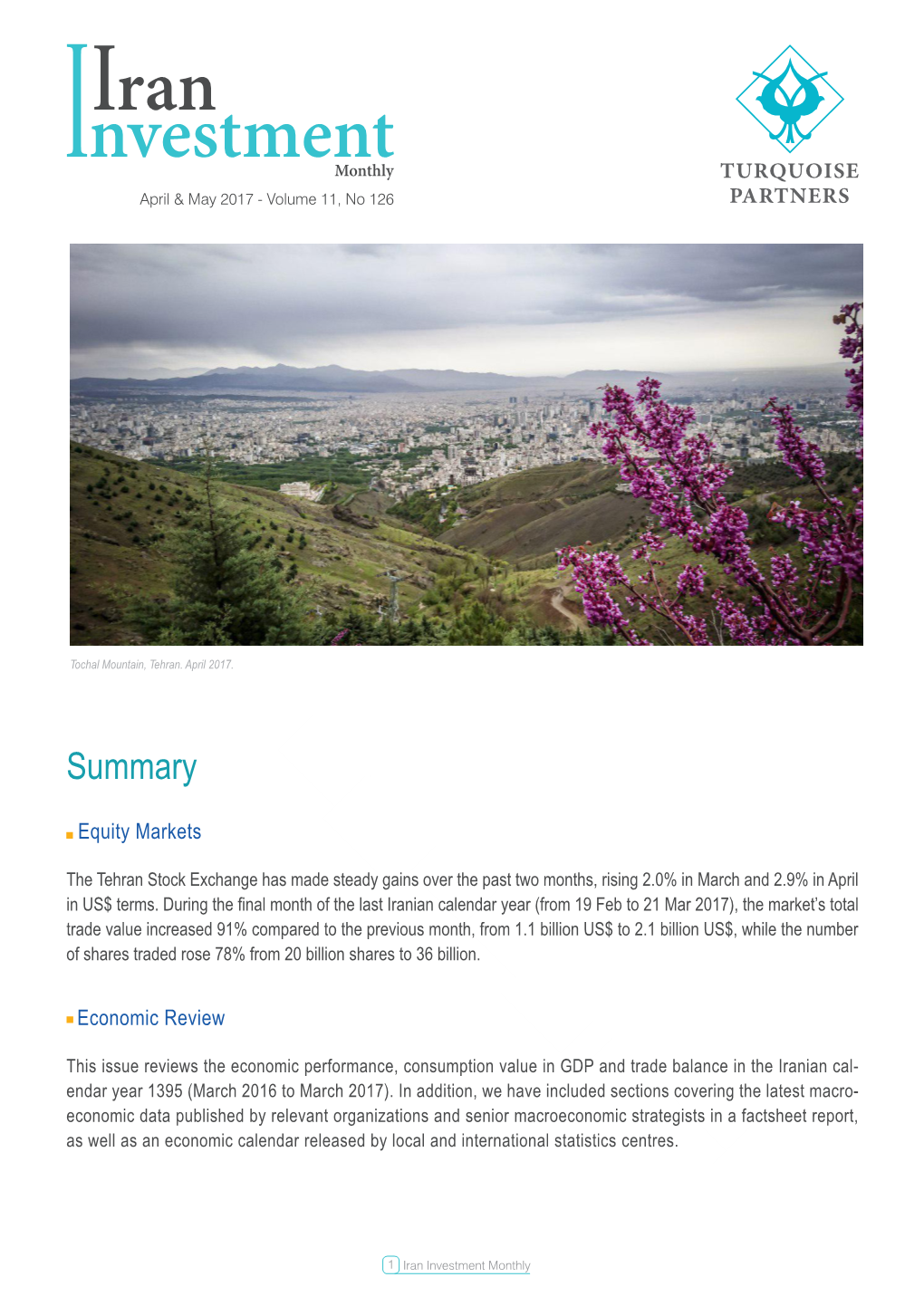

April & May 2017 No 126, Volume 11

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Iran Chamber of Commerce,Industries and Mines Date : 2008/01/26 Page: 1

Iran Chamber Of Commerce,Industries And Mines Date : 2008/01/26 Page: 1 Activity type: Exports , State : Tehran Membership Id. No.: 11020060 Surname: LAHOUTI Name: MEHDI Head Office Address: .No. 4, Badamchi Alley, Before Galoubandak, W. 15th Khordad Ave, Tehran, Tehran PostCode: PoBox: 1191755161 Email Address: [email protected] Phone: 55623672 Mobile: Fax: Telex: Membership Id. No.: 11020741 Surname: DASHTI DARIAN Name: MORTEZA Head Office Address: .No. 114, After Sepid Morgh, Vavan Rd., Qom Old Rd, Tehran, Tehran PostCode: PoBox: Email Address: Phone: 0229-2545671 Mobile: Fax: 0229-2546246 Telex: Membership Id. No.: 11021019 Surname: JOURABCHI Name: MAHMOUD Head Office Address: No. 64-65, Saray-e-Park, Kababiha Alley, Bazar, Tehran, Tehran PostCode: PoBox: Email Address: Phone: 5639291 Mobile: Fax: 5611821 Telex: Membership Id. No.: 11021259 Surname: MEHRDADI GARGARI Name: EBRAHIM Head Office Address: 2nd Fl., No. 62 & 63, Rohani Now Sarai, Bazar, Tehran, Tehran PostCode: PoBox: 14611/15768 Email Address: [email protected] Phone: 55633085 Mobile: Fax: Telex: Membership Id. No.: 11022224 Surname: ZARAY Name: JAVAD Head Office Address: .2nd Fl., No. 20 , 21, Park Sarai., Kababiha Alley., Abbas Abad Bazar, Tehran, Tehran PostCode: PoBox: Email Address: Phone: 5602486 Mobile: Fax: Telex: Iran Chamber Of Commerce,Industries And Mines Center (Computer Unit) Iran Chamber Of Commerce,Industries And Mines Date : 2008/01/26 Page: 2 Activity type: Exports , State : Tehran Membership Id. No.: 11023291 Surname: SABBER Name: AHMAD Head Office Address: No. 56 , Beside Saray-e-Khorram, Abbasabad Bazaar, Tehran, Tehran PostCode: PoBox: Email Address: Phone: 5631373 Mobile: Fax: Telex: Membership Id. No.: 11023731 Surname: HOSSEINJANI Name: EBRAHIM Head Office Address: .No. -

Credit Rating Companies with Multi-Criteria Decision Making Models and Artificial Neural Network Model

J. Basic. Appl. Sci. Res., 3(5)536-546, 2013 ISSN 2090-4304 Journal of Basic and Applied © 2013, TextRoad Publication Scientific Research www.textroad.com Credit Rating Companies with Multi-Criteria Decision Making Models and Artificial Neural Network Model Maghsoud Amiri1, Mehdi Biglari Kami*2 1Allameh Tabatabaei University, Tehran, Iran 2Institute of Higher Education Raja, Qazvin, Iran ABSTRACT This research seeks to develop a procedure for credit rating of manufacturing corporations accepted in Tehran stock exchange. So, financial ratios of 181 manufacturing corporations in Iran stock exchange were extracted, These ratios reflect the financial ability to pay principal and interest of loan. Initially, fifty selected corporations ranked by using TOPSIS method based on financial ratios by using of Shannon entropy will be obtained the weight of each criterion. In addition, classification credit with neural network has compared by logistic regression; and finally, each had more credibility, used to rank all corporations. Then all corporations have classified by neural network. Finally, the neural network classification results compared with the expert classification. About 95% of the neural network data has placed in its respective class, and the data results indicated a robust neural network classification based on training. The neural network offered far more accurate answer than the logistic regression in this classification. At the end, the neural network ranked all corporations, and neural network classification results compared with expert opinion, showing that the neural network classification was very close to an expert opinion. KEYWORDS: Financial ratios; TOPSIS; Artificial neural network; Logistic regression. INTRODUCTION Today, the credit industry plays an important role in the economy of corporations. -

Annual Report Annual Report

Tehran Stock Exchange Annual Report Exchange 2011 Stock Tehran Tehran Stock Exchange Address: No.228,Hafez Ave. Tehran - Iran Tel: (+98 021) 66704130 - 66700309 - 66700219 Fax: (+98 021) 66702524 Zip Code: 1138964161 Gun-metal relief discovered in Lorestan prov- ince, among the Achaemedian dynasty’s (550-330 BC)Antiquities. Featuring four men, hand in hands, indicating unity and cooperation; standing inside circles of 2011 globe,which is it, according to Iranian ancient myths, put on the back of two cows, ANNUAL symbols of intelligence and prosperity. Tehran Stock Exchange Implementation: CAPITAL&MARKET REPORT ANNUAL REPORT Tehran Stock Exchange 2011 Tehran Stock Exchange Tehran www.tse.ir Annual Report 2011 2 Tehran Stock Exchange Tehran www.tse.ir Mission Statement To develop a fair, efficient and transparent market equipped with diversified instruments and easy access in order to create added value for the stakeholders. Vision To be the region’s leading Exchange and country’s economic growth driver. Goals To increase the capital market’s share in financing the economic productive activities. To apply the effective rules and procedures to protect the market’s integrity and shareholders’ equity. To expand the market through using updated and efficient technology and processes. To promote financial literacy and develop investing and shareholding culture in Iran. To extend and facilitate the market access through information technology. To create value for shareholders and comply with transparency and accountability principles, with cooperation -

1 アフガニスタン Islamic Republic of Afghanistan Al Qa

国名、地域名 企業名、組織名 別名 懸念区分 No. Country or Region Company or Organization Also Known As Type of WMD ・The Base ・Al Qaeda ・Islamic Salvation Foundation ・The Group for the Preservation of the アフガニスタン Holy Sites 化学 1 Islamic Republic of Al Qa'ida/Islamic Army ・The Islamic Army for the Liberation of C Afghanistan Holy Places ・The World Islamic Front for Jihad against Jews and Crusaders ・Usama Bin Laden Network ・Usama Bin Laden Organisation ・Safa Nicu Sepahan アフガニスタン ・Safanco Company 核 2 Islamic Republic of Safa Nicu ・Safa Nicu Afghanistan Company N Afghanistan ・Safa Al-Noor Company ・Safa Nicu Ltd Company アフガニスタン Islamic Republic of Afghanistan 核 3 Ummah Tameer E-Nau (UTN) N パキスタン Islamic Republic of Pakistan アラブ首長国連邦 生物、化学、ミ 4 United Arab Energy Global International FZE サイル、核 Emirates B,C,M,N アラブ首長国連邦 ミサイル 5 United Arab International General Resourcing FZE M Emirates アラブ首長国連邦 核 6 United Arab Modern Technologies FZC (MTFZC) N Emirates アラブ首長国連邦 ・PetroIran Petroiran Development Company (PEDCO) ミサイル、核 7 United Arab ・PEDCO Ltd M,N Emirates ・National Iranian Oil Company - PEDCO アラブ首長国連邦 核 8 United Arab Qualitest FZE N Emirates ・Safa Nicu Sepahan アラブ首長国連邦 ・Safanco Company 核 9 United Arab Safa Nicu ・Safa Al-Noor Company N Emirates ・Safa Nicu Ltd Company イスラエル 核 10 Ben-Gurion University (of the Negev) State of Israel N イスラエル 核 11 Nuclear Research Center Negev (NRCN) State of Israel N ・7th of Tir Complex ・7th of Tir Industrial Complex イラン ・7th of Tir Industries 核 12 Islamic Republic of 7th of Tir ・7th of Tir Industries of Isfahan/Esfahan N Iran ・Mojtamae Sanate Haftome Tir ・Sanaye Haftome Tir ・Seventh of Tir 1 / 32 ページ イラン 核 13 Islamic Republic of Abadan Oil Refining Company ・Abadan Oil Refining Co. -

Market Transaction Trade Resumption 11-May-2016 Trading Halt 11

11-May-2016 Market Transaction Trade resumption 11-May-2016 Name Opening Price Etebari Iran Co-R (RKSH) ----------- Nirou Trans-R (NIRO) 4000R Parsian Ecommerc(EPRS) -------- Neiriz Cement (SSNR) ------- Buali Inv (BALI) --------- Nirou Trans-R (NIRO) 4000R Khazar Shipping(KHZZ) 7950R Sabzevar Cement(SBZZ) 732R Pegah Fars Co(GFRZ) 3630R Alborz Invest(ETLZ) 1351R Trading halt 11- May -2016 Name Closing Price Reasons Kh. Pegah Dairy (SPKH) 5797 R General Assembly Inf. Services (INFO) 18795 R General Assembly Gharb Cement (SGRB) 2763 R General Assembly 4689 R Extraordinary assembly in case of choosing board Boroujerd T (BROJ) members Banks Employees-R (SKBV) 5 R End of underwriting Bahman Inv.-R(SBAH) 493R End of underwriting Baghmishe(BGHZ) 2702R Adjusted EPS Zagros Petro(PZGZ) 11,199R General Assembly Alborz Bulk Co(BLKZ) 4,715R General Assembly Saadi Tile(KSAD) 1,979R Adjusted EPS Sand Foundry(TAMI) 1,930R Adjusted EPS www.behgozinbroker.com 11-May-2016 Block trading 11-May -2016 Name Number of Shares Price Kharazmy Invest (IKHR) 25,500,000 1355R Bank Melli Inv (BANK) 25,000,000 2400R Mobarakeh Steel (FOLD) 10,152,000 1377R Sina Fin. Ins (VSIN) 7,500,000 1377R Atye Damavand (ATDM) 5,500,000 2184R The best industry groups (in terms of volume) 11- May -2016 Industry Index Change Best Trade(Value) Automotives & autoparts -2.49% Iran Khodro (IKCO) Basic Metals -0.49% Isfahan Steel(ZOBZ) Investment Companies -1.16% Saipa Inv (SSAP) Conglomerates -0.55% Omid Inv. Mng (OIMC) Bank -0.20% Saderat Bank (BSDR) Chemical and petrochemical -0.41% Shazand Petr (PARK) Metalic products -3.19% Azarab Ind (AZAB) www.behgozinbroker.com 11-May-2016 There are some changes in active shareholders ,we summarize the important ones. -

Identification and Ranking Performance Indicators Using ISM and BWM Methods in Companies Listed in Tehran Stock Exchange

Original Article Identification and Ranking performance Indicators Using ISM and BWM Methods in Companies Listed in Tehran Stock Exchange 1 2 2 Saber Amjadian , Ata Mohammadi *, Behzad Parvizi 1 Ph.D. student in Accounting, Sanandaj Branch, Islamic Azad University of Sanandaj, Iran.2 Assistant professor in Accounting, Accounting group, Sanandaj Branch, Islamic Azad University, Sanandaj, Iran, Abstract The current research sought to present a model for evaluating the financial performance of companies active in Tehran stock exchange. T this end, 50 financial ratios proposed by experts were utilized, among which, 49 ratios were finalized. These ratios were categorized into 6 groups including consolidation, economic, leverage, liquidity, profitability and activity. According to the experts` views, these ratios were weighted and analyzed using multivariate decision making criteria of BWM and Aras technique as well as Lingo software. Finally, the companies were ranked; among the existing 516 companies whose ratios were accessible, the investigations were conducted. The results indicated that Iran mineral salts company, Golgohar mining and industrial company and Khouzestan steel company obtained 1 to 3 rankings, respectively. Keywords: Performance evaluation, Financial ratios, The best worst method, Tehran stock exchange controlling in the production and finally improving the INTRODUCTION products or presenting services. Edward Deming has emphasized on the fact that all business processes should be In fact, if it is not possible to measure what is being spoken a part of evaluation system along with the feedback cycle. of, and if it is not possible to express the intended meaning Jac Fitz Enz believed that evaluating every business activity in terms of numbers, it seems that nothing has been is an essential issue. -

Q3 2016 Iran

Q3 2016 www.bmiresearch.com IRAN PHARMACEUTICALS & HEALTHCARE REPORT INCLUDES 10-YEAR FORECASTS TO 2025 Published by:BMI Research Iran Pharmaceuticals & Healthcare Report Q3 2016 INCLUDES 10-YEAR FORECASTS TO 2025 Part of BMI’s Industry Report & Forecasts Series Published by: BMI Research Copy deadline: May 2016 ISSN: 1748-1953 BMI Research © 2016 Business Monitor International Ltd Senator House All rights reserved. 85 Queen Victoria Street London All information contained in this publication is EC4V 4AB copyrighted in the name of Business Monitor United Kingdom International Ltd, and as such no part of this Tel: +44 (0) 20 7248 0468 publication may be reproduced, repackaged, Fax: +44 (0) 20 7248 0467 redistributed, resold in whole or in any part, or used Email: [email protected] in any form or by any means graphic, electronic or Web: http://www.bmiresearch.com mechanical, including photocopying, recording, taping, or by information storage or retrieval, or by any other means, without the express written consent of the publisher. DISCLAIMER All information contained in this publication has been researched and compiled from sources believed to be accurate and reliable at the time of publishing. However, in view of the natural scope for human and/or mechanical error, either at source or during production, Business Monitor International Ltd accepts no liability whatsoever for any loss or damage resulting from errors, inaccuracies or omissions affecting any part of the publication. All information is provided without warranty, and Business Monitor International Ltd makes no representation of warranty of any kind as to the accuracy or completeness of any information hereto contained. -

Annual Report 2015/16

Annual Report 2015/16 Table of Contents Saman Bank at a Glance Main Financial Items ........................................................................ 5 Credit Rating .................................................................................... 7 Board of Directors Report ............................................................... 11 Statement by CEO ............................................................................. 16 Retail Banking .................................................................................. 18 Corporate Banking ........................................................................... 22 International Banking ...................................................................... 24 Premium Banking ............................................................................ 27 Saman Bank Investment ....................................................................................... 31 Retail and Syndicated Loans ............................................................ 38 In 2015/16 Electronic Banking ........................................................................... 42 Human Capital .................................................................................. 45 Social Responsibilities ..................................................................... 48 Risk Management ............................................................................ 50 Corporate Governance ..................................................................... 55 Inspection ........................................................................................ -

United Arab Emirates Al Haitam for Industries Aal Khobar

Al Had General Trading FzDubai - - United Arab Emirates Al Haitam For Industries AAl Khobar - - Saudi Arabia Al Zayani Trading CompaSafat - - Kuwait Azar Refractories CompaEsfahan - - Iran Black Cat Construction WDoha - - Qatar Geco Chemicals Co Ltd - - - - United Arab Emirates Giffin Graphics Co Llc RecAbu Dhabi - - United Arab Emirates Modjtaba Shaban TradingBur Dubai - - United Arab Emirates Nafco Chartering And TradSharjah - - United Arab Emirates Oman International ElectrAl Khuwair - - Oman Prime Trading Co Llc RecMuscat - - Oman Shahroud Cement CompaTehran - - Iran The Arabian Medical ComDamascus - - Syria Zalvand Trading CompanyMashhad - - Iran Al Nasser Holdings ComAbu Dhabi Abu Dhabi United Arab Emirates Anabeeb Pipe ManufaturAl Musaffah Abu Dhabi United Arab Emirates Oasis International LeasiAbu Dhabi Abu Dhabi United Arab Emirates Suhail Al Mazroui Group OfAbu Dhabi Abu Dhabi United Arab Emirates Tata Projects Ltd Record AbuDept Dhabi Abu Dhabi United Arab Emirates Tristar Transport & ContrMussafah Abu Dhabi United Arab Emirates Al Ain National Juice AndAl Ain Al Ain United Arab Emirates Al Dahra Agricultural ComAl Ain Al Ain United Arab Emirates Bin Darwish Gen Cont & MaAl Ain Al Ain United Arab Emirates Oman Electric Company (Al Ain Al Ain United Arab Emirates A B C Islamic Bank E C RecManama Bahrain Adel & Sadiq Trading Co ManamaW Bahrain Al Jazira Cold Store ComManama Bahrain Arab Insurance Group (B.Manama Bahrain B F G International W L LManama Re Bahrain Bahrain Kuwait InsuranceManama Co Bahrain Bank Muscat InternationalManama -

In the Name of GOD

In the Name of GOD SINA BANK Annual Report 2015 - 2016 Table of Contents Financial Highlights 4 Message of the Board of Directors 5 Introducing the Board of Directors 6 Introducing the Executive Board 7 Organisational Chart 8 CHAPTER I - Introduction 9 Background 10 Objectives 10 Vision 10 Mission Statement 10 Strategies 11 Regulatory Environment 12 Specialist Committees & Workgroups 12 Our Capital 13 Prizes, Distinctions & Accomplishments 16 Sina Bank Listed in the Stock Exchange 19 Composition of Shareholders 20 Our Future Plans 20 CHAPTER II - Performance 21 Operational Performance 22 Human Resources 22 Branch Network 22 International Banking & Foreign Exchange Services 23 Anti-Money Laundering Department 24 Information Technology 27 Risk Management 29 Regulation Compliance Department 32 Financial Performance 34 Main Financial Items 34 Balance of Deposits 35 Islamic Banking Principles 36 Balance of Loans 38 Revenues 39 Interest Paid to Depositors 40 Ratios 41 Capital Adequacy Ratio 42 Our Investments 42 CHAPTER III - Independent Auditor’s Reports & Financial 43 Statements Sina Bank Financial Highlights Total Revenues Total Assets 35,000,000 180,000,000 30,000,000 160,000,000 140,000,000 25,000,000 120,000,000 20,000,000 100,000,000 15,000,000 80,000,000 million IRR million IRR 60,000,000 10,000,000 40,000,000 5,000,000 20,000,000 0 0 2014-15 2015-16 2014-15 2015-16 Balance of Loans Total Shareholders’ Equity (IRR & Foreign Currency) 140,000,000 16,000,000 120,000,000 14,000,000 12,000,000 100,000,000 10,000,000 80,000,000 8,000,000 60,000,000 million IRR million IRR 6,000,000 40,000,000 4,000,000 20,000,000 2,000,000 0 0 2014-15 2015-16 2014-15 2015-16 Balance of Deposits Registered Capital (IRR & Foreign Currency) 160,000,000 12,000,000 140,000,000 10,000,000 120,000,000 8,000,000 100,000,000 80,000,000 6,000,000 million IRR million IRR 60,000,000 4,000,000 40,000,000 2,000,000 20,000,000 0 0 2014-15 2015-16 2014-15 2015-16 The rate of exchange was $1/IRR 30,240 at the end of the reported period. -

Iranian Top Export Companies

Company Name Tel Fax E-mail Web-site Product Meraat International Trading (+98-21)22222922 (+98-21)22222944 [email protected] www.meraat.com Bitumen Novin Alloys Semnan (+98-21)88881126 (+98-21)88799065 [email protected] www.novinalloys.com moulding Mammut Industrial Group Tehran (+98-21)88554233 (+98-21)88103520 [email protected] www.sandwichpanel.com Trailers Behshahr Ind. (+98-21)66250435 (+98-21)66250013 info@behshahr_ind.co www.ladanoil.com Vegetable oil Yazd Baf (+98-21)66463395 (+98-21)66952513 [email protected] www.yazdbaf.com Cloth Arta Industrial Group (+98-21)88772814 (+98-21)88775185 [email protected] www.artagroup.com Carpet & Moqutte hygienic & Detergent Tolypers ( ) ( ) [email protected] www.kafsa.com/tolypers +98-21 22019940 +98-21 22010260 Product Minoo Industrial (+98-21)66706009 (+98-21)66703152 [email protected] www.minoo.com Sweets and chocolates Pars Tire (+98-21)88739778-80 (+98-21)88739781 [email protected] www.parstire.ir Tire Iran Pharmaceutical Industries (+98-21)88736335 (+98-21)88731069 [email protected] www.pharmieco.com Drug Momtaz Sahand Industrial ( ) ( ) - - Plastic Products Production +98-21 77341610 +98-21 77341609 Afroozkar Tabriz Leather (+98-41)32853063 (+98-41)32852922 [email protected] www.afroozkar.com Leather Doodeh Sanati Pars (+98-21)88783062 (+98-21)88779222 [email protected] www.dsp.co.ir Industrial soot Dashte Neshat (+98-21)88192154 (+98-21)88192477 [email protected] www.dashteneshat.com Food Product Payam Shoe Manufacturing (+98-21)55201801 (+98-21)56545753 [email protected] -

In the Name of God International Court Of

IN THE NAME OF GOD INTERNATIONAL COURT OF JUSTICE CASE CONCERNING ALLEGED VIOLATIONS OF THE 1955 TREATY OF AMITY, ECONOMIC RELATIONS, AND CONSULAR RIGHTS (ISLAMIC REPUBLIC OF IRAN V. UNITED STATES OF AMERICA) MEMORIAL OF THE ISLAMIC REPUBLIC OF IRAN 24 May 2019 TABLE OF CONTENTS PART I. INTRODUCTION AND FACTUAL BACKGROUND ........................................ 1 CHAPTER I. INTRODUCTION ........................................................................................... 1 SECTION 1. THE SUBJECT-MATTER OF THE DISPUTE 1 SECTION 2. PROCEDURAL HISTORY: PROVISIONAL MEASURES AND THE U.S. REACTION TO THE COURT’S ORDER DATED 3 OCTOBER 2018 6 SECTION 3. JURISDICTION 10 SECTION 4. APPLICABLE LAW 12 SECTION 5. OUTLINE OF IRAN’S ARGUMENTS AND STRUCTURE OF THE MEMORIAL 14 CHAPTER II. THE RE-IMPOSITION OF THE SO-CALLED “NUCLEAR- RELATED” SANCTIONS BY THE UNITED STATES ................................................... 18 SECTION 1. THE NUCLEAR-RELATED MEASURES RE-IMPOSED AS OF 7 AUGUST 2018 22 A. The nuclear-related measures re-imposed under E.O. 13846 and related statutory authorities 22 i. Sanctions relating to support for the Government of Iran’s purchase or acquisition of U.S. dollar bank notes or precious metals 23 ii. Sanctions on transactions with Iran in precious metals, graphite, raw, or semi-finished metals, and industrial software 24 iii. Sanctions on transactions in the Iranian Rial 29 iv. Sanctions related to the issuance of Iranian sovereign debt 31 v. Sanctions on Iran’s automotive sector 32 B. The revocation of authorizations under U.S. sanctions regarding Iran whereby the scope of permissible direct trade between the two countries had been expanded 34 i. Sanctions concerning activities related to the export or re-export to Iran of commercial passenger aircraft and related parts and services 34 ii.