The Costs of Payment Methods in the Retail Sector

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Set of Rules for AAU Credit Cards with Corporate Liability - Staff

Aalborg University Set of rules for AAU credit cards with corporate liability - staff Disclaimer This set of rules for AAU credit cards with corporate liability has been translated into English from the Danish language. However, the original Danish text shall be the governing text for all purposes and in any discrepancies. Finance and Accounts Department Translated into English 28 May 2014 Contents 1. Introduction ..................................................................................................................................................2 2. Who can obtain an AAU credit card with corporate liability? ......................................................................2 3. Application for a credit card with corporate liability ...................................................................................2 4. Personal data ................................................................................................................................................2 5. Receipt of credit card and PIN ......................................................................................................................3 6. Card holder's obligations ..............................................................................................................................3 7. User guide for holders of credit cards with corporate liability ....................................................................3 8. Settlement of e-transactions on credit cards with corporate liability ..........................................................4 -

Word Files Coverted

About MasterCard International: MasterCard International is a leading global payments solutions company that provides a broad variety of innovative services in support of their global members' credit, deposit access, electronic cash, business-to-business and related payment programs. MasterCard international manages a family of well-known, widely accepted payment cards brands including MasterCard®, Maestro®, and Cirrus® and serves financial institutions, consumers and businesses in over 210 countries and territories. What is a Debit Card: Maestro® is the Global Debit Card cum ATM Card product of MasterCard International. This card can be used to make on-line bill payments through 49,000 Point of Sale (POS) terminals in India and 70,00,000 merchant establishments worldwide exhibiting “MAESTRO” logo. In other words the Debit Card holder can pay their bills, at shops exhibiting “Maestro” Logo, using this card instead by cash or cheque. The card holder need not carry cash in future when all the shops provide this facility. SIB's Debit Card can also be used as an ATM card within the ATM network of the Bank. People around the world prefer debit card over credit card since the spending can be restricted to what they have in their account. Since payment is effected only if there is available balance in the customer's account, it is absolutely risk-free for the banks. SIB plans to issue debit cards liberally as an added convenience to its customers which in turn reduces the pressure on cash transactions at the counters. How is CIRRUS relevant to other bank's Maestro Card holders: SIB has acquired “CIRRUS”, the product of MasterCard International. -

The Millennials Influence

RESEARCH 2016 THE MILLENNIAL INFLUENCE HOW MILLENNIALS OF THE USA WILL SHAPE TOMORROW’S PAYMENTS LANDSCAPE USA INTRODUCTION CONTENTS INTRODUCTION 3 This research into US millennials’ Millennials are coming of age – the I hope you find these insights and payments behavior is part of our long- oldest of them are hitting the peak of themes both interesting and useful WHAT ARE WE TALKING ABOUT? 4 standing commitment to play a leading their economic productivity and their and encourage you to continue the role in the discussion about the future of greatest purchasing power. Their choices, debate through our online hub OUR AIMS AND APPROACH 5 payments systems. their behaviors and their concerns are Vocalink CONNECT. MILLENNIALS AND THEIR TECH 6 set to profoundly shape developments Having been at the forefront of across every spectrum of business and SOCIAL MILLENNIALS 8 developments in our industry for 60 commerce, and nowhere more so than years, we see proprietary research and in how they access their money. Starting MILLENNIALS AND THEIR MONEY 10 market analysis as a fundamental part in the US, and moving to South East Asia of our offering. As providers of the and Europe, we are taking a close look CARA O’NIONS HOW MILLENNIALS LIKE TO PAY 12 infrastructure through which so much at what millennials are saying about how MARKETING AND CUSTOMER of business and personal commerce INSIGHT DIRECTOR THE MILLENNIAL INFLUENCE 14 they want to pay and what this means for is conducted, we are uniquely well- the next generation of payments. HOW MILLENNIALS LIKE TO BE PAID 16 placed to explore and offer insight on emerging trends and behaviors For us this has already been a MILLENNIALS AND MOBILE PAYMENTS 18 in the way people and organizations fascinating journey, and we’re only want to access and move their money. -

Authorisation Service Sales Sheet Download

Authorisation Service OmniPay is First Data’s™ cost effective, Supported business profiles industry-leading payment processing platform. In addition to card present POS processing, the OmniPay platform Authorisation Service also supports these transaction The OmniPay platform Authorisation Service gives you types and products: 24/7 secure authorisation switching for both domestic and international merchants on behalf of merchant acquirers. • Card Present EMV offline PIN • Card Present EMV online PIN Card brand support • Card Not Present – MOTO The Authorisation Service supports a wide range of payment products including: • Dynamic Currency Conversion • Visa • eCommerce • Mastercard • Secure eCommerce –MasterCard SecureCode, Verified by Visa and SecurePlus • Maestro • Purchase with Cashback • Union Pay • SecureCode for telephone orders • JCB • MasterCard Gaming (Payment of winnings) • Diners Card International • Address Verification Service • Discover • Recurring and Installment • BCMC • Hotel Gratuity • Unattended Petrol • Aggregator • Maestro Advanced Registration Program (MARP) Supported authorisation message protocols • OmniPay ISO8583 • APACS 70 Authorisation Service Connectivity to the Card Schemes OmniPay Authorisation Server Resilience Visa – Each Data Centre has either two or four Visa EAS servers and resilient connectivity to Visa Europe, Visa US, Visa Canada, Visa CEMEA and Visa AP. Mastercard – Each Data Centre has a dedicated Mastercard MIP and resilient connectivity to the Mastercard MIP in the other Data Centre. The OmniPay platform has connections to Banknet for both European and non-European authorisations. Diners/Discover – Each Data Centre has connectivity to Diners Club International which is also used to process Discover Card authorisations. JCB – Each Data Centre has connectivity to Japan Credit Bureau which is used to process JCB authorisations. UnionPay – Each Data Centre has connectivity to UnionPay International which is used to process UnionPay authorisations. -

(Automated Teller Machine) and Debit Cards Is Rising. ATM Cards Have A

Consumer Decision Making Contest 2001-2002 Study Guide ATM/Debit Cards The popularity of ATM (automated teller machine) and debit cards is rising. ATM cards have a longer history than debit cards, but the National Consumers League estimates that two-thirds of American households are likely to have debit cards by the end of 2000. It is expected that debit cards will rival cash and checks as a form of payment. In the future, “smart cards” with embedded computer chips may replace ATM, debit and credit cards. Single-purpose smart cards can be used for one purpose, like making a phone call, or riding mass transit. The smart card keeps track of how much value is left on your card. Other smart cards have multiple functions - serve as an ATM card, a debit card, a credit card and an electronic cash card. While this Study Guide will not discuss smart cards, they are on the horizon. Future consumers who understand how to select and use ATM and debit cards will know how to evaluate the features and costs of smart cards. ATM and Debit Cards and How They Work Electronic banking transactions are now a part of the American landscape. ATM cards and debit cards play a major role in these transactions. While ATM cards allow us to withdraw cash to meet our needs, debit cards allow us to by-pass the use of cash in point-of-sale (POS) purchases. Debit cards can also be used to withdraw cash from ATM machines. Both types of plastic cards are tied to a basic transaction account, either a checking account or a savings account. -

B+S Card Service: Transaction Volume Grows – Newly Established Top Management

Press release B+S Card Service: Transaction Volume Grows – Newly Established Top Management Frankfurt/Main, January 28th 2013. Once again, in the just ended fiscal year 2012 (October 2011 thru September 2012), B+S Card Service was able to grow processing volume originating from the processing of card payment transactions. In whole, B+S, a partly owned subsidiary of Deutscher Sparkassenverlag, processed payments amounting to 23.1 billion Euros (2 per cent increase) – the B+S all-time corporate record since start up in 1989. At the end of the 2012 fiscal year, B+S had more than 227,000 customers in fourteen European countries. As one of the few companies not only offering one-stop network and POS but also comprehensive acquiring services, B+S currently operates approximately 167,000 payment terminals that processed roughly 553 Million transactions during the fiscal year. B+S Innovation in Contactless Payment In 2011/12, the focus in particular was on product development for contactless payments. B+S started the service of payment processing compliant to the new girogo payment process and as first service provider even introduced two further contactless-enabled payment terminals H5000 and VX820 to the German market. The product portfolio was honoured with numerous awards, most recently with an innovation prize sponsored by the Deutscher Sparkassen- und Giroverband (German Savings Banks Association, DSGV) contactless payments terminal competition.“. - 1 - „From a product perspective, contactless payment remains the central issue for our company“, B+S managing director Matthias Kaufmann explains. “Especially in Germany it accelerates the existing trend towards distinctly more cashless payments. -

Sonderbedingungen Für Die Girocard (Fassung

Girocard (Debit Card) The present translation is furnished for the customer’s convenience only. The original German text is binding in all respects. Special Terms and Conditions In the event of any divergence between the English and the German texts, A. Guaranteed Types of Payment constructions, meanings, or interpretations, the German text, construction, meaning B. Other Bank Services or interpretation shall govern exclusively. C. Additional Applications D. Amicable Dispute Resolution and Other Possibilities for Complaints A. Guaranteed Types of Payment I. Scope of Application Girocard is a debit card. Card Holder may use the Card for the below payment services if the Card and the terminals are equipped accordingly: 1 in connection with a personal identification number (PIN) with all German debit card systems: a) for withdrawing cash at cash machines belonging to the German cash machine system showing the girocard logo; b) for using it with retailers and services providers at automated tills belonging to the German girocard system showing the girocard logo (“Girocard Terminals”); c) for topping up prepaid mobile phone accounts at cash machines which a user has with a mobile phone operator if the cash machine operator offers such services and the mobile phone operator participates in the system. 2 in connection with a personal identification number (PIN) with third-party debit card systems: a) for withdrawing cash at cash machines belonging to third-party cash machine systems if the card is equipped accordingly; b) for using it with retailers and services providers at automated tills belonging to third-party systems if the card is equipped accordingly; c) for topping up prepaid mobile phone accounts at third-party cash machines which a user has with a mobile phone operator if the cash machine operator offers such services and the mobile phone operator participates in the system, whereby Card acceptance by third-party systems is subject to the third-party system acceptance logo. -

ATM and Debit Card Safety Tips P1

ATM DEBIT CARD SAFETY TIPS Sensible Steps for: Personal Safety Account Security Identity Theft Protection ATM and Debit Card Safety and Security ith the banking convenience made possible with Automated Teller Machines WW (ATMs) and other Point of Sale terminals comes an increased need for security and personal caution. This includes protecting your ATM card number, Debit Card number, Personal Identication Number (PIN), and cash, and being aware of the condition of the machine and your surroundings. It’s no longer enough to take measures to protect your physical safety and your cash after a transaction at the ATM – now you must be aware of cameras and skimming devices that secretly record (steal) your bank account numbers and PIN numbers. Here are some other tips for safer transactions both Electronic and Personal: Electronic Safety Tips PROTECT YOUR CARD AND PIN Protect your ATM and debit cards as if they were cash. Report lost or stolen cards immediately. Don’t write your Personal Identication Number (PIN) on your card or give the number out to anyone, including friends and family, and do not reveal it to anyone over the phone. Avoid using numbers that are easily identied (birth date, phone number, etc.) with your personal identity. CONDUCT YOUR TRANSACTIONS PRIVATELY Use common courtesy at the ATM. Give people ahead of you space to conduct their transactions. When you use the ATM conduct your business quickly and eciently, make sure no one watches you key in your PIN number. Use your body and free hand to shield the ATM keypad during the transaction. -

CONSUMER DEBIT CARD ATM CARD Look for These Logos at ATM

CONSUMER DEBIT CARD ATM CARD Make purchases plus get cash fast at ATMs Get cash fast at ATMs Applicant Name: New Student _____________________________________________________________ Card Type: Sunset Eagle Your card and PIN will be sent to the address on your account statement. Please speak to an Account Representative for special mailing __________________________________ CHECKING ACCOUNT NUMBER accommodations. (Required for Debit Card __________________________________ Last 4 digits of Applicant’s Social Security Number: ___________________ SECONDARY CHECKING ACCOUNT NUMBER __________________________________ Daytime Phone: Evening or Message Phone: SAVINGS ACCOUNT NUMBER __________________________ __________________________ __________________________________ Reason for new card (lost, damage, etc.) I hereby request that I be issued a First Bank Consumer Debit card or a ATM card and Personal Identification Number for use at merchant locations, point-of-sale terminals (Consumer Debit Card only) and automated teller machines (ATMs) to access my account(s) at First Bank. I understand that I may use my card to access my savings account through an ATM only. I also acknowledge receipt of an Electronic Funds Transfer Disclosure and a Cardholder Agreement, and understand that use of my Consumer Debit Card or ATM card shall governed by the terms and conditions applicable to my account(s), to the terms of the Cardholder Agreement, by laws, rules, regulations or applicable law, and such terms, conditions, and/or amendments as may be established from time to time and communicated to me in writing. ________ As the parent/guardian on this account, I understand that I am responsible for the Please Initial transactions conducted by the minor owner. Applicant’s Signature Date If applicable, Parent Signature Date In order to expedite the processing of your application form, please remember: 1. -

New Debit Card Solutions At

New Debit Card Solutions Debit Mastercard and Visa Debit are ready Swiss Banking Services Forum, 22 May 2019 Philippe Eschenmoser, Head Cards & A2A, Swisskey Ltd Maestro/V PAY Have Established Themselves As the “Key to the Account” – Schemes, However, Are Forcing Market Entry For Successor Products Response from the Maestro and V PAY are successful… …but are not future-capable products schemes # cards Maestro V PAY on Lower earnings potential millions8 for issuers as an alternative payment traffic products (e.g. 6 credit cards, TWINT) Issuer 4 V PAY will be 2 decommissioned by VISA Functional limitations: in 20211 – Visa Debit as 0 • No e-commerce the successor 2000 2018 • No preauthorizations Security and stability have End- • No virtualization proven themselves customer High acceptance in CH and Merchants with an online MasterCard is positioning abroad in Europe offer are demanding an DMC in the medium term online-capable debit as the successor to Standard product with an Merchan product Maestro integrated bank card t 2 1: As of 2021 no new V PAY may be issued TWINT (Still) No Substitute For Debit Cards – Credit Cards With Divergent Market Perception TWINT (still) not alternative for debit Credit cards a no alternative for debit Lacking a bank card Debit function Limited target group (age, ~1.1 M 1 ~10 M. creditworthiness...) Issuer ~48.5 k ~170 k1 No direct account debiting DMC/ Visa Debit Potentially high annual fee End-customer Lower customer penetration Banks and merchants DMC/ P2P demand an online- Higher costs Merchant Visa Debit -

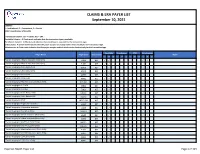

Claims and Remits Payer List

CLAIMS & ERA PAYER LIST September 10, 2021 LEGEND: I = Institutional, P = Professional, D = Dental COB = Coordination of Benefits Transaction Column: 837 = Claims, 835 = ERA Available Column: A Check-mark indicates that the transaction type is available. Enrollment Column: A Check-mark indicates that enrollment is required for the transaction type. COB Column: A Check-mark Indicates that the payer accepts secondary claims electronically for the transaction type. Attachments: A Check-mark indicates that the payer accepts medical attachments electronically for the transaction type. Available Enrollment COB Attachments Payer Name Payer Code Transaction Notes I P D I P D I P D I P D *Carisk Imaging to Allstate Insurance (Auto Only) E1069 837 ✓ ✓ ✓ ✓ *Carisk Imaging to Allstate Insurance (Auto Only) E1069 835 ✓ ✓ *Carisk Imaging to Geico (Auto Only) GEICO 837 ✓ ✓ ✓ ✓ *Carisk Imaging to Geico (Auto Only) GEICO 835 ✓ ✓ *Carisk Imaging to Nationwide A0002 837 ✓ ✓ ✓ ✓ *Carisk Imaging to Nationwide A0002 835 ✓ ✓ *Carisk Imaging to New York City Law Department NYCL001 837 ✓ ✓ ✓ ✓ *Carisk Imaging to NJ-PLIGA E3926 837 ✓ ✓ ✓ ✓ *Carisk Imaging to NJ-PLIGA E3926 835 ✓ ✓ *Carisk Imaging to North Dakota WSI NDWSI 837 ✓ ✓ ✓ ✓ *Carisk Imaging to North Dakota WSI NDWSI 835 ✓ ✓ *Carisk Imaging to NYSIF NYSIF1510 837 ✓ ✓ ✓ ✓ *Carisk Imaging to Progressive Insurance E1139 837 ✓ ✓ ✓ ✓ *Carisk Imaging to Progressive Insurance E1139 835 ✓ ✓ *Carisk Imaging to Pure (Auto Only) PURE01 837 ✓ ✓ ✓ ✓ *Carisk Imaging to Safeco Insurance (Auto Only) E0602 837 ✓ ✓ ✓ ✓ -

Mastercard Frequently Asked Questions Platinum Class Credit Cards

Mastercard® Frequently Asked Questions Platinum Class Credit Cards How do I activate my Mastercard credit card? You can activate your card and select your Personal Identification Number (PIN) by calling 1-866-839-3492. For enhanced security, RBFCU credit cards are PIN-preferred and your PIN may be required to complete transactions at select merchants. After you activate your card, you can manage your account through your Online Banking account and/or the RBFCU Mobile app. You can: • View transactions • Enroll in paperless statements • Set up automatic payments • Request Balance Transfers and Cash Advances • Report a lost or stolen card • Dispute transactions Click here to learn more about managing your card online. How do I change my PIN? Over the phone by calling 1-866-297-3413. There may be situations when you are unable to set your PIN through the automated system. In this instance, please visit an RBFCU ATM to manually set your PIN. Can I use my card in my mobile wallet? Yes, our Mastercard credit cards are compatible with PayPal, Apple Pay®, Samsung Pay, FitbitPay™ and Garmin FitPay™. Click here for more information on mobile payments. You can also enroll in Mastercard Click to Pay which offers online, password-free checkout. You can learn more by clicking here. How do I add an authorized user? Please call our Member Service Center at 1-800-580-3300 to provide the necessary information in order to qualify an authorized user. All non-business Mastercard account authorized users must be members of the credit union. Click here to learn more about authorized users.