Annual Report 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Announcement Report for the First Quarter of 2021 Of

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. ANNOUNCEMENT REPORT FOR THE FIRST QUARTER OF 2021 OF CHINA CITIC BANK CORPORATION LIMITED This announcement is made by CITIC Limited (the “Company”) pursuant to Rule 13.09(2)(a) of the Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limited and the Inside Information Provisions under Part XIVA of the Securities and Futures Ordinance (Chapter 571 of the Laws of Hong Kong). The Company notes the announcement (the “CITIC Bank Announcement”) of today’s date made by China CITIC Bank Corporation Limited (“CITIC Bank”), a principal subsidiary of the Company, in relation to the unaudited consolidated results of CITIC Bank and its subsidiaries for the first quarter ended 31 March 2021. The CITIC Bank Announcement is available on the website of Hong Kong Exchanges and Clearing Limited at www.hkexnews.hk and is set out at the end of this announcement. By Order of the Board CITIC Limited Zhu Hexin Chairman Hong Kong, 29 April 2021 As at the date of this announcement, the executive directors of the Company are Mr Zhu Hexin (Chairman), Mr Xi Guohua and Ms Li Qingping; the non-executive directors of the Company are Mr Song Kangle, Mr Liu Zhuyu, Mr Peng Yanxiang, Ms Yu Yang, Mr Liu Zhongyuan and Mr Yang Xiaoping; and the independent non-executive directors of the Company are Mr Francis Siu Wai Keung, Dr Xu Jinwu, Mr Anthony Francis Neoh, Mr Shohei Harada and Mr Gregory Lynn Curl. -

Fidelity® Emerging Markets Index Fund

Quarterly Holdings Report for Fidelity® Emerging Markets Index Fund January 31, 2021 EMX-QTLY-0321 1.929351.109 Schedule of Investments January 31, 2021 (Unaudited) Showing Percentage of Net Assets Common Stocks – 92.5% Shares Value Shares Value Argentina – 0.0% Lojas Americanas SA rights 2/4/21 (b) 4,427 $ 3,722 Telecom Argentina SA Class B sponsored ADR (a) 48,935 $ 317,099 Lojas Renner SA 444,459 3,368,738 YPF SA Class D sponsored ADR (b) 99,119 361,784 Magazine Luiza SA 1,634,124 7,547,303 Multiplan Empreendimentos Imobiliarios SA 156,958 608,164 TOTAL ARGENTINA 678,883 Natura & Co. Holding SA 499,390 4,477,844 Notre Dame Intermedica Participacoes SA 289,718 5,003,902 Bailiwick of Jersey – 0.1% Petrobras Distribuidora SA 421,700 1,792,730 Polymetal International PLC 131,532 2,850,845 Petroleo Brasileiro SA ‑ Petrobras (ON) 2,103,697 10,508,104 Raia Drogasil SA 602,000 2,741,865 Bermuda – 0.7% Rumo SA (b) 724,700 2,688,783 Alibaba Health Information Technology Ltd. (b) 2,256,000 7,070,686 Sul America SA unit 165,877 1,209,956 Alibaba Pictures Group Ltd. (b) 6,760,000 854,455 Suzano Papel e Celulose SA (b) 418,317 4,744,045 Beijing Enterprises Water Group Ltd. 2,816,000 1,147,720 Telefonica Brasil SA 250,600 2,070,242 Brilliance China Automotive Holdings Ltd. 1,692,000 1,331,209 TIM SA 475,200 1,155,127 China Gas Holdings Ltd. 1,461,000 5,163,177 Totvs SA 274,600 1,425,346 China Resource Gas Group Ltd. -

中 國 民 生 銀 行 股 份 有 限 公 司 China Minsheng Banking Corp., Ltd

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. 中國民生銀行股份有限公司 CHINA MINSHENG BANKING CORP., LTD. (A joint stock limited company incorporated in the People’s Republic of China with limited liability) (Stock Code: 01988) (USD Preference Shares Stock Code: 04609) Results Announcement For the Year Ended 31 December 2019 The Board of Directors (the “Board”) of China Minsheng Banking Corp., Ltd. (the “Company”) hereby announces the audited results of the Company and its subsidiaries for the year ended 31 December 2019. This announcement, containing the full text of the 2019 Annual Report of the Company, complies with the relevant requirements of the Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limited (the “Hong Kong Stock Exchange”) in relation to information to accompany preliminary announcements of annual results. Publication of Annual Results Announcement and Annual Report This results announcement will be published on the HKEXnews website of Hong Kong Stock Exchange (www.hkexnews.hk) and the Company’s website (www.cmbc.com.cn). The 2019 Annual Report of the Company will be dispatched to holders of H shares of the Company and published on the websites of the Company and Hong Kong Stock Exchange in due course. Profit Distribution On 30 March 2020, the 20th meeting of the seventh session of the Board of the Company approved the profit distribution plan to declare to holders of A shares and H shares whose names appear on the registers as at the record dates as indicated in the notice of 2019 annual general meeting of the Company to be published by the Company in due course, a cash dividend of RMB3.70 (tax inclusive) for every 10 shares being held. -

Printmgr File

THIS WEB PROOF INFORMATION PACK IS IN DRAFT FORM. The information contained herein is incomplete and subject to change and it must be read in conjunction with the section headed “Warning” on the cover of this Web Proof Information Pack. OUR HISTORY AND CORPORATE STRUCTURE Important Milestones The following are the important milestones in our history to date: Year Event August 1999 Our Company was incorporated in the PRC. July 2000 We first obtained accreditation of ISO 9001 in respect of our quality control system. October 2000 We became listed on the SZSE. July 2003 We received certification from TüV Rheinland, German for our quality management system. August 2003 We acquired all the operating assets of Zhongbiao. November 2003 We acquired the crane machinery business of Hunan Puyuan Construction Machinery Co., Ltd. December 2004 We manufactured the QUY200 crawler crane, the then largest crawler crane in the PRC. March 2005 We developed and manufactured a 12-tons high pressure washing vehicle ZLJ520GQX. July 2005 The Company received CE certification for pumping machines and entered into the European market. July 2006 We implemented our share reform, where the non-tradable Shares of our Company were converted into tradable Shares. August 2006 Our Company’s tower crane was first exported to Europe. October 2006 We successfully manufactured and developed the QUY600 crawler crane, the then largest crawler crane in the PRC. November 2006 Our Company manufactured the YZ27 road roller with the largest vibrating power in the PRC. September 2008 We acquired CIFA. August 2009 We manufactured a four-bridge chassis six-joint jibs 56m pump-truck. -

Lu Zhiqiang China Oceanwide

08 Investment.FIN.qxp_Layout 1 14/9/16 12:21 pm Page 81 Week in China China’s Tycoons Investment Lu Zhiqiang China Oceanwide Oceanwide Holdings, its Shenzhen-listed property unit, had a total asset value of Rmb118 billion in 2015. Hurun’s China Rich List He is the key ranked Lu as China’s 8th richest man in 2015 investor behind with a net worth of Rmb83 billlion. Minsheng Bank and Legend Guanxi Holdings A long-term ally of Liu Chuanzhi, who is known as the ‘godfather of Chinese entrepreneurs’, Oceanwide acquired a 29% stake in Legend Holdings (the parent firm of Lenovo) in 2009 from the Chinese Academy of Social Sciences for Rmb2.7 billion. The transaction was symbolic as it marked the dismantling of Legend’s SOE status. Lu and Liu also collaborated to establish the exclusive Taishan Club in 1993, an unofficial association of entrepreneurs named after the most famous mountain in Shandong. Born in Shandong province in 1951, Lu In fact, according to NetEase Finance, it was graduated from the elite Shanghai university during the Taishan Club’s inaugural meeting – Fudan. His first job was as a technician with hosted by Lu in Shandong – that the idea of the Shandong Weifang Diesel Engine Factory. setting up a non-SOE bank was hatched and the proposal was thereafter sent to Zhu Getting started Rongji. The result was the establishment of Lu left the state sector to become an China Minsheng Bank in 1996. entrepreneur and set up China Oceanwide. Initially it focused on education and training, Minsheng takeover? but when the government initiated housing Oceanwide was one of the 59 private sector reform in 1988, Lu moved into real estate. -

Annual Report 2019 Mobility

(a joint stock limited company incorporated in the People’s Republic of China with limited liability) Stock Code: 1766 Annual Report Annual Report 2019 Mobility 2019 for Future Connection Important 1 The Board and the Supervisory Committee of the Company and its Directors, Supervisors and Senior Management warrant that there are no false representations, misleading statements contained in or material omissions from this annual report and they will assume joint and several legal liabilities for the truthfulness, accuracy and completeness of the contents disclosed herein. 2 This report has been considered and approved at the seventeenth meeting of the second session of the Board of the Company. All Directors attended the Board meeting. 3 Deloitte Touche Tohmatsu CPA LLP has issued standard unqualified audit report for the Company’s financial statements prepared under the China Accounting Standards for Business Enterprises in accordance with PRC Auditing Standards. 4 Liu Hualong, the Chairman of the Company, Li Zheng, the Chief Financial Officer and Wang Jian, the head of the Accounting Department (person in charge of accounting affairs) warrant the truthfulness, accuracy and completeness of the financial statements in this annual report. 5 Statement for the risks involved in the forward-looking statements: this report contains forward-looking statements that involve future plans and development strategies which do not constitute a substantive commitment by the Company to investors. Investors should be aware of the investment risks. 6 The Company has proposed to distribute a cash dividend of RMB0.15 (tax inclusive) per share to all Shareholders based on the total share capital of the Company of 28,698,864,088 shares as at 31 December 2019. -

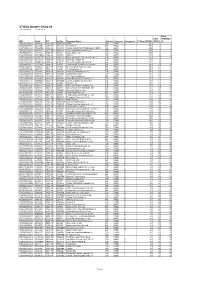

STOXX Greater China 80 Last Updated: 01.08.2017

STOXX Greater China 80 Last Updated: 01.08.2017 Rank Rank (PREVIOU ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) (FINAL) S) TW0002330008 6889106 2330.TW TW001Q TSMC TW TWD Y 113.9 1 1 HK0000069689 B4TX8S1 1299.HK HK1013 AIA GROUP HK HKD Y 80.6 2 2 CNE1000002H1 B0LMTQ3 0939.HK CN0010 CHINA CONSTRUCTION BANK CORP H CN HKD Y 60.5 3 3 TW0002317005 6438564 2317.TW TW002R Hon Hai Precision Industry Co TW TWD Y 51.5 4 4 HK0941009539 6073556 0941.HK 607355 China Mobile Ltd. CN HKD Y 50.8 5 5 CNE1000003G1 B1G1QD8 1398.HK CN0021 ICBC H CN HKD Y 41.3 6 6 CNE1000003X6 B01FLR7 2318.HK CN0076 PING AN INSUR GP CO. OF CN 'H' CN HKD Y 32.0 7 9 CNE1000001Z5 B154564 3988.HK CN0032 BANK OF CHINA 'H' CN HKD Y 31.8 8 7 KYG217651051 BW9P816 0001.HK 619027 CK HUTCHISON HOLDINGS HK HKD Y 31.1 9 8 HK0388045442 6267359 0388.HK 626735 Hong Kong Exchanges & Clearing HK HKD Y 28.0 10 10 HK0016000132 6859927 0016.HK 685992 Sun Hung Kai Properties Ltd. HK HKD Y 20.6 11 12 HK0002007356 6097017 0002.HK 619091 CLP Holdings Ltd. HK HKD Y 20.0 12 11 CNE1000002L3 6718976 2628.HK CN0043 China Life Insurance Co 'H' CN HKD Y 20.0 13 13 TW0003008009 6451668 3008.TW TW05PJ LARGAN Precision TW TWD Y 19.7 14 15 KYG2103F1019 BWX52N2 1113.HK HK50CI CK Property Holdings HK HKD Y 18.3 15 14 CNE1000002Q2 6291819 0386.HK CN0098 China Petroleum & Chemical 'H' CN HKD Y 16.4 16 16 HK0823032773 B0PB4M7 0823.HK B0PB4M Link Real Estate Investment Tr HK HKD Y 15.4 17 19 HK0883013259 B00G0S5 0883.HK 617994 CNOOC Ltd. -

China Vanke Co., Ltd. 2013 First Quarterly Report

China Vanke Co., Ltd. 2013 First Quarterly Report §1 Important Notice 1.1 The Board, the Supervisory Committee, Directors, members of the Supervisory Committee and senior management of the Company warrant that in respect of the information contained in this Quarterly Report, there are no misrepresentations or misleading statements, or material omission, and individually and collectively accept full responsibility for the authenticity, accuracy and completeness of the information contained in this Quarterly Report. 1.2 None of the Directors, members of the Supervisory Committee and senior management fails to assure or disputes with the authenticity, accuracy and completeness of the contents of this Quarterly Report. 1.3 Deputy Chairman Qiao Shibo and Director Wei Bin were not able to attend the board meeting in person due to their business engagements and had authorised Director Chen Ying to represent them and vote on behalf of them. Director Yu Liang was not able to attend the board meeting in person due to personal reasons and had authorised Director Xiao Li to represent him and vote on behalf of him. 1.4 This quarterly financial report of the Company has not been audited. 1.5 The Company’s Chairman Wang Shi, Director and President Yu Liang, and Executive Vice President and Supervisor of Finance Wang Wenjin declare that the financial report contained in this Quarterly Report is warranted to be true and complete. §2 Basic Corporate Information 2.1 Major accounting data and financial guidance (Unit: RMB’000) As at 31 March 2013 As at 31 -

Shop Direct Factory List Dec 18

Factory Factory Address Country Sector FTE No. workers % Male % Female ESSENTIAL CLOTHING LTD Akulichala, Sakashhor, Maddha Para, Kaliakor, Gazipur, Bangladesh BANGLADESH Garments 669 55% 45% NANTONG AIKE GARMENTS COMPANY LTD Group 14, Huanchi Village, Jiangan Town, Rugao City, Jaingsu Province, China CHINA Garments 159 22% 78% DEEKAY KNITWEARS LTD SF No. 229, Karaipudhur, Arulpuram, Palladam Road, Tirupur, 641605, Tamil Nadu, India INDIA Garments 129 57% 43% HD4U No. 8, Yijiang Road, Lianhang Economic Development Zone, Haining CHINA Home Textiles 98 45% 55% AIRSPRUNG BEDS LTD Canal Road, Canal Road Industrial Estate, Trowbridge, Wiltshire, BA14 8RQ, United Kingdom UK Furniture 398 83% 17% ASIAN LEATHERS LIMITED Asian House, E. M. Bypass, Kasba, Kolkata, 700017, India INDIA Accessories 978 77% 23% AMAN KNITTINGS LIMITED Nazimnagar, Hemayetpur, Savar, Dhaka, Bangladesh BANGLADESH Garments 1708 60% 30% V K FASHION LTD formerly STYLEWISE LTD Unit 5, 99 Bridge Road, Leicester, LE5 3LD, United Kingdom UK Garments 51 43% 57% AMAN GRAPHIC & DESIGN LTD. Najim Nagar, Hemayetpur, Savar, Dhaka, Bangladesh BANGLADESH Garments 3260 40% 60% WENZHOU SUNRISE INDUSTRIAL CO., LTD. Floor 2, 1 Building Qiangqiang Group, Shanghui Industrial Zone, Louqiao Street, Ouhai, Wenzhou, Zhejiang Province, China CHINA Accessories 716 58% 42% AMAZING EXPORTS CORPORATION - UNIT I Sf No. 105, Valayankadu, P. Vadugapal Ayam Post, Dharapuram Road, Palladam, 541664, India INDIA Garments 490 53% 47% ANDRA JEWELS LTD 7 Clive Avenue, Hastings, East Sussex, TN35 5LD, United Kingdom UK Accessories 68 CAVENDISH UPHOLSTERY LIMITED Mayfield Mill, Briercliffe Road, Chorley Lancashire PR6 0DA, United Kingdom UK Furniture 33 66% 34% FUZHOU BEST ART & CRAFTS CO., LTD No. 3 Building, Lifu Plastic, Nanshanyang Industrial Zone, Baisha Town, Minhou, Fuzhou, China CHINA Homewares 44 41% 59% HUAHONG HOLDING GROUP No. -

Table of Codes for Each Court of Each Level

Table of Codes for Each Court of Each Level Corresponding Type Chinese Court Region Court Name Administrative Name Code Code Area Supreme People’s Court 最高人民法院 最高法 Higher People's Court of 北京市高级人民 Beijing 京 110000 1 Beijing Municipality 法院 Municipality No. 1 Intermediate People's 北京市第一中级 京 01 2 Court of Beijing Municipality 人民法院 Shijingshan Shijingshan District People’s 北京市石景山区 京 0107 110107 District of Beijing 1 Court of Beijing Municipality 人民法院 Municipality Haidian District of Haidian District People’s 北京市海淀区人 京 0108 110108 Beijing 1 Court of Beijing Municipality 民法院 Municipality Mentougou Mentougou District People’s 北京市门头沟区 京 0109 110109 District of Beijing 1 Court of Beijing Municipality 人民法院 Municipality Changping Changping District People’s 北京市昌平区人 京 0114 110114 District of Beijing 1 Court of Beijing Municipality 民法院 Municipality Yanqing County People’s 延庆县人民法院 京 0229 110229 Yanqing County 1 Court No. 2 Intermediate People's 北京市第二中级 京 02 2 Court of Beijing Municipality 人民法院 Dongcheng Dongcheng District People’s 北京市东城区人 京 0101 110101 District of Beijing 1 Court of Beijing Municipality 民法院 Municipality Xicheng District Xicheng District People’s 北京市西城区人 京 0102 110102 of Beijing 1 Court of Beijing Municipality 民法院 Municipality Fengtai District of Fengtai District People’s 北京市丰台区人 京 0106 110106 Beijing 1 Court of Beijing Municipality 民法院 Municipality 1 Fangshan District Fangshan District People’s 北京市房山区人 京 0111 110111 of Beijing 1 Court of Beijing Municipality 民法院 Municipality Daxing District of Daxing District People’s 北京市大兴区人 京 0115 -

2.2 Anhui Province Anhui Wanzhong Group Co., Ltd.1, Affiliated with The

2.2 Anhui Province Anhui Wanzhong Group Co., Ltd.1, affiliated with the Anhui Provincial Prison Administration Bureau, has 27 prison enterprises Legal representative of the prison company: Xu Xiaogang, Chairman of the company and Director of the Anhui Provincial Prison Administration Bureau.2 The company’s registered capital is 443.469 million yuan. Its total assets amounted to 1.5 billion yuan. Founded in December 1996, it has 19 wholly-owned subsidiaries (other information indicates that it has 27 prison enterprises) spreading out in 11 cities and counties in the province, with more than 7,000 regular workers and 47,000 prisoners. Its main products include railway sleeper fasteners, medium and low-pressure valves, automotive forgings, power accessories, textiles and garments, cement and building materials, specialty agricultural products, various types of labor processing products and hotel catering and other tertiary industry services. In 2007, the group realized an operating income of 1.44 billion yuan and a profit of 82 million yuan, and it paid taxes of 70.9 million yuan. Its total profit and taxes were 156 million yuan. No. Company Name of the Legal Person Legal Registered Business Scope Company Notes on the Prison Name Prison, to and representative / Capital Address which the Shareholder(s) Title Company Belongs 1 Anhui Anhui Anhui Xu Xiaogang 44.3469 Capital management; project 100 Qingxi The Anhui Provincial Prison Administration Province Provincial Provincial Chairman of Anhui million yuan investment, management and Road, Shushan Bureau4 is the administrative agency of the Wanzhong Prison People’s Wanzhong Group operation; material supply and District, Hefei provincial government responsible for the Group Co., Administrati Government Co., Ltd.; Director product sale related to investment City, Anhui administration of prisons throughout the province. -

Leeches Alleviates.Pdf

Leeches alleviates diabetic macroangiopathy by increasing nitric oxide production in rat aorta and restoring endothelium-dependent vasodilatation Type Research paper Keywords NO, endothelium, diabetic macroangiopathy, aorta, Leeches Abstract Introduction Diabetes mellitus (DM) is a chronic metabolic disorder characterized by elevated blood glucose level over a prolonged period, leading to severe damage in tissues including the heart, blood vessels, eyes and the kidneys. Danzhi Jiangtang Capsule (DJC) is an effective drug for diabetes, but the mechanism responsible for its efficacy remains unknown. This study aimed to explore the effective ingredient of DJC that ameliorated diabetes and the possible mechanisms. Material and methods We orally treated streptozotocin (STZ)-induced diabetic rats with 540 mg/kg DIC or the same dose of its four active components, namely Leeches, Pseudostellaria Polysaccharides (PP), Paeonia Suffruticosa Andr (PSA) and Rehmannia Glutinosa Libosch (RGL), respectively for 8 weeks. Results Although all of these components could reduce blood glucose levels in diabetic rats, the extent of alleviation of DJC was more pronounced than all of its four ingredients. Unlike the other three components, Leeches is the only effective ingredient of DJC that decreased tetrahydrobiopterin (BH4) oxidation to activate endothelial nitric oxide synthase (eNOS), and increased nitric oxide (NO) production, leading to improvedPreprint endothelium-dependent relaxation both in diabetic rats and in immortalized human mesangial cells under