Press Release Paris – June 21St, 2021

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Global Exchange Indices

Global Exchange Indices Country Exchange Index Argentina Buenos MERVAL, BURCAP Aires Stock Exchange Australia Australian S&P/ASX All Ordinaries, S&P/ASX Small Ordinaries, Stock S&P/ASX Small Resources, S&P/ASX Small Exchange Industriials, S&P/ASX 20, S&P/ASX 50, S&P/ASX MIDCAP 50, S&P/ASX MIDCAP 50 Resources, S&P/ASX MIDCAP 50 Industrials, S&P/ASX All Australian 50, S&P/ASX 100, S&P/ASX 100 Resources, S&P/ASX 100 Industrials, S&P/ASX 200, S&P/ASX All Australian 200, S&P/ASX 200 Industrials, S&P/ASX 200 Resources, S&P/ASX 300, S&P/ASX 300 Industrials, S&P/ASX 300 Resources Austria Vienna Stock ATX, ATX Five, ATX Prime, Austrian Traded Index, CECE Exchange Overall Index, CECExt Index, Chinese Traded Index, Czech Traded Index, Hungarian Traded Index, Immobilien ATX, New Europe Blue Chip Index, Polish Traded Index, Romanian Traded Index, Russian Depository Extended Index, Russian Depository Index, Russian Traded Index, SE Europe Traded Index, Serbian Traded Index, Vienna Dynamic Index, Weiner Boerse Index Belgium Euronext Belgium All Share, Belgium BEL20, Belgium Brussels Continuous, Belgium Mid Cap, Belgium Small Cap Brazil Sao Paulo IBOVESPA Stock Exchange Canada Toronto S&P/TSX Capped Equity Index, S&P/TSX Completion Stock Index, S&P/TSX Composite Index, S&P/TSX Equity 60 Exchange Index S&P/TSX 60 Index, S&P/TSX Equity Completion Index, S&P/TSX Equity SmallCap Index, S&P/TSX Global Gold Index, S&P/TSX Global Mining Index, S&P/TSX Income Trust Index, S&P/TSX Preferred Share Index, S&P/TSX SmallCap Index, S&P/TSX Composite GICS Sector Indexes -

Case Study: the Bayer-Monsanto Acquisition Deal

Case Study: The Bayer-Monsanto Acquisition Deal Student: Georgios Ritsos-Kokkinis (SNR:2013707, ANR:927674) Supervisor: Prof. Dr. Christoph Schneider Second reader: Prof. Dr. Olivier de Jonghe Tilburg, August 2020 Acknowledgements I would like to thank my supervisor Dr. Christoph Schneider, Assistant Professor at Tilburg University – Department of Finance, whose expertise and guidance were invaluable in soundly formulating all the relevant methodologies, and concisely structuring the output results. Your feedback pushed me to sharpen my thinking and brought my work to a higher level. I would also like to thank fellow scholar Thanos Vasiliadis, PhD candidate in Mathematics at Université côté d'Azur, Laboratoire Dieudonné, for his support, encouragement and constructive comments, which were instrumental to the completion of this dissertation. ABSTRACT The acquisition of Bayer-Monsanto was one of the largest M&A deals of the past decade. In this study, I document the motives of this transaction and the timeline of events that took place, from the initial rumors until Bayer’s milestone settlement of Monsanto’s “Roundup” litigation in mid-2020. Fundamental valuations of the two individual companies and their officially disclosed synergies reveal that the premium paid over Monsanto’s overvalued share price was not justified, as is commonly observed in the M&A ecosystem. Multiple approaches to the calculation of the discount factor reach the same conclusion. Averaging across multiple costs of capital, shows that the combined intrinsic value with synergy of roughly $177bn was some $2.12bn higher than the sum of parts, suggesting a rather profitable investment opportunity. However, Bayer, did overpay by 18.08% to reap these benefits. -

Are Retail Investors Less Aggressive on Small Price Stocks?

Are retail investors less aggressive on small price stocks? Carole M´etais∗ Tristan Rogery January 13, 2021 Abstract In this paper, we investigate whether number processing impacts the limit orders of retail investors. Building on existing literature in neuropsychology that shows that individuals do not process small numbers and large numbers in the same way, we study the influence of nominal stock price level on order aggressiveness. Using a unique database that allows us to identify order and trade records issued by retail investors on Euronext Paris, we show that retail investors, when posting non-marketable orders, are less aggressive on small price stocks than on large price stocks. This difference in order aggressiveness is not explained by differences in liquidity and other usual drivers of order aggressiveness. We provide additional evidence by showing that no such difference exists for limit orders of high frequency traders (HFTs) over the same period and the same sample of stocks. This finding confirms that our results are driven by a behavioral bias and not by differential market dynamics between small price stocks and large price stocks. ∗LaRGE Research Center, University of Strasbourg { Mailing address: 61 Avenue de la For^etNoire, 67000 Strasbourg FRANCE { Email: [email protected]. I acknowledge support from the French State through the National Agency for Research under the program Investissements d'Avenir ANR-11-EQPX- 006. yDRM Finance, Universit´eParis-Dauphine, PSL Research University { Mailing address: Place du Mar´echal de Lattre de Tassigny, 75775 Paris Cedex 16 FRANCE { Email: [email protected] 1 1 Introduction While conventional finance theory posits that nominal stock prices are irrelevant for firm valuation, a number of papers provide empirical evidence that nominal prices do impact investor behavior. -

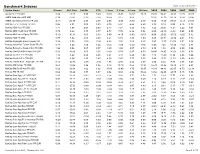

Benchmark Indexes Data As Of: 03/31/2011 Index Name Sharpe Std

Benchmark Indexes Data as of: 03/31/2011 Index Name Sharpe Std. Dev. 1st Qtr YTD 1 Year 3 Year 5 Year 10 Year 2010 2009 2008 2007 2006 Alerian MLP TR USD 0.89 23.25 5.99 5.99 33.02 20.03 16.57 17.25 35.85 76.41 -36.91 12.72 26.07 AMEX Gold Miners PR USD 0.39 47.82 -2.15 -2.15 35.65 8.12 9.68 - 33.94 37.30 -26.79 16.86 21.86 AMEX International Market PR USD -0.13 25.37 2.77 2.77 4.05 -5.95 -0.80 2.17 0.80 17.60 -39.51 16.18 21.51 BarCap 1-5 Yr Treasury TR USD 0.98 2.51 0.00 0.00 2.79 2.91 4.88 4.20 3.73 0.19 8.83 8.16 3.75 BarCap ABS Auto TR USD 1.17 5.68 0.63 0.63 2.47 7.21 6.23 5.12 3.25 26.07 -5.57 5.22 4.61 BarCap ABS Credit Card TR USD 0.79 9.42 0.77 0.77 4.73 7.76 6.86 5.84 6.55 29.89 -9.33 5.45 4.55 BarCap ABS Home Equity TR USD -0.19 16.91 0.00 0.00 0.00 -4.10 -5.80 -0.53 0.00 20.63 -36.00 -8.25 5.32 BarCap ABS TR USD 0.77 6.92 0.64 0.64 4.21 5.74 4.36 4.59 5.85 24.71 -12.72 2.21 4.70 BarCap Aggregate Bond Treasury TR 0.58 5.58 -0.16 -0.16 4.53 3.55 5.69 5.15 5.87 -3.57 13.74 9.01 3.08 BarCap Asian Pac Taiwan Dollar TR JPY 0.78 6.24 1.54 1.54 -2.45 -1.00 -2.50 -0.66 -2.26 7.45 -11.24 -7.52 2.81 BarCap Bellwether Swap 6 Mon TR USD 1.92 0.56 0.07 0.07 0.39 1.50 3.07 2.79 0.38 1.58 4.09 5.39 5.54 BarCap CMBS ERISA Eligible TR USD 0.53 18.46 2.05 2.05 12.62 8.79 6.87 6.53 20.40 28.45 -20.52 5.58 4.72 BarCap Credit 1-3 Yr TR USD 1.16 3.62 0.58 0.58 3.24 4.73 5.29 4.80 4.15 11.59 0.30 5.96 4.66 BarCap Credit 1-5 Yr TR USD 1.06 4.64 0.85 0.85 4.36 5.47 5.77 5.27 5.44 13.52 -1.13 6.09 4.69 BarCap Danish Krone Aggregate TR DKK 0.12 14.76 -

Paris, Le 26 Mars 2001

PR/14/12 Eutelsat Communications joins CAC Large 60 index from 19 March 2012 Paris, March 2, 2012 - Eutelsat Communications (Euronext Paris: ETL) will join the CAC Next 20 and CAC Large 60 indices of NYSE Euronext Paris after the trading session of Monday 19 March 2012, at which point it will be withdrawn from the CAC Mid 60 and CAC Mid & Small indices. Following this, Eutelsat Communications will be part of the following indices of NYSE Euronext Paris: - CAC Next 20 - CAC Large 60 - SBF 120 - CAC All Shares - CAC All-Tradable - CAC Consumer Serv. - CAC Media The decision of the Scientific Board of Euronext Indices of 1 March 2012 enables Eutelsat to increase its visibility in the French and international financial community. Financial calendar The financial calendar below is provided for information purposes only. It is subject to change and will be regularly updated. - May 10, 2012: financial report for third quarter ended March 31, 2012 - July 30, 2012: earnings for full year ended June 30, 2012 - October 25, 2012: financial report for first quarter ended September 30, 2012 - November 8, 2012: Annual General Shareholders Meeting About Eutelsat Communications Eutelsat Communications (Euronext Paris: ETL, ISIN code: FR0010221234) is the holding company of Eutelsat S.A.. With capacity commercialised on 28 satellites that provide coverage over the entire European continent, as well as the Middle East, Africa, India and significant parts of Asia and the Americas, Eutelsat is one of the world's three leading satellite operators in terms of revenues. As of 31 December 2011, Eutelsat’s satellites were broadcasting more than 4,150 television channels. -

Why Switzerland?

Why Switzerland? Marwan Naja, AS Investment Management January, 2010 I. Executive Summary Swiss Equities Have Outperformed: Here is a fact you probably did not know: The Swiss equity market has arguably been the best performing developed world market over the past 20, 10, 5 and 2 years. The SPI Index, which incorporates over 200 Swiss stocks, is the best performing index in Swiss Franc (“CHF”), US Dollars (“USD”), Euro (“EUR”) and British Pounds (“GBP”) over the past 20 years1,10 years, 5 years, and 2 years when compared to similar broad-based total return indices in the United States (S&P 500 Total Return), the United Kingdom (FTSE 350 Total Return), Germany (CDAX), France (SBF 120 Total Return) and Japan (TOPIX Total Return)2. For most of these periods the magnitude of the outperformance is significant. Furthermore, the Swiss market has exhibited attractive risk characteristics including lower volatility than comparable markets. Figure 1: SPI 20 Year Performance (red) Compared to Major Developed Indices in CHF3 1 The 20 year comparable excludes the EUR which has not existed for that duration and the French SBF 120 TR which was established in 1990 and has underperformed the SPI over the 19 year period. 2 The Swiss market is the best performer in our local currency comparison (stripping out the foreign exchange effects) over 20 years and marginally trails the FTSE 350 for the 10 year, 5 year and 2 year comparisons. 3 Source of all graphs is Bloomberg unless otherwise indicated. Why Switzerland? AS Investment Management Contents I. Executive Summary ............................................................................................................ 1 Swiss Equities Have Outperformed ................................................................................... -

Eurofins Fact Sheet March 2021

FACT SHEET Company Overview Our Vision: To be the Global Leader in Eurofins is Testing for Life. Eurofins is the global leader in food, environment, pharmaceutical and Testing for Life cosmetic product testing and in agroscience Contract Research services. Eurofins is also one of the market leaders in certain testing and laboratory services for genomics, discovery pharmacology, Our Mission: To contribute to a safer and forensics, advanced material sciences and in the support of clinical studies, as well as having an healthier world by providing our customers emerging global presence as a Contract Development and Manufacturing Organisation. The Group with innovative and high quality laboratory, also has a rapidly developing presence in highly specialised and molecular clinical diagnostic testing research and advisory services, whilst and in-vitro diagnostic products. creating opportunities for our employees and generating sustainable shareholder value History Eurofins Scientific was founded in 1987 with four employees to market the SNIF-NMR technology, Our Values: Customer Focus, Quality, a patented analytical method used to verify the origin and purity of several types of food and Competence & Team Spirit and Integrity beverages and identify sophisticated fraud not detectable by other methods. Today, the Eurofins Group is a leading provider of testing and analytical services with: • an international network of more than 800 laboratories in over 50 countries Revenues in EUR million • over 50,000 staff • a portfolio of over 200,000 analytical methods • more than 450 million tests performed each year Eurofins has been one of the fastest growing listed European companies. Since its IPO on the French stock exchange in 1997, Eurofins’ revenues have increased by 34% each year (in compound average) to over EUR 5.4 billion in 2020. -

Financial Market Data for R/Rmetrics

Financial Market Data for R/Rmetrics Diethelm Würtz Andrew Ellis Yohan Chalabi Rmetrics Association & Finance Online R/Rmetrics eBook Series R/Rmetrics eBooks is a series of electronic books and user guides aimed at students and practitioner who use R/Rmetrics to analyze financial markets. A Discussion of Time Series Objects for R in Finance (2009) Diethelm Würtz, Yohan Chalabi, Andrew Ellis R/Rmetrics Meielisalp 2009 Proceedings of the Meielisalp Workshop 2011 Editor Diethelm Würtz Basic R for Finance (2010), Diethelm Würtz, Yohan Chalabi, Longhow Lam, Andrew Ellis Chronological Objects with Rmetrics (2010), Diethelm Würtz, Yohan Chalabi, Andrew Ellis Portfolio Optimization with R/Rmetrics (2010), Diethelm Würtz, William Chen, Yohan Chalabi, Andrew Ellis Financial Market Data for R/Rmetrics (2010) Diethelm W?rtz, Andrew Ellis, Yohan Chalabi Indian Financial Market Data for R/Rmetrics (2010) Diethelm Würtz, Mahendra Mehta, Andrew Ellis, Yohan Chalabi Asian Option Pricing with R/Rmetrics (2010) Diethelm Würtz R/Rmetrics Singapore 2010 Proceedings of the Singapore Workshop 2010 Editors Diethelm Würtz, Mahendra Mehta, David Scott, Juri Hinz R/Rmetrics Meielisalp 2011 Proceedings of the Meielisalp Summer School and Workshop 2011 Editor Diethelm Würtz III tinn-R Editor (2010) José Cláudio Faria, Philippe Grosjean, Enio Galinkin Jelihovschi and Ri- cardo Pietrobon R/Rmetrics Meielisalp 2011 Proceedings of the Meielisalp Summer Scholl and Workshop 2011 Editor Diethelm Würtz R/Rmetrics Meielisalp 2012 Proceedings of the Meielisalp Summer Scholl and Workshop 2012 Editor Diethelm Würtz Topics in Empirical Finance with R and Rmetrics (2013), Patrick Hénaff FINANCIAL MARKET DATA FOR R/RMETRICS DIETHELM WÜRTZ ANDREW ELLIS YOHAN CHALABI RMETRICS ASSOCIATION &FINANCE ONLINE Series Editors: Prof. -

Neoen Joins the SBF 120Index

Paris, June 11, 2020 Neoen joins the SBF 120 index Neoen (ISIN: FR0011675362, Ticker: NEOEN), one of the world’s leading and fastest-growing independent producers of exclusively renewable energy, is announcing it is joining the SBF 120 index consisting of the top 120 stocks listed on the Euronext Paris market in term of both liquidity and market capitalization. As part of its quarterly review of the Euronext Paris indices, the Index Committee decided to include Neoen in both the SBF 120 and the CAC Mid 60 indices. This decision will take effect from June 22, 2020. Neoen’s inclusion in these indices is a testament to its good share price performance since its October 2018 IPO. Over the past 20 months, the Company’s market capitalization has more than doubled to almost €3 billion. This strong rise was accompanied by a steady increase in trading volumes. Since its IPO, Neoen has consistently delivered strong earnings growth and expansion in its project portfolio. Assets in operation or under construction have increased from 1.8 GW at June 30, 2018 to 3.1 GW at March 31, 2020, and the target is to have more than 5 GW by year-end 2021. This rapid and profitable growth has been founded on geographical and technological diversification of its asset base. Neoen is present in 14 countries on 4 continents and it develops and operates solar and wind energy generation and storage capacity. Xavier Barbaro, Neoen’s Chairman and Chief Executive Officer, commented: “We are very pleased to be joining this benchmark index, which marks a new important step for Neoen. -

Final Report Amending ITS on Main Indices and Recognised Exchanges

Final Report Amendment to Commission Implementing Regulation (EU) 2016/1646 11 December 2019 | ESMA70-156-1535 Table of Contents 1 Executive Summary ....................................................................................................... 4 2 Introduction .................................................................................................................... 5 3 Main indices ................................................................................................................... 6 3.1 General approach ................................................................................................... 6 3.2 Analysis ................................................................................................................... 7 3.3 Conclusions............................................................................................................. 8 4 Recognised exchanges .................................................................................................. 9 4.1 General approach ................................................................................................... 9 4.2 Conclusions............................................................................................................. 9 4.2.1 Treatment of third-country exchanges .............................................................. 9 4.2.2 Impact of Brexit ...............................................................................................10 5 Annexes ........................................................................................................................12 -

Profil Financier Du CAC 40

Profil financier du CAC 40 Un CAC 40 agile et confiant en l’avenir 15e édition – Année 2020 15 ans, c’est l’âge de notre Profil financier du CAC 40. 15 ans d’une vie mouvementée pour un indice qui aura connu une belle croissance de son chiffre d’affaires et de ses résultats cumulés ainsi qu’un développement réel de ses fondamentaux, mais Nicolas Klapisz Associé, Responsable du également les affres de la crise financière de 2008 département Valuation, Modeling & Economics et, à présent, les conséquences d’une crise sanitaire sans précédent. Pour son quinzième anniversaire, nous Mais les conclusions de notre étude aurions souhaité offrir au Profil – et résident pour nous ailleurs : certes, surtout à ses lecteurs – une véritable les entreprises du CAC 40 ont connu envolée de la croissance et des records une contraction de leur activité et une en abondance. Las ! Les récents réduction de leurs marges inédites, le événements en ont décidé autrement et nier serait un non-sens. Cependant, sont venus contrarier nos ambitions. elles ont fait preuve, dans ce contexte, d’une agilité hors norme. Agilité Les chiffres sont têtus et l’on ne stratégique pour adapter leurs modèles pourra nier l’impact du Covid-19 : une économiques et développer leurs activité en chute de -15 %, un résultat activités digitales, agilité commerciale d’exploitation courant* en recul de -30 %, pour réduire l’impact de la pandémie sur un résultat net en baisse de près de le chiffre d’affaires au second semestre -60 % par rapport à l’an passé. L’ampleur 2020, agilité opérationnelle pour de ces évolutions est à l’image du maîtriser leurs coûts et agilité financière caractère inédit de cette pandémie pour piloter au mieux les résultats, les et des fermetures administratives dividendes et l’endettement. -

INDEX RULE BOOK Leverage, Short, and Bear Indices

INDEX RULE BOOK Leverage, Short, and Bear Indices Version 20-02 Effective from 15 May 2020 indices.euronext.com Index 1. Index Summary 1 2. Governance and Disclaimer 8 2.1 Indices 8 2.2 Administrator 8 2.3 Cases not covered in rules 8 2.4 Rule book changes 8 2.5 Liability 8 2.6 Ownership and trademarks 8 3. Calculation 9 3.1 Definition and Composition of the Index 9 3.2 Calculation of the Leverage Indices 9 3.3 Calculation of the Bear and Short Indices 9 3.4 Reverse split of index level 10 3.5 Split of index level 10 3.6 Financing Adjustment Rate (FIN) 10 4. Publication 11 4.1 Dissemination of Index Values 11 4.2 Exceptional Market Conditions and Corrections 11 4.3 Announcement Policy 14 5. ESG Disclosures 15 1. INDEX SUMMARY Factsheet Leverage, Short and Bear indices Index names Various based on AEX®, BEL 20®, CAC 40®, PSI 20® and ISEQ® Index type Indices are based on price index versions or Net return index or Gross return index versions. Administrator Euronext Paris is the Administrator and is responsible for the day-to-day management of the index. The underlying indices have independent Steering Committees acting as Independent Supervisor. Calculation Based on daily leverage. May include spread on interest rate or Financing Adjustment rate in the calculation Rule for exceptional trading Either suspend or reset if underlying index moved beyond certain threshold. See reference circumstances table. 1 Mnemo Full name Underlying Factor Rule for ISIN Base level index exceptional and date trading circumstances AEX® based AEXLV AEX® Leverage AEX® 2 Suspend if Underlying QS0011095898 1,000 at Index < 75% of close 31Dec2002 of previous day AEXNL AEX® Leverage AEX® NR 2 Suspend if Underlying QS0011216205 1,000 at NR Index < 75% of close 31Dec2002 of previous day AEXTL AEX® Leverage AEX® GR 2 Suspend if Underlying QS0011179239 1,000 at GR Index < 75% of close 31Dec2002 of previous day AEX3L AEX® NR 3 Reset if Underlying QS0011230115 10,000 at AEX® X3 Leverage Index < 85% of close 31Dec2008 NR of previous day.