Submission to Ofcom's Third Review of Public Service Broadcasting

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

ITV Partners with Viewability Company Meetrics

PRESS RELEASE ITV partners with viewability company Meetrics First measurements across all channels show viewability rates above industry-wide benchmarks ITV, the UK’s biggest commercial broadcaster, announces that it has partnered with Meetrics, a leading European software company for advertising measurement and analytics, to provide enhanced advertising campaign delivery validation for VOD advertising across ITV Hub platforms. As part of the partnership, Meetrics provides video viewability data and reporting for ITV Hub on connected TV platforms and In-App (Android and iOS) as well as desktop and mobile web campaigns. This enriches the reporting capabilities for VOD campaigns run on ITV Hub and demonstrates the high quality of ITV’s ad inventory on metrics that are important to agencies and advertisers. With the partnership, ITV underlines its commitment to very high transparency standards and quality controls for the benefit of its advertising customers. Meetrics is an independent vendor accredited for various services by the Media Rating Council and committed to strict privacy rules in full accordance with GDPR. With Meetrics as a partner ITV is breaking new ground by being the first broadcaster in the world to make use of the IAB Open Measurement SDK, which is considered the most rigorous standard for In-App viewability measurement. To date, average measurement for campaigns running across ITV Hub showed a viewability rate (according to the MRC definition) of 98%, which is far beyond average, compared to industry viewability benchmarks. The new viewability measurement and reporting will give advertisers huge confidence that ITV can deliver standards on human and viewability measures that outperform the VOD market. -

Itv Studios Acquires Swedish Production Company Elk Production

ITV STUDIOS ACQUIRES SWEDISH PRODUCTION COMPANY ELK PRODUCTION 21 June 2017 – ITV Studios has acquired the Swedish production company Elk Production, a subsidiary of Elk Entertainment Group. The production label is known for hit entertainment shows including quiz En Ska Bort (Odd One Out) and award-winning series Wahlgrens and Parneviks. Elk Production currently has 15 shows in production or on air across Sweden’s free to air and pay TV channels including Drömpyramiden (Stacked), Ett jobb för Berg (A Job For Berg) and Superskaparna (Supercrafters). It has also produced local versions of international formats including Ninja Warriors, Superstars and Top Chef: Just Desserts. ITV Studios’ majority stake in Elk Production will see the company combine with ITV Studios’ existing Swedish production business, with the amalgamated companies operating under the brand ITV Studios Sweden. ITV Studios Sweden has produced Come Dine With Me for TV4 since 2008 creating 19 seasons so far. It is also producing This Time Next Year for SVT. Elk Production’s current Managing Director, Anna Rydin, will lead the newly combined ITV Studios Sweden reporting to Mike Beale, Managing Director, Nordics and Global Creative Network, ITV Studios. Elk Formats is not included in the acquisition and remains part of Elk Entertainment. However, ITV Studios will be its exclusive formats partner in the Nordics with the right to produce shows, including Stacked and All Inclusive, through ITV Studios’ production companies in Sweden, Denmark, Finland and Norway. ITV Studios now represents a strong library of formats in the region encompassing ITV Studios, Talpa, Twofour and now Elk 1 Entertainment formats. -

Phil Vischer: Faith Driven Entrepreneur

Phil Vischer: Faith Driven Entrepreneur Luke Bubar, Matthew Thomas, Grayson Boyer, Joseph McCann Phil Vischer: Faith Driven Entrepreneur Introduction Servant Leadership Luke Bubar Matthew Thomas Grayson Boyer Life Before Big Idea Joseph McCann Big Idea Bankruptcy November 10, 2020 Reorganization Present Day Works Cited Works Cited Phil Vischer: Faith Introduction Driven Entrepreneur Luke Bubar, Matthew Thomas, Grayson Boyer, Joseph McCann Introduction Servant Leadership Life Before Big Idea Big Idea Bankruptcy Reorganization 1 Phil Vischer, founder of Big Idea Productions, Inc. Present Day and Jellyfish Labs, and creator of VeggieTales and other Works Cited cartoon series[3]. Works Cited 1Now Big Idea Entertainment, LLC This is quite literally the opposite of the other types of leadership, which is part of what makes it so effective; not being afraid to serve those below lets those below you see that you are humble, honest, and have high moral integrity. Phil Vischer: Faith Servant LeadershipI Driven Entrepreneur Luke Bubar, Matthew Thomas, Grayson Boyer, Servant leadership can be one of the easiest and most Joseph McCann effective management/leadership styles that a person can Introduction use. The main focus for them is to put themselves below Servant Leadership those who they are leading and to allow themselves to Life Before Big become \one with the heard" so that they can better Idea understand situations and create solutions that are Big Idea custom-tailored to those below them. Bankruptcy Reorganization Present Day Works Cited Works -

Scotland's Digital Media Company

Annual Report and Accounts 2010 Annual Report and Accounts Scotland’s digital media company 2010 STV Group plc STV Group plc In producing this report we have chosen production Pacific Quay methods which aim to minimise the impact on our Glasgow G51 1PQ environment. The papers chosen – Revive 50:50 Gloss and Revive 100 Uncoated contain 50% and 100% recycled Tel: 0141 300 3000 fibre respectively and are certified in accordance with the www.stv.tv FSC (Forest stewardship Council). Both the paper mill and printer involved in this production are environmentally Company Registration Number SC203873 accredited with ISO 14001. Directors’ Report Business Review 02 Highlights of 2010 04 Chairman’s Statement 06 A conversation with Rob Woodward by journalist and media commentator Ray Snoddy 09 Chief Executive’s Review – Scotland’s Digital Media Company 10 – Broadcasting 14 – Content 18 – Ventures 22 KPIs 2010-2012 24 Performance Review 27 Principal Risks and Uncertainties 29 Corporate Social Responsibility Corporate Governance 34 Board of Directors 36 Corporate Governance Report 44 Remuneration Committee Report Accounts 56 STV Group plc Consolidated Financial Statements – Independent Auditors’ Report 58 Consolidated Income Statement 58 Consolidated Statement of Comprehensive Income 59 Consolidated Balance Sheet 60 Consolidated Statement of Changes in Equity 61 Consolidated Statement of Cash Flows 62 Notes to the Financial Statements 90 STV Group plc Company Financial Statements – Independent Auditors’ Report 92 Company Balance Sheet 93 Statement -

Case Study ITV

Case Study ITV Case Study ITV “The main benefit of moving to Fujitsu and their VME services is risk mitigation. In moving to Fujitsu from our incumbent provider we get access to a very rare resource base for VME development and support. This provides us with a path enabling us to keep our critical Artist Payments System application running and allows us to keep our options open when VME as a product is end dated in 2020.” Anthony Chin, Head of Technology - Finance Systems, ITV The customer ITV is an integrated producer broadcaster and the largest commercial television network in the UK. It is the home of popular television from the biggest entertainment events, to original drama, major sport, landmark factual series and independent news. It operates a family of channels including ITV, ITVBe, ITV2, ITV3 and ITV4 and CITV, which are broadcast free-to-air, as well as the pay channel ITV Encore. ITV is also focused on delivering its programming across multiple platforms including itv.com, mobile devices, video on demand and third party platforms. ITV Studios is a global production business, creating and selling programmes and formats from offices in the UK, US, Australia, France, Germany, the Nordics and the Netherlands. It is the largest and most successful commercial production company in the UK, the largest independent non-scripted indie in the US and ITV Studios Global Entertainment is a leading international distribution The customer businesses. The challenge Country: United Kingdom ITV receives revenue from advertising, its online, pay and interactive Industry: Broadcasting business as well as from the production and sales of the programmes Founded: 1955 it creates and holds rights to. -

Info Fair Resources

………………………………………………………………………………………………….………………………………………………….………………………………………………….………………………………………………….………………………………………………….………………………………………………….………………………………………………….…………… Info Fair Resources ………………………………………………………………………………………………….………………………………………………….………………………………………………….………………………………………………….………………………………………………….………………………………………………….………………………………………………….…………… SCHOOL OF VISUAL ARTS 209 East 23 Street, New York, NY 10010-3994 212.592.2100 sva.edu Table of Contents Admissions……………...……………………………………………………………………………………… 1 Transfer FAQ…………………………………………………….…………………………………………….. 2 Alumni Affairs and Development………………………….…………………………………………. 4 Notable Alumni………………………….……………………………………………………………………. 7 Career Development………………………….……………………………………………………………. 24 Disability Resources………………………….…………………………………………………………….. 26 Financial Aid…………………………………………………...………………………….…………………… 30 Financial Aid Resources for International Students……………...…………….…………… 32 International Students Office………………………….………………………………………………. 33 Registrar………………………….………………………………………………………………………………. 34 Residence Life………………………….……………………………………………………………………... 37 Student Accounts………………………….…………………………………………………………………. 41 Student Engagement and Leadership………………………….………………………………….. 43 Student Health and Counseling………………………….……………………………………………. 46 SVA Campus Store Coupon……………….……………….…………………………………………….. 48 Undergraduate Admissions 342 East 24th Street, 1st Floor, New York, NY 10010 Tel: 212.592.2100 Email: [email protected] Admissions What We Do SVA Admissions guides prospective students along their path to SVA. Reach out -

ITV Embarks on a Ten-Year Digital Archive Project to Preserve Its Video Content for Future Generations with a Spectra Logic Storage Solution

ITV embarks on a ten-year digital archive project to preserve its video content for future generations with a Spectra Logic storage solution Spectra T950 Spectra Logic has provided us with the tools we need to simply Tape Library and 4U Spectra and affordably archive ITV’s digital content for many years. Through BlackPearl the use of the BlackPearl and Spectra’s T950 tape library, our content is kept safe and secure, yet still easily accessible. Marcel Mester, Senior Project Manager, ITV The Challenge ITV was looking to embark on a new, long-term archive project to preserve the organization’s digital assets for years to come. They anticipated reaching vol- umes of up to 20PB of content over time, with an estimated increase of about 2PB each year, and needed to store it for up to 30 years. Therefore, they ITV is an integrated producer broad- required a solution that was high in capacity and durability, with the ability to caster and the largest commercial scale to accommodate future growth. They also wanted a solution that did not television network in the UK. It is the require expensive proprietary middleware, was open standard, and allowed them the flexibility to work with other ITV departments like sports and news. home of popular television from the biggest entertainment events, to The Solution original drama, major sport, landmark ITV already operated three Spectra tape libraries at other locations throughout the UK. Therefore, they knew that Spectra Logic was a company that could factual series and independent news. It be trusted and that offered high-quality products and support. -

White Rabbit Education 2012

White rabbit education 2012 Published on Nov 21, Check out the website: For the Newsletter: email. Independent education in law, banking, and other interesting stuff. * whiterabbiteducation@ * Facebook Groups "White Rabbit Trust" (For Law and. Si Spaniard from the White Rabbit Education group returns to Lawful Rebellion is here, the Controllers are here, and finally, is here. White Rabbit Workshop. Saturday 28th April 10am – 6pm. The Music Café, 23a New Park Street, LE3 5NH. The truth is we live in a very complicated. have culture too.” The focus of education at the. White Rabbit Gallery has been shaped by the vision of Judith. Neilson, the owner of the White. Rabbit Collection. Posts: Joined: Mon Dec 03, pm White Rabbit Education, also known as ' the Spaniard', has quite a few videos on this site. Posts: Joined: Mon May 14, pm: Location: Sarrrrf London The White rabbit has gone underground for a while to try something important. could be a dedicated website with tailored educational 'program. Click the WhiteRabbit The time has come. To seek that which is just, fair and reasoned. The time is now. Recognise the gift. Dwell not “in” the past and fear not. Collection of Holes in Rules, Eindhoven Classification Model. FOR QUOTATION USE (APA). Tiggelen, K. B. van (). Following the white rabbit: Rule users'. July 9th, by Bernadette. June. This month, my lovely friend Matt Feerick joined me, doing acts of kindness every day whilst on holiday in Toronto. He also. unDisclosed discovery trail Education Kit Card. Jeffrey Smart: Master of White Rabbit – Contemporary Chinese Art Collection Education Resource. -

FTSE Factsheet

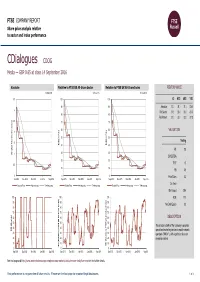

FTSE COMPANY REPORT Share price analysis relative to sector and index performance Data as at: 14 September 2016 CDialogues CDOG Media — GBP 0.65 at close 14 September 2016 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 14-Sep-2016 14-Sep-2016 14-Sep-2016 3.5 100 100 1D WTD MTD YTD 90 90 Absolute 31.3 31.3 31.3 -23.5 3 Rel.Sector 31.5 33.0 33.2 -24.0 80 80 Rel.Market 31.2 33.3 33.2 -27.8 2.5 70 70 60 60 VALUATION 2 (local currency) (local 50 50 Trailing 1.5 Relative Price 40 Relative Price 40 PE 2.8 30 30 Absolute Price Price Absolute 1 EV/EBITDA - 20 20 0.5 PCF 1.0 10 10 PB 0.5 0 0 0 Price/Sales 0.3 Sep-2015 Dec-2015 Mar-2016 Jun-2016 Sep-2016 Sep-2015 Dec-2015 Mar-2016 Jun-2016 Sep-2016 Sep-2015 Dec-2015 Mar-2016 Jun-2016 Sep-2016 Div Yield - Absolute Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Div Payout 29.4 100 100 100 ROE 17.7 90 90 90 Net Debt/Equity 0.0 80 80 80 70 70 70 60 60 60 DESCRIPTION 50 50 50 The principal activity of the Company is provides 40 40 40 RSI (Absolute) RSI specialised marketing services to mobile network 30 30 30 operators ("MNOs" ), with a particular focus on 20 20 20 emerging markets. -

In the United States Bankruptcy Court for the District of Delaware

Case 21-10457-LSS Doc 237 Filed 05/13/21 Page 1 of 2 IN THE UNITED STATES BANKRUPTCY COURT FOR THE DISTRICT OF DELAWARE Chapter 11 In re: Case No. 21-10457 (LSS) MOBITV, INC., et al., Jointly Administered Debtors.1 Related Docket Nos. 73 and 164 NOTICE OF FILING OF SUCCESSFUL BIDDER ASSET PURCHASE AGREEMENT PLEASE TAKE NOTICE that, on April 7, 2021, the United States Bankruptcy Court for the District of Delaware (the “Bankruptcy Court”) entered the Order (A) Approving Bidding Procedures for the Sale of Substantially All Assets of the Debtors; (B) Approving Procedures for the Assumption and Assignment of Executory Contracts and Unexpired Leases; (C) Scheduling the Auction and Sale Hearing; and (D) Granting Related Relief [Docket No. 164] (the “Bidding Procedures Order”).2 PLEASE TAKE FURTHER NOTICE that, pursuant to the Bidding Procedures Order, the Debtors conducted an auction on May 11-12, 2021 for substantially all of the Debtors’ assets (the “Assets”). At the conclusion of the auction, the Debtors, in consultation with their advisors and the Consultation Parties, selected the bid submitted by TiVo Corporation (the “Successful Bidder”) as the Successful Bid. PLEASE TAKE FURTHER NOTICE that, on May 12, 2021, the Debtors filed the Notice of Auction Results [Docket No. 234] with the Bankruptcy Court. PLEASE TAKE FURTHER NOTICE that attached hereto as Exhibit A is the Asset Purchase Agreement dated May 12, 2021 (the “Successful Bidder APA”) between the Debtors and the Successful Bidder. PLEASE TAKE FURTHER NOTICE that a hearing is scheduled for May 21, 2021 at 2:00 p.m. -

Ted Sarandos Chief Content Officer Netflix One of Time Magazine's 100

Ted Sarandos Chief Content Officer Netflix One of Time Magazine's 100 Most influential People of 2013, Ted Sarandos has led content acquisition for Netflix since 2000. With more than 20 years’ experience in the home entertainment business, Ted is recognized as a key innovator in the acquisition and distribution of films and television programs. From its roots as a U.S. DVD subscription rental company, Netflix is now the world’s leading Internet television network with more than 50 million members in nearly 50 countries. With the 2013 releases of "House of Cards," "Hemlock Grove," "Arrested Development," "Orange is the New Black," “Turbo F.A.S.T.,” “Derek,” and “Lilyhammer,” Ted has led the transformation of Netflix into an original content powerhouse that is changing the rules of how serialized television is produced, released and distributed globally. In its first two years of releasing original series, documentary films and comedy specials, Netflix has been recognized by the film and TV industries with 45 Emmy nominations and 10 Emmy wins; an Oscar nomination; 6 Golden Globe nominations and a win; 2 Peabody Awards; 2 AFI Awards and recognition from all of the major guilds. Ted has also been producer or executive producer of several award winning and critically acclaimed documentaries and independent films, including the Emmy nominated "Outrage," and "Tony Bennett: The Music Never Ends." He is a Henry Crown Fellow at the Aspen Institute and serves on the board of Exploring The Arts, a nonprofit focused on arts in schools. He also serves on the Film Advisory Board for Tribeca and Los Angeles Film Festival, is an American Cinematheque board member and is an Executive Committee Member of the Academy of Television Arts & Sciences. -

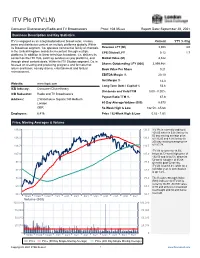

ITV Plc (ITV:LN)

ITV Plc (ITV:LN) Consumer Discretionary/Radio and TV Broadcasters Price: 108.05 GBX Report Date: September 28, 2021 Business Description and Key Statistics ITV is engaged as an integrated producer broadcaster, creates, Current YTY % Chg owns and distributes content on multiple platforms globally. Within its Broadcast segment, Co. operates commercial family of channels Revenue LFY (M) 3,308 3.0 in the United Kingdom and delivers content through multiple EPS Diluted LFY 0.12 1.7 platforms. In addition to linear television broadcast, Co. delivers its content on the ITV Hub, catch up services on pay platforms, and Market Value (M) 4,322 through direct content deals. Within its ITV Studios segment, Co. is focused on creating and producing programs and formats that Shares Outstanding LFY (000) 3,999,984 return and travel, namely drama, entertainment and factual Book Value Per Share 0.21 entertainment. EBITDA Margin % 20.10 Net Margin % 14.3 Website: www.itvplc.com Long-Term Debt / Capital % 53.6 ICB Industry: Consumer Discretionary Dividends and Yield TTM 0.00 - 0.00% ICB Subsector: Radio and TV Broadcasters Payout Ratio TTM % 67.8 Address: 2 Waterhouse Square;140 Holborn London 60-Day Average Volume (000) 8,573 GBR 52-Week High & Low 132.50 - 65.68 Employees: 6,416 Price / 52-Week High & Low 0.82 - 1.65 Price, Moving Averages & Volume 136.0 136.0 ITV Plc is currently trading at 108.05 which is 6.0% below its 50 day moving average price 126.3 126.3 of 115.00 and 8.3% below its 200 day moving average price 116.7 116.7 of 117.78.