Automotive NEUTRAL ↔

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

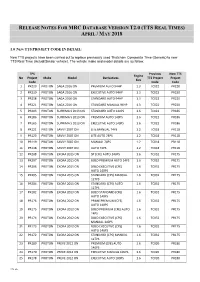

Release Notes for Mrc Database Version T2.0 (Tts Real Times) April / May 2018

RELEASE NOTES FOR MRC DATABASE VERSION T2.0 (TTS REAL TIMES) APRIL / MAY 2018 1.0 NEW TTS PROJECT CODE IN DETAIL: New TTS projects have been carried out to replace previously used Thatcham Composite Time (Generic) to new TTS Real Time (Actual/Similar vehicle). The vehicle make and model details are as follow: TPS Previous New TTS Engine No Project Make Model Derivatives TTS Project Project Size Code Code Code 1 PR220 PROTON SAGA 2016 ON PREMIUM AUTO 94HP 1.3 TC022 PR220 2 PR219 PROTON SAGA 2016 ON EXECUTIVE AUTO 94HP 1.3 TC022 PR220 3 PR218 PROTON SAGA 2016 ON STANDARD AUTO 94HP 1.3 TC022 PR220 4 PR221 PROTON SAGA 2016 ON STANDARD MANUAL 94HP 1.3 TC022 PR220 5 PR203 PROTON SUPRIMA S 2013 ON STANDARD AUTO 140PS 1.6 TC022 PR186 6 PR186 PROTON SUPRIMA S 2013 ON PREMIUM AUTO 140PS 1.6 TC022 PR186 7 PR165 PROTON SUPRIMA S 2013 ON EXECUTIVE AUTO 140PS 1.6 TC022 PR186 8 PR121 PROTON SAVVY 2007 ON LITE MANUAL 74PS 1.2 TC018 PR118 9 PR120 PROTON SAVVY 2007 ON LITE AUTO 74PS 1.2 TC018 PR118 10 PR119 PROTON SAVVY 2007 ON MANUAL 74PS 1.2 TC018 PR118 11 PR118 PROTON SAVVY 2007 ON AUTO 74PS 1.2 TC018 PR118 12 PR208 PROTON EXORA 2015 ON SP (CFE) AUTO 140PS 1.6 TC032 PR175 13 PR207 PROTON EXORA 2015 ON BOLD PREMIUM AUTO 14PS 1.6 TC032 PR175 14 PR206 PROTON EXORA 2015 ON BOLD EXECUTIVE (CFE) 1.6 TC032 PR175 AUTO 140PS 15 PR205 PROTON EXORA 2015 ON STANDARD (CPS) MANUAL 1.6 TC032 PR175 127PS 16 PR204 PROTON EXORA 2015 ON STANDARD (CPS) AUTO 1.6 TC032 PR175 127PS 17 PR182 PROTON EXORA 2013 ON BOLD STANDARD (CFE) 1.6 TC032 PR175 AUTO 140PS 18 PR176 PROTON -

I the RELATIONSHIP BETWEEN CUSTOMER SATISFACTION, BRAND IMAGE and CUSTOMER LOYALTY from the PERSPECTIVE of PROTON's CUSTOMERS

i THE RELATIONSHIP BETWEEN CUSTOMER SATISFACTION, BRAND IMAGE AND CUSTOMER LOYALTY FROM THE PERSPECTIVE OF PROTON’S CUSTOMERS Yeoh Hooi Chin (VIVIAN) A thesis submitted in fulfillment of the requirement for the award of the degree of Master of Management (Technology) Faculty of Management and Human Resources Development Universiti Teknologi Malaysia APRIL 2010 iii To my beloved parents, Sister & Friends, Thanks for your support…. iv ACKNOWLEDGEMENT First of all, I would like to take this opportunity to express my gratitude to my supervisor Mr Ahmad Jusoh and FPPSM’s lecturers for giving me the guidelines needed to make this project a reality. Without the guidelines given, I would not have completed my report as smoothly as I plan to. I would also like to express my gratitude to all the employees of 3S Platinum Sales and Service Centre whose were kind enough to help me distributed my survey form to their customers during working hours. Special thanks are due to my friends who had providing me encouragement, motivation and support, either directly or indirectly. Finally, I wish to acknowledge my parents with great respect. Their love, encouragement, support and sacrificed giving themselves have been exemplary, who have been always concerning my education and giving me various supports in succeeding this research. v ABSTRACT The objective of this study was determine the relationship between the customer satisfaction (perceived product quality, perceived service quality and perceived price fairness) and customer loyalty in order to identify whether perceived product quality, perceived service quality and perceived price fairness have any significance effect on the loyalty of customer. -

Get Away to Discover the Secret

EARLY BIRD TOUR Organizes from local (Kuching) holidays to BOOKING! adventures tours, Eco to Agro-tourism. We also caters to specialized incentive trips BOOK NOW BEFORE in the state of Sabah and also other parts of fascinating Malaysia. 24th JUNE 2013 Air Tickets & Hotel Reservation KUCHING HOLIDAYS & You can book your air ticket through us for CAR RENTAL SDN.BHD. both national and international travel and also book your hotel rooms from budget to 5 star luxury resort in Kuching and other parts About Kuching of Malaysia. Kuching is the Capital of East Malaysia State of Sarawak. Being the most popular city in the of Sarawak. Kuching Car Rental emerged as on of the most vibrant cities Provides a variety of vehicles to suite everyone in the region and it is the lagest city on budget and purposes to book a budget car, the island of Borneo and the fourth luxury limousine, minivan, coaches, chauffeur largest city in Malaysia. Kuching was service or self-drive. We rent cars with excel- elevated to city status on 1st August 1988 lent performances at affordable prices and all and carries the nick name of CAT CITY. are equipped with air-conditioning and CD player facilities. PLEASE VISIT US AT : www.kuchingholidays.com Email : [email protected] Tel : +6082 422955 / +6016 822 8222 KUCHING HOLIDAYS & CAR RENTAL SDN. BHD. Get away to Company No: 820168-D KPL/LN: 5526 Sarawak Tourism Complex (Old Court House), Block D1, discover the secret Jalan Tun Abang Haji Openg, 93000 Kuching, Sarawak. GUNUNG GADING N.PARK “Things to do in Kuching “ Wildlife & Adventure Marine Wildlife KUCHING CITY TOUR (3 HRS) RM 80 RM 65 RM 520 This tour will take you around the city making SEMENGGOH WILDLIFE CENTRE (3 HRS) SATANG—TALANG ISLAND (2D1N) stops at places of interests including the famous Cat Statue A shelter for semi wild ‘Orang Utan’ who has been Satang Island is one of the two islands set aside by Gov- of the city, the oldest Chinese Temple, Old Town of rescued from captivity and trained to survive in the wild. -

LH & RH) Chrome Inner Door Handle (4Pcs/Set

85 (ADVANCE) Air-Cond Panel Switch PROTON EXORA Fog Lamp Panel Switch PROTON EXORA Door Mirror (LH & RH) Led Door Mirror (LH & RH) TOYOTA FORTUNER / HILUX PROTON PERSONA ELEGANCE * 7 wire Upgrade PERSONA “OLD” & GEN.2 Safety Belt (Rear) Security Alarm System Auto Adjustable with Motor System TOYOTA * LH. RH, Center Fog Lamp (LH & RH) Car Audio PROTON PREVE PROTON PREVE with GPS Chrome Inner Door Handle (4pcs/set) Chrome Fog Lamp Rim (LH & RH) PROTON PERSONA / EXORA PROTON EXORA © Copyright 2006 YAC AUTO (M) Sdn. Bhd. All Rights Reserved. 86 Fog Lamp (LH & RH) Fog Lamp (LH & RH) M.TRITON '09 / PROTON INSPIRA PROTON EXORA “campaign ” Chrome Front Garnish PROTON EXORA FL 'BOLD' Reverse Sensor (Colour) PROTON EXORA “campaign ” Air Scoop (w/out Paint) TOYOTA HILUX Aluminium Loading Sill PROTON EXORA/PERODUA MYVI/PERODUA ALZA YC1990 Lower Tie Frame Bar (Beaks Bar) PROTON - WIRA/WAJA/GEN.2/PERSONA PROTON - SATRIA/SATRIA NEO Blue | Gold | Red | Silver Polishing 15” Wheel Cover Door Handle Cover (4pcs/set) Silver | Titanium PEROUDA MYVI '2011 IS200 YC2947 © Copyright 2006 YAC AUTO (M) Sdn. Bhd. All Rights Reserved. 87 Head Lamp Lid Cover (2pcs/set) Head Lamp Lid Cover (2pcs/set) PERODUA MYVI '2011 PROTON EXORA Chrome | Black | Silver | White | Grey | Yellow | Chrome | Black | Silver | White | Elegance Brown | Purple | Orange | Carbon Fiber Carbon Fiber YC2987 YC3787 Tail Lamp Cover (2pcs/set) Ultra Car Seat Mat PERODUA MYVI '2011 Chrome | Black | Silver | White | Grey | Yellow | Purple | Orange | Carbon Fiber YC2997 Aluminium Loading Si (LH & RH) PROTON EXORA YC1990 Emergency Led Lid with Magnet * 36cm x 31.5cm © Copyright 2006 YAC AUTO (M) Sdn. -

S/N Model Dimensions (L X W X H

S/N Model Dimensions (L x W x H) L5200xW2150xH2100 1 Alfa Romeo 147 4223 x 1729 x 1421 Y 2 Alfa Romeo 159 4660 x 1828 x 1417 Y 3 Alfa Romeo 159 Sportwagon 4660 x 1828 x 1417 Y 4 Alfa Romeo Brera 4416 x 1830 x 1372 Y 5 Alfa Romeo GT 4489 x 1763 x 1355 Y 6 Alfa Romeo Spider 4396 x 1830 x 1318 Y 7 Aston Martin DB9 4710 x 1875 x 1270 Y 8 Aston Martin DBS 4721 x 1905 x 1280 Y 9 Aston Martin V8 Vantage - Coupe 4380 x 1865 x 1265 Y 10 Aston Martin V8 Vantage - Roadster 4380 x 1865 x 1255 Y 11 Audi 12-cylinder A8 (A8 W12 L) 5192 x 1894 x 1455 Y 12 Audi 12-cylinder A8 (A8 W12) 5062 x 1894 x 1424 Y 13 Audi 4 Saloon 4703 x 1826 x 1427 Y 14 Audi A3 Sportback 4292 x 1765 x 1423 Y 15 Audi A4 Cabriolet 4573 x 1777 x 1391 Y 16 Audi A5 4625 x 1854 x 1372 Y 17 Audi A6 4927 x 1855 x 1459 Y 18 Audi A6 Avant 4927 x 1855 x 1463 Y 19 Audi A8 5062 x 1894 x 1444 Y 20 Audi A8 L 5192 x 1894 x 1455 Y 21 Audi Q7 5086 x 1983 x 1737 Y 22 Audi R8 4178 x 1904 x 1249 Y 23 Audi S3 4230 x 1765 x 1399 Y 24 Audi S5 4635 x 1854 x 1369 Y 25 Audi S8 5062 x 1894 x 1424 Y 26 Audi The TT Coupe 4178 x 1842 x 1352 Y 27 Audi The TT Roadster 4178 x 1842 x 1358 Y 28 Audi TTS Coupe 4198 x 1842 x 1345 Y 29 Bentley Arnage - 6.8 R 5390 x 1900 x 1515 N 30 Bentley Arnage - 6.8 RL 5640 x 1900 x 1515 N 31 Bentley Arnage - 6.8 T 5400 x 1900 x 1515 N 32 Bentley Azure 5410 x 1900 x 1492 N 33 Bentley Contiental GT 4804 x 1965 x 1390 N 34 Bentley Continental Flying Spur 5290 x 1976 x 1475 N 35 BMW 1 Series 4329 x 1934 x 1421 Y 36 BMW 1 Series Convertible 4329 x 1934 x 1421 Y 37 BMW 1 Series Coupe -

Prices Issued by Car Dealers As of 31 August 2020

PASSENGER MOTOR VEHICLES (PMV) PRICES ISSUED BY CAR DEALERS AS OF 31ST AUGUST 2020 Prices on the JPES website are every 2 weeks. For the most up-to-date prices, please download the PenggunaBijak mobile app SER SHOWROOM PRICE ON-THE-ROAD PRICE PMV MODEL & BRAND DESCRIPTION DATE ISSUED No. (SRP) (OTR) 1.00 ALFA ROMEO (G.H.K. MOTORS SDN BHD) 1.01 ALFA ROMEO GIULIA 620 GME 2.0L AUTO SEDAN PETROL $ 63,900.00 $ 65,800.00 17-Jul-20 1.02 ALFA ROMEO GIULIA 620 QV V6 2.9L AUTO SEDAN PETROL $ 139,973.00 $ 144,094.00 17-Jul-20 1.03 ALFA ROMEO GIULIA VELOCE 620 2.0L AUTO GME 2000 SEDAN PETROL $ 72,700.00 $ 74,800.00 17-Jul-20 1.04 ALFA ROMEO STELVIO 2.0L AUTO AWD SUV PETROL $ 75,500.00 $ 77,800.00 17-Jul-20 2.00 AUDI (T.C.Y. MOTORS SDN BHD) 2.01 AUDI A4 2.0L TFSI ULTRA QUATTRO S-TRONIC AUTO SEDAN PETROL $ 74,440.00 $ 76,448.00 16-Jul-20 2.02 AUDI A6 1.8L TFSI S-TRONIC S-LINE AUTO PETROL $ 72,570.00 $ 74,533.00 16-Jul-20 2.03 AUDI A3 1.2L S-LINE TFSI S-TRONIC AUTO SPORTBACK PETROL $ 52,600.00 $ 54,100.00 16-Jul-20 2.04 AUDI A3 1.2L TFSI S-TRONIC AUTO SEDAN PETROL $ 44,530.00 $ 45,847.00 16-Jul-20 2.05 AUDI A3 1.2L TFSI S-TRONIC AUTO SPORTBACK PETROL $ 49,350.00 $ 50,769.00 16-Jul-20 2.06 AUDI A4 2.0L TFSI ULTRA S-TRONIC AUTO S-LINE BLACK STYLING SEDAN PETROL $ 73,130.00 $ 75,117.00 16-Jul-20 2.07 AUDI A5 2.0L TFSI QUATTRO S-TRONIC AUTO COUPE PETROL $ 83,310.00 $ 85,501.00 16-Jul-20 2.08 AUDI A6 2.0L TFSI S-TRONIC AUTO SEDAN PETROL $ 78,790.00 $ 80,879.00 16-Jul-20 2.09 AUDI A6 3.0L TFSI QUATTRO S-TRONIC AUTO SEDAN PETROL $ 109,930.00 $ 112,716.00 16-Jul-20 -

Proton Persona-Iriz

PROTON PERSONA/IRIZ Variant Year Built PROTON PERSONA TESTED DECEMBER 2020 STANDARD 2020 Vehicle Model Year Category 2020 SEDAN Engine Capacity Kerb Mass 1.6 L 1170 kg No. of Airbags Test Lab 4 TESTED VARIANT ORIGIN MALAYSIA FOR MALAYSIA OTHER ASEAN PRODUCTION – FOR – (ALL VARIANTS) FRONTAL IMPACT SIDE IMPACT HEAD PROTECTION TOTAL TECHNOLOGY 14.63 15.68 2.00 32.31 FRONTAL IMPACT SIDE IMPACT DRIVER PASSENGER No Modifier No Modifier The vehicle compartment remained During the side impact test, the driver stable during the frontal offset test. Data obtained adeduate protection to the from the test showed the driver received chest. adequate protection to the chest and both dummies sustained injuries to each of their lower legs. SAFETY ITEMS (PASSIVE) ITEMS COUNTRIES Driver NS NS NS NS S NS NS NS NS NS Passenger NS NS NS NS S NS NS NS NS NS Airbags Side (2) NS NS NS NS S NS NS NS NS NS Curtain (2) NS NS NS NS O NS NS NS NS NS Knee NS NS NS NS X NS NS NS NS NS Retractor Pre-tensioner & NS NS NS NS S NS NS NS NS NS Load Limiter for Driver Seatbelts Retractor Pre-tensioner & NS NS NS NS S NS NS NS NS NS Load Limiter for Passenger S : Standard on all variants, O : Optional on base; Standard on higher variants, X : Not available, TBA : To be advised, NS : Not sold DYNAMIC TEST VEHICLE BASED INSTALLATION TOTAL 23.20 8.00 11.72 42.92 DYNAMIC TEST ASSESSMENT 18-MONTH-OLD CHILD 3-YEAR-OLD CHILD Restraint : Britax Baby Safe Plus Restraint : Britax Duo Plus Facing : Rearward Facing Facing : Forward Facing Installation : ISOFIX & Supportleg Installation -

News Release

Perusahaan Otomobil Nasional Sdn Bhd (100995-U) Persiaran Kuala Selangor, Seksyen 26, 40400 Shah Alam Selangor Darul Ehsan, Malaysia. T (+603) 5102 6000 F (+603) 5191 9120 News Release PROTON INTRODUCES THE NEW 2022 IRIZ AND PERSONA • Both models get new features and refreshed styling with new colour options • 2022 Proton Iriz debuts new Active variant Subang Jaya, 5 August 2021 – PROTON today announced the launch of the new 2022 Proton Iriz and Persona, offering updated design elements plus enhanced features. The latest additions to the company’s range also come in new colours, while offering improved comfort and safety for all passengers. “The Proton Iriz and Persona have won many fans since their introduction, so we took a measured approach to updating them. The styling changes and addition of a new Active variant for the Proton Iriz will help boost their visual appeal while the changes we have made to the interior and infotainment system ensures they deliver better comfort and connectivity while retaining Proton’s trademark driving experience,” said Roslan Abdullah, Chief Executive Officer, Proton Edar. Updated design to appeal to a wider audience For the exterior, the changes begin with newly redesigned bumpers and the iconic Infinite Weave with Ethereal Bow grille. On the Proton Iriz, it features a new profile and is presented in red whilst the Proton Persona comes with additional chrome to better frame the new PROTON logo. The updated look for the 2022 models also includes LED headlamps that support auto on/off and follow me home functions. The design is complemented by new 16-inch alloy wheels, a black roof finish and new finishing on the rear combination lamps. -

Approval Car Price Issued As of 30Th September 2019

APPROVAL CAR PRICE ISSUED AS OF 30TH SEPTEMBER 2019 DATE SHOWROOM PASSENGER MOTOR VEHICLES BRAND PASSENGER MOTOR VEHICLES MODEL /TYPE DATE ISSUED PRICE (SRP) EFFECTIVE EXPIRY ALFA ROMEO ALFA ROMEO GIULIA 620 QV V6 (G.H.K MOTORS SDN BHD) ALFA ROMEO GIULIA 620 QV V6 2.9L AUTO SEDAN PETROL 27-May-19 21-Apr-19 20-Apr-20 $139,973.00 ALFA ROMEO GIULIA 620 GME ALFA ROMEO GIULIA 620 GME 2.0L AUTO SEDAN PETROL 27-May-19 21-Apr-19 20-Apr-20 $63,353.00 ALFA ROMEO VELOCE 620 2.0L GME 2000 ALFA ROMEO GIULIA VELOCE 620 2.0L AUTO GME 2000 SEDAN PETROL 27/0/2019 3-Jun-19 2-Jun-20 $69,666.00 AUDI AUDI A3 TFSI S-TRONIC (T. C. Y. MOTORS SDN BHD) AUDI A3 1.2L TFSI S-TRONIC AUTO SEDAN PETROL 22-Jan-19 31-Dec-18 30-Dec-19 $43,631.00 AUDI A3 TFSI S-TRONIC SPORTBACK AUDI A3 1.2L TFSI S-TRONIC AUTO SPORTBACK PETROL 7-Sep-19 11-Sep-19 10-Sep-20 $46,803.00 AUDI A4 TFSI S-TRONIC BLACK EDITION AUDI A4 2.0L TFSI S-TRONIC AUTO SEDAN PETROL - BLACK EDITION 19-Jun-19 3-Jun-19 2-Jun-20 $55,068.00 AUDI A4 TFSI QUATTRO S-TRONIC AUDI A4 2.0L TFSI QUATTRO S-TRONIC AUTO AWD SEDAN PETROL 19-Jun-19 3-Jun-19 2-Jun-20 $67,560.00 AUDI A4 TFSI ULTRA S-TRONIC AUDI A4 2.0L TFSI ULTRA S-TRONIC AUTO S-LINE BLACK STYLING SEDAN PETROL 31-Dec-18 31-Dec-18 30-Dec-19 $58,515.00 (MODEL CODE: 8W2BDG) AUDI A4 TFSI ULTRA QUATTRO S-TRONIC AUDI A4 2.0L TFSI ULTRA QUATTRO AWD S-TRONIC AUTO SEDAN PETROL 25-Feb-19 11-Feb-19 10-Feb-20 $68,676.00 AUDI A5 TFSI QUATTRO S-TRONIC COUPE AUDI A5 2.0L TFSI QUATTRO S-TRONIC AUTO COUPE PETROL 13-Aug-19 14-Aug-19 13-Aug-20 $79,952.00 AUDI A5 TFSI QUATTRO S-TRONIC -

PROCLAMATION of SALE MOTOR VEHICLES for Sale by Public Auction on Thursday, 25Th October 2018 @ 2.30 P.M Venue : Unit No

PROCLAMATION OF SALE MOTOR VEHICLES For Sale By Public Auction On Thursday, 25th October 2018 @ 2.30 p.m Venue : Unit No. 6 (B-0-6), Ground Floor, Block B Megan Avenue II, No 12, Jln Yap Kwan Seng, Kuala Lumpur www.ngchanmau.com/auto "Prospect bidders may submit bids for the Auto e-Bidding via www.ngchanmau.com/auto. *Please register at least one (1) working day before auction day for registration & verification purposes". To get a digital copy of auction listings by Car Make / Model, please SMS or Whatsapp to 012-5310600. LEGAL OWNER : CIMB BANK BERHAD (13491-P) / CIMB ISLAMIC BANK BERHAD (671380-H) REGN. TRANSM RESERVE LOT REGISTRATION YEAR OF PUSPAKOM ENGINE CHASSIS MAKE & MODEL CARD REMARKS ISSION PRICE NO NO MAKE VR 1 RESULT NUMBER NUMBER (YES / NO) TYPE (RM) STORE YARD : G-MART SUNGAI SERAI - LOT 8253, BATU 11 3/4, JALAN HULU LANGAT, 43100 HULU LANGAT, SELANGOR TELEPHONE NO : (03) 9074 3815 VIEWING DATES : 19th & 22nd October 2018 (10.00 AM - 4.00 PM) C101 WA5393H PROTON SAGA 1.3 2014 NO PASSED S4PEUD8365 PL1BT3SNREB456931 M 10,000.00 C102 MAW8778 KIA SPORTAGE 2.0 2002 NO PASSED FE-213681 KNAJA553325164435 A 3,000.00 AP COPY - FORM 1,8 & JK69 ONLY, MERCEDES BENZ C103 WUK6382 2008 NO ENGINE FAILED 27298530871758 WDD2193572A134970 A 57,000.00 CLS350 3.5 NUMBER CANNOT BE VERIFIY(DIRTY) C104 W642E PERODUA MYVI 1.3 2013 NO PASSED T41A31T PM2M602S002138245 A 18,000.00 VR-1 NOT C105 NCX3711 PERODUA VIVA 1.0 2014 NO WITHDRWAN L87B72D PM2L251S002236397 A 14,200.00 DONE C106 WXT8754 PERODUA VIVA 1.0 2012 NO PASSED L19B73A PM2L251S002200453 -

PROCLAMATION of SALE MOTOR VEHICLES for Sale by Public Auction on Monday 1St April 2019 @ 2.30 P.M Venue : Unit No

PROCLAMATION OF SALE MOTOR VEHICLES For Sale By Public Auction On Monday 1st April 2019 @ 2.30 p.m Venue : Unit No. 6 (B-0-6), Ground Floor, Block B Megan Avenue II, No 12, Jln Yap Kwan Seng, Kuala Lumpur www.ngchanmau.com/auto "Prospect bidders may submit bids for the Auto e-Bidding via www.ngchanmau.com/auto. *Please register at least one (1) working day before auction day for registration & verification purposes". To get a digital copy of auction listings by Car Make / Model, please SMS or Whatsapp to 012-5310600. LEGAL OWNER : PUBLIC BANK BERHAD (6463-H) / PUBLIC ISLAMIC BANK BERHAD (14328-V) REGN. REGISTRATION YEAR OF KEY RESERVE PRICE LOT NO MAKE & MODEL CARD REMARKS NO MAKE (YES / NO) (RM) (YES / NO) STORE YARD : INTER PACIFIC AUTO AUCTION SDN. BHD. PANDAN SAFARI SHOPPING COMPLEX, CAR PARK (LEVEL 3) , NO. 1, JALAN PERDANA 6/10A, PANDAN PERDANA, 55300 KUALA LUMPUR (TELEPHONE NO : 03-9274 7612 / 9274 7613) VIEWING DATES: 28th, 29th & 30th March 2019 (10.00AM - 3.00PM) & 1st April 2019 (10.00AM - 12.00PM) P101 WB3177S PROTON SAGA 1.3 2015 YES NO 12,000 P102 PGM2662 TOYOTA AVANZA 1.3 2005 YES NO 7,000 P103 WRR1627 HYUNDAI SONATA EF 2.4 2008 YES YES 5,000 P104 WWJ2704 PROTON EXORA 1.6 2012 YES NO 11,000 P105 PKV6892 PROTON SAGA 1.3 2012 NO NO 6,000 AP Incomplete. Only AP Form 1 P106 WXN3467 NISSAN MURANO 2.5 2009/12 YES NO 37,000 And 69 Available. P107 WRQ9922 MAZDA 6 2.5 2008 NO NO Engine number different. -

Automotive UNDERWEIGHT “March-Ing” Downhill on MCO ↓ by Wan Mustaqim Bin Wan Ab Aziz L [email protected]

Sector Update 30 April 2020 Automotive UNDERWEIGHT “March-ing” Downhill on MCO ↓ By Wan Mustaqim Bin Wan Ab Aziz l [email protected] Given the worse-than-expected impact of the extended MCO and sharp slowing of the economy, we downgrade our sector call to UNDERWEIGHT (from NEUTRAL) with a lower 2020 TIV target units of 420k (- 31% YoY) from 560k (-7% YoY), mindful that the 2QCY20 is a lost quarter. With this downgrade, we will revise our company calls and TP in the upcoming reports. According to the Malaysian Automotive Association (MAA), TIV for March 2020 registered sales of 22,478 units (-44% MoM, -59% YoY). Both MoM and YoY sales growth skidded downhill due to the movement control order (MCO) which started on 18th March 2020. 3MCY20 reported TIV of 106,428 units (-26%), forming 25% of our 2020 renewed sales target, with national marques (63%) expected to continue surpassing non-national marques (37%) driven mainly by Proton’s robust sales growth (+19% YoY) and supported by Perodua (-26% YoY) to cushion the impact. There were no sales expected for April 2020 as the MCO was extended until 12th May 2020 with showrooms closed across the country. March 2020 registered sales of 22,478 units (-44% MoM, -59% YoY). Both MoM and YoY sales growth skidded downhill due to the movement control order (MCO) which started on 18th March 2020. Taking a detailed look at the passenger vehicles segment (-45% MoM, -60% YoY), both MoM and YoY performances tracked the overall unit sales trend on the above-mentioned reasons.