LEO Year 1 Plug-In Projects Review

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Pupil Place Plan 2019-2023

Oxfordshire County Council Pupil Place Plan 2019-2023 November 2019 For 2019/20, the DfE has approved a change in primary school planning areas for Oxfordshire. Several of the previous planning areas have been subdivided into smaller areas, to support more detailed planning. This Pupil Place Plan is structured according to the larger areas – e.g. “Abingdon” – but comments have been made relating to the smaller sub-areas – e.g. “Abingdon East” – where appropriate. Pupil forecasts at sub-area level have been provided in the Annex. The list of schools starting on page 43 indicates which planning area each is in. The detailed data section starting on page 53 also indicates which planning area each is in, where this is relevant. Contents 1. INTRODUCTION .................................................................................................. 3 2. SCHOOL ORGANISATION CONTEXT ................................................................ 4 2.1 Oxfordshire’s education providers ...................................................................... 4 Early education ............................................................................................. 4 Primary education ......................................................................................... 4 Secondary education .................................................................................... 5 Specialist education ...................................................................................... 5 School planning areas .................................................................................. -

Artweeks 10.2.Pages

saturday 8 - monday 31 may 2010 free guide www.artweeks.org Sponsored by Welcome to Artweeks 2010 2010 is set to be the biggest Artweeks ever with 474 sites exhibiting during the Festival. Artweeks plays a vital role in bringing artists and art enthusiasts and buyers together across the county. Our goal this year is to bring new audiences to the work of Oxfordshire's creative community, those who might find the idea of going to a gallery daunting. By visiting an open studio and talking to the artist you get to understand the creative process, the way they have tried to convey their ideas and the effect they have created. Most of the works on view are for sale and you'll find some originals at prices that you might pay for a mass-produced copy in a quality department store. Artweeks is all about involvement and originality; by simply going along to a couple of studios and seeing what is on offer, you too add to the vibrancy of Oxfordshire's biggest arts festival. See it. Love it. Buy it. Nick Thorn Chair, Oxfordshire Artweeks Key to abbreviations and symbols in this guide W wheelchair access OPC Oxford Printmakers Co-op PW partial wheelchair access OCG Oxfordshire Craft Guild F family friendly OAS Oxford Art Society 2 T teas WOA West Oxfordshire Arts D demonstrations Contents Artweeks Office Special Events 7 PO Box 559, Abingdon, Oxon, OX14 9EF Children’s Workshops 11 Tel 01865 865596 [email protected] Oxford City 19 www.artweeks.org Sat 8 May - Sun 16 May The office is open Monday, Oxford City 20 Wednesday and Friday, 9.30-2.30. -

2018 PPP FINAL COMPLETE , Item 120

Oxfordshire County Council Pupil Place Plan 2018-2022 November 2018 Contents 1. INTRODUCTION .................................................................................................. 3 2. SCHOOL ORGANISATION CONTEXT ................................................................ 4 2.1 Oxfordshire’s education providers ...................................................................... 4 Early education ............................................................................................. 4 Primary education ......................................................................................... 4 Secondary education .................................................................................... 5 Specialist education ...................................................................................... 5 2.2 Policies and legislation ....................................................................................... 6 Early education and childcare sufficiency ..................................................... 6 School places - local authorities’ statutory duties .......................................... 7 Policy on spare school places ....................................................................... 7 Special Educational Needs & Disabilities (SEND)......................................... 8 Academies in Oxfordshire ............................................................................. 9 Oxfordshire Education Strategy .................................................................. 10 2.3 -

Preferences Met for Oxfordshire Secondary Schools on 1 March 2021

ALLOCATION TO START SECONDARY SCHOOL IN SEPTEMBER 2021 - DETAILS FOR EACH OXFORDSHIRE SCHOOL e) ) ) ) bl s n n ) ) al ) ) n i n)o xo ) xo n n on ion xo x va at ti O ) n O xo ) xo ) a ci n O n l ca de n xo dei O ) O ) e O p li n xo de xo d tsi xo O st de ide i on O i aces ap pp u O u si xo O s ts x ts l a de o t t u p o si uo O de u ide r ide t o e O s ou or te s u sit o id t ( d as rom t o rom ide s u r te af f u st u om t om o f rom o rom r o be ea n n om f u f f fr r re r n o ou m t dl om f e om rom u s i r n ldren r r f draw f e i d om f dren ldren omr ldren fer h ch ri li r n il i f n N f it ( ld (ch f e hi s) o o w s d ch r ch (ch dren (c i ( re s ldren d ( ld ( li on ion i s d n i ch ri e s i s dren d ti iss LA s d s io ( ldren d l ch n re at l qu ion ire t ch s u n i ch re on hi ( ire ica m g io c sr e s ( io ( i ti u d in t s ui li sa r at l qu cai s al eq t ch s u (c ls pl ency A p e u t c sr er t r ( ca ) ca s al req f f li sa pl er us ca s al eq i rs sa eq ap tu ud i ap of e p e u t f i r e u t r ti d cl pl erf us t r no f f ap ref no pl erf us t pl f f s ee ni p f ef o ap of e ef e ns r ( ce ce ce ce r no e e of e e ape r no ap r no d a o g s rs e e a e o e r e n n n n n e of e e e e of e e e a ef e e e e ce ce ce ce nc nc nc nc t r f s bl nc nc nc nc er er er er n n n n re re re re nc nc nc nc nc nc nc nc y C o ion la er er er e e e e e e e e e e e e e re er er er rea ( t l o al i r ef ef ef ef er er er er f f f f r r r r t( ar d ef ef ef e er er er e ef ef ef e e e e e nt ica al us va f ef ef ef ef r f ef ef ef ef s e l -

Adderbury and Milton

1 Foreword Welcome! A warm welcome to this beautiful part of Oxfordshire! We are delighted to present this Welcome to the Benefice of Adderbury with Milton, which comprises St Mary the Virgin, profile for the post of Vicar of this benefice. You will see that there is plenty going on in Adderbury and its daughter church, St John the Evangelist, in the adjacent village of these communities, with opportunities to build on all the good work that has been Milton. John Betjeman described Adderbury as a ‘large hilly village of golden ironstone achieved and to find new ways to serve in Christ’s name. houses and old cottages with a magnificent decorated and perpendicular church to There is a real energy and willingness to experience a fresh approach to worship and match.’ outreach here, particularly in relation to children, young people and families. Developing The clusters of honey-coloured ironstone cottages within Adderbury are the stuff of a fruitful relationship with the school will be a key part of this, as will growing a picture postcards and, together with the parish church with its impressive steeple, collaborative team and encouraging the gifts and ministries of lay people. Having said provide echoes of a history that can be traced back over 1000 years. Adderbury has over that, there is a commitment to good (but creative) liturgy and to the needs of those who 100 listed buildings, but only the church is Grade I listed. The Parish has an attractive prefer a traditional approach. The new Vicar is likely to be the kind of person who can rural environment, featuring a village green, playing fields, lakes (designed by Capability hold these together creatively, pastorally, imaginatively and prayerfully. -

A B C D = A+B+C

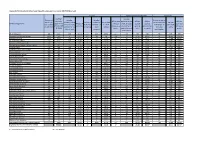

SEN High Needs Top Up - Secondary Schools - 2019-20 The top up amounts below will be paid to Secondary Academies from 1 September 2019 to 31 August 2020. The top up elements for maintained Secondary schools will be paid from 1 April 2019 to 31 March 2020. Per Pupil Unit Rates £17.36 £199.50 £84.55 LCHI SEN Basic (Prior High Needs Payable in Payable in Deprivation LCHI SEN Entitlement Deprivation Attainment) Top up 2018- 2019-20 2020-21 LAEstab DfE School Name NOR units (FSM%) units element element element 19 Financial Year Financial Year Academy? Low Attainment Secondary FSM Secondary NOR units Units A B C D = A+B+C 9314041 4041 Carterton Community College 540 50 157.42 £9,373 £9,975 £13,310 £32,658 £32,658 £0 A 9314000 4000 Wykham Park Academy 775 122 198.55 £13,452 £24,338 £16,788 £54,578 £31,837 £22,741 A 9314004 4004 Aureus Secondary 433 61 112.20 £7,514 £12,221 £9,487 £29,223 £17,047 £12,176 A 9314006 4006 Space Studio Banbury 43 6 9.92 £746 £1,197 £839 £2,782 £1,623 £1,159 A 9314007 4007 The Warriner School 1,176 59 234.22 £20,413 £11,770 £19,803 £51,986 £30,325 £21,661 A 9314008 4008 UTC Oxfordshire 224 15 52.50 £3,888 £2,992 £4,439 £11,319 £6,603 £4,716 A 9314010 4010 Chipping Norton School 789 55 131.54 £13,695 £10,972 £11,122 £35,789 £20,877 £14,912 A 9314011 4011 The Bicester School 904 61 193.25 £15,691 £12,169 £16,340 £44,200 £25,783 £18,417 A 9314012 4012 Bicester Technology Studio 77 7 22.65 £1,337 £1,396 £1,915 £4,648 £2,711 £1,937 A 9314013 4013 Maiden Erlegh Chiltern Edge 366 32 104.78 £6,353 £6,384 £8,859 £21,596 £12,597 -

School Name POSTCODE AUCL Eligible If Taken GCSE's at This

School Name POSTCODE AUCL Eligible if taken GCSE's at this AUCL Eligible if taken A-levels at school this school City of London School for Girls EC2Y 8BB No No City of London School EC4V 3AL No No Haverstock School NW3 2BQ Yes Yes Parliament Hill School NW5 1RL No Yes Regent High School NW1 1RX Yes Yes Hampstead School NW2 3RT Yes Yes Acland Burghley School NW5 1UJ No Yes The Camden School for Girls NW5 2DB No No Maria Fidelis Catholic School FCJ NW1 1LY Yes Yes William Ellis School NW5 1RN Yes Yes La Sainte Union Catholic Secondary NW5 1RP No Yes School St Margaret's School NW3 7SR No No University College School NW3 6XH No No North Bridge House Senior School NW3 5UD No No South Hampstead High School NW3 5SS No No Fine Arts College NW3 4YD No No Camden Centre for Learning (CCfL) NW1 8DP Yes No Special School Swiss Cottage School - Development NW8 6HX No No & Research Centre Saint Mary Magdalene Church of SE18 5PW No No England All Through School Eltham Hill School SE9 5EE No Yes Plumstead Manor School SE18 1QF Yes Yes Thomas Tallis School SE3 9PX No Yes The John Roan School SE3 7QR Yes Yes St Ursula's Convent School SE10 8HN No No Riverston School SE12 8UF No No Colfe's School SE12 8AW No No Moatbridge School SE9 5LX Yes No Haggerston School E2 8LS Yes Yes Stoke Newington School and Sixth N16 9EX No No Form Our Lady's Catholic High School N16 5AF No Yes The Urswick School - A Church of E9 6NR Yes Yes England Secondary School Cardinal Pole Catholic School E9 6LG No No Yesodey Hatorah School N16 5AE No No Bnois Jerusalem Girls School N16 -

Annex 8 – Academy Trusts Consolidated Into SARA 2018/19 This Annex Lists All Ats Consolidated Into SARA 2018/19, with Their Constituent Academies

Annex 8 – Academy Trusts consolidated into SARA 2018/19 This annex lists all ATs consolidated into SARA 2018/19, with their constituent Academies. * These Academies transferred into the AT from another AT during the year. ** Newly opened or converted to academy status during 2018/19. ^ These Academies transferred out of the AT into another AT during the year. + Closed during the year to 31 August 2019. ++ Closed prior to 31 August 2018. +++ ATs where the Academies had all transferred out over the course of 2018/19. # City Technology colleges (CTC) are included in the SARA consolidation, but do not appear in Annex 1 – Sector Development Data. Further details can be found at www.companieshouse.gov.uk by searching on the company number. -

Contextual Data Education Indicators: 2020 Cycle

Contextual Data Education Indicators: 2020 Cycle Schools are listed in alphabetical order. You can use CTRL + F/ Level 2: GCSE or equivalent level qualifications Command + F to search for Level 3: A Level or equivalent level qualifications your school or college. Notes: 1. The education indicators are based on a combination of three years' of school performance data, where available, and combined using z-score methodology. For further information on this please follow the link below. 2. 'Yes' in the Level 2 or Level 3 column means that a candidate from this school, studying at this level, meets the criteria for an education indicator. 3. 'No' in the Level 2 or Level 3 column means that a candidate from this school, studying at this level, does not meet the criteria for an education indicator. 4. 'N/A' indicates that there is no reliable data available for this school for this particular level of study. All independent schools are also flagged as N/A due to the lack of reliable data available. 5. Contextual data is only applicable for schools in England, Scotland, Wales and Northern Ireland meaning only schools from these countries will appear in this list. If your school does not appear please contact [email protected]. For full information on contextual data and how it is used please refer to our website www.manchester.ac.uk/contextualdata or contact [email protected]. Level 2 Education Level 3 Education School Name Address 1 Address 2 Post Code Indicator Indicator 16-19 Abingdon Wootton Road Abingdon-on-Thames -

Oxfordshire County Council's Information for Parents and Carers of Children Due to Transfer to Secondary School in September 2020

Oxfordshire County Council’s information for parents and carers of children due to transfer to secondary school in September 2020 Apply online at www.oxfordshire.gov.uk/ secondaryadmissions Deadline for applications: 31 October 2019 Apply on-line www.oxfordshire.gov.uk/secondaryadmissions Apply online at: www.oxfordshire.gov.uk/secondaryadmissions Contents Introduction ............................................................................................................................ 1 Key Dates .............................................................................................................................. 2 Section 1 – Application Process............................................................................................. 3 Applying ............................................................................................................................. 3 Applying on-time ................................................................................................................. 3 Preferences ........................................................................................................................ 3 Applying for a place at a school in England but outside Oxfordshire .................................. 4 Applying for a place at a school in Northern Ireland, Scotland or Wales ............................ 4 Supplementary Information Forms (SIFs) .......................................................................... 4 Applying late ...................................................................................................................... -

Appendix B: a Level and Other Level 3 Qualifications Per Institution 2017/18 (Revised)

Appendix B: A level and other level 3 qualifications per institution 2017/18 (revised) A levels Applied general qualification Tech level Number Number Number of Number Number Number at end of students APS in best students at end APS per APS per APS per 16-18 year students at end APS per A students in APS in best 16-18 study who APS per School/college name aged 16-18 APS per A 3 A level of 16-18 study applied applied tech level old students of 16-18 study level entry the best 3 A 3 A level entered for 1+ tech level at end of 16- level entry entries as a entered for 1+ general general entry entry as a in sixth form entered for 1+ as a grade levels entries tech level entry 18 study grade applied general entry as a grade grade AS or A level measure qualification qualification 16-19 Abingdon 283 142 138 31.92 C+ 117 33.62 C+ NE NE NE NE NE NE Abingdon and Witney College 1634 931 3 SUPP SUPP NE NE NE 74 27.60 Merit+ 65 26.63 Merit Activate Learning 5515 2720 131 25.23 C- 71 27.14 C- 18 16.75 Pass+ 34 21.68 Merit- Bartholomew School 242 119 114 32.28 C+ 88 33.52 C+ 12 32.78 Dist- 3 SUPP SUPP Bicester Technology Studio 40 29 15 4.84 U 7 3.33 U 17 22.69 Merit- 4 SUPP SUPP Blessed George Napier Catholic School 165 86 74 31.36 C 69 29.32 C 2 SUPP SUPP NE NE NE Burford School 232 109 108 31.69 C+ 83 34.78 C+ 6 32.50 Dist- 10 24.00 Merit Carterton Community College 56 35 27 19.55 D 16 18.13 D- 6 18.33 Pass+ NE NE NE Cheney School 238 125 107 31.33 C 76 31.84 C+ 16 20.11 Merit- NE NE NE Chipping Norton School 155 89 87 30.08 C 62 34.14 C+ 3 SUPP SUPP -

North LCSS Link Workers

Locality and Community Support Service North Link Workers This is the list of schools in North Oxfordshire, to find your school please press Ctrl and F which will enable the search box, please use this to locate your school and your link worker. For any further support please contact the team: Team Line: 0345 241 2703 Team Email: [email protected] Page 1 of 16 Assistant Team Managers: Jo Lloyd 07584 581180 Senior Practitioner: Pippa Sinclair 0776 997958 [email protected] Updated May 2019 Locality and Community Support Service Banbury Area Office Line: 0345 241 2703 Link LCSS Workers: Amy Beasley – 07917 534203 (until 30/09/19) Cary Johnston - 07827 947300 Allocated Schools Nurseries/Pre schools Banbury Campus (Banbury and Bicester College) A Plus Tuition Ltd Bishop Carpenter CofE Primary School Adderbury Day Nursery Bishop Loveday CofE Primary School Banbury and District Community Bus Project (Creche) Blessed George Napier Catholic School Banbury School Day Nursery Ltd Bloxham CofE Primary School Bloxham Pre-School Bloxham School (Private) Castle Pre-School (Banbury) Chipping Norton School Chasewell Playgroup Christopher Rawlins CofE Primary School Cherry Tree - Bloxham Cropredy CofE Primary School Child First - Banbury Dashwood Banbury Academy Childcare Day Nursery (The Sunshine Centre) Deddington Primary School Chipping Norton Pre-school Great Rollright CE (Aided) Primary Christopher Rawlins Nursery Class EMBS College Banbury Cropredy Pre-school Hanwell Fields Community School Dashwood Banbury Academy