View This Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Lender Panel List December 2019

Threemo - Available Lender Panels (16/12/2019) Accord (YBS) Amber Homeloans (Skipton) Atom Bank of Ireland (Bristol & West) Bank of Scotland (Lloyds) Barclays Barnsley Building Society (YBS) Bath Building Society Beverley Building Society Birmingham Midshires (Lloyds Banking Group) Bristol & West (Bank of Ireland) Britannia (Co-op) Buckinghamshire Building Society Capital Home Loans Catholic Building Society (Chelsea) (YBS) Chelsea Building Society (YBS) Cheltenham and Gloucester Building Society (Lloyds) Chesham Building Society (Skipton) Cheshire Building Society (Nationwide) Clydesdale Bank part of Yorkshire Bank Co-operative Bank Derbyshire BS (Nationwide) Dunfermline Building Society (Nationwide) Earl Shilton Building Society Ecology Building Society First Direct (HSBC) First Trust Bank (Allied Irish Banks) Furness Building Society Giraffe (Bristol & West then Bank of Ireland UK ) Halifax (Lloyds) Handelsbanken Hanley Building Society Harpenden Building Society Holmesdale Building Society (Skipton) HSBC ING Direct (Barclays) Intelligent Finance (Lloyds) Ipswich Building Society Lambeth Building Society (Portman then Nationwide) Lloyds Bank Loughborough BS Manchester Building Society Mansfield Building Society Mars Capital Masthaven Bank Monmouthshire Building Society Mortgage Works (Nationwide BS) Nationwide Building Society NatWest Newbury Building Society Newcastle Building Society Norwich and Peterborough Building Society (YBS) Optimum Credit Ltd Penrith Building Society Platform (Co-op) Post Office (Bank of Ireland UK Ltd) Principality -

Low-Impact Living Initiative

building societies what are they? They’re mutual institutions offering savings accounts and mortgages, and occasionally current accounts. This is all they provide. They are simple beasts compared to banks, and their mutual nature means that they are owned by their members, and are not listed on stock exchanges and owned by shareholders. They’re similar to co- operatives, but, from Wikipedia: ‘unlike a true cooperative, members usually do not contribute to the capital of the company by direct investment, but derive their right to profits and votes through The sign on the Penrith Building Society (the their customer relationship.’ smallest in the UK) says it all: ‘Every man his History: the first building society was formed in own landlord’ (well, all apart from the fact that 1775, by Richard Ketley, proprietor of the Golden they left out half the population). Cross pub in Snow Hill, Birmingham. At the time, publicans encouraged meetings of working men in Demutualisation: many building societies were their pubs in order to sell more beer! Lots of ‘demutualised’, starting in the 1980s, after trades unions and friendly societies were formed deregulation allowed mutual societies to become in pubs. This society was quickly followed by banks with shareholders, or to merge with existing others in Birmingham, then Dudley, Rowley Regis banks. Members were offered incentives in the and other places in the Midlands, North and form of cash payments or shares. The first mutual Scotland. Members of early societies like this paid society to be demutualised was Abbey National, money into a pot, and when there was enough, followed by famous names such as Alliance and one member’s name was drawn by lot and the Leicester and Northern Rock. -

Lenders Who Have Signed up to the Agreement

Lenders who have signed up to the agreement A list of the lenders who have committed to the voluntary agreement can be found below. This list includes parent and related brands within each group. It excludes lifetime and pure buy-to-let providers. We expect more lenders to commit over the coming months. 1. Accord Mortgage 43. Newcastle Building Society 2. Aldermore 44. Nottingham Building Society 3. Bank of Ireland UK PLC 45. Norwich & Peterborough BS 4. Bank of Scotland 46. One Savings Bank Plc 5. Barclays UK plc 47. Penrith Building Society 6. Barnsley Building Society 48. Platform 7. Bath BS 49. Principality Building Society 8. Beverley Building Society 50. Progressive Building Society 9. Britannia 51. RBS plc 10. Buckinghamshire BS 52. Saffron Building Society 11. Cambridge Building Society 53. Santander UK Plc 12. Chelsea Building Society 54. Scottish Building Society 13. Chorley Building Society 55. Scottish Widows Bank 14. Clydesdale Bank 56. Skipton Building Society 15. The Co-operative Bank plc 57. Stafford Railway Building Society 16. Coventry Building Society 58. Teachers Building Society 17. Cumberland BS 59. Tesco Bank 18. Danske Bank 60. Tipton & Coseley Building Society 19. Darlington Building Society 61. Trustee Savings Bank 20. Direct Line 62. Ulster Bank 21. Dudley Building Society 63. Vernon Building Society 22. Earl Shilton Building Society 64. Virgin Money Holdings (UK) plc 23. Family Building Society 65. West Bromwich Building Society 24. First Direct 66. Yorkshire Bank 25. Furness Building Society 67. Yorkshire Building Society 26. Halifax 27. Hanley Economic Building Society 28. Hinckley & Rugby Building Society 29. HSBC plc 30. -

Draft-Minutes-17-June-2019-2

Unit 1,Church House, 19-24 Friargate, Penrith, Cumbria, CA11 7XR Tel: 01768 899773 Email: [email protected] Draft Minutes of the meeting of the: FINANCE COMMITTEE Held on Monday 17 June 2019 6.00pm – 8.00pm Board Room, Penrith Town Council Office, Unit 1, Church House, 19-24 Friargate. PRESENT: Cllr. Burgin Cllr. Bowen Cllr. Hawkins Cllr. Jackson Services & Contracts Manager Responsible Finance Officer Finance Committee/ 17 June 2019/ Penrith Town Council / Page 1 PENRITH TOWN COUNCIL MINUTES FINANCE COMMITTEE 17 JUNE 2019 FIN.COM.19/01 Apologies for Absence Apologies for absence were received from Councillor Shepherd and Councillor Kenyon. FIN.COM.19/02 Appointment of Vice Chairman Members considered and voted for the appointment of the Vice Chairman of the Finance Committee. Moved, seconded and RESOLVED THAT: Councillor Bowen be appointed Vice Chairman for the municipal year 2019-20. FIN.COM.19/03 Declaration of Interests and Dispensations Members were asked to disclose their interests in matters to be discussed and to decide requests for dispensations. None recorded. FIN.COM.19/04 Public Participation No members of the public had requested in writing to speak prior to the meeting. FIN.COM.19/05 Public Bodies (Admission to Meetings) Act 1960 Members considered whether any items should be considered without the presence of the press and public, pursuant to the Public Bodies (Admission to Meetings) Act 1960 Section 2. RESOLVED THAT: Items 16,17,18 be considered without the presence of the press and public as all three matters involve the disclosure of exempt information as defined in paragraph 3 of Part 1 to Schedule 12A of the Local Government Act 1972, containing information relating to the financial or business affairs of any particular person. -

Finding the Sweet Spot: How Building Societies Need to Strike a Balance

BUILDING SOCIETIES RESEARCH REPORT FINDING THE SWEET SPOT: HOW BUILDING SOCIETIES NEED TO STRIKE A BALANCE. For professional use only 2 BUILDING SOCIETIES RESEARCH REPORT BUILDING SOCIETIES RESEARCH REPORT 3 EXECUTIVE SUMMARY For building societies, the rise of a week, and 84% use their building society’s website the digital banking environment Building societies remain “Building societies are at the heart at least once a month. heavily dependent on branches changes not just their strategy of their communities, but the way for product purchases. Most rate these services highly, with three quarters but also their fundamental their customers want to interact giving them a score of eight out of ten or more. going forward will change. Whilst nature. How do organisations Half (50%) of customers They’re also going to be increasingly important traditionally rooted in – opened their savings account branches have been at the core of revenue generators. and owned by – their local in branch against only 37% distribution, customers are telling using the building society’s us more and more that they want Insurance, among the most commoditized of financial communities fulfill their vision website. to buy their products and services services products, has long been the bread and butter in a society dominated by the online as well as through the of price comparison sites, for example. Yet at the Internet? 45% bought their mortgage in moment the branch is still the most common sales branch, against 19% online. branches.” channel for holders of life (47%), home (43%), critical Politicians, regulators, product Mark Holweger, Managing Director, illness (38%) and income protection (33%) insurance. -

Rpt MFI-EU Hard Copy Annual Publication

MFI ID NAME ADDRESS POSTAL CITY HEAD OFFICE RES* UNITED KINGDOM Central Banks GB0425 Bank of England Threadneedle Street EC2R 8AH London No Total number of Central Banks : 1 Credit Institutions GB0005 3i Group plc 91 Waterloo Road SE1 8XP London No GB0015 Abbey National plc Abbey National House, 2 Triton NW1 3AN London No Square, Regents Place GB0020 Abbey National Treasury Services plc Abbey National House, 2 Triton NW1 3AN London No Square, Regents Place GB0025 ABC International Bank 1-5 Moorgate EC2R 6AB London No GB0030 ABN Amro Bank NV 10th Floor, 250 Bishopsgate EC2M 4AA London NL ABN AMRO Bank N.V. No GB0032 ABN AMRO Mellon Global Securities Services Princess House, 1 Suffolk Lane EC4R 0AN London No BV GB0035 ABSA Bank Ltd 75 King William Street EC4N 7AB London No GB0040 Adam & Company plc 22 Charlotte Square EH2 4DF Edinburgh No GB2620 Ahli United Bank (UK) Ltd 7 Baker Street W1M 1AB London No GB0050 Airdrie Savings Bank 56 Stirling Street ML6 OAW Airdrie No GB1260 Alliance & Leicester Commercial Bank plc Building One, Narborough LE9 5XX Leicester No GB0060 Alliance and Leicester plc Building One, Floor 2, Carlton Park, LE10 0AL Leicester No Narborough GB0065 Alliance Trust Savings Ltd Meadow House, 64 Reform Street DD1 1TJ Dundee No GB0075 Allied Bank Philippines (UK) plc 114 Rochester Row SW1P 1JQ London No GB0087 Allied Irish Bank (GB) / First Trust Bank - AIB 51 Belmont Road, Uxbridge UB8 1SA Middlesex No Group (UK) plc GB0080 Allied Irish Banks plc 12 Old Jewry EC2R 8DP London IE Allied Irish Banks plc No GB0095 Alpha Bank AE 66 Cannon Street EC4N 6AE London GR Alpha Bank, S.A. -

Mortgage Lenders That Accept Personal Local Authority Searches

FREE PHONE 0800 318611 FAX 01483 221854 Mortgage lenders that accept Personal Local Authority Searches Accord Buy to Let* Leeds Building Society* Accord Mortgages Ltd* Lloyds Bank plc (pre-fixed 20/40)* Adam & Co Lloyds Bank plc (pre-fixed 50/30/77)* Adam & Co International Lloyds TSB Scotland plc* Ahli United Bank (UK) plc **** Magellan Homeloans Aldermore Bank Plc* Manchester Building Society Allied Irish Bank (GB), a trading name of AIB Group (UK) **** Mansfield Building Society Astra Mortgages* Market Harborough Building Society Aviva Equity Release UK Ltd* Marsden Building Society Bank of Cyprus MBS Lending Ltd*** Bank of Ireland (UK) plc* Melton Mowbray Building Society*** Bank of Ireland (as Bank of Ireland Mortgages)* Metro Bank plc* Bank of Scotland (Beginning A)* Monmouthshire Building Society*** Bank of Scotland (Beginning O)* Mortgage Express* Barclays Bank (as Woolwich)* ** National Counties Building Society* Barnsley Building Society (a trading name of Yorkshire Building Society)* National Westminster Bank plc Bath Investment and Building Society** Nationwide Building Society* Beverley Building Society*** New Life Mortgages Ltd* Birmingham Midshires Newbury Building Society* Bradford & Bingley plc* Newcastle Building Society Britannia (a trading name of The Co-operative Bank)* Norwich & Peterborough Building Society* Cambridge Building Society Nottingham Building Society Capital Home Loans* NRAM (Northern Rock Asset Management) plc** Chelsea Building Society (a trading name of Yorkshire Building Society)* Precise Mortgages -

Direction for Modification by Consent of 5.1 to 5.3 and 5.5 of the Capital Buffers Part of the PRA Rulebook

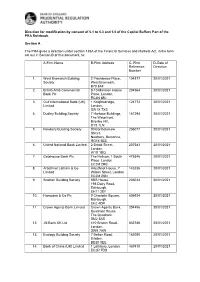

Direction for modification by consent of 5.1 to 5.3 and 5.5 of the Capital Buffers Part of the PRA Rulebook. Section A The PRA gives a direction under section 138A of the Financial Services and Markets Act, in the form set out in Section B of this document, to: A-Firm Name B-Firm Address C- Firm D-Date of Reference Direction Number 1. West Bromwich Building 2 Providence Place, 104877 20/01/2021 Society West Bromwich, B70 8AF 2. British Arab Commercial 8-10 Mansion House 204564 20/01/2021 Bank Plc Place, London, EC4N 8BJ 3. Gulf International Bank (UK) 1 Knightsbridge, 124772 20/01/2021 Limited London, SW1X 7XS 4. Dudley Building Society 7 Harbour Buildings, 161294 20/01/2021 The Waterfront, Brierley Hill, DY5 1LN 5. Newbury Building Society 90 Bartholomew 206077 20/01/2021 Street, Newbury, Berkshire, RG14 5EE 6. United National Bank Limited 2 Brook Street, 207381 20/01/2021 London, W1S 1BQ 7. Gatehouse Bank Plc The Helicon, 1 South 475346 20/01/2021 Place, London EC2M 2RB 8. Arbuthnot Latham & Co Arbuthnot House, 7 143336 20/01/2021 Limited Wilson Street, London EC2M 2SN 9. Scottish Building Society SBS House, 206034 20/01/2021 193 Dalry Road, Edinburgh, EH11 2EF 10. Hampden & Co Plc 9 Charlotte Square, 606934 20/01/2021 Edinburgh, EH2 4DR 11. Crown Agents Bank Limited Crown Agents Bank, 204456 20/01/2021 Quadrant House, The Quadrant, SM2 5AS 12. JN Bank UK Ltd 410 Brixton Road, 832786 20/01/2021 London, SW9 7AW 13. Ecology Building Society 7 Belton Road, 162090 20/01/2021 Silsden, BD20 0EE 14. -

FOI3002 Information Provided

Firm Ref Firm Name 100013 Skipton Financial Services Ltd 100014 Leek United Building Society 100015 Saffron Building Society 100017 SBCA 100129 Allotts 100163 Alexander Ash & Co Ltd 100266 Bevan & Buckland 100556 Oury Clark 100732 Alliotts 100747 Heywood Shepherd 100799 Forrester Boyd 100813 Gibbons 100820 Gilberts 100825 Greaves West & Ayre 100883 Friend-James 101012 Neville A. Joseph 101022 Howard Worth 101092 Javed & Co 101112 Lamont Pridmore 101117 Winningtons 101133 Gross Klein (incorporating Gross Klein Wood and Gross Klein & Partners) 101142 Larking Gowen 101163 Latif & Company 101180 Keymer Haslam & Co 101321 J.H. Greenwood & Company 101330 John Kerr 101494 Lovewell Blake 101501 McCabe Ford Williams 101566 Hamilton Brading 101579 Robinson and Co 101608 Pentins 101609 Peters, Elworthy & Moore 101633 Palmer, Riley & Co 101739 Nicholsons 101840 Price Mann & Co 101886 Leftley, Rowe & Company 102046 Mitchell Charlesworth 102167 Playfoot & Company 102245 Stephenson & Co 102323 Volans, Leach & Schofield 102395 Whitakers 102411 Shelvoke, Pickering, Janney & Co 102529 Trudgeon Halling 102531 Uppal & Warr 102557 Shah Dodhia & Co 102577 Wildin & Co 102581 Gerald Thomas & Co 102677 Arthur E Walker & Co 102722 BSG Valentine 102781 Pierce 102903 Winburn Glass Norfolk 102983 Mark J Rees 103410 Sedley Richard Laurence Voulters 103440 Leonard Gold 103630 Tyas & Company 103677 Daly, Hoggett & Co 103876 Sandison Easson & Co 104021 Sampson West 104101 Geo Little Sebire & Co 104219 M. Emanuel 104354 Potter Baker 104433 Millener Davies 104538 Bird Simpson & Co 104673 Thomson Cooper 104732 Gilmour Hamilton & Co 104752 James S Lessells 104753 Walker, Dunnett & Co 104766 James Hair & Co 104875 Ipswich Building Society 104877 West Bromwich Building Society 104917 Armstrong Watson 104961 Morris Owen 104965 Mercer & Hole 104982 Strover, Leader & Co 105125 Hicks and Company 105181 Malthouse & Company Wealth Management 105402 H.B. -

Mortgage Lenders That Accept Personal Local Authority Searches

FREE PHONE 0800 318611 FAX 01483 221854 Mortgage lenders that accept Personal Local Authority Searches Accord Buy to Let* Leeds Building Society* Accord Mortgages Ltd* Lloyds Bank plc (pre-fixed 20/40)* Adam & Co Lloyds Bank plc (pre-fixed 50/30/77)* Adam & Co International Lloyds TSB Scotland plc* Ahli United Bank (UK) plc **** Magellan Homeloans Aldermore Bank Plc* Manchester Building Society Allied Irish Bank (GB), a trading name of AIB Group (UK) **** Mansfield Building Society Astra Mortgages* Market Harborough Building Society Aviva Equity Release UK Ltd* Marsden Building Society Bank of Cyprus MBS Lending Ltd*** Bank of Ireland (UK) plc* Melton Mowbray Building Society*** Bank of Ireland (as Bank of Ireland Mortgages)* Metro Bank plc* Bank of Scotland (Beginning A)* Monmouthshire Building Society*** Bank of Scotland (Beginning O)* Mortgage Express* Barclays Bank (as Woolwich)* ** National Counties Building Society* Barnsley Building Society (a trading name of Yorkshire Building Society)* National Westminster Bank plc Bath Investment and Building Society** Nationwide Building Society* Beverley Building Society*** New Life Mortgages Ltd* Birmingham Midshires Newbury Building Society* Bradford & Bingley plc* Newcastle Building Society Britannia (a trading name of The Co-operative Bank)* Norwich & Peterborough Building Society* Cambridge Building Society Nottingham Building Society Capital Home Loans* NRAM (Northern Rock Asset Management) plc** Chelsea Building Society (a trading name of Yorkshire Building Society)* Precise Mortgages -

Finance-Committee-Agenda-28-June-2021

Unit 1, Church House, 19-24 Friargate, Penrith, Cumbria, CA11 7XR Tel: 01768 899 773 Email: [email protected] DATE: 21 June 2021 NOTICE IS HEREBY GIVEN that an ORDINARY MEETING of THE FINANCE COMMITTEE will be held on 28 June 2021, at 6.00pm and you are hereby SUMMONED to attend to transact the business as specified in the agenda and reports hereunder. The Meeting will be held at Penrith Parish Centre, St Andrews To assist in the speedy and efficient dispatch of business’, Members should read the agenda and reports in advance of the meeting. Members wishing to obtain factual information on items included on the Agenda are asked to enquire of the relevant officer PRIOR to 9.00am on the day of the meeting. Members are asked to indicate if they wish to speak on an item PRIOR to the meeting (by 1.00pm on the day of the meeting at the latest) by emailing [email protected] COMMITTEE MEMBERSHIP Cllr. Burgin South Ward Cllr. Jackson North Ward Cllr. Davies West Ward Cllr. Kenyon North Ward Cllr. Hawkins North Ward Cllr. Shepherd East Ward Mr I Parker, Acting Town Clerk Members of the public are welcome to attend. Due to Covid Guidelines, details about how to attend the meeting and how to comment on an agenda item are available on the appropriate committee page on the Town Council Website. 1 The Town Council resolved from 20 May 2019, until the next relevant Annual Meeting of the Council, that having met the conditions of eligibility as defined in the Localism Act 2011 and SI 965 The Parish Councils (General Power of Competence)(Prescribed Conditions) Order 2012, to adopt the General Power of Competence. -

Mortgages | Procuration Fees

Mortgages | Procuration Fees See below a list of procuration fees for our lenders and master brokers. Updated 07/08/18 Gross Fee Net Fee Lender / Product Fee Min Max Fee Min Max 3mc www.3-mc.com | 0161 962 7800 Dependent on lender and product. Call 3mc directly. Accord Mortgages www.accordmortgages.com | Lends in England, Scotland, Wales and Northern Ireland | Procuration fee paid by PMS Standard / Offset 0.45% £200* 0.425% £200* BTL (England and Wales only) 0.50% £250* 0.45% £250* Ported Products (paid on ‘Top Up’ only) 0.30% 0.30% Further Advance (min loan £5,000) 0.30% £50 0.30% £50 Product Transfer - Residential Only 0.30% 0.28% Affirmative www.affirmativefinance.co.uk | Lends in England, Scotland and Wales | Procuration fee paid directly by the lender Constructive Lending / Self Build / Bridging 1.50% 1.45% Aldermore Mortgages www.aldermore.co.uk | Lends in England, Scotland and Wales | Procuration fee paid directly by the lender Residential / BTL 0.45% 0.40% Product Transfers 0.35% 0.30% Al Rayan Bank www.alrayanbank.com | Lends in England, Scotland and Wales | Procuration fee paid directly by the lender Residential 0.35% 0.33% BTL 0.50% 0.45% AToM www.atomltd.co.uk | 01403 272 625 Dependent on lender and product. Call AToM directly. Aviva Equity Release www.aviva-for-advisers.co.uk | Lends in England, Scotland, Wales and Northern Ireland | Procuration fee paid directly by the lender 2.25% + Lifetime Lump Sum Max 2.25% £60 2.25% (of initial loan) 2.25% + Lifestyle Flexible Option £500 £500 + 0.70%1 0.70% + £60 Bank of Ireland www.bankofireland4intermediaries.co.uk | Lends in England, Wales, Scotland and Northern Ireland | Procuration fee paid by PMS *Only available to a selected distribution, please check with lender.