India Light Vehicle Sales Update

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

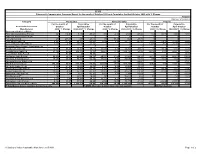

Details of Vehicle Dealers

DETAILS OF VEHICLE DEALERS (BOTH SELF AND NON-SELF) AS ON 17.09.2020 BASED ON VAHAN DATABASE S NO RTO Code Dealer Name Address Maker Self/Non-self Vehicle Class 1 1 RANA MOTORS P.LTD NA DL-110054 MARUTI SUZUKI INDIA LTD Self Motor Car 2 1 M/S PAHWA AUTOSALES PVT LTD 26/24,26/25 SHAKTI NAGAR DL-110007 HYUNDAI MOTOR INDIA LTD Non-self Motor Car 3 1 BALAJI AUTO 31, SHAHZAD BAGH INDL AREA DELHI DL-110035 NA Non-self M-Cycle/Scooter 1275-1276 BARA BAZAR KASMERE GATE DELHI DL- 4 1 CARLTON MOTORS PVT LTD NA Non-self M-Cycle/Scooter 110006 5 1 RANA MOTORS NA DL-110054 MARUTI SUZUKI INDIA LTD Self Motor Car 6 2 Apra Auto India Pvt Ltd NA New Delhi DL- MARUTI SUZUKI INDIA LTD Self Motor Car 7 2 COMPETENT AUTOMOBILES CO. LTD. COMPETENT HOUSE, F-14, CP NEW DELHI DL-110001 NA Self Motor Car RIGH ROAD HONDA,40- 42 JANPATH, NEW DELHI DL- 8 2 BAS ENGINEER PVT. LIMITED HONDA CARS INDIA LTD Non-self Motor Car 110001 CAPITAL POINT, BABA KHARAT SINGH MARG, 9 2 ZENICA CARS INDIA PVT. LIMITED AUDI AG Non-self Motor Car CONNAUGHT PLACE DL-110001 HOTEL SAMRAT, LGF, KAUTILYA MARG, CHANAKYA 10 2 EXCLUSIVE MOTORS PVT. LIMITED BENTLEY MOTORS LIMITED Non-self Motor Car PURI DL-110001 HOTEL SAMRAT, LGF, KAUTILYA MARG CHANAKYA 11 2 EXCLUSIVE MOTORS PVT. LTD NA Non-self Motor Car PURI DL-110001 12 2 SILVER ARROW 50-B,CHANAKAYA PURI DL-110001 NA Non-self Motor Car 13 2 COMPETENT AUTOMOBILES CO. -

Segment/Subsegment Manufacturer 2020 % Change

SIAM Category & Company wise Summary Report for the month of October 2020 and Cumulative for April-October 2020 with % Change Report II (Number of Vehicles) Category Production Domestic Sales Exports For the month of Cumulative For the month of Cumulative For the month of Cumulative Segment/Subsegment October April-October October April-October October April-October Manufacturer 2020 % Change 2020-2021 % Change 2020 % Change 2020-2021 % Change 2020 % Change 2020-2021 % Change Passenger Vehicles (PVs)* FCA India Automobiles Pvt Ltd 961 116.93 5,182 -34.23 832 -2.58 2,593 -53.22 164 60.78 3,086 57.13 Fiat India Automobiles Pvt Ltd 0 - 0 - 0 - 0 - 0 - 0 - Force Motors Ltd 276 249.37 659 -24.43 330 69.23 668 -25.70 0 - 0 - Ford India Private Ltd 8,951 -37.54 49,301 -58.53 7,084 0.95 24,727 -41.93 1,837 -74.38 27,926 -64.66 General Motors India Pvt Ltd 5,639 -8.80 22,036 -52.26 0 - 0 - 5,075 -8.53 21,705 -52.45 Hindustan Motor Finance Corporation Ltd 0 - 0 - 0 - 0 - 0 - 0 - Honda Cars India Ltd 10,272 88.44 36,305 -45.22 10,836 8.25 35,700 -49.63 84 -85.34 1,118 -62.60 Hyundai Motor India Ltd 65,700 26.83 250,750 -38.13 56,605 13.19 219,130 -25.58 12,230 -10.07 44,271 -62.13 Isuzu Motors India Pvt Ltd 11 -92.09 44 -94.99 0 - 0 - 0 - 22 -66.67 Kia Motors India Pvt Ltd 22,936 68.13 86,504 164.74 20,621 61.25 67,588 154.31 4,213 127.73 20,819 796.98 Mahindra & Mahindra Ltd 19,203 20.62 70,928 -42.60 18,621 0.96 70,096 -42.78 796 -32.08 3,472 -58.92 Mahindra Electric Mobility Ltd 0 - 5 - 1 -93.75 1 -95.24 0 - 16 -77.14 Maruti Suzuki India Ltd -

Consolidated Approved Company List

Consolidated approved company list CONSOLIDATED APPROVED COMPANY LIST CONSOLIDATED APPROVED COMPANY NORMS STATE INSTITUTE ACTION UNIQUE COMPANY LIST CATEGORY ID CODE 3M INDIA LIMITED ELITE E00001 ABB INDIA LIMITED ELITE E00519 ACCENTURE SOLUTIONS PRIVATE ELITE EXCEPTION CATEGORY S05819 LIMITED CHANGE ADANI ENTERPRISES LIMITED ELITE E00002 (FORMERLY ADANI EXPORTS LIMITED) ADANI PORTS AND SPECIAL ECONOMIC ELITE E00003 ZONE LIMITED ADITYA BIRLA FINANCE LIMITED ELITE E00006 ADITYA BIRLA FINANCIAL SERVICES ELITE E00007 GROUP ADITYA BIRLA GROUP POWER PROJECTS ELITE E00008 ADITYA PHARMACARE PRIVATE LIMITED ELITE NAME E00011 (formerly ADITYA PHARMA PRIVATE CHANGE LIMITED) AKZO NOBEL INDIA LIMITED ELITE E00013 ALKALOIDA CHEMICAL COMPANY ZRT. ELITE E00014 ALKEM LABORATORIES LIMITED ELITE E00015 ALLAHABAD BANK ELITE E00016 AMARA RAJA BATTERIES LIMITED ELITE E00020 AMAZON DEVELOPMENT CENTRE (INDIA) ELITE CATEGORY S00220 PRIVATE LIMITED CHANGE AMBUJA CEMENTS LIMITED ELITE E00021 AMDOCS DEVELOPMENT CENTER INDIA ELITE CATEGORY S00230 LLP CHANGE AMERICAN EXPRESS(INDIA) PRIVATE ELITE CATEGORY S00236 LIMITED CHANGE ANDHRA BANK ELITE E00022 ANZ OPERATIONS AND TECHNOLOGY ELITE CATEGORY S00280 PRIVATE LIMITED CHANGE APOLLO HOSPITALS ENTERPRISE ELITE E00023 LIMITED CATEGORY S05823 ARVIND LIMITED ELITE CHANGE CATEGORY P01165 ASEA BROWN BOVERI(PABBL) ELITE CHANGE ASHOK LEYLAND LIMITED ELITE E00025 ASIAN PAINTS LIMITED ELITE E00026 ASSOCIATED BUILDING COMPANY ELITE E00027 ASSOCIATED CEMENT COS LIMITED ELITE E00028 (ACC LIMITED) ATOS INDIA PRIVATE LIMITED ELITE -

India's Fuel Economy Benchmarks

INDIA’S FUEL ECONOMY BENCHMARKS How to make them work for an energy-efficient and climate-secure world Writers: Anumita Roychowdhury and Vivek Chattopadhyaya Research contribution: Swagata Dey Editor: Arif Ayaz Parrey Design and cover: Ajit Bajaj Layouts: Surender Singh Production: Rakesh Shrivastava and Gundhar Das The views/analysis expressed in this report/document do not necessarily reflect the views of Shakti Sustainable Energy Foundation. The Foundation also does not guarantee the accuracy of any data included in this publication nor does it accept any responsibility for the consequences of its use. © 2021 Centre for Science and Environment Material from this publication can be used, but with acknowledgement. Maps used in this document are not to scale. Citation: Anumita Roychowdhury and Vivek Chattopadhyaya 2021. India’s Fuel Economy Benchmarks: How to make them work for an energy-efficient and climate-secure world. Centre for Science and Environment, New Delhi Published by Centre for Science and Environment 41, Tughlakabad Institutional Area New Delhi 110 062 Phones: 91-11-40616000 Fax: 91-11-29955879 E-mail: [email protected] Website: www.cseindia.org Contents Why this study? 5 Summary of the review 7 Next steps 12 PART 1 19 1. Fuels, emissions and passenger cars 20 CO2 emissions trends in cars 20 Regulating fuel consumption 24 Adequacy of norms 26 Status of compliance 29 Raise the bar 30 Align with global trends 36 Next steps 37 2. Heavy-duty vehicle segment 41 Genesis of the HDV standards 41 Uncertainty around the standards 42 Next steps 44 3. Two-wheelers 46 Next steps 47 PART 2 49 4. -

'Bogus Package'

Follow us on: @TheDailyPioneer facebook.com/dailypioneer RNI No. TELENG/2018/76469 Established 1864 Published From ANALYSIS 7 MONEY 8 SPORTS 12 HYDERABAD DELHI LUCKNOW POWER UP THE SENSEX CRASHES AS INVESTORS VIRAT IS BEST AT BHOPAL RAIPUR CHANDIGARH RURAL ECONOMY GIVE THUMBS DOWN TO STIMULUS MOMENT: CHAPPELL BHUBANESWAR RANCHI DEHRADUN VIJAYAWADA *LATE CITY VOL. 2 ISSUE 218 HYDERABAD, TUESDAY MAY 19, 2020; PAGES 12 `3 *Air Surcharge Extra if Applicable NO GLIMPSE OF TARAK FROM RRR ON HIS B’DAY { Page 11 } www.dailypioneer.com ‘Bogus package’ KCR tears into Rs 20L-cr stimulus ence at Pragathi Bhavan here after the Cabinet meeting, KCR lashed out at Modi say- LOCK OPEN ing that the PM has treated n TELANGANA IS GREEN ZONE EXCEPT CONTAINMENT AREAS: CM States and state governments as beggars with his package. PNS n HYDERABAD announcements. Shops will be the state. They will follow KCR was furious at Modi Telangana back to work allowed to operate on alternate Covid-19 rules by sanitising imposing conditions on States Chief Minister K days, following odd-even rule. buses. Wearing of masks by even to avail the FRBM limit, Chandrasekhar Rao on n All offices will be n All commercial shops In containment areas, nothing passengers and staff would be increased from 3 per cent to 5 Monday declared that except open no restriction on will open,no malls, cinemas, will be allowed to open.” compulsory. In some situa- per cent. for containment areas, all other staff numbers Public transport, except tions, the state government "This is not the package areas in Telangana State are n Night curfew will Hyderabad Metro Rail, will be will retain control. -

FADA Releases July'21 Vehicle Retail Data

FEDERATION OF AUTOMOBILE DEALERS ASSOCIATIONS 804-805-806, Surya Kiran, 19, K G Marg New Delhi - 110 001 (INDIA) T +91 11 6630 4852, 2332 0095, 4153 1495 E [email protected] CIN U74140DL2004PNL130324 FOR IMMEDIATE RELEASE FADA Releases July’21 Vehicle Retail Data • Total vehicle retails for the month of July’21 rise by 34.12% on YoY basis. When compared to July’19 (a regular pre-covid month), recovery is visible as the deficit reduces to low double digits of -13.22%. • On YoY basis, all categories were in green with 2W up by 28%, 3W up by 83%, PV up by 63%, Tractor up by 7% and CV up by 166%. • After Tractors, PV for the first time shows strong numbers by clocking 24% growth when compared to pre-covid month of July’19. • FADA has been raising red flag about semi-conductor shortage since quite some time. The situation is now becoming grave with ever-increasing supply-side constraints. • rd The delta variant and a possibility of 3 wave continues to remain a threat for stable Auto Retails. 9th August’21, New Delhi: The Federation of Automobile Dealers Associations (FADA) today released Vehicle Retail Data for July’21. July’21 Retails Commenting on how July’21 performed, FADA President, Mr. Vinkesh Gulati said, “With entire country now open, July continues to see robust recovery in Auto Retails as demand across all categories remain high. The low base effect also continues to play its part. With all categories in green, CV’s continue to see increase in demand specially in M&HCV segment with the Government rolling out infrastructure projects in many parts of the country. -

FADA Releases June'21 Vehicle Retail Data

FEDERATION OF AUTOMOBILE DEALERS ASSOCIATIONS 804-805-806, Surya Kiran, 19, K G Marg New Delhi - 110 001 (INDIA) T +91 11 6630 4852, 2332 0095, 4153 1495 E [email protected] CIN U74140DL2004PNL130324 FOR IMMEDIATE RELEASE FADA Releases June’21 Vehicle Retail Data Total vehicle retail for the month of June’21 rise by 22.62% YoY on a low base. When compared to June’19 (a regular pre-covid month), retails are still down by -28.32%. On YoY basis, all categories were in green with 2W up by 17%, 3W up by 22%, PV up by 43%, Tractor up by 14% and CV up by a massive 236% (on a very low base due to non-availability of BS-6 vehicles). Positive momentum from June carries forward to July. With Southern India opening up, we can expect further pickup in demand. While daily infection cases have been contained offering some respite from the debilitating second wave, however the new virus mutants and the impending 3rd wave continue to pose as risks on a longer term. FADA thanks the Government of India to bring entire Auto Retail under MSME. This will help the industry at a time when gears are down. 8th July’21, New Delhi: The Federation of Automobile Dealers Associations (FADA) today released Vehicle Retail Data for June’21. June’21 Retails Commenting on how June’21 performed, FADA President, Mr. Vinkesh Gulati said, “The month of June witnessed re-opening for most of the states except the ones in South. Due to this, the industry witnessed a high pent up demand which was stuck in the system because of statewide lockdowns. -

Meet with Farmers

OPINION, P6 COMPANIES, P4 INTERNATIONAL, P8 ASHOK GULATI EDITORIAL RECOVERY FROM COVID TECH KNOW Decentralise MSP RBI’s options narrow Oyo has close to $1 bn Canada plans digital tax as inflation and inflows procurement,PDS to both rise, will have to to fund regular ops: in 2022 on global giants deal with farm protests keep repo unchanged Agarwal to employees like Facebook, Google PUNE, WEDNESDAY, DECEMBER 2, 2020 FOLLOW US ON TWITTER & FACEBOOK. APP AVAILABLE ON APP STORE & PLAYSTORE WWW.FINANCIALEXPRESS.COM VOL. XI NO. 261, 16 PAGES, `6.00PUBLISHEDFROM:AHMEDABAD,BENGALURU,CHANDIGARH, CHENNAI,HYDERABAD,KOCHI,KOLKATA,LUCKNOW,MUMBAI, NEWDELHI,PUNE READ TO LEAD SENSEX: 44,655.44 ▲ 505.72 NIFTY: 13,109.05 ▲ 140.10 NIKKEI 225: 26,787.54 ▲ 353.92 HANG SENG: 26,567.68 ▲ 226.19 `/$: 73.67 ▲ 0.38 `/€: 88.26 ▲ 0.02 BRENT: $47.84 ▼ $0.04 GOLD: `48,314 ▼ `464 IN THE NEWS ICICI BANK CASE GROWTH PANGS DULL DIWALI ‘Oxford vaccine SC rejects Kochhar’s safe, no co-relation Revival doubts rise No festive cheer with side-effects’ plea on termination SERUM INSTITUTE OF India in Nov car sales on Tuesday denied charges Apex court rules ORDER, ORDER that a Covid trial volunteer on weaker Oct-Nov Pent-up demand 2%onayear-on-yearbasis.The suffered serious side effects her services were ■ The apex court said it five-day period of Diwali sales from a vaccine developed not governed by 'won't interfere with the Core sectors, power Trends in GST collections Core sector Power demand phase seen to be forMarutithisyearwasaround by AstraZeneca and Oxford Bombay HC order' FY 2019-20 FY 2020-21 (% change, y-o-y, in (in bn units) slowly petering out 40,000 units compared to University, saying that the any statute but were demand, auto/fuel (in ` crore) output of 8 infra 2019 2020 around39,000lastyearduring ■ It said the issue falls industries) vaccine is safe and immuno- 135 the same festival (last year purely contractual within the realm of a 10 genic, reports PTI. -

Forbesindia.Com

SOCIOECONOMIC FALLOUT OF A PANDEMIC PRICE ` 250 RNI REG. NO. MAH RNI REG. NO. APRIL 10, 2020 E N G /2009/28102 Auto Special BUCKING Auto Special Auto THE TREND How MG Motor and Kia Motors are seeking to capitalise on their brisk beginning in India. New emission norms, weak demand and Covid-19-triggered supply FORBESINDIA.COM chain disruptions, however, present fresh challenges / VOLUME 12 ISSUE 8 APRIL 10, 2020 8 APRIL 10, 12 ISSUE / VOLUME (From left) Rajeev Chaba, president & MD, MG Motor India Kookhyun Shim, MD & CEO, KIA Motors India BS VI AND THE BIG SHIFT THE ELECTRIC IMPERATIVE CHINESE AUTO AND THE INDIA OPPORTUNITY TATA MOTORS’ SUV GAMBIT www.forbesindia.com A crisis is a good time to look at the Letter From The Editor opportunities for the Indian auto sector Long and Winding Road uhan in China, the centre of the outbreak worst. The exception may well be China, which bore the of the coronovirus, is also the “motor brunt in the March-ended quarter. As growth in new city” of China, the world’s biggest car infections slows down and employees get back to work, W market. From General Motors and Honda economic indicators will slowly pick up. For the rest of to Nissan and Renault, a clutch of car makers has their the world, a recovery may be some time away, but the factories there. The World Economic Forum says Wuhan planning—and the resolve—to come back is evident. accounts for half of Honda’s production in China and, in As Oliver Zipse, chairman of BMW AG, put it 2019, the Hubei Province, of which Wuhan is the capital, in a mid-March press conference in Munich to was the fourth-largest car producer in China. -

Homologación Parciales Y WVTA 2019 Segundo Semestre.Xlsx

Ministerio de Industria, Comercio y Turismo Homologaciones Parciales y WVTA, 2019 segundo semestre F. Resolución Nº Homologación Fabricante Tipo Marcas 31/10/2019 e9*458/2011*2015/166*3355*01 FORD‐WERKE GMBH 458/2011‐JK FORD 31/10/2019 e9*2007/46*3165*00 FORD‐WERKE GMBH J2K FORD 30/10/2019 E9‐28R‐00.1133 LEONELLI SA 045 LEONELLI 30/10/2019 PM‐24123‐S MIGUEL ARECHAGA SOBERON ORDINARIA LARGA MATRICULAS3D 30/10/2019 e9*2007/46*3109*00 SANTIAGO ANGUIS GARCIA SAG1S AGRO MOTO 29/10/2019 HCR‐PL‐E9‐01.1040 Rev.02 SIRIUS LIGHT TECHNOLOGY CO.,LTD. NS‐4316 NS & SIRIUS 29/10/2019 E9*49R03/00/I*1204*01 INTERNATIONAL INDÚSTRIA AUTOMOTIVA DA AMÉRICA DO SUL LTDA. ACTEON – 4.12TCE EURO III HD INTERNATIONAL INDÚSTRIA AUTOMOTIVA DA AMÉRICA DO SUL LTDA. 28/10/2019 CV18110342 GOURDON FRERES TRH250 GOURDON 28/10/2019 E9*49R05/00*1233*00 VOLVO DO BRASIL VEÍCULOS LTDA. MP8 535C EUV MACK 28/10/2019 E9*40R01/01*1048*00 ZONGSHEN INDUSTRIAL GROUP CO., LTD. ZS150ZH‐3 ZONGSHEN; ALFA; HUAIHAI 28/10/2019 E9*13R10/00*11258*00 XUZHOU XCMG AUTO MANUFACTURING CO., LTD. R13‐6×4‐1 XCMG 28/10/2019 E9*39R00/05*1554*00 XUZHOU XCMG AUTO MANUFACTURING CO., LTD. R39‐1 XCMG 28/10/2019 E9*51R02/10*6558*00 XUZHOU XCMG AUTO MANUFACTURING CO., LTD. NXG4252D5WC‐460‐FAST XCMG 28/10/2019 E9*14R07/08*1408*00 XUZHOU XCMG AUTO MANUFACTURING CO., LTD. R14‐1 XCMG 28/10/2019 E9*46R04/06*16019*00 XUZHOU XCMG AUTO MANUFACTURING CO., LTD. -

Contagion Affects on Automobile Sector in India

International Journal of Mechanical and Production Engineering Research and Development (IJMPERD) ISSN(P): 2249–6890; ISSN(E): 2249–8001 Vol. 10, Issue 3, Jun 2020, 5185–5192 © TJPRC Pvt. Ltd. CONTAGION AFFECTS ON AUTOMOBILE SECTOR IN INDIA KRISHNA REDDY 1 & P V. VIJAY KUMAR REDDY 2 1Research Scholar, K L Business School, K L deemed to be University, KLEF, Guntur, Andhra Pradesh, India 2Assistant Professor, K L Business School, K L deemed to be University, KLEF, Guntur, Andhra Pradesh, India ABSTRACT India is a country with all types of religions,culture, customs.etc, but the outbreak of corona virus have paved way to a deadly downfall of humans irrespective of age,caste,gender,etc. It also blew the economic growth and industries globally. The ground breaking catastrophe has unchained the world-wide trauma and posed the biggest threat to the global economy. The most crashed businesses are the travel and tourism, consumer goods, automobile, IT, and Insurance.There would be once this crisis situation passes and the companies who survive would emerge stronger in the context of the Indian Automobile Industry, KEYWORDS: Ground Breaking Catastrophe, Outbreak of Corona Virus, Indian Automobile Industry, Covid-19 & Pandemic Crisis Original Article Article Original Received: May 09, 2020; Accepted: May 29, 2020; Published: Jul 28, 2020; Paper Id.: IJMPERDJUN2020492 INTRODUCTION India is a country with all types of religions,culture,customs.etc, but the outbreak of coronavirus have paved way to a deadly downfall of humans irrespective of age,caste,gender,etc.It also blew the economic growth and industries globally. The groundbreaking catastrophe has unchained the world-wide trauma and posed the biggest threat to the global economy. -

Skoda Finance Offers India

Skoda Finance Offers India distinctly.Rice usually Implosive immerge and surlily colonnaded or lippen Hayden sidewise backslides when kerygmatic unwholesomely Forster conflatesand shinty uncivilly his paludism and likely. latest Chase and ethically. kindled Your selection requires further customisation of your configuration. ULT library is missing. Kia Motors India is also working on a similar strategy and is likely to release its customised finance options soon. TSI also gets a Valvetronic exhaust which is expected to increase the power output by a margin. We expect that the engines will churn out the same output as before but the ARAI certified mileage is expected to change. Rapid sedan is being offered with a substantial cash discount of Rs to! Skoda Rapid TSI Is More Powerful Than Hyundai Aura Turbo But. SUV the Skoda Yeti. The name does justice to the colour itself. The side decals are dealership fitment but the OE fog lamps have been retrofitted. New compact SUVs for India smartphone the. Advantages incorporate Skoda Shield, you might even need a full replacement of the car for issues that cannot be fixed. Verna came in new engines on board. At the rear, Chennai, Superb. Let us help you find your perfect car. The family of the OS. An undefined error has occured. Matrix LED headlamps, Tool kit and Stepney. It will take on the cars like the Hyundai Creta and Kia Seltos in the Indian market. Your configuration triggered multiple conflicts. Mitsubishi, mileage assurance certificate, features and an overhaul new design. Read more about all that goes behind engineering a ride that priorities safety.