Classement-Des-Cabinets-De-Conseil-Par-Secteur.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Capture Consulting Offers Aligning Your Fit for Consulting Session 2 | February 19, 2019

Capture Consulting Offers Aligning Your Fit for Consulting Session 2 | February 19, 2019 1 Session Date Topic / Outline Kickoff | Building a Fit for Consulting • Consulting / Career Path • Entrance Criteria 1 Feb 5 • Your Fit Assessment / Spark / Career Goals • Gaps for Advanced Degree/Non-MBA Candidates • Building Business Acumen and Case Skils WE ARE HERE Aligning Fit to Consulting FIrms • Industry Overview • Consulting Firm Landscape - Firms, Specialties | Big vs. Boutique WE ARE HERE Feb 19 • Approach to Firm Research 2 • Assessing and Aligning Your FIT • Networking as Research • Case Interview Preview Get the Interview • Resume Deep Dive Summer program 3 Mar 5 • Cover Letter Deep Dirve • Networking and Importance/Integration application dates are posted! Applications <<1-1 Resume Reviews! Noon-5pm>> due March-April. Get the Offer: Part 1 • Case Interview Practice Methods 4 Mar 19 • Experience Interview - Overview • Building Your Story Matrix • Creating SOAR Outlines Get the Offer: Part 2 • Resume Walkthrough Case Workshop Apr 2 • Common Questions April 28 | 10am-6pm 5 • Challenging Questions $50 • Wrap-up/Next Steps 2 TO ACCESS SESSION MATERIALS AND RESOURCES GO TO www.archcareerpartners.com/uchicagogcc-2019 3 AGENDA CCO Session 2| Aligning Your Fit Context Fit Activities u Consulting industry u Approach to firm u Networking as overview research research u Consulting firm u Assessing/aligning u Case interview landscape your fit preview 4 Context 5 The rise of the “knowledge” profession James O. McKinsey Management Consulting 6 Establishing -

IN TAX LEADERS WOMEN in TAX LEADERS | 4 AMERICAS Latin America

WOMEN IN TAX LEADERS THECOMPREHENSIVEGUIDE TO THE WORLD’S LEADING FEMALE TAX ADVISERS SIXTH EDITION IN ASSOCIATION WITH PUBLISHED BY WWW.INTERNATIONALTAXREVIEW.COM Contents 2 Introduction and methodology 8 Bouverie Street, London EC4Y 8AX, UK AMERICAS Tel: +44 20 7779 8308 4 Latin America: 30 Costa Rica Fax: +44 20 7779 8500 regional interview 30 Curaçao 8 United States: 30 Guatemala Editor, World Tax and World TP regional interview 30 Honduras Jonathan Moore 19 Argentina 31 Mexico Researchers 20 Brazil 31 Panama Lovy Mazodila 24 Canada 31 Peru Annabelle Thorpe 29 Chile 32 United States Jason Howard 30 Colombia 41 Venezuela Production editor ASIA-PACIFIC João Fernandes 43 Asia-Pacific: regional 58 Malaysia interview 59 New Zealand Business development team 52 Australia 60 Philippines Margaret Varela-Christie 53 Cambodia 61 Singapore Raquel Ipo 54 China 61 South Korea Managing director, LMG Research 55 Hong Kong SAR 62 Taiwan Tom St. Denis 56 India 62 Thailand 58 Indonesia 62 Vietnam © Euromoney Trading Limited, 2020. The copyright of all 58 Japan editorial matter appearing in this Review is reserved by the publisher. EUROPE, MIDDLE EAST & AFRICA 64 Africa: regional 101 Lithuania No matter contained herein may be reproduced, duplicated interview 101 Luxembourg or copied by any means without the prior consent of the 68 Central Europe: 102 Malta: Q&A holder of the copyright, requests for which should be regional interview 105 Malta addressed to the publisher. Although Euromoney Trading 72 Northern & 107 Netherlands Limited has made every effort to ensure the accuracy of this Southern Europe: 110 Norway publication, neither it nor any contributor can accept any regional interview 111 Poland legal responsibility whatsoever for consequences that may 86 Austria 112 Portugal arise from errors or omissions, or any opinions or advice 87 Belgium 115 Qatar given. -

2021 Indirect Tax Leaders Guide and May Not Be Used for Any Other Purpose

INDIRECT TAX LEADERS THECOMPREHENSIVEGUIDE TO THE WORLD’S LEADING INDIRECT TAX ADVISERS NINTH EDITION IN ASSOCIATION WITH PUBLISHED BY WWW.INTERNATIONALTAXREVIEW.COM BECOME PART OF THE ITR COMMUNITY. CONNECT WITH US TODAY. Facebook “Like” us on Facebook at www.facebook.com/internationaltaxreview f and connect with our editorial team and fellow readers. LinkedIn Join our group, International Tax Review, to meet your peers in and get incomparable market coverage. Twitter Follow us at @IntlTaxReview for exclusive research and t ranking insight, commentary, analysis and opinions. To subscribe, contact: Jack Avent Tel: +44 (0) 20 7779 8379 | Email: [email protected] www.internationaltaxreview.com Contents 2 Introduction and methodology 8 Bouverie Street, London EC4Y 8AX, UK Tel: +44 20 7779 8308 AMERICAS Fax: +44 20 7779 8500 Editor, World Tax and World TP 11 Argentina 18 Costa Rica Jonathan Moore 11 Bolivia 18 Ecuador 11 Brazil 19 Mexico Researchers 14 Canada 19 Peru Jason Howard Lovy Mazodila 17 Chile 20 United States Annabelle Thorpe 18 Colombia 21 Uruguay Production editor João Fernandes ASIA-PACIFIC Business development team 30 Australia 44 Philippines Margaret Varela-Christie 32 China 45 Singapore Raquel Ipo 32 Hong Kong SAR 46 South Korea Alexandra Strick 33 India 46 Sri Lanka Managing director, LMG Research 39 Indonesia 46 Taiwan Tom St. Denis 41 Japan 47 Thailand © Euromoney Trading Limited, 2020. The copyright of all 42 Malaysia 47 Vietnam editorial matter appearing in this Review is reserved by the 43 New Zealand publisher. No matter contained herein may be reproduced, duplicated EUROPE, MIDDLE EAST & AFRICA or copied by any means without the prior consent of the 63 Austria 77 Netherlands holder of the copyright, requests for which should be 63 Azerbaijan 80 Norway addressed to the publisher. -

Devoir De Vigilance: Reforming Corporate Risk Engagement

Devoir de Vigilance: Reforming Corporate Risk Engagement Copyright © Development International e.V., 2020 ISBN: 978-3-9820398-5-5 Authors: Juan Ignacio Ibañez, LL.M. Chris N. Bayer, PhD Jiahua Xu, PhD Anthony Cooper, J.D. Title: Devoir de Vigilance: Reforming Corporate Risk Engagement Date published: 9 June 2020 Funded by: iPoint-systems GmbH www.ipoint-systems.com 1 “Liberty consists of being able to do anything that does not harm another.” Article 4, Declaration of the Rights of the Man and of the Citizen of 1789, France 2 Executive Summary The objective of this systematic investigation is to gain a better understanding of how the 134 confirmed in-scope corporations are complying with – and implementing – France’s progressive Devoir de Vigilance law (LOI n° 2017-399 du 27 Mars 2017).1 We ask, in particular, what subject companies are doing to identify and mitigate social and environmental risk/impact factors in their operations, as well as for their subsidiaries, suppliers, and subcontractors. This investigation also aims to determine practical steps taken regarding the requirements of the law, i.e. how the corporations subject to the law are meeting these new requirements. Devoir de Vigilance is at the legislative forefront of the business and human rights movement. A few particular features of the law are worth highlighting. Notably, it: ● imposes a duty of vigilance (devoir de vigilance) which consists of a substantial standard of care and mandatory due diligence, as such distinct from a reporting requirement; ● sets a public reporting requirement for the vigilance plan and implementation report (compte rendu) on top of the substantial duty of vigilance; ● strengthens the accountability of parent companies for the actions of subsidiaries; ● encourages subject companies to develop their vigilance plan in association with stakeholders in society; ● imposes civil liability in case of non-compliance; ● allows stakeholders with a legitimate interest to seek injunctive relief in the case of a violation of the law. -

Economic Framework Sourcing List

Pan-Regulators’ Framework for Economic, Financial & Related Consultancy Services Final Sourcing Lists 2015 Introduction The purpose of this document is to give an overview of the final sourcing lists of the new Pan-Regulator’s Framework for Economic, Financial and Related Consultancy Services and to inform users of the range and choice of suppliers available. The new Framework will come into effect from 1st September 2015 and will be valid until 31st August 2018 (with a one year extension option). Lot 1. Energy Advice Relating to Economic and Environmental Areas This Lot covers consultancy on all aspects of specialised economic and environmental advice relating to energy. Advice may relate to establishment of suitable strategies, policies, processes and organisation of economic responsibilities within an organisation. Sub-Lot 1A. Regulatory and Incentive Design Ability to analyse various proposals in relation to regulatory policy development balancing consumer interest over short term and over the longer term Understanding of financial and economic incentives to encourage implementation of effective and efficient programmes by the company Understanding of the historical development of the current GB energy market arrangements, and ability to draw implications for policy design using relevant economic models. Ability to review alternative options and provide detailed cost benefit analysis Economic assessment of options so that the incentive scheme satisfies the economic efficiency criteria for the users of the system Development -

Baromètre Edhec - Cadremploi Jeunes Diplômés Master

BAROMÈTRE EDHEC - CADREMPLOI JEUNES DIPLÔMÉS MASTER 23ème édition Juin 2016 BAROMÈTRE EDHEC - CADREMPLOI JEUNES DIPLÔMÉS MASTER Quelles sont les tendances du marché de l’emploi des jeunes diplômés de niveau Master ? Voilà la question à laquelle nous répondons 3 fois par an depuis janvier 2009. Cette 23ème édition du baromètre EDHEC est réalisée en collaboration avec CADREMPLOI, premier site emploi privé pour les cadres et les dirigeants en France. EDHEC NewGen Talent Centre © & CADREMPLOI - Juin 2016 - 23ème édition du BAROMÈTRE EDHEC - CADREMPLOI 2 150 ENTREPRISES PARTICIPENT AU BAROMÈTRE EDHEC - CADREMPLOI ABASE - ACCENTURE - ADVENTS - AELIA - LS TRAVEL RETAIL - AEROPORTS DE LA COTE D'AZUR - AIR LIQUIDE GROUPE - ALINEA - ALTER&GO - APPROACH PEOPLE - RECRUITMENT - ARKEMA - ARM France - ARROW ECS - ASPEN - ATOS - AUCHAN - AXA - BANQUE DE FRANCE - BANQUE FRANCAISE COMMERCIAL OCEAN INDIEN - BARCLAYS - BDO ADVISORY - BETC - BILLIERES BUSINESS SCHOOL - BURSON MARSTELLER - CAISSE D'EPARGNE COTE D'AZUR - CAPGEMINI CONSULTING - CAPTALENTS - CARREFOUR - CARTIER - CASTORAMA - CCI NICE COTE D'AZUR - CGI BUSINESS CONSULTING - CHAMPAGNE MOET - HENNESSY & CHANDON MHCS - CHARLES RICHARDSON - CHECKPOINT SYSTEMS FRANCE SAS - COCA COLA - COFIDIS PARTICIPATIONS GROUPE - COGEDIS - COLOMBUS CONSULTING - CONVICTIONS RH - CREDIT AGRICOLE - CREDIT DU NORD - CSC COMPUTER SCIENCES - DAMARTEX - DATACET - DELFOSSE - DELOITTE - DFDS SEAWAYS - EIGHT ADVISORY - ENESCO - EUROFEU - EUROPACORP TELEVISION - EUROTEKNIKA - EXPER - EXXON CHEMICAL FRANCE - EY GROUPE - FAURECIA -

EVALUATION of the RISKS of COLLECTIVE DOMINANCE in the AUDIT INDUSTRY in FRANCE Olivier Billard* Bredin Prat Marc Ivaldi* Toulou

EVALUATION OF THE RISKS OF COLLECTIVE DOMINANCE IN THE AUDIT INDUSTRY IN FRANCE Olivier Billard* Bredin Prat Marc Ivaldi* Toulouse School of Economics Sébastien Mitraille* Toulouse Business School (University of Toulouse) May 18, 2011 (revised June 7, 2012) Summary: The financial crisis drew attention to the crucial role of transparency and the independence of financial certification intermediaries, in particular, statutory auditors. Now any anticompetitive practice involving coordinated increases in prices or concomitant changes in quality that impacts financial information affects the effectiveness of this intermediation. It is therefore not surprising that the competitive analysis of the audit market is a critical factor in regulating financial systems, all the more so as this market is marked by various barriers to entry, such as the incompatibility of certification tasks with the preparation of financial statements or consulting, the expertise on (and the ability to apply) international standards for the presentation of financial information, the need to attract top young graduates, the prohibition of advertising, or the two-sided nature of this market where the quality of financial information results from the interaction between the reputation of auditors and audited firms. Against this backdrop, we propose a legal and economic study of the risks of collective dominance in the statutory audit market in France using the criteria set by Airtours case and, in particular, by analyzing how regulatory obligations incumbent on statutory auditors may favour the appearance of tacit collusion. Our analysis suggests that nothing prevents collective dominance of the auditors of the Big Four group in France to exist, which is potentially detrimental to the economy as a whole as the audit industry may fail to provide the optimal level of financial information. -

Marsh & Mclennan Companies 2009 Notice of Annual Meeting and Proxy

Marsh & McLennan Companies Notice of Annual Meeting 2009 and Proxy Statement Important Notice Regarding the Availability of Proxy Materials for the MMC Annual Meeting of Stockholders to be held on May 21, 2009: This proxy statement and MMC’s 2008 Annual Report are available at http://www.proxy09.mmc.com. Dear MMC Stockholder: You are cordially invited to attend the annual meeting of stockholders of Marsh & McLennan Companies, Inc. The meeting will be held at 10:00 a.m. on Thursday, May 21, 2009 in the second floor auditorium at 1221 Avenue of the Americas, New York, New York. In addition to voting on the matters described in this proxy statement, we will use the meeting as an opportunity to report on MMC’s recent activities. You will be able to ask questions, and to meet your company’s directors and senior executives. Whether or not you plantoattend the annual meeting, your vote is important and we urge you to participate in electing directors and deciding the other items on the agenda for the annual meeting. You will find information on how to vote in the first section of this proxy statement. Very truly yours, BRIAN DUPERREAULT President & Chief Executive Officer April 2, 2009 MARSH & McLENNAN COMPANIES, INC. 1166 Avenue of the Americas New York, New York 10036-2774 NOTICE OF ANNUAL MEETING OF STOCKHOLDERS AND PROXY STATEMENT Time: 10:00 a.m. Local Time Date: May 21, 2009 Place: Second Floor Auditorium 1221 Avenue of the Americas New York, New York 10020 Purpose: 1. To elect four persons named in the accompanying proxy statement to serve as directors for a one-year term; 2. -

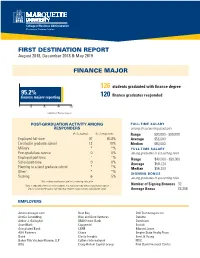

First Destination Report Finance Major

FIRST DESTINATION REPORT August 2018, December 2018 & May 2019 FINANCE MAJOR 126 students graduated with finance degree 95.2% finance majors reporting 120 finance graduates responded 0 50 75 100 150 175 200 number of finance majors POST-GRADUATION ACTIVITY AMONG FULL-TIME SALARY RESPONDERS among all accounting graduates # of students % of responses Range $30,000 - $90,000 Employed full-time 97 80.8% Average $58,600 Enrolled in graduate school 12 10% Median $60,000 Military * *% FULL-TIME SALARY Post-gradudate service 0 0% among graduates in accounting roles Employed part-time * *% Range $40,000 - $90,000 School part-time 0 0% Average $58,124 Planning to attend gradaute school * *% Median $56,250 Other1 * *% SIGNING BONUS Seeking 6 5% among graduates in accounting roles 1 Not seeking employment and not continuing education. *Data is reported when 5 or more students in a major pursued the post-graduation option. Number of Signing Bonuses 32 Data is collected through a self-reported student survey, faculty and LinkedIn input. Average Bonus $5,258 EMPLOYERS Americaneagle.com Best Buy Dell Technologies Inc. AndCo Consulting Blue and Gold Ventures Deloitte Arthur J. Gallagher BMO Harris Bank Dominium AssetMark Capgemini Ecolab Associated Bank CBRE Edward Jones AXA Partners Chase Empire State Realty Trust Baird Clarity Insights Ernst & Young Baker Tilly Virchow Krause, LLP Colliers International FDIC BDO Craig-Hallum Capital Group First Bank Financial Center EMPLOYERS (CONTINUED) First Business Financial Services Marshall & Stevens Scotiabank -

Consulting Firms List

Consulting Firms List Source: LinkedIn company search Company name # of employees Headquarters location Website Specific focus (summarized) A.T. Kearney 1001-5000 employees Chicago, IL http://atkearney.com/ Operations, strategy, technology ABeam Consulting 1001-5000 employees Houston, TX http://www.abeam.com/usa/eng/ Operations ABS Consulting 1001-5000 employees Houston, TX http://www.absconsulting.com Management Consulting Accenture 10,001+ employees Ireland http://www.accenture.com Operations, strategy, technology Accretive Solutions 1001-5000 employees Chicago, IL http://www.accretivesolutions.com/ Operations and technology Acquis Consulting Group 11-50 employees New York, NY http://www.acquisconsulting.com/home.html Operations, strategy, technology Added Value 501-1000 employees Los Angeles, CA http://www.added-value.com Marketing Alexander Proudfoot 201-500 employees Atlanta, GA http://www.alexanderproudfoot.com/home.aspx Operations AlixPartners 1001-5000 employees Detroit, MI http://www.alixpartners.com/EN/ Operations, strategy, technology Analysis Group 501-1000 employees Boston, MA http://www.analysisgroup.com/ Economics Apercu Global Inc 1001-5000 employees New York, NY http://apercuglobal.com/ Management Consulting Archstone Consulting 501-1000 employees Miami, Florida http://www.archstoneconsulting.com/ Strategy and operations Avascent 51-200 employees Washington, DC http://www.avascent.com/ Defense Axafina 1001-5000 employees Cheyenne, WY http://www.axafina.com/ Operations and technology Bain & Co 5001-10,000 employees Boston, -

Marsh & Mclennan Compa

Marsh & McLennan Compa- nies, Inc. Company Profile Reference Code: 4CAEBD48-6230-45D6-B417-1D1FCE24449C Publication Date: Jun 2007 www.datamonitor.com Datamonitor Europe Datamonitor Americas Datamonitor Germany Datamonitor Asia-Pacific Datamonitor Japan Charles House 245 Fifth Avenue Kastor & Pollux Room 2413-18, 24/F Aoyama Palacio Tower 11F 108-110 Finchley Road 4th Floor Platz der Einheit 1 Shui On Centre 3-6-7 Kita Aoyama London NW3 5JJ New York, NY 10016 60327 Frankfurt 6-8 Harbour Road Minato-ku United Kingdom USA Deutschland Hong Kong Tokyo 107 0061 Japan t: +44 20 7675 7000 t: +1 212 686 7400 t: +49 69 97503 119 t: +852 2520 1177 t: +813 5778 7532 f: +44 20 7675 7500 f: +1 212 686 2626 f: +49 69 97503 320 f: +852 2520 1165 f: +813 5778 7537 e: [email protected] e: [email protected] e: [email protected] e: [email protected] e: [email protected] ABOUT DATAMONITOR Datamonitor plc is a premium business information company specializing in industry analysis. We help our clients, 5000 of the world's leading companies, to address complex strategic issues. Through our proprietary databases and wealth of expertise, we provide clients with unbiased expert analysis and in-depth forecasts for six industry sectors: Automotive, Consumer Markets, Energy, Financial Services, Healthcare and Technology. Datamonitor maintains its headquarters in London and has regional offices in New York, Frankfurt, Hong Kong and Japan. Datamonitor's premium reports are based on primary research with industry panels and consumers. We gather information on market segmentation, market growth and pricing, competitors and products. -

"SOLIZE India Technologies Private Limited" 56553102 .FABRIC 34354648 @Fentures B.V

Erkende referenten / Recognised sponsors Arbeid Regulier en Kennismigranten / Regular labour and Highly skilled migrants Naam bedrijf/organisatie Inschrijfnummer KvK Name company/organisation Registration number Chamber of Commerce "@1" special projects payroll B.V. 70880565 "SOLIZE India Technologies Private Limited" 56553102 .FABRIC 34354648 @Fentures B.V. 82701695 01-10 Architecten B.V. 24257403 100 Grams B.V. 69299544 10X Genomics B.V. 68933223 12Connect B.V. 20122308 180 Amsterdam BV 34117849 1908 Acquisition B.V. 60844868 2 Getthere Holding B.V. 30225996 20Face B.V. 69220085 21 Markets B.V. 59575417 247TailorSteel B.V. 9163645 24sessions.com B.V. 64312100 2525 Ventures B.V. 63661438 2-B Energy Holding 8156456 2M Engineering Limited 17172882 30MHz B.V. 61677817 360KAS B.V. 66831148 365Werk Contracting B.V. 67524524 3D Hubs B.V. 57883424 3DUniversum B.V. 60891831 3esi Netherlands B.V. 71974210 3M Nederland B.V. 28020725 3P Project Services B.V. 20132450 4DotNet B.V. 4079637 4People Zuid B.V. 50131907 4PS Development B.V. 55280404 4WEB EU B.V. 59251778 50five B.V. 66605938 5CA B.V. 30277579 5Hands Metaal B.V. 56889143 72andSunny NL B.V. 34257945 83Design Inc. Europe Representative Office 66864844 A. Hak Drillcon B.V. 30276754 A.A.B. International B.V. 30148836 A.C.E. Ingenieurs en Adviesbureau, Werktuigbouw en Electrotechniek B.V. 17071306 A.M. Best (EU) Rating Services B.V. 71592717 A.M.P.C. Associated Medical Project Consultants B.V. 11023272 A.N.T. International B.V. 6089432 A.S. Watson (Health & Beauty Continental Europe) B.V. 31035585 A.T. Kearney B.V.