FICO Mortgage Credit Risk Managers Handbook

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Down Payment and Closing Cost Assistance

STATE HOUSING FINANCE AGENCIES Down Payment and Closing Cost Assistance OVERVIEW STRUCTURE For many low- and moderate-income people, the The structure of down payment assistance programs most significant barrier to homeownership is the down varies by state with some programs offering fully payment and closing costs associated with getting a amortizing, repayable second mortgages, while other mortgage loan. For that reason, most HFAs offer some programs offer deferred payment and/or forgivable form of down payment and closing cost assistance second mortgages, and still other programs offer grant (DPA) to eligible low- and moderate-income home- funds with no repayment requirement. buyers in their states. The vast majority of HFA down payment assistance programs must be used in combi DPA SECOND MORTGAGES (AMORTIZING) nation with a first-lien mortgage product offered by the A second mortgage loan is subordinate to the first HFA. A few states offer stand-alone down payment and mortgage and is used to cover down payment and closing cost assistance that borrowers can combine closing costs. It is repayable over a given term. The with any non-HFA eligible mortgage product. Some interest rates and terms of the loans vary by state. DPA programs are targeted toward specific popula In some programs, the interest rate on the second tions, such as first-time homebuyers, active military mortgage matches that of the first mortgage. Other personnel and veterans, or teachers. Others offer programs offer more deeply subsidized rates on their assistance for any homebuyer who meets the income second mortgage down payment assistance. Some and purchase price limitations of their programs. -

Commercial Mortgage Loans

STRATEGY INSIGHTS MAY 2014 Commercial Mortgage Loans: A Mature Asset Offering Yield Potential and IG Credit Quality by Jack Maher, Managing Director, Head of Private Real Estate Mark Hopkins, CFA, Vice President, Senior Research Analyst Commercial mortgage loans (CMLs) have emerged as a desirable option within a well-diversified fixed income portfolio for their ability to provide incremental yield while maintaining the portfolio’s credit quality. CMLs are privately negotiated debt instruments and do not carry risk ratings commonly associated with public bonds. However, our paper attempts to document that CMLs generally available to institutional investors have a credit profile similar to that of an A-rated corporate bond, while also historically providing an additional 100 bps in yield over A-rated industrials. CMLs differ from public securities such as corporate bonds in the types of protections they offer investors, most notably the mortgage itself, a benefit that affords lenders significant leverage in the relationship with borrowers. The mortgage is backed by a hard, tangible asset – a property – that helps lenders see very clearly the collateral behind their investment. The mortgage, along with other protections, has helped generate historical recovery from defaulted CMLs that is significantly higher than recovery from defaulted corporate bonds. The private CML market also provides greater flexibility for lenders and borrowers to structure mortgages that meet specific needs such as maturity, loan amount, interest terms and amortization. Real estate as an asset class has become more popular among institutional investors such as pension funds, insurance companies, open-end funds and foreign investors. These investors, along with public real estate investment trusts (REITs), generally invest in higher quality properties with lower leverage. -

Basel III: Post-Crisis Reforms

Basel III: Post-Crisis Reforms Implementation Timeline Focus: Capital Definitions, Capital Focus: Capital Requirements Buffers and Liquidity Requirements Basel lll 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 1 January 2022 Full implementation of: 1. Revised standardised approach for credit risk; 2. Revised IRB framework; 1 January 3. Revised CVA framework; 1 January 1 January 1 January 1 January 1 January 2018 4. Revised operational risk framework; 2027 5. Revised market risk framework (Fundamental Review of 2023 2024 2025 2026 Full implementation of Leverage Trading Book); and Output 6. Leverage Ratio (revised exposure definition). Output Output Output Output Ratio (Existing exposure floor: Transitional implementation floor: 55% floor: 60% floor: 65% floor: 70% definition) Output floor: 50% 72.5% Capital Ratios 0% - 2.5% 0% - 2.5% Countercyclical 0% - 2.5% 2.5% Buffer 2.5% Conservation 2.5% Buffer 8% 6% Minimum Capital 4.5% Requirement Core Equity Tier 1 (CET 1) Tier 1 (T1) Total Capital (Tier 1 + Tier 2) Standardised Approach for Credit Risk New Categories of Revisions to the Existing Standardised Approach Exposures • Exposures to Banks • Exposure to Covered Bonds Bank exposures will be risk-weighted based on either the External Credit Risk Assessment Approach (ECRA) or Standardised Credit Risk Rated covered bonds will be risk Assessment Approach (SCRA). Banks are to apply ECRA where regulators do allow the use of external ratings for regulatory purposes and weighted based on issue SCRA for regulators that don’t. specific rating while risk weights for unrated covered bonds will • Exposures to Multilateral Development Banks (MDBs) be inferred from the issuer’s For exposures that do not fulfil the eligibility criteria, risk weights are to be determined by either SCRA or ECRA. -

Personal Loans 101: Understanding Your Credit Risk Loans Have Some Risk for Both the Borrower and the Lender

PERSONAL LOANS 101: Understanding YoUr credit risk Loans have some risk for both the borrower and the lender. The borrower takes on the responsibilities and terms of paying back the loan. The lender’s risk is the chance of non-payment. Consumers can choose from several types of loans. As a borrower, you need to understand the type of loan you are considering and its possible risk. This brochure provides information to help you make a smart choice before applying for a loan. 2 It is important to review your financial situation to see if you can handle another monthly payment before applying for a loan. Creating a budget will help you apply for the loan that best meets your present and future needs. For an interactive budget, visit www.afsaef.org/budgetplanner or www.afsaef.org/personalloans101. You will need to show the lender that you can repay what you borrow, with interest. After you have made a budget, consider these factors, which maY redUce or add risk to a Loan. 3 abiLitY to repaY the Loan Is the lender evaluating your ability to repay the loan based on facts such as your credit history, current and expected income, current expenses, debt-to- income ratio (your expenses compared to your income) and employment status? This assessment, often called underwriting, helps determine if you can make the monthly payment and raises your chances of getting a loan to fit your needs that you can afford to repay. It depends on you providing complete and correct information to the lender. Testing “your ability to repay” and appropriate “underwriting” reduces your risk when taking out any type of loan. -

Credit Risk Models

Lecture notes on risk management, public policy, and the financial system Credit risk models Allan M. Malz Columbia University Credit risk models Outline Overview of credit risk analytics Single-obligor credit risk models © 2020 Allan M. Malz Last updated: February 8, 2021 2/32 Credit risk models Overview of credit risk analytics Overview of credit risk analytics Credit risk metrics and models Intensity models and default time analytics Single-obligor credit risk models 3/32 Credit risk models Overview of credit risk analytics Credit risk metrics and models Key metrics of credit risk Probability of default πt defined over a time horizon t, e.g. one year Exposure at default: amount the lender can lose in default For a loan or bond, par value plus accrued interest For OTC derivatives, also driven by market value Net present value (NPV) 0 ( counterparty risk) S → But exposure at default 0 ≥ Recovery: creditor generally loses fraction of exposure R < 100 percent Loss given default (LGD) equals exposure minus recovery (a fraction 1 − R) Expected loss (EL) equals default probability × LGD or fraction πt × (1 − R) Credit risk management focuses on unexpected loss Credit Value-at-Risk related to a quantile of the credit return distribution Differs from market risk in excluding EL Credit VaR at confidence level of α defined as: 1 − α-quantile of credit loss distribution − EL 4/32 Credit risk models Overview of credit risk analytics Credit risk metrics and models Estimating default probabilities Risk-neutral default probabilities based on market -

Your Step-By-Step Mortgage Guide

Your Step-by-Step Mortgage Guide From Application to Closing Table of Contents In this Guide, you will learn about one of the most important steps in the homebuying process — obtaining a mortgage. The materials in this Guide will take you from application to closing and they’ll even address the first months of homeownership to show you the kinds of things you need to do to keep your home. Knowing what to expect will give you the confidence you need to make the best decisions about your home purchase. 1. Overview of the Mortgage Process ...................................................................Page 1 2. Understanding the People and Their Services ...................................................Page 3 3. What You Should Know About Your Mortgage Loan Application .......................Page 5 4. Understanding Your Costs Through Estimates, Disclosures and More ...............Page 8 5. What You Should Know About Your Closing .....................................................Page 11 6. Owning and Keeping Your Home ......................................................................Page 13 7. Glossary of Mortgage Terms .............................................................................Page 15 Your Step-by-Step Mortgage Guide your financial readiness. Or you can contact a Freddie Mac 1. Overview of the Borrower Help Center or Network which are trusted non- profit intermediaries with HUD-certified counselors on staff Mortgage Process that offer prepurchase homebuyer education as well as financial literacy using tools such as the Freddie Mac CreditSmart® curriculum to help achieve successful and Taking the Right Steps sustainable homeownership. Visit http://myhome.fred- diemac.com/resources/borrowerhelpcenters.html for a to Buy Your New Home directory and more information on their services. Next, Buying a home is an exciting experience, but it can be talk to a loan officer to review your income and expenses, one of the most challenging if you don’t understand which can be used to determine the type and amount of the mortgage process. -

Sample Mortgage Application (PDF)

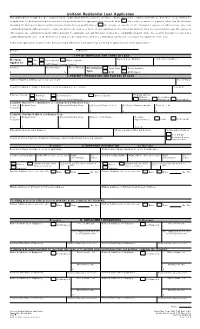

Uniform Residential Loan Application This application is designed to be completed by the applicant(s) with the Lender's assistance. Applicants should complete this form as "Borrower" or "Co-Borrower," as applicable. Co-Borrower information must also be provided (and the appropriate box checked) when the income or assets of a person other than the Borrower (including the Borrower's spouse) will be used as a basis for loan qualification or the income or assets of the Borrower's spouse or other person who has community property rights pursuant to state law will not be used as a basis for loan qualification, but his or her liabilities must be considered because the spouse or other person has community property rights pursuant to applicable law and Borrower resides in a community property state, the security property is located in a community property state, or the Borrower is relying on other property located in a community property state as a basis for repayment of the loan. If this is an application for joint credit, Borrower and Co-Borrower each agree that we intend to apply for joint credit (sign below): Borrower Co-Borrower I. TYPE OF MORTGAGE AND TERMS OF LOAN Agency Case Number Lender Case Number Mortgage VA Conventional Other (explain): Applied for: FHA USDA/Rural Housing Service Amount Interest Rate No. of Months Amortization Fixed Rate Other (explain): $%Type: GPM ARM (type): II. PROPERTY INFORMATION AND PURPOSE OF LOAN Subject Property Address (street, city, state & ZIP) No. of Units Legal Description of Subject Property (attach description if necessary) Year Built Purpose of Loan Purchase Construction Other (explain): Property will be: Primary Secondary Refinance Construction-Permanent Residence Residence Investment Complete this line if construction or construction-permanent loan. -

Capital Adequacy Requirements (CAR)

Guideline Subject: Capital Adequacy Requirements (CAR) Chapter 3 – Credit Risk – Standardized Approach Effective Date: November 2017 / January 20181 The Capital Adequacy Requirements (CAR) for banks (including federal credit unions), bank holding companies, federally regulated trust companies, federally regulated loan companies and cooperative retail associations are set out in nine chapters, each of which has been issued as a separate document. This document, Chapter 3 – Credit Risk – Standardized Approach, should be read in conjunction with the other CAR chapters which include: Chapter 1 Overview Chapter 2 Definition of Capital Chapter 3 Credit Risk – Standardized Approach Chapter 4 Settlement and Counterparty Risk Chapter 5 Credit Risk Mitigation Chapter 6 Credit Risk- Internal Ratings Based Approach Chapter 7 Structured Credit Products Chapter 8 Operational Risk Chapter 9 Market Risk 1 For institutions with a fiscal year ending October 31 or December 31, respectively Banks/BHC/T&L/CRA Credit Risk-Standardized Approach November 2017 Chapter 3 - Page 1 Table of Contents 3.1. Risk Weight Categories ............................................................................................. 4 3.1.1. Claims on sovereigns ............................................................................... 4 3.1.2. Claims on unrated sovereigns ................................................................. 5 3.1.3. Claims on non-central government public sector entities (PSEs) ........... 5 3.1.4. Claims on multilateral development banks (MDBs) -

Guidance for Managing Third-Party Risk

GUIDANCE FOR MANAGING THIRD-PARTY RISK Introduction An institution’s board of directors and senior management are ultimately responsible for managing activities conducted through third-party relationships, and identifying and controlling the risks arising from such relationships, to the same extent as if the activity were handled within the institution. This guidance includes a description of potential risks arising from third-party relationships, and provides information on identifying and managing risks associated with financial institutions’ business relationships with third parties.1 This guidance applies to any of an institution’s third-party arrangements, and is intended to be used as a resource for implementing a third-party risk management program. This guidance provides a general framework that boards of directors and senior management may use to provide appropriate oversight and risk management of significant third-party relationships. A third-party relationship should be considered significant if the institution’s relationship with the third party is a new relationship or involves implementing new bank activities; the relationship has a material effect on the institution’s revenues or expenses; the third party performs critical functions; the third party stores, accesses, transmits, or performs transactions on sensitive customer information; the third party markets bank products or services; the third party provides a product or performs a service involving subprime lending or card payment transactions; or the third party poses risks that could significantly affect earnings or capital. The FDIC reviews a financial institution’s risk management program and the overall effect of its third-party relationships as a component of its normal examination process. -

Credit Risk Measurement: Developments Over the Last 20 Years

Journal of Banking & Finance 21 (1998) 1721±1742 Credit risk measurement: Developments over the last 20 years Edward I. Altman, Anthony Saunders * Salomon Brothers Center, Leonard Stern School of Business, New York University, 44 West 4th street, New York, NY 10012, USA Abstractz This paper traces developments in the credit risk measurement literature over the last 20 years. The paper is essentially divided into two parts. In the ®rst part the evolution of the literature on the credit-risk measurement of individual loans and portfolios of loans is traced by way of reference to articles appearing in relevant issues of the Journal of Banking and Finance and other publications. In the second part, a new approach built around a mortality risk framework to measuring the risk and returns on loans and bonds is presented. This model is shown to oer some promise in analyzing the risk-re- turn structures of portfolios of credit-risk exposed debt instruments. Ó 1998 Elsevier Science B.V. All rights reserved. JEL classi®cation: G21; G28 Keywords: Banking; Credit risk; Default 1. Introduction Credit risk measurement has evolved dramatically over the last 20 years in response to a number of secular forces that have made its measurement more * Corresponding author. Tel.: +1 212 998 0711; fax: +1 212 995 4220; e-mail: asaun- [email protected]. 0378-4266/97/$17.00 Ó 1997 Elsevier Science B.V. All rights reserved. PII S 0 3 7 8 - 4 2 6 6 ( 9 7 ) 0 0 0 3 6 - 8 1722 E.I. Altman, A. Saunders / Journal of Banking & Finance 21 (1998) 1721±1742 important than ever before. -

1 I. Introduction Interest Rates, Financial Leverage, and Asset Values Are

I. Introduction Interest rates, financial leverage, and asset values are among the most important variables in the economy. Many economists, policy makers, and investors believe that these variables may affect each other; therefore, manipulation of some variables may cause desired changes in the others. While interest rates are traditionally the variable that the Federal Reserve monitors and tries to influence, research on the recent financial crisis highlights the importance of financial leverage in the economy (see, e.g. Geanakoplos (2009), Acharya and Viswanathan (2011), among others). Recognizing this, Federal Reserve researchers are investigating whether changing requirements for mortgages’ loan-to-value ratios based on the economic environment could improve financial stability.1 The effectiveness of such policies would depend on how the loan to value ratios and property values exactly interact with each other, as well as whether and how they are endogenously determined. For example, if the two variables are only endogenously correlated and do not affect each other, policies that tries to manipulate the loan to value ratios to affect property values would have little effect. A natural starting point to understand the interactions between the loan to value ratios and property values is to understand their long-run equilibrium relationship. However, the existing literature is virtually silent on this very important issue. 1 See the speech by Ben S. Bernanke at the Annual Meeting of the American Economic Association at Philadelphia: http://www.federalreserve.gov/newsevents/speech/bernanke20140103a.htm. 1 This paper develops a very simple theoretical model in which commercial real estate mortgage interest rates, leverage, and property values are jointly determined. -

Nber Working Paper Series Covered Farm Mortgage

NBER WORKING PAPER SERIES COVERED FARM MORTGAGE BONDS IN THE LATE NINETEENTH CENTURY U.S. Kenneth A. Snowden Working Paper 16242 http://www.nber.org/papers/w16242 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge, MA 02138 July 2010 This paper has benefited from the comments of Walid BuSaba, Charles Courtemanche, John Neufeld, Dan Rosenbaum, Chris Ruhm, Chris Swann, Insan Tunali, two anonymous referees and participants of seminars at UNC Greensboro, Rutgers and the University of Western Ontario. Nidal Abu Saba assembled the Watkins loan sample while Debra Ritch and Michael Cofer provided invaluable research assistance in coding Watkins’s mortgage ledgers. The material is based upon work supported by the National Science Foundation Grant No. SES-9122566. The views expressed herein are those of the author and do not necessarily reflect the views of the National Bureau of Economic Research. NBER working papers are circulated for discussion and comment purposes. They have not been peer- reviewed or been subject to the review by the NBER Board of Directors that accompanies official NBER publications. © 2010 by Kenneth A. Snowden. All rights reserved. Short sections of text, not to exceed two paragraphs, may be quoted without explicit permission provided that full credit, including © notice, is given to the source. Covered Farm Mortgage Bonds in the Late Nineteenth Century U.S. Kenneth A. Snowden NBER Working Paper No. 16242 July 2010 JEL No. G28,G29,N1,N11,N2,N21,N5,N51,R51 ABSTRACT Covered mortgage bonds have been used successfully in Europe for two centuries, but failed in the U.S.