Ancillary Service Provision by RES and DSM Connected at Distribution Level in the Future Power System D1.1

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Next Generation Wind and Solar Power from Cost to Value FULL REPORT Next Generation Wind and Solar Power from Cost to Value INTERNATIONAL ENERGY AGENCY

FULL REPORT Next Generation Wind and Solar Power From cost to value FULL REPORT Next Generation Wind and Solar Power From cost to value INTERNATIONAL ENERGY AGENCY The International Energy Agency (IEA), an autonomous agency, was established in November 1974. Its primary mandate was – and is – two-fold: to promote energy security amongst its member countries through collective response to physical disruptions in oil supply, and provide authoritative research and analysis on ways to ensure reliable, affordable and clean energy for its 29 member countries and beyond. The IEA carries out a comprehensive programme of energy co-operation among its member countries, each of which is obliged to hold oil stocks equivalent to 90 days of its net imports. The Agency’s aims include the following objectives: Secure member countries’ access to reliable and ample supplies of all forms of energy; in particular, through maintaining effective emergency response capabilities in case of oil supply disruptions. Promote sustainable energy policies that spur economic growth and environmental protection in a global context – particularly in terms of reducing greenhouse-gas emissions that contribute to climate change. Improve transparency of international markets through collection and analysis of energy data. Support global collaboration on energy technology to secure future energy supplies and mitigate their environmental impact, including through improved energy efficiency and development and deployment of low-carbon technologies. Find solutions to global -

System Plan 2018 – Electricity and Gas in Denmark 2 System Plan 2018

SYSTEM PLAN 2018 – ELECTRICITY AND GAS IN DENMARK 2 SYSTEM PLAN 2018 CONTENTS 1. A holistic approach to electricity and gas planning ......................................3 1.1 Energinet’s objectives and the political framework .............................................. 3 1.2 New organisation ............................................................................................................. 4 1.3 Analysis and planning .................................................................................................... 5 1.4 Research and development .......................................................................................... 8 1.5 Environmental reporting ..............................................................................................10 1.6 Energy efficiency ............................................................................................................11 2. Electricity .........................................................................................................16 2.1 Security of electricity supply ......................................................................................17 2.2 Resources to safeguard balance and technical quality ......................................22 2.3 Cooperation with other countries ..............................................................................24 2.4 Cooperation with other grid operators ....................................................................29 2.5 Planning for conversion and expansion of electrical installations -

Engineering Economics

CASE STUDIES Engineering Economics AAGE U. MICHELSEN ISBN 978-87-89359-32-8 Aage U. Michelsen : Engineering Economics 27th edition 2016 Publisher: Bodano Publishing & Communication ApS Copyright © Bodano 2016 Bodano Publishing & Communication ApS Hovedgaden 47 DK 2970 Hørsholm Phone +45 38 74 78 76 www.bodanopub.dk E-mail: [email protected] 2 Foreword This collection of case studies is designed to be used as educational material in the teaching of business economics to engineering students. Many engineering students are primarily interested in the technical disciplines and perceive “economics” as uninteresting and more or less irrelevant to the solution of technical problems. A main objective of this collection of case studies is to illustrate that in business, the economic dimension is highly relevant in the resolution of the vast majority of technical problems. By presenting the economic problems in a tech- nical context, it is hoped that a greater number of engineering students will become interested in economic studies and see the relevance of this. An emphasis has been placed on making the cases realistic, in that they reflect con- crete problems faced by the companies. At the same time, it has been necessary to simplify some of the problems to make them suitable for educational use. In addition, some of the numerical values have been changed for reasons of confidentiality. Most numerical values, however, have the proper order of magnitude. Proposed solutions have been prepared for the numerical problems in the cases, designed to complement textbook theories and models. Some cases also contain discussion portions, which include keywords or keyword-like phrases. -

A Snapshot of the Danish Energy Transition

A Snapshot of the Danish Energy Transition Objectives, Markets, Grid, Support Schemes and Acceptance STUDY A Snapshot of the Danish Energy Transition IMPRINT STUDY A Snapshot of the Danish Energy Transition Objectives, Markets, Grid, Support Schemes and Acceptance WRITTEN BY Agora Energiewende Rosenstrasse 2 | 10178 Berlin | Germany Stephanie Ropenus, Ph.D. [email protected] DTU Management Engineering Danmarks Tekniske Universitet | Produktionstorvet Bygning 426 | rum 109 2800 Kongens Lyngby | Denmark Prof. MSO Henrik Klinge Jacobsen, Ph.D. [email protected] Typesetting: UKEX GRAPHIC, Ettlingen Please quote as: Cover: © robertharding/Fotolia Agora Energiewende and DTU Management Engineering (2015): A Snapshot of the Danish Energy Transition. Objectives, Markets, Grid, Support Schemes 084/17-S-2015/EN and Acceptance. Publication: November 2015 www.agora-energiewende.de Preface Dear Readers, In recent years, Denmark has gained considerable interna- underlying grid expansion within Denmark? What types of tional attention as one of the first movers in implementing consumer participation schemes exist? a green energy transition – the so-called grøn omstilling. In order to achieve an energy system independent from fos- This paper aims to explore some of the lessons learned from sil fuels by 2050, Denmark is pursuing an integrated policy the Danish experience. At the same time, this paper can approach that takes all energy sectors into account. In 2014, serve as an introductory overview to the Danish power wind energy covered 39 percent of Danish electricity de- system and the policies that govern it. The paper is part of mand. Wind and bioenergy – the latter in particular for the Agora Energiewende’s “Lessons Learned from Denmark” se- conversion of combined heat and power plants – will play ries. -

Thesis in Sustainable Energy Planning and Management Aalborg University

Modelling of Energy Systems with High Integration of Renewable Energy Sources Maria-Eftychia Vestarchi Master Thesis in Sustainable Energy Planning and Management Aalborg University Abbreviations AC Alternate Current APF Advanced Pulverised Fuel BEV Battery Electric Vehicle CCGT Combined Cycle Gas Turbine CHP Combined Heat and Power CO2 Carbon Dioxide DC Direct Current ENTSO-E European Network of Transmission System Operators for electricity EOP End of Pipe EU European Union EV Electric vehicle GAMS General Algebraic Modelling System GHG Green House Gases GW Gigawatt GWh Gigawatt hours HVDC High Voltage Direct Current IEA International Energy Agency Kg Kilogram KJ Kilojoule KV Kilovolts KWh Kilowatt hours LPG Liquefied Petroleum Gas MIP Mixed Integer Programming MW Megawatt MWh Megawatt hours Nat_gas Natural gas NOx Nitrous oxides O&M Operation and Maintenance OECD Organisation for Economic Co-operation and Development PHEV Plug-in Hybrid Electric Vehicle PV Photovoltaic RE Renewable Energy SO2 Sulphur Dioxide TEN-E Trans-European Energy Network TIC Techno-Institutional Complex TSO Transmission System Operator TYNDP Ten Year Network Development Plan UC Unit commitment V2G Vehicle to Grid i Title: Modelling of Energy Systems with High Aalborg University Sustainable Energy Planning and Management Integration of Renewable Energy Sources Department of Development and Planning Skibbrogade 5 9000 Aalborg Project period: Abstract February 2nd 2015 – June 3rd 2015 This project examines the Nordic and the German energy systems using the energy model Balmorel. Two core scenarios in 2030 including additional RE capacities, Author interconnectors and EVs, are examined with and without the option of Balmorel to implement unit commitment to power plants, in order to include inflexibility in the systems Maria-Eftychia Vestarchi and approach a more realistic representation of their operation. -

Annual Report 2009 Contents

Annual Report 2009 Contents What is Energinet.dk 3 Promotion of environmentally Income statement 36 friendly power generation 22 The Energinet.dk Group 4 Balance sheet - Assets 37 Research and development 22 Supervisory and Executive Boards 5 Balance sheet - Equity and liabilities 38 Environment 23 Financial highlights for the Statement of changes in equity 39 Energinet.dk Group 6 Knowledge resources and organisation 25 Cash flow statement 41 Statements and reports 7 Energinet.dk’s corporate social Notes 42 Management’s review 13 responsibility (CSR) 26 Segment financial statements 57 Preface by Management 13 Good corporate governance 26 Accounting policies 64 Electricity and gas markets 13 Financial review 27 Managerial posts held by Collaboration with European TSOs 15 Balance sheet 30 Supervisory Board members 69 Tomorrow’s energy system 17 Cash flow statement 31 Stakeholder Forum 69 Investments in the electricity and Outlook 2010 31 Basic principles for gas transmission grids 17 Energinet.dk’s finances 70 Events after the balance sheet date 31 Operation of electricity and Glossary 71 gas transmission grids 20 Business segments 31 Preparedness 22 Risk policy 34 Energinet.dk establishes interconnection between Eastern and Western Denmark In June 2010, the Danish energy system reaches a milestone. This happens when Energinet.dk starts the operational testing of the Great Belt Power Link and transmits power under the Great Belt for the first time. The decision to connect Denmark electrically was made in 2005. The intensive construc- tion work commenced in 2008, and in autumn 2010 the new link will be inaugurated. The photographs on pages 12, 16, 19, 24, 28, 32, 35 and 63 show the building of the Great Belt Power Link. -

Methodology Application Implicit Grid Loss on The

Til Sekretariatetfor Forsyningstilsynet Energinet TonneKjærsvej 65 DK-7000Fredericia +45 70 10 22 44 MethodologyApplication implicit grid loss [email protected] CVR-nr.39 31 49 59 Dato: 30. juni 2020 METHODOLOGYAPPLICATION IMPLICIT GRID LO SS ONTHE GREAT BELT POWER LINK Theenclosed document contains Energinet’s application to introduce implicit losshandling on the GreatBelt PowerLink (betweenthe biddingzones Western Denmark DK1 and EasternDen- mark DK2),in the forward, day-aheadand intradaymarkets as well as the rationalebehind the application.Th isdocumentincludes a descriptionof the appliedfor method and an assessment of the expectedsocio-economic consequences, including distribution effects,of introducing implicit losshandling on the GreatBelt PowerLink .Moreover ,the attachedappendices include additionalbackground information relevantto the application. Theimplicit lossfactor is a correctionmechanism for negativeexternal effects, incentivising the market to respectthe cost of electricitylosses on HVDCinterconnections in the market coupling. Theimplicit losshandling functionality will be implementedby the introduction of a fixed an- nual lossfactor for the GreatBelt PowerLink .It will be possibleto adjustthe lossfactor based on historic medianflowsfor all hours with flow for the interconnectorduringperiods where capacitieshave not yet been providedfor long-term transmissionrights . Thesocio-economic gain over a 40-yearperiod from introducingimplicitloss handlingfor the GreatBelt PowerLink is estimatedat approximatelyDKK 75.39 million for Denmark. Therelevant legal basis in Denmarkfor the introduction ofimplicit losshandlingon the Great Belt PowerLink is the CCRNordic CapacityCalculation Methodologyarticle 6. 1(c).Thus, th e applicationis basedon AnnexI of Regulation943/2019 ,as directly applicableEU law, i.e. regu- lation 714/2009and/or the EuropeanCommission’s regulations on network guidelines,the CACMRegulation etc., replaceany nationalDanish provisionson the actualsubject matter, the introduction ofmethodologiesetc. on cross-borderinterconnectors. -

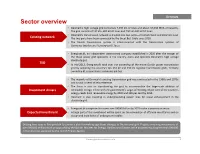

Sector Overview • Denmark’S High Voltage Grid Comprises 7,348 Km of Lines and About 37,638 MVA of Capacity

Denmark Sector overview • Denmark’s high voltage grid comprises 7,348 km of lines and about 37,638 MVA of capacity. The grid consists of 132 kV– 400 kV AC lines and 250 kV–500 kV DC lines. • Denmark’s transmission network is divided into two parts—Denmark West and Denmark East. Existing network The two parts have been connected by the Great Belt Cable since 2010. • The Danish transmission system is interconnected with the transmission systems of Germany, Sweden and Norway via DC lines. • Energinet.dk, an independent state-owned company established in 2005 after the merger of the three power grid operators in the country, owns and operates Denmark’s high voltage electricity grid. TSO • In mid-2012, Energinet.dk took over the ownership of the entire Danish power transmission grid by acquiring the country’s ten 132 kV and 150 kV regional transmission grids, formerly owned by 41 cooperatives and municipalities. • The majority of Denmark’s existing transmission grid was constructed in the 1960s and 1970s and is now in need of reinvestments. • The focus is also on transforming the grid to accommodate the large-scale addition of Investment drivers renewable energy, in line with the government’s target of meeting 50 per cent of the country’s energy needs from renewable energy by 2020 and 100 per cent by 2050. • Denmark is also investing in undergrounding power lines for visual enhancement in the electricity grid. • Energinet.dk is expected to invest over DKKXX billion by 2025 in the transmission sector. Expected investment • A large part of this investment will be spent on the connection of offshore wind farms and on design and installation of underground cables. -

Offshore Wind Farm Projects Kristinestad

Tornio Royttan merotuulivoimapuisto (70 MW, 14) Rajakiiri OY Ajos (26.4 MW, 8) IKEA Kemin Ajoksen Merituulivoimapuiston (81+ MW, 27) Ajos Wind Oy Suurhiekka (480 MW, 80) Suurhiekka Offshore Oy (WPD Offshore GmbH) Lumijoki, Varjakka (2MW, 1) Lumituuli Oy Raahe / Pertunmatala (48+ MW, 12+) Suomen Hyötytuuli Oy Raahe / Ulkonahkiainen (140+ MW, 70) Suomen Hyötytuuli Oy Raahe / Maanahkiaisen (210+MW,70) Rajakiiri OY Rata Storgrund P2(10+turbines) Rewind Offshore AB Kokkolan Merituulivoimapuiston Merventoi Oy Rata Storgrund P1 (10+ turbines) Rewind Offshore AB Europe - Offshore Wind Projects 2020 Kristiansund U Vaasa Averøya Havvind Demonstation Site G Sandøy Havsul (350MW,35+) Havgul Nordic AS EUROPE Härnösand Ålesund Offshore Wind Farm Projects Kristinestad Stadt Test Areas (10MW, 2) Kvernevick Engineering Siipyyn/Kristiinakaupunki (240+ MW, 80+) Suomen Merituuli Oy/EPV Energia/ Helsigem Energia Tórshavn Måløy 11th Edition - 2020 Compiled, Designed and Produced by La Tene Maps Pori Tahkoluoto extension (?MW) Tel: +353-1-2847914 Fax: +353-1-2826311 Email: [email protected] Website: www.latenemaps.com Suomen Hyotytuuli Oy Pori Tahkoluoto (42MW, 10 ) Suomen Hyotytuuli Oy Pori 1 (2.3 MW, 1) Suomen Hyotytuuli Oy Pori Hywind Tampen (88MM, 11) Gretas Klackar (?MW) Equinor, Petoro, Exxon Mobil Northern Gulf of Bothnia SVEA Vind Offshore Kalix Tornio Royttan merotuulivoimapuisto (70 MW, 14) Rajakiiri OY Storgrundet (420MW, 70) Rauma Føroyar Kemi Storgrundet Offshore AB (WPD Offshore GmbH) Ajos (26.4 MW, 8) IKEA Luleå Fenno-Skan HVDC Link (500 -

The European Power System Note De L'ifri

NNoottee ddee ll’’IIffrrii The European Power System Decarbonization and Cost Reduction: Lost in Transmissions? ______________________________________________________________________ Maïté Jauréguy-Naudin January 2012 . Gouvernance européenne et géopolitique de l’énergie The Institut français des relations internationales (Ifri) is a research center and a forum for debate on major international political and economic issues. Headed by Thierry de Montbrial since its founding in 1979, Ifri is a non- governmental and a non-profit organization. As an independent think tank, Ifri sets its own research agenda, publishing its findings regularly for a global audience. Using an interdisciplinary approach, Ifri brings together political and economic decision-makers, researchers and internationally renowned experts to animate its debate and research activities. With offices in Paris and Brussels, Ifri stands out as one of the rare French think tanks to have positioned itself at the very heart of European debate. The opinions expressed in this text are the responsibility of the author alone. ISBN: 978-2-86592-977-1 © All rights reserved, Ifri, 2012 IFRI IFRI-BRUXELLES 27, RUE DE LA PROCESSION RUE MARIE-THERESE, 21 75740 PARIS CEDEX 15 – FRANCE 1000 – BRUSSELS – BELGIUM Tel: +33 (0)1 40 61 60 00 Tel: +32 (0)2 238 51 10 Fax: +33 (0)1 40 61 60 60 Fax: +32 (0)2 238 51 15 Email: [email protected] Email: [email protected] WEBSITE: Ifri.org Executive Summary Europe‘s energy policy is commonly defined by three axes of equal importance: security of supplies, competitiveness and sustainable development. The European Commission is mandated to develop the policy tools that allow the implementation of this common policy. -

Energy Policies of Iea Countries

ENERGY POLICIES OF IEA COUNTRIES Denmark 2017 Review Secure Sustainable Together ENERGY POLICIES OF IEA COUNTRIES Denmark 2017 Review INTERNATIONAL ENERGY AGENCY The International Energy Agency (IEA), an autonomous agency, was established in November 1974. Its primary mandate was – and is – two-fold: to promote energy security amongst its member countries through collective response to physical disruptions in oil supply, and provide authoritative research and analysis on ways to ensure reliable, affordable and clean energy for its 29 member countries and beyond. The IEA carries out a comprehensive programme of energy co-operation among its member countries, each of which is obliged to hold oil stocks equivalent to 90 days of its net imports. The Agency’s aims include the following objectives: n Secure member countries’ access to reliable and ample supplies of all forms of energy; in particular, through maintaining effective emergency response capabilities in case of oil supply disruptions. n Promote sustainable energy policies that spur economic growth and environmental protection in a global context – particularly in terms of reducing greenhouse-gas emissions that contribute to climate change. n Improve transparency of international markets through collection and analysis of energy data. n Support global collaboration on energy technology to secure future energy supplies and mitigate their environmental impact, including through improved energy efficiency and development and deployment of low-carbon technologies. n Find solutions to global -

SECURITY of ELECTRICITY SUPPLY REPORT 2018 2 Security of Electricity Supply Report 2018 Security of Electricity Supply Report 2018 3

SECURITY OF ELECTRICITY SUPPLY REPORT 2018 2 Security of electricity supply report 2018 Security of electricity supply report 2018 3 TABLE OF CONTENTS Summary.....................................................................................................................4 1. Security of electricity supply .............................................................................8 1.1 What is security of electricity supply? ........................................................................ 8 1.2 The security of electricity supply framework is becoming more international ................................................................................... 8 1.3 Level of security of electricity supply ......................................................................10 2. Historical security of electricity supply .........................................................12 2.1 Outage statistics ............................................................................................................. 12 2.2 Electricity system incidents in 2017 .........................................................................14 2.3 Ancillary services ..........................................................................................................18 3. Forward-looking risk assessment ................................................................20 3.1 Expectations for the future electricity system .....................................................20 3.2 Generation adequacy ....................................................................................................20