Comprehensive Annual Financial Report City of Temple, Texas

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

31295005193577.Pdf (3.496Mb)

WARD CARLTON MAYBORN: SILENT GIANT OF THE NEWSPAPER INDUSTRY by JAMES EDMOND CASON, B.S. A THESIS IN MASS COMMUNICATIONS Submitted to the Graduate Faculty of Texas Tech University in Partial Fulfillment of the Requirements for the Degree of MASTER OF ARTS Approved Accepted May, 1987 it\ /:- 90-~ N^, 1' C^' .. ^ TABLE OF CONTENTS CHAPTER I. INTRODUCTION 1 II. HARD TIllES AND THE LAUNCHING OF A CAREER ... 9 III. STARTING THE EVANSVILLE PRESS 16 IV. THE PUBLISHING HOUSE CONCEPT 31 V. MAYBORN LEAVES THE SCRIPPS ORGANIZATION ... 47 VI. STARTING THE CHICAGO SUN 54 VII. MAYBORN RETURNS TO TEXAS 61 VIII. SUMMARY 70 REFERENCES 75 11 CHAPTER I INTRODUCTION When Ward Carlton Mayborn was born October 10, 1879, the Civil War had been over for 14 years. The nation was experiencing the problems associated with healing the wounds of war while the age of the industrial revolution was dawning upon the nation. Thomas A. Edison in 1864 invented an automatic telegraph repeater, making possible the sending of mes sages over long distances (1, p. 587). In the early 1870s, less than 10 years before Mayborn's birth, a telegraph system was incorporated into the nation's fledgling railway system (1, p. 587). Edison started to work in his Menlo Park, New Jersey laboratory in 1876 (1, p. 587). It was not until Septem ber 4, 1882, when Mayborn was almost three years old, that New York City got its first electric street lights (2, p. 118) . In his book, The Rise of Industrial America, Page Smith detailed events taking place in the nation at the time of Mayborn's birth and during the next 20 years when Mayborn was receiving all the formal education he was to have and when he found himself, due to economic conditions of the time, looking for work. -

49818 19 1120031

Control Number: 49818 Item Number: 19 Addendum StartPage: 0 VANTAGE POINT ADVISORS, INC. Take aim. 180 State Stieet, Suite 225 Southlake, TX 76092 682 2377126 Greqorv E. Scheiq CFA, CEIV, CP~~JEIVU~FIWCIGX, 21~* www.vpadvlsors com Managing Director- Uti/itie*Pra¢tice Leader 180 State St., Suite 225, Southlake, TX 76092 SAN DIEGO [email protected] LOS ANGELES NEWYORK 214.254.4801 PORFLAND SEATTLE DALLAS EMPLOYMENT HISTORY February 2020 - Present Vantage Point Advisors Managing Director Providing valuation, expert testimony, and financial advisory services. Focus is business valuation, economic damages and forensic accounting testimony. September 2008 - February 2020 ValueScope, Inc. Principal Provided valuation, expert testimony, and financial advisory services with a focus on energy and regulated utility companies. Developed rate of return analyses and valued utility and energy assets. July 2008 - September 2008 Present Value Advisors, LLC Principal Formed Present Value Advisors to provide valuation, litigation support, and financial advisory services. July 2005 - June 2008 Kroll Associates, Inc. Senior Director Performed valuation analyses for transactions, financial reporting, tax, and other management requirements, and provided expert testimony for litigation support. Key focus was in the energy and utility sectors with larger clients. 2002 - July 2005 CBIZ Valuation Group, LLC, Managing Director - Southwest Region Ran the southwest region's valuation practice for approximately three and a half years. In that role, valued many types of businesses, business interests, and professional practices. 1997 - 2002 Deloitte Consulting Senior Manager: Utility Strategy Competency Led projects dealing with utility valuations, mergers and acquisition synergy analyses, real option analyses, strategic assessments, and complex regulatory issues. Served a wide variety of domestic and international clients, including companies in Canada, England, Republic of South Africa, Italy, Scotland, and Singapore. -

CONGRESSIONAL RECORD— Extensions Of

February 29, 2016 CONGRESSIONAL RECORD — Extensions of Remarks E247 SENATE REPUBLICAN SUPPORT OF into the Angus Heritage Foundation, served as to recognize a milestone anniversary in the life OBAMA’S SUPREME COURT NOMI- a member of the American Angus Association of Toledo’s Indiana Avenue Baptist Church. NATION for over 50 years, served as President of the This month the congregation has been cele- Colorado Cattle Feeders, and was presented brating its 70th anniversary with a series of HON. TERRI A. SEWELL with the CSU Leadership in Agriculture Award. special gatherings. I was privileged to join the OF ALABAMA Mr. Houston was involved with a number of congregation yesterday. IN THE HOUSE OF REPRESENTATIVES other organizations, where his limitless knowl- Founded by Reverend M. J. Stephenson in edge and service will always be remembered. February 1946, the congregation has been Monday, February 29, 2016 It is the hard work Mr. Houston embodied shepherded by Reverend John Roberts for Ms. SEWELL of Alabama. Mr. Speaker, throughout his life that makes America excep- more than half a century. Pastor Roberts, in today, I rise to urge the Senate Republicans to tional. He has shown true leadership in his in- fact, was part of the organizational meeting of consider President Obama’s Supreme Court dustry and community. I extend my deepest the church. Thus, this long standing beacon in nominee. It is disappointing that our demo- sympathies to Mr. Houston’s family and our city has been blessed with a continuity of cratic process is being so unduly hindered by friends. leadership since its beginnings. -

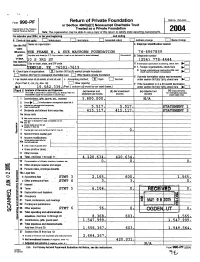

Return of Private Foundation Form 990-PF

Z Foundation OMB No 15450052 Form 990-PF Return of Private or Section 4947(a)(1) Nonexempt Charitable Trust Department of the Treasury Treated as a Private Foundation Internal Revenue Service Note : The organrzafron may be able to use a copy of this return to satisfy state iepoi 2004 For calendar or tax veer baainnina . and ending Use the IRS Name of organization A Employer identification number label. otherwise, HE FRANK W . & SUE MAYBORN FOUNDATION 74-6067859 print Number and street (a P O box number A mad is not delivered to street address) Room/suite g Telephone number 01type. 10 S 3RD ST 254 778-4444 See specific City or town, state, ZIP code C H exemption application is pending, check here , Instructions . and TEMPLE , TX 76501-7619 D 1. Foreign organizations, check here 1[] 2 . Foreign organizations meehng the 85% test H Check type of organization : ~ Section 501(c)(3) exempt private foundation check here and anacn ~o~P~canon . ... ..1D Section 4947(a)(1) nonexempt charitable trust = Other taxable private foundation E If private foundation status was terminated I Fair market value of all assets at end of year J Accounting method: [f] Cash ~ Accrual under section 507(b)(1)(A), check here 10 (from Part 11, coL (c), line 76) D Other (specify) F If the foundation is to a 60-month termination 15 , 58 2 . 33 9 . (E'~ l~ column (d) must be on cash basis.) under section 507(b)( 1 B check here { / Analysis of Revenue and Expenses (e) Revenue and (6) Net investment (c) Adjusted net (d) Disbursements (The total of amounts in columns (b) (c), and (d) may not for charitable purposes necessarily equal me amounts .n column ~~a~.~ expenses per books income income (cash bay only) 1 Contributions, gifts, grants, etc., received , . -

Academic Honors & Awards

AUSTIN COLLEGE 2020 ACADEMIC HONORS & AWARDS Austin College President Steven P. O’Day, J.D. Vice President for Academic Affairs and Dean of the Faculty Dr. Elizabeth Gill Honors Convocation 2020 was not convened due to Remote Learning in effect at Austin College for Spring Term 2020 in response to the coronavirus pandemic. President Steven P. O’Day and Dr. Beth Gill, vice president for Academic Affairs and Dean of the Faculty, join together with the entire Austin College community to celebrate in absentia all the award recipients and honorees included in this program. 2 FACULTY RECOGNITION Installation to Faculty Chairs and Professorships The Donald MacGregor Chair in Natural Science ..........................................................................Dr. Ronald David Baker II The Richardson Chair for the Center for Research, Experience & Transformative Education ........ Dr. Lance Frederick Barton The Ray C. Fish Professorship in Mathematics .......................................................................................... Dr. J’Lee Bumpus The Richardson Chair for the Philosophy, Politics, and Economics Program ..................................... Dr. Mark Ronald Hébert The Richardson Chair for the Professionalism and the Humanities Leadership Program .......... Dr. Jennifer Johnson-Cooper The Henry L. and Laura H. Shoap Professorship of English Literature .................................................. Dr. Gregory S. Kinzer The Richardson Chair for the STEM Teaching and Research Leadership Program ........................ -

Table of Contents

Table of Contents About TPA ............................................................................................................................................... 2 Member Services..................................................................................................................................... 2 Board of Directors.................................................................................................................................... 4 TPA Staff ................................................................................................................................................. 5 Newspapers (sorted by city) .................................................................................................................... 6 Directory Cover Contest Finalists ......................................................................................................... 81 Texas Group Newspapers by Ownership .............................................................................................. 83 Newspapers by County ......................................................................................................................... 85 Map of Texas Counties.......................................................................................................................... 85 Associate Members ............................................................................................................................... 89 Texas Newspaper Foundation Hall of Fame Members ........................................................................ -

Materials from the Johnson Library Pertaining to the Assassination of John F

National Archives and Records Administration http://archives.gov National Archives Catalog https://catalog.archives.gov http://www.lbjlibrary.org MATERIALS FROM THE JOHNSON LIBRARY PERTAINING TO THE ASSASSINATION OF JOHN F. KENNEDY INTRODUCTION This list includes the principal files in the Johnson Library that contain material relating to the assassination of John F. Kennedy. It is not definitive, however, and researchers should consult with the Library's archivists about other potentially useful files. The guide includes those collections which have been opened for research in part or in whole, and those collections which are currently unprocessed or unavailable. WHITE HOUSE CENTRAL FILES (WHCF) This permanent White House office was the main filing unit during the Johnson presidency, though not the primary file for foreign policy documents. Material was filed under 60 major subject headings, several of which are pertinent to the Kennedy assassination. Box # FE 3-1/Kennedy, John F. Federal Government Deaths/Funerals, JFK 3-5 EX FG 1 The President of the United States, 11/22/64-1/10/64 9 FG 2/Kennedy, John F. Former Presidents/Kennedy, John F. 40-41, 43-45 FG 635 Commission to Report on the Assassination of President John F. 376 Kennedy (Warren Commission) JL 3/FG 1 Justice - Legal Matters/Presidential Assassinations 37 JL 3/FG 2/Kennedy, John F. Justice Legal Matters/Former Presidents/ Kennedy, John F. 37 PP 1/FG 2/Kennedy, John F. President, Personal/Former Presidents/ Kennedy, John F. 9-10 02/28/17 1 National Archives and Records Administration http://archives.gov National Archives Catalog https://catalog.archives.gov http://www.lbjlibrary.org (Cross references and letters from the general public regarding the assassination.) PR 4-1 Public Relations - Support after the Death of John F. -

Village Cleanup Slated Sept. 29

Salado Villageillage Voiceoice VOL. XLI, NUMBER 22 VTHURSDAY,SEPTEMBER 13, 2018 254/947-5321 V SALADOviLLAGEVOICE.COM 50¢ BoA agrees to policy for new requests for sewer BY TIM FLEISCHER “Some developments Bryan and College Station. EDitOR-in-CHIEF may need service within six None of those cities “makes months while others may their developers pay up front Aldermen adopted a want the ability to reserve with cash... If we adopt this, policy to guide village ad- capacity for a period of years we’re in trouble.” He added ministrator Don Ferguson to allow for phased develop- that development will only in discussing bringing sewer ment,” Ferguson stated. happen outside the city lim- service to new develop- The policy will require its with this requirement. ments. the developer to build neces- “It’s on us to worry about The policy will require sary infrastructure from the providing capacity,” he said. that sewer service only be proposed development to the Michael Coggin said that provided to properties that Village wastewater system, the impact fee requirement are inside the corporate city or make a payment of the gets “builders to put skin in limits, so adjacent properties pro rata fees for the cost of the game.” would need to voluntarily extending wastewater mains. Frank Coachman said annex into the Village to be The developer will be re- that the impact fee is “$3,750 eligible to tie in to the sewer sponsible for obtaining and per rooftop versus $15,000 line. dedicating rights-of-way or per rooftop to put in a septic The policy comes as the easements for the extensions system,” adding that sewer is Village has been contacted and shall provide payment of also the difference between by two potential single-fam- applicable impact fees. -

NOTICE of WORKSHOP SESSION of the COMMISSIONERS COURT of BELL COUNTY, TEXAS January 9, 2017

NOTICE OF WORKSHOP SESSION OF THE COMMISSIONERS COURT OF BELL COUNTY, TEXAS January 9, 2017 Notice is hereby given that a Workshop Session of the Commissioners Court will be held immediately following the Regular Agenda meeting, or, if there is no Regular Agenda, at 9:30 a.m. in the Commissioners Court Conference Room, County Courthouse, 2nd Floor, Belton, Texas, where the following items will be discussed but no action will be taken. 1. Bell County Construction Status, Maintenance & Equipment Updates a. Buildings & Grounds/Maintenance projects status b. Construction Projects reports c. Contract reports d. Expo Project reports e. Update regarding Temple Annex f. Complaint status on policies/procedures on weapons in buildings/county property 2. Project Management priorities and projects. a. Strategic Capital Improvement Project Plan and Policy and Funding b. Review of Project priorities and current funding status/projections c. Update on consultants on jail staffing/scheduling/wage & hour reviews 3. Juvenile Probation Department a. Personnel b. Building/Roof repairs update 4. Engineering Office and Road & Bridge Department Updates a. Subdivision and Precinct issues (1) Pct 1 (2) Pct 2 (3) Pct 3 (4) Pct 4 b. Model Subdivision Rules/ review of existing Subdivision Regulations c. Abandonment of excess real property process/procedures 5. BellNET meeting review and update a. Amendments to Bylaws and governing documents b. Restructure of organization 6. Technology Services/Communications Center a. Operational Review and systems evaluation b. Update on Indigent Defense projects and Jail Management Project c. Updates on Prosecutor and Courts programs d. Pre-Trial Services process e. New Dawn and New World Projects f. -

Ellie B. Caston, Ph

ABSTRACT Bringing the Mayborn Museum Complex Discovery Boxes into the 21st Century Maria Buonafede Project Chairperson: Ellie B. Caston, Ph. D. Museums have realized the sustaining benefits of school partnerships over the last fifty years and are better meeting the needs of teachers through outreach. This project focuses on one successful outreach program employed at the Mayborn Museum Complex in Waco, TX called Discovery Boxes. Discovery Boxes are thematic kits containing related 3-D objects, media, books and lessons to aid teachers in science and social studies. This project consisted of redesigning elements of selected boxes based on evaluation from area classroom teachers, in order to increase their accessibility and effectiveness. In order to evaluate these boxes, interviews were conducted with six elementary school teachers who had previously used the Discovery Boxes. The feedback provided from these teachers guided the redesigning of the boxes; and the same teachers then used the redesigned boxes in their classrooms. The teachers evaluated the redesigned boxes and made further recommendations. This project also includes a brief literature review of museum-school partnerships and outreach throughout history and the specific development of Discovery Boxes at the Mayborn Museum Complex. The results of the project provide recommendations to staff at the Mayborn Museum Complex for the continuation of redesigning the remaining Discovery Boxes. The process and recommendations can also be used as a model by other museums with similar outreach programs. Bringing the Mayborn Museum Discovery Boxes into the 21st Century by Maria Buonafede, B.A. A Project Approved by the Department of Museum Studies _____________________________________ Kenneth C. -

Peabody College Catalog

Peabody College Catalog Vanderbilt University 2020/2021 Catalog 2020/2021 Containing general Collegeinformation and courses of study for the 2020/2021 session corrected to 1 July 2020 Archived Peabody 1 The university reserves the right, through its established procedures, to modify the requirements for admission and graduation and to change other rules, regulations, and provisions, including those stated in this catalog and other publications, and to refuse admission to any student, or to require the withdrawal of a student if it is determined to be in the interest of the student or the university. All students, full or part-time, who are enrolled in Vanderbilt courses are subject to the same policies. Policies concerning noncurricular matters and concerning withdrawal for medical or emotional reasons can be found in the Student Handbook, which is on the Vanderbilt website at vanderbilt.edu/student_handbook. NONDISCRIMINATION STATEMENT In compliance with federal law, including the provisions of Title VI and Title VII of the Civil Rights Act of 1964, Title IX of the Education Amendment of 1972, Sections 503 and 504 of the Rehabilitation Act of 1973, the Americans with Disabilities Act (ADA) of 1990,the ADA Amendments Act of 2008, Executive Order 11246, the Vietnam Era Veterans Readjustment Assistance Act of 1974 as amended by the Jobs for Veterans Act, and the Uniformed Services Employment and Reemployment Rights Act, as amended, and the Genetic Information Nondiscrimination Act of 2008, Vanderbilt University does not discriminate against individuals on the basis of their race, sex, sexual orientation, gender identity, religion, color, national or ethnicCatalog origin, age, disability, military service, covered veterans status, or genetic information in its administration of educational policies, programs, or activities; admissions policies; scholarship and loan programs; athletic or other university-administered programs; or employment. -

The Rock Rattler Published Monthly by the Ark-La-Tex Gem and Mineral Society Volume: 48 No

THE ROCK RATTLER PUBLISHED MONTHLY BY THE ARK-LA-TEX GEM AND MINERAL SOCIETY VOLUME: 48 NO. 8 Peridot- Birthstone of the month , Presidents Notes - by Del Glasner Hoping our Governor thinks it ok for our Aug 15 & 16 show to go on. We should find out on July 24 ThatIt’s so most hot this clubs time of year that most clubs don’t have field trips and the virus has shutdown rock shows and museums I was thinking of a “Five Minute Stop Field Trip”. Consisting of a car caravan to rock & fossil sites were we can: Pull over to the side of the road, Step out and pick up a rock, Return back to the air-conditioned car, Go the the next spot and so on. This also might be good for those that cannot scamper up a hillside or hike to a site. Let me know what you think. Birthstone for August – Peridot Called “the extreme gem” by the Gemological Institute of America, Peridot is born of fire and brought to light, one of only two gems (Diamond is the other) formed not in the Earth’s crust, but in molten rock of the upper mantle and brought to the surface by the tremendous forces of earthquakes and volcanoes. While these Peridots are born of Earth, other crystals of Peridot have extraterrestrial origins, found in rare pallasite meteorites (only 61 known to date) formed some 4.5 billion years ago, remnants of our solar system’s birth. Peridot in its basic form, Olivine, was also found in comet dust brought back from the Stardust robotic space probe in 2006, has been discovered on the moon, and detected by instrument on Mars by NASA’s Global Surveyor.