Washington State Legislature Olympia, WA 98504-0482

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

King County Official Local Voters' Pamphlet

August 2, 2016 Primary and Special Election King County Official Local Voters’ Pamphlet Your ballot will arrive by July 18 206-296-VOTE (8683) | kingcounty.gov/elections Reading the local From the voters’ pamphlet Director Why are there measures in the local voters’ pamphlet that are not on my ballot? Dear Friends. The measures on your ballot refl ect the districts in which you are registered to This is a big year for King County Elections. To vote. The local voters’ pamphlet may cover start, we are on track to hit 10 million ballots multiple districts and include measures counted without a single discrepancy this fall. outside of your districts. We expect to process over 1 million ballots this November alone. What is the order of candidates in the local voters’ pamphlet? I’m eager to continue our track record of transparency and accuracy – especially in light of Candidates in the local voters’ pamphlet this year’s Presidential Election – and I am also appear in the order they will appear on the excited about several projects that will mean ballot. transformative change for elections. For this Primary Election you will now have access to Are candidate statements fact checked 29 permanent ballot drop boxes that are open before they are published? 24-hours-a-day. November will see that number No. King County Elections is not responsible increase to 43 ballot drop boxes, meaning that for the content or accuracy of the 91.5% of King County residents will live within 3 statements, and we print them exactly as miles of a drop-off location. -

Microsoft Corporate Political Contributions H2 2012 July 1, 2012 – December 31, 2012

Microsoft Corporate Political Contributions H2 2012 July 1, 2012 – December 31, 2012 Name State Amount Apple for Kansas Senate KS $ 250 Armstrong Campaign Committee WA $ 700 Barbara Bailey for State Senate WA $ 600 Bob Hasegawa for State Senate WA $ 400 Brad Owen for Lt. Governor WA $ 500 Breaux for Indiana IN $ 250 Brownback for Governor KS $ 1,000 Bruce Chandler Campaign Committee WA $ 700 Bruce for Kansas Senate KS $ 250 Burgess for Kansas House KS $ 250 Burroughs for Kansas House KS $ 200 Campaign of Doug Holder FL $ 500 Carlin Yoder 2008 IN $ 250 Carlson for Kansas House KS $ 200 Cathy Dahlquist Campaign Committee WA $ 500 Chris Dorworth for State House District 29 FL $ 500 Citizens for Andy Hill (2014) WA $ 400 Citizens for Christopher Hurst WA $ 500 Citizens for Jim McIntire WA $ 500 Citizens for Karen Fraser WA $ 400 Citizens for Kevin Ranker WA $ 500 Citizens for Kim Wyman WA $ 1,000 Citizens for Marcie Maxwell WA $ 400 Citizens for Merritt IN $ 250 Citizens for Mike Carrell WA $ 700 Citizens for Ruth Kagi WA $ 400 Citizens for Steve Litzow WA $ 700 Citizens to Elect Larry Seaquist WA $ 500 Citizens to Re-Elect Lt. Governor Brad Owen WA $ 500 Colgan for Senate VA $ 500 Committee to Elect Brian C. Bosma IN $ 500 Committee to Elect Bruce Dammeier WA $ 500 Committee to Elect Cary Condotta WA $ 500 Committee to Elect Charles Ross WA $ 400 Committee to Elect Heath VanNatter IN $ 250 Committee to Elect Jim Hargrove WA $ 400 Committee to Elect Katrina Asay WA $ 400 Committee to Elect Linda Lawson IN $ 250 Committee to Elect Tim Lanane -

Elway Poll: Two-Thirds of Washingtonians Support Raising Tobacco Sale Age to 21

atg.wa.gov http://www.atg.wa.gov/news/news-releases/elway-poll-two-thirds-washingtonians-support-raising-tobacco-sale-age-21 Elway Poll: Two-thirds of Washingtonians support raising tobacco sale age to 21 Attorney General Bob Ferguson speaks at a press conference announcing an Elway Poll showing overwhelming support among Washingtonians for raising the purchase age for tobacco. Poll finds widespread bipartisan support for AG legislative proposal to combat youth smoking OLYMPIA — A Stuart Elway poll released today shows an overwhelming 65 percent of Washingtonians support raising the sale age of tobacco to 21. This result shows clear public support for Washington State Attorney General Bob Ferguson’s proposal to raise the legal age to purchase tobacco and vapor products to 21. The poll, commissioned by the Campaign for Tobacco-Free Kids and issued by Elway Research, an independent research firm, surveyed 500 registered voters in Washington state from Dec. 28-30, 2015. The results show strong support among both men and women and in every region of the state. Support in Eastern Washington (66 percent) was similar to support in Western Washington (70 percent). Additionally, the poll found strong support across political ideology, with 66 percent of Republicans and 72 percent of Democrats supporting increasing the tobacco sale age. “Smoking is the number one cause of preventable death in the United States,” said Ferguson. “Elway’s poll proves Washingtonians agree: It is time to make this common-sense change to state law and save kids’ lives.” Washington has long been at the forefront of the fight to protect youth from the dangers of smoking . -

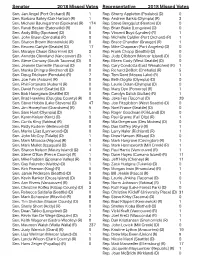

Senator 2018 Missed Votes Representative 2018 Missed Votes Sen

Senator 2018 Missed Votes Representative 2018 Missed Votes Sen. Jan Angel (Port Orchard) (R) 1 Rep. Sherry Appleton (Poulsbo) (D) 0 Sen. Barbara Bailey (Oak Harbor) (R) 1 Rep. Andrew Barkis (Olympia) (R) 3 Sen. Michael Baumgartner (Spokane) (R) 174 Rep. Steve Bergquist (Renton) (D) 0 Sen. Randi Becker (Eatonville) (R) 0 Rep. Brian Blake (Longview) (D) 0 Sen. Andy Billig (Spokane) (D) 0 Rep. Vincent Buys (Lynden) (R) 1 Sen. John Braun (Centralia) (R) 0 Rep. Michelle Caldier (Port Orchard) (R) 1 Sen. Sharon Brown (Kennewick) (R) 0 Rep. Bruce Chandler (Granger) (R) 1 Sen. Reuven Carlyle (Seattle) (D) 17 Rep. Mike Chapman (Port Angeles) (D) 0 Sen. Maralyn Chase (Shoreline) (D) 3 Rep. Frank Chopp (Seattle) (D) 0 Sen. Annette Cleveland (Vancouver) (D) 1 Rep. Judy Clibborn (Mercer Island) (D) 0 Sen. Steve Conway (South Tacoma) (D) 0 Rep. Eileen Cody (West Seattle) (D) 0 Sen. Jeannie Darneille (Tacoma) (D) 0 Rep. Cary Condotta (East Wenatchee) (R) 1 Sen. Manka Dhingra (Redmond) (D) 0 Rep. Richard DeBolt (Chehalis) (R) 5 Sen. Doug Ericksen (Ferndale) (R) 7 Rep. Tom Dent (Moses Lake) (R) 1 Sen. Joe Fain (Auburn) (R) 0 Rep. Beth Doglio (Olympia) (D) 0 Sen. Phil Fortunato (Auburn) (R) 0 Rep. Laurie Dolan (Olympia) (D) 0 Sen. David Frockt (Seattle) (D) 0 Rep. Mary Dye (Pomeroy) (R) 1 Sen. Bob Hasegawa (Seattle) (D) 0 Rep. Carolyn Eslick (Sultan) (R) 1 Sen. Brad Hawkins (Douglas County) (R) 0 Rep. Jake Fey (Tacoma) (D) 29 Sen. Steve Hobbs (Lake Stevens) (D) 47 Rep. Joe Fitzgibbon (West Seattle) (D) 0 Sen. -

Gun Responsibility Scorecard !

Paid for by Alliance for Gun Responsibility | PO Box 21712 | Seattle, WA 98111 | (206) 659-6737 | [email protected] Prsrt Std US Postage PAID Publishers Mailing Service UNPRECEDENTED PROGRESS IN 2017 In 2017, a record number of bi-partisan legislators sponsored gun responsibility legislation. Two of our priority bills, including Law Enforcement and Victim Safety, passed with overwhelming majorities and have been signed into law. Looking to the future, we need to build on this momentum in partnership with our legislative champions, to create a gun responsibility majority in the Legislature and pass commonsense laws that help make our communities and families safe. THANK YOU TO OUR STARS! These Legislators Were True Leaders In Prime Sponsoring Gun Responsibility Legislation. Sen. Jamie Pedersen Sen. Patty Kudererr Sen. David Frockter Sen. Guy Palumboer 2017 Rep. Ruth Kagi Rep. Laurie Jinkins Rep. Drew Hansen Rep. Dave Hayes Rep. Tann Senn To Learn More Or Get Involved, Visit GUN RESPONSIBILITY gunresponsibility.org SCORECARD Paid for by Alliance for Gun Responsibility | PO Box 21712 | Seattle, WA 98111 | (206) 659-6737 | [email protected] 2017 GUN RESPONSIBILITY Senator LD VOTE Sponsorship Legislative Community Overall Grade State Representative LD VOTE Sponsorship Legislative Community Overall Grade State Representative LD VOTE Sponsorship Legislative Community Overall Grade Grade Grade Grade Grade Grade Trajectory Grade Grade Grade Grade Grade Trajectory Grade Grade Grade Grade Grade Trajectory LEGISLATIVE SCORECARD Guy Palumbo 1 100.00% 15.00 15.00 15.00 A+ n/a Derek Stanford 1 100.00% 13.50 14.25 15.00 A Joyce McDonald 25 100.00% 15.00 15.00 15.00 D n/a Randi Becker 2 100.00% N/A 9.00 0.00 C Shelley Kloba 1 100.00% 12.75 14.25 14.25 A n/a Melanie Stambaugh 25 100.00% N./A 0.00 0.00 D Andy Billig 3 100.00% 14.25 14.40 14.25 A Andrew Barkis 2 100.00% N/A 9.00 0.00 C n/a Michelle Caldier 26 100.00% N/A 7.50 9.00 B 2017 LEGISLATOR GRADES – Legislative leadership Mike Padden 4 100.00% N/A 9.00 0.00 C J.T. -

May 6, 2015 2 May 6, 2015 the Honorable Mark Schoesler, Senate

May 6, 2015 2 May 6, 2015 The Honorable Mark Schoesler, Senate Majority Leader The Honorable Frank Chopp, Speaker of the House The Honorable Sharon Nelson, Senate Democratic Leader The Honorable Pat Sullivan, House Majority Leader The Honorable Andy Hill, Ways & Means Chair The Honorable Dan Kristiansen, House Minority Leader The Honorable Jim Hargrove, Ways & Means Ranking Member The Honorable Ross Hunter, Appropriations Chair The Honorable John Braun, Ways & Means Vice Chair The Honorable Bruce Chandler, Appropriations Ranking Member The Honorable Ann Rivers, Majority Whip The Honorable Reuven Carlyle, Finance Chair The Honorable Mark Mullet, Democratic Assistant Whip The Honorable Eileen Cody, Health Care & Wellness Chair Dear Legislators; On behalf of Washington’s 281 cities, we are writing to urge your quick action on HB 2136. This proposal includes numerous important provisions that will provide greater clarity to cities and assist the State’s emerging legal marijuana market. In particular, cities ask for your assistance with the following provisions in the bill: • Local Flexibility: Cities support the provisions in Section 301 for local flexibility to adjust the 1,000 foot buffer between retailers and certain sensitive uses. This flexibility will help cities better site business, while still meeting the public safety needs for their communities. • Opposition to pre-emption: Cities strongly oppose the inclusion of a public vote requirement prior to enacting a prohibition on marijuana businesses. This is a clear pre-emption of existing local regulatory authority. It is also inconsistent with the language of I-502 and at odds with recent court decisions and the state’s Attorney General Opinion. -

First Day, January 10, 2005 Fifty Ninth Legislature

FIRST DAY, JANUARY 10, 2005 1 FIFTY NINTH LEGISLATURE - REGULAR SESSION FIRST DAY House Chamber, Olympia, Monday, January 10, 2005 The House was called to order at 12:00 Noon by Chief Legislature of the State of Washington Clerk Nafziger. Olympia, Washington The flag was escorted to the rostrum by the Joint Service Mr. Speaker: Color Guard. The Chief Clerk led the Chamber in the Pledge of Allegiance. The House observed a moment of silence for the I, Sam Reed, Secretary of State of the State of Washington, do victims of the Southeast Asian tsunami. Prayer was offered by hereby certify that the following is full, true, and correct list of Father Bob Kenney, St. Michael's Parish, Olympia. persons elected to the office of State Representative at the State General Election held in the State of Washington on the "Almighty and eternal God, we ask you to bless the people second day of November, 2004, as shown by the official of the State of Washington with security, prosperity, generosity returns of said election now on file in the office of the and peace. Secretary of State: We pray for he members of this legislature, who are entrusted to guard our political welfare. May they be enabled REPRESENTATIVES ELECTED NOVEMBER 2, 2004 to discharge their duties with honesty and ability. May the light of divine wisdom direct the deliberations of these men DIS COUNTIES NAME and women, and be evident in all of their proceedings. 1 King (part), Snohomish (part) Al O'Brien (D) We pray that these representatives will be blessed with Mark Ericks (D) 2 Pierce (part), Thurston (part) Jim McCune (R) wisdom and strength of purpose in the exercise of their high Tom Campbell (R) office. -

State Small Dollar Rule Comments

State Small Dollar Rule Comments All State Commenters State Associations Florida, Georgia, Indiana, Kansas, Louisiana, Nebraska, Nevada, North Dakota, Oklahoma, • AL // Alabama Consumer Finance Association South Carolina, South Dakota, Tennessee, Texas, • GA // Georgia Financial Services Association Utah, West Virginia, Wisconsin • ID // Idaho Financial Services Association • IL // Illinois Financial Services Association State Legislators • IN // Indiana Financial Services Association • MN // Minnesota Financial Services Association • MO // Missouri Installment Lenders Association; • AZ // Democratic House group letter: Rep. Stand Up Missouri Debbie McCune Davis, Rep. Jonathan Larkin, • NC // Resident Lenders of North Carolina Rep. Eric Meyer, Rep. Rebecca Rios, Rep. Richard • OK // Independent Finance Institute of Andrade, Rep. Reginald Bolding Jr., Rep. Ceci Oklahoma Velasquez, Rep. Juan Mendez, Rep. Celeste • OR // Oregon Financial Services Association Plumlee, Rep. Lela Alston, Rep. Ken Clark, Rep. • SC // South Carolina Financial Services Mark Cardenas, Rep. Diego Espinoza, Rep. Association Stefanie Mach, Rep. Bruce Wheeler, Rep. Randall • TN // Tennessee Consumer Finance Association Friese, Rep. Matt Kopec, Rep. Albert Hale, Rep. • TX // Texas Consumer Finance Association Jennifer Benally, Rep. Charlene Fernandez, Rep. • VA // Virginia Financial Services Association Lisa Otondo, Rep. Macario Saldate, Rep. Sally Ann • WA // Washington Financial Services Association Gonzales, Rep. Rosanna Gabaldon State Financial Services Regulators -

WOVE Legislative Update for Career and Technical Education

WOVE Legislative Update for Career and Technical Education Legislative Session Week 4 - 2016 February 5, 2016 WOVE…Representing the Career and Technical Education field through advocacy activities, which promotes the value of CTE and the policies that are needed to support CTE practitioners, advance the field, and improve student learning. To subscribe to the WOVE Legislative Update or to view past issues, please click here. Tim Knue, Executive Director Washington Association for Career and Technical Education PO Box 315, Olympia WA 98507-0315 Tel: 360-786-9286 / Cell: 360-202-5297 / Fax: 360-357-1491 / [email protected] / www.wa-acte.org Send a personal email to [email protected] to sign up for the “CTE Advocacy Updates” CTE & SC MSOC Funding Bills: February 5 is the short session Policy Cutoff Day in the state legislature. Policy bills either pass by today in their House or Senate committee origin or fail to move and die, unless revived in end-of-session political decisions…AKA NTIB…necessary to implement the budget. Next on to the fiscal committee cutoff day in house of origin on Tuesday, February 9 and then floor of origin cutoff on February 17. http://leg.wa.gov/legislature/pages/cutoff.aspx There is never a cutoff for advocacy work - voters/constituents keep calling and emailing legislators for good policy and budget decisions. That being said… The CTE MSOC Funding bill SB 6415 - Concerning career and technical education materials, supplies, and operating costs did not make it out of the Early Learning and K-12 Education committee in the Senate this week. -

Washington St Ate Senate

MEmBERS OF THE Washington State Senate 2011 Lt. Gov. Brad Owen 62nd LEGISLATURE President of the Senate (D) Senator Michael Baumgartner Senator Randi Becker Senator Don Benton Senator Lisa J. Brown Senator Mike Carrell Senator Maralyn Chase Senator Steve Conway 6th District (R) 2nd District (R) 17th District (R) 3rd District (D) 28th District (R) 32nd District (D) 29nd District (D) Senator Jerome Delvin Senator Tracey J. Eide Senator Doug Ericksen Senator Joe Fain Senator Karen Fraser Senator James E. Hargrove Senator Nick Harper 8th District (R) 30th District (D) 42nd District (R) 47th District (R) 22nd District (D) 24th District (D) 38th District (D) Senator Brian Hatfield Senator Mary Margaret Senator Mike Hewitt Senator Andy Hill Senator Steve Hobbs Senator Janéa Holmquist Senator Jim Honeyford 19th District (D) Haugen 16th District (R) 45th District (R) 44th District (D) 13th District (R) 15th District (R) 10th District (D) Senator Jim Kastama Senator Karen Keiser Senator Derek Kilmer Senator Curtis King Senator Adam Kline Senator Jeanne Kohl-Welles Senator Steve Litzow 25th District (D) 33rd District (D) 26th District (D) 14th District (R) 37th District (D) 36th District (D) 41st District (R) Senator Rosemary McAuliffe Senator Bob McCaslin Senator Bob Morton Senator Ed Murray Senator Sharon Nelson Senator Linda Evans Parlette Senator Cheryl Pflug 1st District (D) 4th District (R) 7th District (R) 43rd District (D) 34th District (D) 12th District (R) 5th District (R) Senator Margarita Prentice Senator Craig Pridemore Senator Kevin Ranker Senator Debbie Regala Senator Pam Roach Senator Phil Rockefeller Senator Mark Schoesler 11th District (D) 49th District (D) 40th District (D) 27th District (D) 31st District (R) 23rd District (D) 9th District (R) Senator Tim Sheldon Senator Paull H. -

2016 Lilly Report of Political Financial Support

16 2016 Lilly Report of Political Financial Support 1 16 2016 Lilly Report of Political Financial Support Lilly employees are dedicated to innovation and the discovery of medicines to help people live longer, healthier and more active lives, and more importantly, doing their work with integrity. LillyPAC was established to work to ensure that this vision is also shared by lawmakers, who make policy decisions that impact our company and the patients we serve. In a new political environment where policies can change with a “tweet,” we must be even more vigilant about supporting those who believe in our story, and our PAC is an effective way to support those who share our views. We also want to ensure that you know the story of LillyPAC. Transparency is an important element of our integrity promise, and so we are pleased to share this 2016 LillyPAC annual report with you. LillyPAC raised $949,267 through the generous, voluntary contributions of 3,682 Lilly employees in 2016. Those contributions allowed LillyPAC to invest in 187 federal candidates and more than 500 state candidates who understand the importance of what we do. You will find a full financial accounting in the following pages, as well as complete lists of candidates and political committees that received LillyPAC support and the permissible corporate contributions made by the company. In addition, this report is a helpful guide to understanding how our PAC operates and makes its contribution decisions. On behalf of the LillyPAC Governing Board, I want to thank everyone who has made the decision to support this vital program. -

2017 Regular Session

Legislative Hotline & ADA Information Telephone Directory and Committee Assignments of the Washington State Legislature Sixty–fifth Legislature 2017 Regular Session Washington State Senate Cyrus Habib . .President of the Senate Tim Sheldon . .President Pro Tempore Jim Honeyford . Vice President Pro Tempore Hunter G . Goodman . Secretary of the Senate Pablo G . Campos . .Deputy Secretary of the Senate Washington House of Representatives Frank Chopp . Speaker Tina Orwall . Speaker Pro Tempore John Lovick . Deputy Speaker Pro Tempore Bernard Dean . Chief Clerk Nona Snell . Deputy Chief Clerk 65th Washington State Legislature 1 Members by District District 1 District 14 Sen . Guy Palumbo, D Sen . Curtis King, R Rep . Derek Stanford, D Rep . Norm Johnson, R Rep . Shelley Kloba, D Rep . Gina R . McCabe, R District 2 District 15 Sen . Randi Becker, R Sen . Jim Honeyford, R Rep . Andrew Barkis, R Rep . Bruce Chandler, R Rep . J T. Wilcox, R Rep . David Taylor, R District 3 District 16 Sen . Andy Billig, D Sen . Maureen Walsh, R Rep . Marcus Riccelli, D Rep . William Jenkin, R Rep . Timm Ormsby, D Rep . Terry Nealey, R District 4 District 17 Sen . Mike Padden, R Sen . Lynda Wilson, R Rep . Matt Shea, R Rep . Vicki Kraft, R Rep . Bob McCaslin, R Rep . Paul Harris, R District 5 District 18 Sen . Mark Mullet, D Sen . Ann Rivers, R Rep . Jay Rodne, R Rep . Brandon Vick, R Rep . Paul Graves, R Rep . Liz Pike, R District 6 District 19 Sen . Michael Baumgartner, R Sen . Dean Takko, D Rep . Mike Volz, R Rep . Jim Walsh, R Rep . Jeff Holy, R Rep . Brian Blake, D District 7 District 20 Sen .