AUTOMOBILE SECTOR August, 2020 2

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Module 1 Kia Body Repair Manuals General Information

be returned to pre-impact dimensions prior to Module 1 beginning the sectioning repair procedures. Kia Body Repair Manuals The extent of damage that must be repaired All Kia “Body Repair Manuals” (BRM) include a should then be evaluated to determine the good overview of the vehicle body structure appropriate repair procedures. This manual along with generic general information and provides locations and procedures where cautions for repairing Kia vehicles. Much of the structural sectioning may be employed. It is same information is included in all manuals the responsibility of the repair technician, and applies to all current models in the Kia based upon the extent of damage, to fleet. determine which location and procedure is suitable for the particular damaged vehicle. Modules 1 of this manual will cover the Kia During the repair of a collision damaged generic body repair information covering all automobile, it is impossible to fully duplicate models included in those course. Module 2 will the methods used in the factory during the look at model specific information for each of vehicle manufacture. Therefore, auto body the following vehicles:- repair techniques have been developed to . Picanto (TA) provide a repair that has strength properties equivalent to those of the original design and . Rio (UB) manufacture. Soul l (PS) 2015 . Cerato (YD) 2,4 & 5 door 2014 . Pro-Ceed (JD) 2013 Safety Factors . Optima (TF) 2014 When repairing Kia vehicles it is important to . Carens (RP) 2014 follow the following recommendations. Sportage (SL) 1. Disconnect the negative (-) battery cable . Sorento (UM12) before performing any work on the . -

(Page 1 of 2) Volume Auto Brands Outperform Tech-Heavy Premium Brands in Overall Dependability Among UK Buyers, J.D. Power Stud

Volume Auto Brands Outperform Tech-Heavy Premium Brands In Overall Dependability Among UK Buyers, J.D. Power Study Finds Škoda Ranks Highest in Vehicle Dependability in the UK for a Second Consecutive Year LONDON: 13 July 2016 — Volume automotive brands in the United Kingdom collectively have fewer problems than premium brands, according to the J.D. Power 2016 UK Vehicle Dependability StudySM (VDS), released today. The study, now in its second year, measures problems experienced during the past 12 months by original owners of vehicles in the UK after 12-36 months of ownership. J.D. Power examined 177 problem symptoms across eight categories: engine and transmission; vehicle exterior; driving experience; features/controls/displays (FCD); audio/communication/entertainment/navigation (ACEN); seats; heating, ventilation and cooling (HVAC); and vehicle interior. Overall dependability is determined by the number of problems experienced per 100 vehicles (PP100), with a lower score reflecting higher quality. Volume brands average 99 PP100, compared with the premium brand average of 161 PP100—a difference of 62 PP100. Volume brands also outpaced premiums in 2015, but by a smaller margin (52 PP100). However, premium brands also have more tech features—one of the largest sources of quality issues. Five of the top 10 problems in the industry are related to technology in the ACEN category. The most often reported ACEN problem is built-in Bluetooth mobile phone/device frequent pairing/connectivity issues. Premium brands have a huge opportunity to improve the ownership experience by providing needed customer support and training for technology features like ACEN. Commenting on the survey, Dr. -

History of Pakistan's Automobile Industry

History of Pakistan’s Automobile Industry Following international trends, the automobile industry in Pakistan showed substantial growth in the years under review. The growth was aided by favorable government policies during this period and levy of lower import duties on raw material inputs and on intermediate products. A significant rise in demand for automobiles, propelled at least partly by easy availability of auto leases and loans from banks and leasing companies at low financial cost, was instrumental in the fast growth of the sector. The expansion in the sector, besides boosting the country‟s industrial output, also provided significant direct and indirect employment opportunities. In the past years, there has been a high growth of more than 40 percent per year in the automobile market. The growth declined somewhat in 2008 and 2009 due mainly to a dip in demand because of rising prices and lease financing becoming expensive for the consumers. Pakistan Car Industry The first automobile plant was set up in May 1949 by General Motor & Sales Co. It was set up on an experimental basis, however grew into an assembly plant. Seeing such progress, three major auto manufacturers from the US collaborated with Pakistani business men to set up; Ali Automobiles to manufacture Ford Products in 1955, Haroon Industries to assemble Chrysler Dodge cars in 1956, Khandawalla Industries to assemble American Motor Products in 1962, and Mack Trucks Plant in 1963. However towards the end of the seventies all automobile assembly in Pakistan stopped, until 1983 when Pak Suzuki started manufacturing their vehicles in Pakistan. Further Toyota Indus Motors was set up in 1990, followed by Honda. -

Topline Market Review P

Pakistan Weekly January 12, 2018 REP‐057 Topline Market Review Gains erode as profit taking ensues KSE‐100 Index +1.0 % WoW; Weekly net FIPI US$26mn Topline Research Best Local Brokerage House [email protected] Brokers Poll 2011-14, 2016-17 Tel: +9221‐35303330, Ext: 133 Topline Securities, Pakistan www.jamapunji.pk Best Local Brokerage House 2015-16 Index gains 1% in outgoing week as profit taking ensues Market Weekly Data KSE Volume & Value KSE‐100 Index 42,933.72 (Shares mn) Volume Value (US$mn) 330 150 1‐Week Change (%) 1.0% 260 Market Cap (Rs tn) 8.9 106 190 1‐Week Change (%) 0.2% 63 Market Cap (US$ bn) 80.6 120 1‐Week Change (%) 0.2% 50 20 18 18 18 18 18 ‐ ‐ 1‐Week Avg. Daily Vol (shares mn) 276.4 ‐ ‐ ‐ n n n n n aa aa aa aa aa J J J J J ‐ ‐ 1‐Week Avg. Daily Value (Rs bn) 12.2 ‐ ‐ ‐ 9 8 1‐Week Avg. Daily Value (US$ mn) 110.2 10 11 12 Source: PSX Source: PSX Outgoing week saw the culmination of the Santa Clause rally which commenced on December 20, 2017 and peaked on Jan 10, 2018 with a net gain of 14%. Since then index has had red two sessions correcting 2%/697pts, which has trimmed weekly gains to 1%/410pts with the index closing the week at 42,934pts level. Going forward, equities maybe further pressured as agitation movement by opposition parties begin on Jan 17 to protest against the Model Town. PtiitiParticipation idimproved siifitlignificantlyasprofitswerebkdbooked, average volumes idincreased 30% WWWoW whilevalue rose 44%. -

Board of Directors

8 Board of Directors Mr. Yusuf H. Shirazi Chairman Mr. Shirazi is a Law graduate (LLB) with BA (Hons) and JD (Diploma in Journalism) from Punjab University and AMP Harvard. He served in the financial services of the Central Superior Services of Pakistan for eight years. He is the author of five books including ‘Aid or Trade’ adjudged by the Writers Guild as the best book of the year and continues to be a columnist, particularly on economy. Mr. Shirazi is the Chairman of Atlas Group, which among others, has joint ventures with Honda, GS Yuasa, MAN and Total. He has been the President Karachi Chamber of Commerce and Industries for two terms. He has been the founder member of Karachi Stock Exchange, Lahore Stock Exchange and International Chamber of Commerce and Industry. He has been on the Board of Harvard Business School Alumni Association and is the Founder President of Harvard Club of Pakistan and Harvard Business School Club of Pakistan. He has been a visiting Faculty Member at National Defense College, Navy War College and Pakistan Administrative Staff College. He has been on the Board of Governors of LUMS, GIK and FC College. Previously he also served, among others on the Board of Fauji Foundation Institute of Management and Computer Sciences (FFIMCS) and Institute of Space Technology - Space & Upper Atmosphere Research Commission (SUPARCO). Mr.Takeharu Aoki President & CEO Mr. Aoki is President & Chief Executive Officer (CEO) of Honda Atlas Cars (Pakistan) Ltd. He has been associated with Honda Motor Company Limited, Japan for last 22 years and has rich experience of Sales & Marketing. -

1 (31St Session) NATIONAL ASSEMBLY SECRETARIAT

1 (31st Session) NATIONAL ASSEMBLY SECRETARIAT ———— “QUESTIONS FOR ORAL ANSWERS AND THEIR REPLIES” to be asked at a sitting of the National Assembly to be held on Thursday, the 1st April, 2021 33. *Mr. Muhammad Afzal Khokhar: (Deferred during 28th Session) Will the Minister for National Health Services, Regulations and Coordination be pleased to state: (a) whether Government has taken notice that buying power of public at large of medicines is significantly decreased since the inception of the incumbent Government; if so, the details thereof; (b) what steps are being taken by the Government to decrease the prices of medicines forthwith; and (c) average prices of essential / life saving medicines as on May, 2018 and detail of prices at present? Minister for National Health Services, Regulations and Coordination: (a) Federal Government and Drug Regulatory Authority of Pakistan are cognizant of the impact of increase in prices of drugs and it has been tried at best to allow increase at minimum level as compared to increase in manufacturing/import cost of drugs. Its impact is much lesser than non availability of drugs. Prices of drugs are mostly lower in Pakistan as compared to average prices in the region i.e. Bangladesh, Srilanka and India. (b) Following steps have been taken to reduce prices of medicines:— 2 (i) Regulation imposed: Drug Regulatory Authority of Pakistan, with the approval of Federal Cabinet notified a Drug Pricing Policy2018 which provides a transparent mechanism for fixation, decrease & increase in MRPs of drugs. (ii) Reduction in MRPs of drugs: Maximum Retail Prices (MRPs) of 562 drugs have been reduced and notified after approval by the Federal Government. -

Exd Company Profile

Company Profile AGENDA 01Su ExD - At a Glance 02Su SAP 03Su Oracle 04Su Digital 05Su Outsourcing 06Su Optimisation 07Su Core Values At a Glance Technology Services Outsourcing Services Optimization Services ■ ERP ■ IT Outsourcing ■ Technology Selection • SAP S/4HANA • IT/HR/Finance Organization ■ Business Process Reengineering • SAP Business One • IT Support Helpdesk ■ Change Management • SAP Business By Design • Software Development ■ System Audit & Review • SAP C/4HANA • Infrastructure Management ■ IT Organization Design • SAP Ariba • E-commerce ■ Development of IT Strategy • SAP SuccessFactors • Digital Media Marketing ■ IT Procurement Services • SAP Fiori • SAP Analytics ■ Accounting ■ IT Contract Negotiation • Oracle EBS • Back office services ■ TCO Reduction • Oracle Cloud ■ Training ■ Offsite Support • IFS • Help Desk (http://support.exdnow.com/) ■ Digital ■ Onsite Support • Secondary Sales Solution • Dedicated Resources • Big Data Analytics • E-commerce (Shopify/Magento) • On call basis • AI Chatbot Office Locations Office Locations Offices Opening Soon Karachi Lahore Toronto Islamabad Melbourne Denver Kuala Lumpur Dubai Riyadh Doha Awards FASTEST GROWING PARTNER 2011 Awards Recognitions INFORMATION ECONOMY REPORT The Software Industry & 2012 Developing Countries ExD was highlighted in the UNCTAD Information Economy Report 2012 from United Nations. Partners Our Customers Nishat Chunian Group Wateen Telecom Our Customers – List ▪ WASCO, Saudi Arabia ▪ Ghani group ▪ Saudi Electric Services Polytechnic, Dammam, Saudi Arabia ▪ Pepsico -

Authorized Sales, Service & Spare Parts (3S) Dealers

16 Authorized Sales, Service & Spare Parts (3S) Dealers KARACHI LAHORE FAISALABAD Honda Shahrah-e-Faisal Honda City Sales Honda Faisalabad 13-Banglore Town, 75 B, Block L, Gulberg III, East Canal Road. Main Shahrah-e-Faisal Ferozepur Road. Tel: (041) 8731741-4 Tel: (021) 34527070, 34527373, Tel: (042) 35841100-06 Fax: (041) 8524029 34547113-6 Fax: (042) 35841107 Fax: (021) 34526758 Honda Chenab Honda Fort 123 JB Raja Wala Green View Colony. Honda Defence 32 Queens Road. Tel: (041) 2603449, 2603549 67/1, Korangi Road Near HINO Circle. Tel: (042) 36314162-3 5500897, 5508297 Tel: (021) 35805291-4 36309062-3, 36313925 Fax: (041) 2603349 Fax: (021) 35805294 Fax: (042) 36361076 PESHAWAR Honda Site Honda Point Honda North C 1, Main Manghopir Road, SITE. Main Defence Road. Main University Road. Tel: (021) 32577411-2, 32564926 Tel: (042) 35700994-5 Tel: (091) 5854901, 5700807, 5700808 32570301, 32569381 Fax: (042) 35700993 Fax: (091) 5854753 Fax: (021) 32577412, 32565056 Honda Canal Bank MIRPUR A.K. Honda South 13-B,Block-K, Johar Town, 1 B/1, Sec. 23, Korangi Industrial Area. Shoukat Khanaum Bypass. Honda Empire Tel: (021) 35050251-4 Tel: (042) 35300822-33, 7029360-61 Mian Muhammad Road, Fax: (021) 35064599 Fax: (042) 35300841 Quaid-e-Azam Chowk. Tel: (058274) 51501,1032701 Honda Drive In MULTAN Fax: (058274) 51500-3 118 C, Rashid Minhas Road. Honda Breeze Tel: (021) 34992832-7, 34992824 GUJRANWALA 63 Abdali Road. Fax: (021) 34992825 Tel: (061) 4588871-3 Honda Gujranwala 4548881, 4542862 G.T. Road. Honda Quaideen Fax: (061) 4588874 Tel: (055) 3893481-3 233-A-2, PECHS. -

153(4) (Order to Grant / Refuse Reduced Rate of Withholding on Supplies / Services / Contracts) (For Parties Addition)

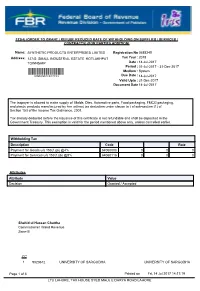

153(4) (ORDER TO GRANT / REFUSE REDUCED RATE OF WITHHOLDING ON SUPPLIES / SERVICES / CONTRACTS) (FOR PARTIES ADDITION) Name: SYNTHETIC PRODUCTS ENTERPRISES LIMITED Registration No 0688349 Address: 127-S SMALL INDUSTRIAL ESTATE KOTLAKHPAT Tax Year : 2018 TOWNSHIP Date : 14-Jul-2017 Period : 01-Jul-2017 - 31-Dec-2017 Medium : System Due Date : 14-Jul-2017 Valid Upto : 31-Dec-2017 Document Date 14-Jul-2017 The taxpayer is allowed to make supply of Molds, Dies, Automotive parts, Food packaging, FMCG packaging, and plastic products manufactured by him without tax deduction under clause (a ) of sub-section (1) of Section 153 of the Income Tax Ordinance, 2001. Tax already deducted before the issuance of this certificate is not refundable and shall be deposited in the Government Treasury. This exemption is valid for the period mentioned above only, unless cancelled earlier. Withholding Tax Description Code Rate Payment for Goods u/s 153(1)(a) @4% 64060008 0 0 0 Payment for Services u/s 153(1)(b) @8% 64060116 0 0 0 Attributes Attribute Value Decision Granted / Accepted Shahid ul Hassan Chattha Commissioner Inland Revenue Zone-III CC 1 9020612 UNIVERSITY OF SARGODHA UNIVERSITY OF SARGODHA Page 1 of 6 Printed on Fri, 14 Jul 2017 14:17:19 LTU LAHORE, TAX HOUSE SYED MAUJ E DARYA ROAD LAHORE 153(4) (ORDER TO GRANT / REFUSE REDUCED RATE OF WITHHOLDING ON SUPPLIES / SERVICES / CONTRACTS) (FOR PARTIES ADDITION) Name: SYNTHETIC PRODUCTS ENTERPRISES LIMITED Registration No 0688349 Address: 127-S SMALL INDUSTRIAL ESTATE KOTLAKHPAT Tax Year : 2018 TOWNSHIP -

Project Report Customer Satisfaction on Honda City

Project Report CUSTOMER SATISFACTION ON PREMIUM SEGMENT CARS WITH SPECIAL REFERENCE TO HONDA CITY 1 Acknowledgement A Good start leads to a Fine end. The ideal way to begin documenting this project work would be to extend my earnest gratitude to everyone who has encouraged, motivated and guided me to make a fine effort for successful completion of this project. I am very thankful to Siddhanta Mangal Kashyap, Head Marketing, Cogtest Service Pvt. Ltd for guiding me throughout the project. My sincere gratitude to the IMT- Gurgaon team for extending their co-operation for successful completion of my project. A final word of thanks goes to my friends and colleagues and everyone else who made this project possible. Your contributions have been most appreciated 2 PROJECT SUBMITTED IN PARTIAL FULFILLMENT FOR THE AWARD OF PGDM in MARKETING Declaration I hereby declare that this project report titled “Customer Satisfaction with Special reference to Premium segment car Honda City” submitted by me to Institute of Management Technology Ghaziabad is a bonafide work undertaken by me and it is not submitted to any other University or Institute for the Award of any degree diploma/certificate or published any time before. (Signature) 3 Index CHAPTER 1 Page no INTRODUCTION - 5 OBJECTIVES OF STUDY - 7 SCOPE AND LIMITATION OF STUDY - 9 RESEARCH METHODOLOGY - 11 CAR STATISTICS IN INDIA - 18 COMPANY PROFILE - 23 COMPETITORS PROFILE - 37 CHAPTER 2 FINDING AND ANALYSIS - 46 CONCLUSION - 59 FINDINGS & SUGGESTION - 61 BIBLIOGRAPHY - 62 4 Introduction The automobile industry today is the most lucrative industry. Due to the increase in disposable income in both rural and urban sector and easy finance being provided by all the financial institutions, the passenger car sales have increased. -

1-Honda Civic Diesel Variant 2019

Top Upcoming Cars In Pakistan 2019 Price, Release Date: We are going through the 20 Upcoming Cars In Pakistan 2019 which will include their Price, Release Date and Pictures Of Course. Recently, it's detected that Pakistan has revised its auto- policy, that has attracted the attention of a number of the well-known automotive brands within the automobile world. several automobile companies have already confirmed that they're about to invest in Pakistan automobile industry in 2019, whereas a number of the automotive brands are within the queue to process all the legal formalities to launch their top of the line vehicles within the native market of Pakistan. Here are 20+ upcoming cars in Pakistan 2019 that may inspire the customers of Pakistan to shop for it right once their official unharness within the Pakistan industry. Following Are the List of Upcoming Cars In Pakistan 2019: 1. Honda Civic Diesel Variant 2019 2. Faw R7 SUV 3. Toyota Yaris Hybrid 2019 4. Toyota Vios 2019 5. Renault Duster 2019 6. Kia Sportage 2019 7. Kia Picanto 2019 8. Kia Carnival 2019 9. Kia Rio 2019 10. Hyundai Elantra 2019 11. Hyundai Santro 2019 12. Hyundai Tucson Crossover 2019 13. Hyundai Verna 2019 14. Hyundai Creta Crossover 2019 15. Toyota Fortuner Diesel Variant 2019 16. Honda Civic 1.5 Turbo 2019 17. DFSK Van Pasajeros 2019 18. DFSK KO5 2019 19. Road Prince DFSK Loadhopper 2019 20. Volkswagen T6 2019 1-HONDA CIVIC DIESEL VARIANT 2019: After the good success of Honda Civic gasoline variants within the Pakistani industry. Honda is going to launch its Honda Civic in a very diesel variant, which is able to even be the first diesel automobile introduced by Honda in Pakistan. -

Companies Listed On

Companies Listed on KSE SYMBOL COMPANY AABS AL-Abbas Sugur AACIL Al-Abbas CementXR AASM AL-Abid Silk AASML Al-Asif Sugar AATM Ali Asghar ABL Allied Bank Limited ABLTFC Allied Bank (TFC) ABOT Abbott (Lab) ABSON Abson Ind. ACBL Askari Bank ACBL-MAR ACBL-MAR ACCM Accord Tex. ACPL Attock Cement ADAMS Adam SugarXD ADMM Artistic Denim ADOS Ados Pakistan ADPP Adil Polyprop. ADTM Adil Text. AGIC Ask.Gen.Insurance AGIL Agriautos Ind. AGTL AL-Ghazi AHL Arif Habib Limited AHSL Arif Habib Sec. AHSM Ahmed Spining AHTM Ahmed Hassan AIBL Asset Inv.Bank AICL Adamjee Ins. AJTM Al-Jadeed Tex AKDCL AKD Capital Ltd AKDITF AKD Index AKGL AL-Khair Gadoon ALFT Alif Tex. ALICO American Life ALNRS AL-Noor SugerXD ALQT AL-Qadir Tex ALTN Altern Energy ALWIN Allwin Engin. AMAT Amazai Tex. AMFL Amin Fabrics AMMF AL-Meezan Mutual AMSL AL-Mal Sec. AMZV AMZ Ventures ANL Azgard Nine ANLCPS Azg Con.P.8.95 Perc.XD ANLNCPS AzgN.ConP.8.95 Perc.XD ANLPS Azgard (Pref)XD ANLTFC Azgard Nine(TFC) ANNT Annoor Tex. ANSS Ansari Sugar APL Attock Petroleum APOT Apollo Tex. APXM Apex Fabrics AQTM Al-Qaim Tex. ARM Allied Rental Mod. ARPAK Arpak Int. ARUJ Aruj Garments ASFL Asian Stocks ASHT Ashfaq Textile ASIC Asia Ins. ASKL Askari Leasing ASML Amin Sp. ASMLRAL Amin Sp.(RAL) ASTM Asim Textile ATBA Atlas Battery ATBL Atlas Bank Ltd. ATFF Atlas Fund of Funds ATIL Atlas Insurance ATLH Atlas Honda ATRL Attock Refinery AUBC Automotive Battery AWAT Awan Textile AWTX Allawasaya AYTM Ayesha Textile AYZT Ayaz Textile AZAMT Azam Tex AZLM AL-Zamin Mod.