Goudriaan & Co. B.V., Rotterdam, 1987 verkocht aan Victoria Line Shipping S.A., Panama, herdoopt LAMDA, 1988 verkocht aan Hartmann Schiffahrts G.m.b.H., Cyprus, herdoopt EASTERN MERCHANT, 1989 verkocht aan Tweendeck II K/S, Noorwegen, herdoopt NORTWEEN MERCHANT, 1990 herdoopt NORTHERN MERCHANT, 1992 verkocht aan Afrimar Shipping Ltd., Bahamas, herdoopt SECIL NAMIBIA, 1998 verkocht aan Namibia Shipping Ltd., Bahamas, herdoopt NAMIBIA, 10-2003 in beheer bij Clipper Project Ship Management, 8-12-2006 in beheer bij Nordane Shipping A/S, Svendborg, 2010 verkocht voor sloop naar India, 2010 herdoopt AMI, 24-2-2010 vertrokken van Durban naar India, 27-3-2010 gearriveerd te Alang om gesloopt te worden. ALIOTH 8511445 (NB-164), 27-6-1985 besteld, 25-2-1986 kiel gelegd, 13-12-1986 gedoopt ALIOTH door mevr. J.A. Groeneveld-Volgers en te water gelaten, 3-2-1987 vertrokken van Heusden, 4-2-1987 gearriveerd bij Scheepswerf Niehuis & v.d. Berg B.V., Pernis voor afbouw, 5/6-3-1987 proefvaart op de Noordzee, 19-3-1987 opgeleverd door Verolme Scheepswerf Heusden B.V., Heusden (1001) aan Netcon Alioth B.V., Rotterdam (Netcon B.V.) beheer: Joon Shipping & Trading B.V., technisch beheer en bemanning: Van Nievelt, Goudriaan & Co. B.V., Rotterdam, 20- 3-1987 vertrokken op de 1e reis naar Hamburg, 12-4-1987 herdoopt KHYBER, 16-11-1987 herdoopt ALIOTH, 2- 1990 herdoopt INDEPENDENT ACCORD, in beheer bij Wijsmuller Ship Management B.V., 31-8-1990 Van Nievelt, Goudriaan & Co. -

From 1940 to 2011

A Cumulative Index for and From 1940 to 2011 © 2010 Steamship Historical Society of America 2 This is a publication of THE STEAMSHIP HISTORICAL SOCIETY OF AMERICA, INC. 1029 Waterman Avenue, East Providence, RI 02914 This project has been compiled, designed and typed by Jillian Fulda, and funded by Brent and Relly Dibner Charitable Trust. 2010 TABLE OF CONTENTS Part Subject Page I Listing of whole numbers of issues, 3 with publication date of each II Feature Articles 6 III Authors of Feature Articles 42 IV Illustrations of Vessels 62 V Portraits 150 VI Other Illustrations (including cartoons) 153 VII Maps and Charts 173 VIII Fleet Lists 176 IX Regional News and Departments 178 X Reviews of Books and Other Publications 181 XI Obituaries 214 XII SSHSA Presidents 216 XIII Editors-in-Chief 216 (Please note that Steamboat Bill becomes PowerShips starting with issue #273.) 3 PART I -- WHOLE NUMBERS AND DATES (Under volume heading will follow issue number and date of publication.) VOLUME I 33 March 1950 63 September 1957 34 June 1950 64 December 1957 1 April 1940 35 September 1950 2 August 1940 36 December 1950 VOLUME XV 3 December 1940 4 April 1941 VOLUME VIII 65 March 1958 5 August 1941 66 June 1958 6 December 1941 37 March 1951 67 September 1958 7 April 1942 38 June 1951 68 December 1958 8 August 1942 39 September 1951 9 December 1942 40 December 1951 VOLUME XVI VOLUME II VOLUME IX 69 Spring 1959 70 Summer 1959 10 June 1943 41 March 1952 71 Fall 1959 11 August 1943 42 June 1952 72 Winter 1959 12 December 1943 43 September 1952 13 April 1944 -

Characterization of Pathogenic and Non-Pathogenic Vibrio

AN ABSTRACT OF THE THESIS OF Jingyi Du for the degree of Master of Science in Food Science and Technology presented on August 31, 2017. Title: Characterization of Pathogenic and Non-pathogenic Vibrio parahaemolyticus Strains and the Antimicrobial Activity of Fruit Juice and Fruit Extracts against Seafood Pathogens Abstract approved: ______________________________________________________ Christina Ann Mireles DeWitt Vibrio parahaemolyticus is frequently isolated or detected from raw seafoods, especially shellfish. Also, Listeria monocytogenes, Salmonella spp. are pathogens that are frequently found in ready-to-eat (RTE) seafood, such as smoked fish and shellfish, seafood salad, cooked shrimp and crabmeat, and seafood consumed raw. Two studies to improve safety in RTE seafoods were conducted. FDA’s regulatory limit, 10,000 cells/g, for V. parahaemolyticus in RTE fish products encompasses both pathogenic and non-pathogenic V. parahaemolyticus. However, limited studies exist on the factors that influence growth and die-off rate of pathogenic and non-pathogenic V. parahaemolyticus strains. This study investigated the influence of temperature (5-30 °C) on the growth (positive µmax) and die-off rates (negative µmax) of pathogenic and non-pathogenic V. parahaemolyticus strains. There was a significant effect of strain type (non-pathogenic vs pathogenic, P < 0.001), temperature (P < 0.001) and a strain type x temperature interaction (P = 0.026). At 5 °C, µmax was negative for both strain types indicating die-off. At 10 °C, µmax was negative for two pathogenic and one non-pathogenic strain. From 15-30 °C, µmax was positive for all strains. When evaluating differences between strain type at each temperature, significant difference (P < 0.001) between strain type only occurred at 30 °C. -

Daily Collection of Maritime Press Clippings 2008 –213

DAILY COLLECTION OF MARITIME PRESS CLIPPINGS 2008 –213 Number 213 *** COLLECTION OF MARITIME PRESS CLIPPINGS *** Sunday 17-08-2008 News reports received from readers and Internet News articles taken from various news sites. The ASM ALPHA is the former SMIT-LLOYD 106, built during 1973 at the Bodewes shipyard in The Netherlands under yard number 710, sailed for Smit-Lloyd and later for Smit Singapore as the “106” and was sold in 2002 to Auo Siam Marine and renamed ASM ALPHA Photo top : Capt. Jelle de Vries © Photo Left : Piet Sinke © Distribution : daily 4675 copies worldwide Page 1 8/16/2008 DAILY COLLECTION OF MARITIME PRESS CLIPPINGS 2008 –213 IF YOU HAVE PICTURES OR OTHER SHIPPING RELATED INFORMATION FOR THE NEWS CLIPPINGS ?? PLEASE SEND THIS TO : [email protected] CONTENTS EVENTS, INCIDENTS & OPERATIONS • US: No plan for naval blockade of Iran • Salvage of sunken ship starts off Antique town • Svitzer Salvage appointed to recover overboard logs • Somali pirates hijack Thai cargo ship • Ten perlemoen boats seized over poaching allegations • The South Korean Vessel Returned Today • Somalia - Puntland police reportedly arrest wounded pirate • Weer meer schepen uitgevlagd uit Duitsland • Horizon Lines Completes Marine Fire Exercise in Guam • Thor crew ‘safe’ CASUALTY REPORTING • VERONICA B. hits pier in Gibraltar Bay. NAVY NEWS • New boats for SERCO-DENHOLM • Royal Navy scraps Russia exercise plan • PAPALOAPAN arrived in Amsterdam for port visit • U.S.-Russia Naval Exercise May Be Cancelled • U.S. Navy Ship Makes Iraq Port Visit • Russian ship barred from NATO anti-terror patrol • Group wants to sink plan to scrap the NR-1 SHIPYARD NEWS • Halter lays keel for Navy missile-monitoring ship • Crane leg collapses in Mass. -

A Summer of Mission

OFFICIAL PUBLICATION OF THE DIOCESE OF SOUTHEAST FLORIDA www.diosef.org Volume 41 No. 4 August 2010 AA Summer Summer of of Mission Mission Success Story ummer is traditionally the season for “mission trips” — opportunities for members of our con- gregations to travel to another part of the world (or the country, or the diocese) to join in min- istry with friends old and new. Much of the Snews of our diocese is always directly concerned with mission; but this issue focuses on our outreach in our communities and around the world with an expanded “Committed to Mission” section offering stories not only about summer mission projects, but also about several ongoing outreach ministries. Paint Crew Photo by Heidi Shott ERD President Rob Radtke (left) and Canon Richard Miller listen as Simon, a NetsforLife volunteer for the village of Asapaligo, translates for Vita, a mother of five, whose family has not suffered from malaria for four years since they've faithfully used long-lasting insecticide nets. Members of a youth mission team from Good Shepherd, Tequesta, and St. Gregory’s, Boca Raton begin to paint the outside of the buidlings at Holy Redeemer, Lake Worth. The team spent five days in June helping to refurbish Holy Redeemer’s facilities, inside and out. (See story p. 16.) Photo by Elaine Greenfield Seeing need and hope with ERD in Ghana By Canon Richard Miller located in the northern part of the country, where we met with the staff of Anglican Diocesan Development and What a wonderful Father’s Day gift I gave myself Relief Organization (ADDRO). -

Ship-Breaking

Bulletin of information and analysis April 14th, 2014 on ship demolition # 35 from January 1st to March 31st 2014 Ship-Breaking Content Sensational ! the Past reappears in the 1 The END: Cunard Countess, she 60 Gas tanker 42 Caribbean! has had all sorts of experiences Bulk carrier 44 Islang 3 Cattle carrier 10 Cement carrier 51 Baltic Ace is rising back to the surface 6 Heavy load carrier 10 Ro Ro 52 Remove the Rena 6 Container ship 12 Car carrier 53 What has happened to them? 7 General cargo 24 Miscellaneous : tug, offshore 54 A 13 km long and 176,000 boxes 9 Reefer 35 supply vessel, dredger, capacity container ship left for Container ship 35 training ship demolition in Asia! Oil tanker 36 Ferry-passenger ship 55 Make way for the very big ones 11 Chemical tanker 41 Sources 62 Sensational ! Exclusive! the Past reappears in the Caribbean ! Cosette © Robin des Bois Zanoobia © Editions CETIM Cosette (ex-Phoenix Spirit, ex-Widad, ex-Stanmore, ex-Zanoobia, ex-Kusi, ex-Freightline One, ex- Translink, ex-Madouri, ex-Moundra, ex-Salome). OMI 6617025. Ro Ro. Built in 1966 in Papenpurg (Germany) by JL Meyer ; jumboized in 1969 and lengthened from 88 to 95 m. The Zanoobia is in Fort-de-France, in Martinique. The mythic cargo ship is awaiting demolition or sea dumping. She has been at berth there since the end of January 2010. She is known today as Cosette. Her last owner was established in Florida, United States. On the point of transporting humanitarian material to Haiti after the earthquake January 12, 2010, the Cosette was detained in Fort-de-France for security and financial reasons. -

To the P Inte Boca Pointe Country Club July/August 2007 Directory

FIRST CLASS MAIL Boca Pointe Country Club U.S. Postage 7144 Boca Pointe Drive PAID Boca Raton, Florida 33433 Boca Raton, FL Permit No. 962 To The P inte Boca Pointe Country Club July/August 2007 Directory Directory FOOD & BEVERAGE contents Dining Reservations 864-8503 Grand Café 864-8504 Board Message . .3 Grand Café Lounge 864-8505 Membership . .4 Main Dining Room 864-8506 Main Dining Room Lounge 864-8507 Around The Pointe . .5 Palms Terrace 864-8513 Club Events . .6 Center Court Café 864-8508 Dining News . .7 Match Pointe Café 864-8509 Golf . .8-9 Catering 864-8510 Photo Gallery - Golf . .10-11 Calendar . .12-13 SOCIAL & ENTERTAINMENT 864-8517 Photo Gallery - Adventures’ Club . .14-15 Tennis . .16 GOLF DEPARTMENT Fitness & Spa . .17 Morning Tee Time Reservation 864-8520 Events Booked By Jane Young . .18-19 Afternoon Tee Time Reservation 864-8521 Classes & Seminars . .21 Golf Pro Shop 864-8522 Social & Entertainment . .22-23 Ladies’ Golf Locker Room 864-8524 Men’s Golf Locker Room 864-8525 BOARD OF GOVERNORS TENNIS DEPARTMENT Aggie Winthrop Chairman Franklyn B. Weichselbaum Vice-Chairman Tennis Court Reservation 391-9897 Howard Davis Treasurer AC Tennis 864-8551 Carol Kaye Secretary AC Tennis Pros 864-8528 Barry J. Haberman Governor Tennis Pro Shop at Center Court 864-8529 Peter Lebowitz Governor Barry Oster Governor CLUBHOUSE Paul Volin General Manager Clubhouse Manager 864-8515 Directory Ladies’ Card Room 864-8546 MANAGEMENT STAFF Men’s Card Room 864-8547 Louis Bencini Chief Engineer Terry Daniels Executive Chef ADMINISTRATIVE OFFICES -

Downloads at Sea? Imagine Internet Connectivity Offshore the Same

& - • Hp A • - July 2003 MARITIME REPORTER AND «4 ENGINEERING NEWS www.marinelink.(om * a J> f* Older MPs: Save toor Scrap 'em - MM rfri5§Pfy 1 Jr" 1 I Maritime Security ^ / 1—J .» Bryant; Show me the (grant) Money! Hi];; # * m lilpri r Marine Propulsion 2003 Diesel Engine Technical Guide Investment in Design • CADCAM • SatCom Update • NorShipping 2003 Round-up GUASCOR WSSSB -WjHSJW /MO & EPA Compliant Engines & reduction gears from 575 hp to 1550 hp REAGAN MARINE Highway 75 • Plaquemine, LA • Tel (800) 237-3160 • Fax (225) 659-9090 • [email protected] GUASCOR Inc. I V 36 St., Suite 310 • Miami, FL 33166 • Tel (305) 436-8929 • Fax (305) 436-9633 • [email protected] Introducing the WaveCall 4003. Business level connectivity wherever you cruise. Tired of waiting for dial up or downloads at sea? Imagine Internet connectivity offshore the same as you get on shore - always on, lightning fast and multiple users. Just one meter in size, Compact and rugged, the 4003 stands the WaveCall 4003 gives you blazingly fast inbound and outbound speeds for downloading large files, up to all conditions. streaming video, voice, video teleconferencing or simply surfing the web at will. With coverage from Airtime Cost Comparison North to South America, Northern Europe to the Med, and soon in the WaveCall Inmarsat 4003 77' B! Far East, the 4003 also is the most cost efficient. Perfect for business. Download 512 kbps speed 64 kbps 64 kbps 1GB file 1 256 min 2,080 min 2,080 min download Perfect for family and crew. Perfect. 4 The WaveCall 4003 '16.53 ISDN '18.60 Cost/MB •1 '36.00 MPOS ('9.00/min) from the name you trust, Sea Tel. -

Florida's "Cruises to Nowhere" Industry: Current Status and Future Prospects

Nova Southeastern University NSUWorks Faculty Scholarship Shepard Broad College of Law 11-1-2017 Florida's "Cruises to Nowhere" Industry: Current Status and Future Prospects Robert Jarvis [email protected] Follow this and additional works at: https://nsuworks.nova.edu/law_facarticles Part of the Law Commons NSUWorks Citation Robert Jarvis, Florida's "Cruises to Nowhere" Industry: Current Status and Future Prospects, 21 Gaming L. Rev. & Econ. 18 (2017), Available at: https://nsuworks.nova.edu/law_facarticles/374 This Article is brought to you for free and open access by the Shepard Broad College of Law at NSUWorks. It has been accepted for inclusion in Faculty Scholarship by an authorized administrator of NSUWorks. For more information, please contact [email protected]. GAMING LAW REVIEW AND ECONOMICS Volume 21, Number 1, 2017 Ó Mary Ann Liebert, Inc. DOI: 10.1089/glre.2017.2115 Florida’s ‘‘Cruises to Nowhere’’ Industry: Current Status and Future Prospects Robert M. Jarvis I. INTRODUCTION and unregulated form of gambling,4 Florida’s CTN industry, which has existed since 1984,5 has btaining reliable information about the tended to attract operators who, for a variety of rea- O ‘‘cruises to nowhere’’ (CTN)1 industry in Flor- sons, have preferred to maintain a low profile.6 The ida2 always has been difficult.3 As an unlicensed most notable exception—SunCruz Casinos’ brash Keywords: casino boats; cruises to nowhere; floating casinos; it is odd that a profile of the industry is lacking from academic gambling ships; offshore gambling; unregulated gambling textbooks and manuscripts.’’). With few-to-no reporting requirements, how much Florida’s CTN operators annually earn has long been a closely guarded Robert M. -

Volume XXV No. 4 September 2005 Mary R. Nye, Editor 2005 IOBG CONTACT LISTING APPOINTED OFFICERS REPRESENTATIVES COMMITTEES EDUC

Volume XXV No. 4 September 2005 Mary R. Nye, Editor 2005 IOBG CONTACT LISTING APPOINTED OFFICERS REPRESENTATIVES COMMITTEES EDUC. & DEVELOPMENT PROTOCOL OFFICER BOAT U.S. AUDIT Louis Key Jr. 440-944-6200 Marion Hughes (Gerva) Phil Arms (Ann) Vern Bendsen 707-422-3510 Art Garside 734-671-6997 3608 Road #84 352 Seawind Drive Steve Willing 519-944-1397 Pasco, WA 99301 Vallejo, CA 94590 AUXILIARY LIAISON Tel/Fax: 509-547-6743 Tel: 707-644-9016 Richard Janiszewski 609-294-2393 BY-LAWS & POLICY MANUAL [email protected] [email protected] Phil Arms 707-644-9016 LEGAL OFFICER RECORDING SECRETARY HUMANITARIAN FND. LIAISON Dave Phelps 310-297-3743 George Knies (Ann) Sue Brauner Phil Arms 707-644-9016 George Knies 925-939-0230 2333 Lariat Lane 2039 Olympic Drive Carol Promessi 925-427-6250 POSITION STATEMENT Walnut Creek, CA 94596 Martinez, CA 94553 CONVENTION 2005 Tel: 925-939-0230 Tel: 925-229-2906 Joe Zammit 800-298-9445 Harvey Sussel 561-691-4424 Fax: 925944-0474 Fax: 925-932-7603 CONVENTION REVIEW [email protected] [email protected] NATIONAL BOATING FEDERATION Art Theobald 716-633-7122 Phil Arms 707-644-9016 LOG EDITOR-IN-CHIEF SUPPLY OFFICER Marshall Nemoy 888-378-2211 Art Garside 734-671-6997 Mary R. Nye Open Carol Promessi 925-427-6250 1014 117th Street South U.S. SAILING Tacoma, WA 98444-2450 WEBMASTERS ELECTIONS Tel: 253-224-8592 Marshall Nemoy Joe Zammit 800-298-9445 Carol Promessi 925-427-6250 [email protected] [email protected] NOMINATING Mary R. Nye Larry Foote 707-374-2124 [email protected] Art Theobald 716-633-7122 Harvey Sussel 561-691-4424 ELECTED OFFICERS Executive Secretary Northwestern VP North Central VP Northeastern VP Southwestern VP Southeastern VP Mary Eiffert (Alan) Jerry Rudd (Jackie) Steve Willing (Shirley) Marc D.