2021.08.24 NMLS Listing.Xlsx

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Down Payment and Closing Cost Assistance

STATE HOUSING FINANCE AGENCIES Down Payment and Closing Cost Assistance OVERVIEW STRUCTURE For many low- and moderate-income people, the The structure of down payment assistance programs most significant barrier to homeownership is the down varies by state with some programs offering fully payment and closing costs associated with getting a amortizing, repayable second mortgages, while other mortgage loan. For that reason, most HFAs offer some programs offer deferred payment and/or forgivable form of down payment and closing cost assistance second mortgages, and still other programs offer grant (DPA) to eligible low- and moderate-income home- funds with no repayment requirement. buyers in their states. The vast majority of HFA down payment assistance programs must be used in combi DPA SECOND MORTGAGES (AMORTIZING) nation with a first-lien mortgage product offered by the A second mortgage loan is subordinate to the first HFA. A few states offer stand-alone down payment and mortgage and is used to cover down payment and closing cost assistance that borrowers can combine closing costs. It is repayable over a given term. The with any non-HFA eligible mortgage product. Some interest rates and terms of the loans vary by state. DPA programs are targeted toward specific popula In some programs, the interest rate on the second tions, such as first-time homebuyers, active military mortgage matches that of the first mortgage. Other personnel and veterans, or teachers. Others offer programs offer more deeply subsidized rates on their assistance for any homebuyer who meets the income second mortgage down payment assistance. Some and purchase price limitations of their programs. -

Commercial Mortgage Loans

STRATEGY INSIGHTS MAY 2014 Commercial Mortgage Loans: A Mature Asset Offering Yield Potential and IG Credit Quality by Jack Maher, Managing Director, Head of Private Real Estate Mark Hopkins, CFA, Vice President, Senior Research Analyst Commercial mortgage loans (CMLs) have emerged as a desirable option within a well-diversified fixed income portfolio for their ability to provide incremental yield while maintaining the portfolio’s credit quality. CMLs are privately negotiated debt instruments and do not carry risk ratings commonly associated with public bonds. However, our paper attempts to document that CMLs generally available to institutional investors have a credit profile similar to that of an A-rated corporate bond, while also historically providing an additional 100 bps in yield over A-rated industrials. CMLs differ from public securities such as corporate bonds in the types of protections they offer investors, most notably the mortgage itself, a benefit that affords lenders significant leverage in the relationship with borrowers. The mortgage is backed by a hard, tangible asset – a property – that helps lenders see very clearly the collateral behind their investment. The mortgage, along with other protections, has helped generate historical recovery from defaulted CMLs that is significantly higher than recovery from defaulted corporate bonds. The private CML market also provides greater flexibility for lenders and borrowers to structure mortgages that meet specific needs such as maturity, loan amount, interest terms and amortization. Real estate as an asset class has become more popular among institutional investors such as pension funds, insurance companies, open-end funds and foreign investors. These investors, along with public real estate investment trusts (REITs), generally invest in higher quality properties with lower leverage. -

The American ≤Uarter Horse Journal That You Can’T Get Anywhere Else Are the Breeding, Halter and Performance Statistics That We Mine from A≤HA’S Database

J J J J The AMERICAN ≤UARTER HORSE J OURNAL APRIL 2013 • $4.25 WWW.AQHAJOURNAL.COM U ≤≤U R R N N A A ON A HIGH THE JOURNAL’S 2012 HIGH-POINT STORIES BEGIN ON PAGE 72 GRASP THE TWO-REIN WITH L L JIMMY STICKLER SILKY SOCKS WAS AN UNPREDICTABLE CHAMPION CONTENTS FEATURES FEATURES 18 Structure in Detail 58 Hard To Get Playboy By Christine Hamilton By Jennifer K. Hancock The hind limb – looking at the stifle This Bank of America high-point senior horse has an all-around great personality 24 Borrow a Trainer By AQHA Professional Horseman 62 A≤HA’s 2012 Michael Colvin with Christine Hamilton High-Point Winners Lengthening stride at any gait 64 Making Runners 28 Barn Babies By Richard Chamberlain Breeders share their 2013 arrivals. Follow along with 2-year-olds on the track. Part of a continuing series 32 Grasping the Two-Rein By Annie Lambert 68 Ricky Ramirez Symbiosis of the mecate and bridle reins has By Honi Roberts enhanced training since the vaqueros developed This young jockey is going places – fast. it into an art form. 38 The Unpredictable 78 Foundation Donors Champion By Larri Jo Starkey April 2013 Silky Socks spooked on a dime, but he The official publication had a world championship ride in him. of the American Quarter 44 60 Years Ago These two are Horse Association. AQHA’s first high-point award winners all-around About the Cover 46 characters. 2012 AQHA All-Around 46 Kaleena Weakly and Senior Horse Hard To Get Playboy Hours Yours And Mine By Jennifer K. -

Your Step-By-Step Mortgage Guide

Your Step-by-Step Mortgage Guide From Application to Closing Table of Contents In this Guide, you will learn about one of the most important steps in the homebuying process — obtaining a mortgage. The materials in this Guide will take you from application to closing and they’ll even address the first months of homeownership to show you the kinds of things you need to do to keep your home. Knowing what to expect will give you the confidence you need to make the best decisions about your home purchase. 1. Overview of the Mortgage Process ...................................................................Page 1 2. Understanding the People and Their Services ...................................................Page 3 3. What You Should Know About Your Mortgage Loan Application .......................Page 5 4. Understanding Your Costs Through Estimates, Disclosures and More ...............Page 8 5. What You Should Know About Your Closing .....................................................Page 11 6. Owning and Keeping Your Home ......................................................................Page 13 7. Glossary of Mortgage Terms .............................................................................Page 15 Your Step-by-Step Mortgage Guide your financial readiness. Or you can contact a Freddie Mac 1. Overview of the Borrower Help Center or Network which are trusted non- profit intermediaries with HUD-certified counselors on staff Mortgage Process that offer prepurchase homebuyer education as well as financial literacy using tools such as the Freddie Mac CreditSmart® curriculum to help achieve successful and Taking the Right Steps sustainable homeownership. Visit http://myhome.fred- diemac.com/resources/borrowerhelpcenters.html for a to Buy Your New Home directory and more information on their services. Next, Buying a home is an exciting experience, but it can be talk to a loan officer to review your income and expenses, one of the most challenging if you don’t understand which can be used to determine the type and amount of the mortgage process. -

Sample Mortgage Application (PDF)

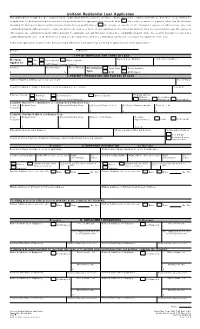

Uniform Residential Loan Application This application is designed to be completed by the applicant(s) with the Lender's assistance. Applicants should complete this form as "Borrower" or "Co-Borrower," as applicable. Co-Borrower information must also be provided (and the appropriate box checked) when the income or assets of a person other than the Borrower (including the Borrower's spouse) will be used as a basis for loan qualification or the income or assets of the Borrower's spouse or other person who has community property rights pursuant to state law will not be used as a basis for loan qualification, but his or her liabilities must be considered because the spouse or other person has community property rights pursuant to applicable law and Borrower resides in a community property state, the security property is located in a community property state, or the Borrower is relying on other property located in a community property state as a basis for repayment of the loan. If this is an application for joint credit, Borrower and Co-Borrower each agree that we intend to apply for joint credit (sign below): Borrower Co-Borrower I. TYPE OF MORTGAGE AND TERMS OF LOAN Agency Case Number Lender Case Number Mortgage VA Conventional Other (explain): Applied for: FHA USDA/Rural Housing Service Amount Interest Rate No. of Months Amortization Fixed Rate Other (explain): $%Type: GPM ARM (type): II. PROPERTY INFORMATION AND PURPOSE OF LOAN Subject Property Address (street, city, state & ZIP) No. of Units Legal Description of Subject Property (attach description if necessary) Year Built Purpose of Loan Purchase Construction Other (explain): Property will be: Primary Secondary Refinance Construction-Permanent Residence Residence Investment Complete this line if construction or construction-permanent loan. -

The General Stud Book : Containing Pedigrees of Race Horses, &C

^--v ''*4# ^^^j^ r- "^. Digitized by tine Internet Arciiive in 2009 witii funding from Lyrasis IVIembers and Sloan Foundation http://www.archive.org/details/generalstudbookc02fair THE GENERAL STUD BOOK VOL. II. : THE deiterol STUD BOOK, CONTAINING PEDIGREES OF RACE HORSES, &C. &-C. From the earliest Accounts to the Year 1831. inclusice. ITS FOUR VOLUMES. VOL. II. Brussels PRINTED FOR MELINE, CANS A.ND C"., EOILEVARD DE WATERLOO, Zi. M DCCC XXXIX. MR V. un:ve PREFACE TO THE FIRST EDITION. To assist in the detection of spurious and the correction of inaccu- rate pedigrees, is one of the purposes of the present publication, in which respect the first Volume has been of acknowledged utility. The two together, it is hoped, will form a comprehensive and tole- rably correct Register of Pedigrees. It will be observed that some of the Mares which appeared in the last Supplement (whereof this is a republication and continua- tion) stand as they did there, i. e. without any additions to their produce since 1813 or 1814. — It has been ascertained that several of them were about that time sold by public auction, and as all attempts to trace them have failed, the probability is that they have either been converted to some other use, or been sent abroad. If any proof were wanting of the superiority of the English breed of horses over that of every other country, it might be found in the avidity with which they are sought by Foreigners. The exportation of them to Russia, France, Germany, etc. for the last five years has been so considerable, as to render it an object of some importance in a commercial point of view. -

On the Laws and Practice of Horse Racing

^^^g£SS/^^ GIFT OF FAIRMAN ROGERS. University of Pennsylvania Annenherg Rare Book and Manuscript Library ROUS ON RACING. Digitized by the Internet Archive in 2009 with funding from Lyrasis IVIembers and Sloan Foundation http://www.archive.org/details/onlawspracticeOOrous ON THE LAWS AND PRACTICE HORSE RACING, ETC. ETC. THE HON^T^^^ ADMIRAL ROUS. LONDON: A. H. BAILY & Co., EOYAL EXCHANGE BUILDINGS, COENHILL. 1866. LONDON : PRINTED BY W. CLOWES AND SONS, STAMFORD STREET, AND CHAKING CROSS. CONTENTS. Preface xi CHAPTER I. On the State of the English Turf in 1865 , . 1 CHAPTER II. On the State of the La^^ . 9 CHAPTER III. On the Rules of Racing 17 CHAPTER IV. On Starting—Riding Races—Jockeys .... 24 CHAPTER V. On the Rules of Betting 30 CHAPTER VI. On the Sale and Purchase of Horses .... 44 On the Office and Legal Responsibility of Stewards . 49 Clerk of the Course 54 Judge 56 Starter 57 On the Management of a Stud 59 vi Contents. KACma CASES. PAGE Horses of a Minor Age qualified to enter for Plates and Stakes 65 Jockey changed in a Race ...... 65 Both Jockeys falling abreast Winning Post . 66 A Horse arriving too late for the First Heat allowed to qualify 67 Both Horses thrown—Illegal Judgment ... 67 Distinction between Plate and Sweepstakes ... 68 Difference between Nomination of a Half-bred and Thorough-bred 69 Whether a Horse winning a Sweepstakes, 23 gs. each, three subscribers, could run for a Plate for Horses which never won 50^. ..... 70 Distance measured after a Race found short . 70 Whether a Compromise was forfeited by the Horse omitting to walk over 71 Whether the Winner distancing the Field is entitled to Second Money 71 A Horse objected to as a Maiden for receiving Second Money 72 Rassela's Case—Wrong Decision ... -

Morgan Horses

The 12th Annual NATIONAL MORGAN HORSE SHOW Sponsored by: Saturday Evening Friday Evening 7:00 P. M. 7:00 P. M. Sunday Saturday Afternoon Afternoon 1:00 P. M. 1:00 P. M. PERFORMANCE BREED CLASSES CLASSES For Stallions and Saddle, Harness, Mares: Colts and Pleasure. Utility Fillies and Equitation THE MORGAN HORSE CLUB Watch The Foundation Breed of America Perform. TRI-COUNTY FAIR GROUNDS NORTHAMPTON, MASS. July 30, 31 and August 1, 1954 Adults $1.00 Children - under 12 - 50' A LAW FOR IT . by 1939 Vermont Legislature "There oughta be a law agin it," is a favorite expresion of Vermonters. Sometimes they reverse themselves and make a law "for it" as they did in 1939 when the legislature passed the following resolution: "Whereas, this is the year recognized as the 150th anniversa y of the famous horse 'Justin Morgan,' which horse not only established a recognized breed of horses named for a single individual, but brought fame th•tzugh his descendants to Vermont and thousands of dollars to Vermonters. "The name Morgan has come to mean beauty, spirit, and action to all lovers of the horse; and the Morgan horses fo• many years held the world's record for trotting horses, and "Whereas the Morgan blood is recognized as foundation stock for the American Saddle Horse, for the American Trotting Horse, and for the Tennessee Walking Horse. In each of these three breeds, the Morgan horse is recognized as a foundation, and therefore, with the recognition of its value to the horse b seeders of the nation, and recognition that it was in Vermont that Morgan -

FICO Mortgage Credit Risk Managers Handbook

FICO Mortgage Credit Risk Manager’s Best Practices Handbook Craig Focardi Senior Research Director Consumer Lending, TowerGroup September 2009 Executive Summary The mortgage credit and liquidity crisis has triggered a downward spiral of job losses, declining home prices, and rising mortgage delinquencies and foreclosures. The residential mortgage lending industry faces intense pressures. Mortgage servicers must better manage the rising tide of defaults and return financial institutions to profitability while responding quickly to increased internal, regulatory, and investor reporting requirements. These circumstances have moved management of mortgage credit risk from backstage to center stage. The risk management function cuts across the loan origination, collections, and portfolio risk management departments and is now a focus in mortgage servicers’ strategic planning, financial management, and lending operations. The imperative for strategic focus on credit risk management as well as information technology (IT) resource allocation to this function may seem obvious today. However, as recently as June 2007, mortgage lenders continued to originate subprime and other risky mortgages while investing little in new mortgage collections and infrastructure, technology, and training for mortgage portfolio management. Moreover, survey results presented in this Handbook reveal that although many mortgage servicers have increased mortgage collections and loss mitigation staffing, few servicers have invested sufficiently in data management, predictive analytics, scoring and reporting technology to identify the borrowers most at risk, implement appropriate treatments for different customer segments, and reduce mortgage re-defaults and foreclosures. The content of this Handbook is based on a survey that FICO, a leader in decision management, analytics, and scoring, commissioned from TowerGroup, a leading research and advisory firm focusing on the strategic application of technology in financial services. -

1 I. Introduction Interest Rates, Financial Leverage, and Asset Values Are

I. Introduction Interest rates, financial leverage, and asset values are among the most important variables in the economy. Many economists, policy makers, and investors believe that these variables may affect each other; therefore, manipulation of some variables may cause desired changes in the others. While interest rates are traditionally the variable that the Federal Reserve monitors and tries to influence, research on the recent financial crisis highlights the importance of financial leverage in the economy (see, e.g. Geanakoplos (2009), Acharya and Viswanathan (2011), among others). Recognizing this, Federal Reserve researchers are investigating whether changing requirements for mortgages’ loan-to-value ratios based on the economic environment could improve financial stability.1 The effectiveness of such policies would depend on how the loan to value ratios and property values exactly interact with each other, as well as whether and how they are endogenously determined. For example, if the two variables are only endogenously correlated and do not affect each other, policies that tries to manipulate the loan to value ratios to affect property values would have little effect. A natural starting point to understand the interactions between the loan to value ratios and property values is to understand their long-run equilibrium relationship. However, the existing literature is virtually silent on this very important issue. 1 See the speech by Ben S. Bernanke at the Annual Meeting of the American Economic Association at Philadelphia: http://www.federalreserve.gov/newsevents/speech/bernanke20140103a.htm. 1 This paper develops a very simple theoretical model in which commercial real estate mortgage interest rates, leverage, and property values are jointly determined. -

Nber Working Paper Series Covered Farm Mortgage

NBER WORKING PAPER SERIES COVERED FARM MORTGAGE BONDS IN THE LATE NINETEENTH CENTURY U.S. Kenneth A. Snowden Working Paper 16242 http://www.nber.org/papers/w16242 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge, MA 02138 July 2010 This paper has benefited from the comments of Walid BuSaba, Charles Courtemanche, John Neufeld, Dan Rosenbaum, Chris Ruhm, Chris Swann, Insan Tunali, two anonymous referees and participants of seminars at UNC Greensboro, Rutgers and the University of Western Ontario. Nidal Abu Saba assembled the Watkins loan sample while Debra Ritch and Michael Cofer provided invaluable research assistance in coding Watkins’s mortgage ledgers. The material is based upon work supported by the National Science Foundation Grant No. SES-9122566. The views expressed herein are those of the author and do not necessarily reflect the views of the National Bureau of Economic Research. NBER working papers are circulated for discussion and comment purposes. They have not been peer- reviewed or been subject to the review by the NBER Board of Directors that accompanies official NBER publications. © 2010 by Kenneth A. Snowden. All rights reserved. Short sections of text, not to exceed two paragraphs, may be quoted without explicit permission provided that full credit, including © notice, is given to the source. Covered Farm Mortgage Bonds in the Late Nineteenth Century U.S. Kenneth A. Snowden NBER Working Paper No. 16242 July 2010 JEL No. G28,G29,N1,N11,N2,N21,N5,N51,R51 ABSTRACT Covered mortgage bonds have been used successfully in Europe for two centuries, but failed in the U.S. -

Model Insurance Requirements for a Commercial Mortgage Loan

Model Insurance Requirements For A Commercial Mortgage Loan James E. Branigan and Joshua Stein Commercial buildings make good collateral for a lender.They make even better collateral when properly insured against damage and destruction. ⅥⅥⅥ REAL ESTATE LOANS START FROM the A fire or other loss affecting the borrower’s fundamental assumption that the borrower’s building can undercut this very fundamental assumption and throw the loan into default building will continue to exist. As long as the rather quickly—unless the borrower has main- building exists, it can produce rental income so tained an appropriate package of insurance cov- the borrower can pay debt service. erage for the mortgaged property. James E. Branigan, President and Chief Executive Officer of Omega Risk Management LLC, has spoken extensively on insurance and risk management for bar associations and major law firms. His firm is a consultancy, which does not sell insurance. He can be reached at (631) 692-9866 or [email protected]. Joshua Stein, a partner in the New York office of Latham & Watkins LLP, is a member of the American College of Real Estate Lawyers, First Vice Chair of the New York State Bar Association Real Property Law Section, and author of New York Commercial Mortgage Transactions (Aspen 2002), A Practical Guide to Real Estate Practice (ALI-ABA 2001), and over 100 articles about commercial real estate law and prac- tice. He can be reached at (212) 906-1342 or [email protected]. An earlier version of this article appeared in The Real Estate Finance Journal 10 (Winter 2004) , and in Joshua Stein’s recent Mortgage Bankers Association book, Lender’s Guide to Structuring and Closing Commercial Mortgage Loans.