Agile Property Holdings Limited, a Company Incorporated in the Cayman Islands, the Shares of Which Are Listed on the Main Board of the Stock Exchange

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Fidelity® Emerging Markets Index Fund

Quarterly Holdings Report for Fidelity® Emerging Markets Index Fund January 31, 2021 EMX-QTLY-0321 1.929351.109 Schedule of Investments January 31, 2021 (Unaudited) Showing Percentage of Net Assets Common Stocks – 92.5% Shares Value Shares Value Argentina – 0.0% Lojas Americanas SA rights 2/4/21 (b) 4,427 $ 3,722 Telecom Argentina SA Class B sponsored ADR (a) 48,935 $ 317,099 Lojas Renner SA 444,459 3,368,738 YPF SA Class D sponsored ADR (b) 99,119 361,784 Magazine Luiza SA 1,634,124 7,547,303 Multiplan Empreendimentos Imobiliarios SA 156,958 608,164 TOTAL ARGENTINA 678,883 Natura & Co. Holding SA 499,390 4,477,844 Notre Dame Intermedica Participacoes SA 289,718 5,003,902 Bailiwick of Jersey – 0.1% Petrobras Distribuidora SA 421,700 1,792,730 Polymetal International PLC 131,532 2,850,845 Petroleo Brasileiro SA ‑ Petrobras (ON) 2,103,697 10,508,104 Raia Drogasil SA 602,000 2,741,865 Bermuda – 0.7% Rumo SA (b) 724,700 2,688,783 Alibaba Health Information Technology Ltd. (b) 2,256,000 7,070,686 Sul America SA unit 165,877 1,209,956 Alibaba Pictures Group Ltd. (b) 6,760,000 854,455 Suzano Papel e Celulose SA (b) 418,317 4,744,045 Beijing Enterprises Water Group Ltd. 2,816,000 1,147,720 Telefonica Brasil SA 250,600 2,070,242 Brilliance China Automotive Holdings Ltd. 1,692,000 1,331,209 TIM SA 475,200 1,155,127 China Gas Holdings Ltd. 1,461,000 5,163,177 Totvs SA 274,600 1,425,346 China Resource Gas Group Ltd. -

The Annual Report on the Most Valuable and Strongest Real Estate Brands June 2020 Contents

Real Estate 25 2020The annual report on the most valuable and strongest real estate brands June 2020 Contents. About Brand Finance 4 Get in Touch 4 Brandirectory.com 6 Brand Finance Group 6 Foreword 8 Executive Summary 10 Brand Finance Real Estate 25 (USD m) 13 Sector Reputation Analysis 14 COVID-19 Global Impact Analysis 16 Definitions 20 Brand Valuation Methodology 22 Market Research Methodology 23 Stakeholder Equity Measures 23 Consulting Services 24 Brand Evaluation Services 25 Communications Services 26 Brand Finance Network 28 © 2020 All rights reserved. Brand Finance Plc, UK. Brand Finance Real Estate 25 June 2020 3 About Brand Finance. Brand Finance is the world's leading independent brand valuation consultancy. Request your own We bridge the gap between marketing and finance Brand Value Report Brand Finance was set up in 1996 with the aim of 'bridging the gap between marketing and finance'. For more than 20 A Brand Value Report provides a years, we have helped companies and organisations of all types to connect their brands to the bottom line. complete breakdown of the assumptions, data sources, and calculations used We quantify the financial value of brands We put 5,000 of the world’s biggest brands to the test to arrive at your brand’s value. every year. Ranking brands across all sectors and countries, we publish nearly 100 reports annually. Each report includes expert recommendations for growing brand We offer a unique combination of expertise Insight Our teams have experience across a wide range of value to drive business performance disciplines from marketing and market research, to and offers a cost-effective way to brand strategy and visual identity, to tax and accounting. -

COVERAGE LIST GEO Group, Inc

UNITED STATES: REIT/REOC cont’d. UNITED STATES: REIT/REOC cont’d. UNITED STATES: NON-TRADED REITS cont’d. COVERAGE LIST GEO Group, Inc. GEO Sabra Health Care REIT, Inc. SBRA KBS Strategic Opportunity REIT, Inc. Getty Realty Corp. GTY Saul Centers, Inc. BFS Landmark Apartment Trust, Inc. Gladstone Commercial Corporation GOOD Select Income REIT SIR Lightstone Value Plus Real Estate Investment Trust II, Inc. Gladstone Land Corporation LAND Senior Housing Properties Trust SNH Lightstone Value Plus Real Estate Investment Trust III, Inc. WINTER 2015/2016 • DEVELOPED & EMERGING MARKETS Global Healthcare REIT, Inc. GBCS Seritage Growth Properties SRG Lightstone Value Plus Real Estate Investment Trust, Inc. Global Net Lease, Inc. GNL Silver Bay Realty Trust Corp. SBY Moody National REIT I, Inc. Government Properties Income Trust GOV Simon Property Group, Inc. SPG Moody National REIT II, Inc. EUROPE | AFRICA | ASIA-PACIFIC | MIDDLE EAST | SOUTH AMERICA | NORTH AMERICA Gramercy Property Trust Inc. GPT SL Green Realty Corp. SLG MVP REIT, Inc. Gyrodyne, LLC GYRO SoTHERLY Hotels Inc. SOHO NetREIT, Inc. HCP, Inc. HCP Sovran Self Storage, Inc. SSS NorthStar Healthcare Income, Inc. UNITED KINGDOM cont’d. Healthcare Realty Trust Incorporated HR Spirit Realty Capital, Inc. SRC O’Donnell Strategic Industrial REIT, Inc. EUROPE Healthcare Trust of America, Inc. HTA St. Joe Company JOE Phillips Edison Grocery Center REIT I, Inc. GREECE: Athens Stock Exchange (ATH) AFI Development Plc AFRB Hersha Hospitality Trust HT STAG Industrial, Inc. STAG Phillips Edison Grocery Center REIT II, Inc. AUSTRIA: Vienna Stock Exchange (WBO) Babis Vovos International Construction S.A. VOVOS Alpha Pyrenees Trust Limited ALPH Highwoods Properties, Inc. -

AGILE GROUP HOLDINGS LIMITED (Incorporated in the Cayman Islands with Limited Liability) (Stock Code: 3383)

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. This announcement does not constitute an offer to sell or the solicitation of an offer to buy any securities in the United States or any other jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. The securities referred to herein will not be registered under the United States Securities Act of 1933, as amended (the “Securities Act”), and may not be offered or sold in the United States except pursuant to an exemption from, or a transaction not subject to, the registration requirements of the Securities Act. Any public offering of securities to be made in the United States will be made by means of a prospectus. Such prospectus will contain detailed information about the company making the offer and its management and financial statements. The Company does not intend to make any public offering of securities in the United States. AGILE GROUP HOLDINGS LIMITED (Incorporated in the Cayman Islands with limited liability) (Stock Code: 3383) OVERSEAS REGULATORY ANNOUNCEMENT This overseas regulatory announcement is issued pursuant to Rule 13.10B of the Rules Governing the Listing of Securities (the “Listing Rules”) on The Stock Exchange of Hong Kong Limited (the “Stock Exchange”). -

Annual Report 2009 Annual Report 2009 Report Annual

KWG PROPERTY HOLDING LIMITED KWG PROPERTY HOLDING LIMITED 合景泰富地產控股有限公司 合景泰富地產 Incorporated in the Cayman Islands with limited liability Stock Code : 1813 Annual Report 2009 Annual Report 2009 合景泰富地產 KWG PROPERTY HOLDING LIMITED 合景泰富地產控股有限公司 Contents 2 Corporate Information 3 Corporate Profile 4 Management Structure of the Group 4 Financial Highlights 6 Major Events for 2009 8 Honours andAwards 16 Letter to the Shareholders 17 Chief Executive Officer’s Report 18 Management Discussion andAnalysis 33 Directors and Senior Management’s Profile 36 Corporate Governance Report 41 Report of the Directors 49 IndependentAuditors’ Report 50 Consolidated Financial Statements 119 Project at a Glance 120 FiveYear Financial Summary Corporate Information Directors Registered Office Principal Bankers Executive Directors Cricket Square Agricultural Bank of China Limited Mr. Kong Jian Min (Chairman) Hutchins Drive Bank of China Limited Mr. Kong JianTao (Chief Executive P.O. Box 2681 China Construction Bank (Asia) Officer) Grand Cayman KY1-1111 Corporation Limited Mr. Kong Jian Nan Cayman Islands China Minsheng Banking Corp. Ltd Mr. Li Jian Ming Industrial and Commercial Bank of Mr.Tsui KamTim Principal Place of Business China (Asia) Limited Mr. HeWei Zhi in Hong Kong Industrial and Commercial Bank of Mr.YuYao Sheng* China Limited Room 6407, 64th Floor Standard Chartered Bank Independent Non-executive Directors Central Plaza, 18 Harbour Road (Hong Kong) Limited Mr. Lee Ka Sze, Carmelo Wanchai, Hong Kong Mr. Dai Feng Auditors Mr.Tam Chun Fai Principal Share Registrar Ernst &Young Company Secretary Butterfield Fulcrum Group (Cayman) Limited Legal Advisors Mr.Tsui KamTim Butterfield House, 68 Fort Street P.O. Box 705, GeorgeTown as to Hong Kong law: Authorized Representatives Grand Cayman KY1-1107 SidleyAustin Cayman Islands Mr. -

KWG Property Holding Limited October Attributable Pre-Sales

Press Release [For Immediate Release] KWG Property Holding Limited October Attributable Pre-sales Surged 28.9% y-o-y to RMB1,911 million ****** Achieved 80% of Full Year Target in First Ten Months with Attributable Pre-sales of RMB16.7 billion (11 November 2014 - Hong Kong) KWG Property Holding Limited (“KWG Property” or the “Group”, 1813.HK), one of the leading property developers in Guangzhou City, is pleased to announce its pre- sales result for October 2014. In October 2014, the Group’s gross pre-sales value amounted to RMB2,718 million. The Group’s attributable pre-sales value amounted to RMB1,911 million (as compared to RMB1,705 million in September 2014 and RMB1,482 million in October 2013), representing a month-on-month increase of 12.1% and a year-on-year increase of 28.9%, respectively. The Group’s attributable pre-sales area amounted to approximately 142,300 sq. m. (as compared to 118,000 sq. m. in September 2014 and 99,500 sq. m. in October 2013). For the first ten months, the Group has achieved a total of RMB16.7 billion of attributable pre-sales value, representing 80% of the Group’s full year pre-sales target of RMB21 billion and a year-on-year increase of 24.8%. - End - About KWG Property (HKSE stock code: 1813) Established in 1995, KWG Property is one of the leading property developers focusing on mid to high- end properties with premium quality in prime locations in Guangzhou. Going through 19 years of development, the Group has an efficient property development system, as well as a balanced product portfolio which includes mid- to high-end residential properties, serviced apartments, villas, office buildings, hotels and shopping malls. -

AGILE PROPERTY HOLDINGS LIMITED (Incorporated in the Cayman Islands with Limited Liability) Stock Code: 3383

雅居樂地產控股有限公司 AGILE PROPERTY HOLDINGS LIMITED (Incorporated in the Cayman Islands with limited liability) Stock code: 3383 Annual Report 2009 2009 Projects on Sale Corporate Profile The Group is one of leading property developers in China. It is principally engaged in the development of large-scale comprehensive property projects. The Group currently owns a diversified portfolio of 66 projects in various stages of development (including 5 developed and sold projects) in 22 different cities and districts such as Guangzhou, Zhongshan, Foshan, Heyuan, Huizhou, Shanghai, Changzhou, Nanjing, Chengdu, Xi’an, Chongqing, Shenyang and Hainan. As of 15 April 2010, the Group has a land bank with total GFA of approximately 32.15 million sq. m. (including both lands with titles and contractual interests). The shares of Agile have been listed on the Main Board of The Stock Exchange of Hong Kong Limited since 15 December 2005 under (Stock code: 3383). They are included as constituent stocks in Morgan Stanley Capital International China Index, the Hang Seng Composite Index and the Hang Seng Freefloat Composite Index. Contents 2 Financial Highlights 84 Senior Management’s Profi le 4 Business Structure 86 Corporate Governance Report 6 Milestone 2009 94 Report of the Directors 8 Honours and Awards 108 Independent Auditor’s Report 10 Chairman’s Statement 110 Consolidated Balance Sheet 18 Management Discussion and Analysis 112 Balance Sheet 26 Property Development 113 Consolidated Income Statement Land Bank of the Group 114 Consolidated Statement of Comprehensive -

Agile Property (3383 HK) Neutral (Maintained) Property - Real Estate Target Price: HKD6.30 Market Cap: USD3,051M Price: HKD6.04

Company Update, 5 June 2015 Agile Property (3383 HK) Neutral (Maintained) Property - Real Estate Target Price: HKD6.30 Market Cap: USD3,051m Price: HKD6.04 Macro Risks 2 Key Takeaways From Zhongshan Visit Growth . 2 0 Value . 01 0 . 02 0 We recently visited Agile’s four major projects in Zhongshan (tier-3 . Agile Property Holdings (3383 HK) 0 Price Close Relative to Hang Seng Index (RHS) city). Reiterate NEUTRAL with a higher HKD6.30 TP (4% upside), 0 7.4 110 following the sector valuation upgrade. Key takeaways: i) a preliminary 0 6.9 104 recovery in sales volume, driven by end-users and loosening mortgage approvals, and ii) ASP tends to stabilise, but upside is limited. We 6.4 98 remain concerned on Agile’s low-tier cities exposure (75% of its 5.9 91 landbank) and profit margin erosion. 5.4 85 Zhongshan the home base. Agile Property (Agile) was founded in 4.9 79 Zhongshan in 1992. It had been headquartered in the city since its establishment, until the headquarters was moved to Guangzhou in 2012. 4.4 73 Zhongshan is the highest contributing city, generating 13.7% and 18.4% 3.9 66 of landbank and contracted sales revenue, respectively, as of end-FY14. In turn, Agile is the market leader in Zhongshan, given that it achieved 3.4 60 250 the highest sales revenue among its peers in 2014. 200 150 Desirable sell-through, but likely an isolated case for Zhongshan. Benefitting from its brand reputation and track record in Zhongshan, 100 Agile’s projects are supported by end-user demand and loosening 50 mortgage approvals from banks. -

Accelerated Scale Expansion to Further Stretch Balance Sheet

September 20, 2016 COMMENT Sunac China Holdings (1918.HK) HK$5.87 Equity Research Accelerated scale expansion to further stretch balance sheet News On Sept 18, Sunac announced a potential transaction with Legend (3396.HK, Sept 19 close HK$20; Neutral; covered by Simon Cheung) to acquire 42 property projects in 16 cities with total unsold GFA of 7.3mn sqm for consideration of Rmb13.8bn, pending approval from shareholders of the companies. The consideration is comprised of Rmb3.6bn equity interest in companies that hold interests in the properties and assumption of Rm10.2bn of external debt, shareholders’ loan and accrued but unpaid interest. It will be paid in cash including Rmb5.5bn in 2016 and the rest in 2017 if the deal completes in early 2017 according to mgmt. Analysis As we highlighted in "Sunac China: Downgrade to Neutral on weak profitability and rising leverage" (Aug 31, 2016), we expect Sunac to continue its aggressive scale expansion at the expense of lower margins and higher leverage, and the proposed transaction comes at an even more accelerated pace than we anticipated. Based on the disclosed details, we note: 1) If completed, Sunac’s attributable landbank size will increase by 18% to GFA36.5mn sqm from 1H16 and geographic coverage will expand by 8 new cities to a total of 35 cities while the share of its attributable land bank in tier- 1/2/3 cities will change to 9%/67%/24% from 10%/75%/15% as of 1H16 (Ex. 1). 2) Stripping out one-off gains, the assets generated c.Rmb0.2bn net profit in 2015 (equivalent to 6% of Sunac's 2015 core profit) due to a deceleration in sales and margin slippage as per Simon Cheung. -

AGILE GROUP HOLDINGS LIMITED (Incorporated with Limited Liability Under the Laws of the Cayman Islands)

香 港 交 易 及 結 算 所 有 限 公 司 及 香 港 聯 合 交 易 所 有 限 公 司 對 本 公 告 的 內 容 概 不 負 責 , 對 其 準 確 性 或 完 整 性 亦 不 發 表 任 何 聲 明 , 並 明 確 表 示 概 不 就 因 本 公 告 全 部 或 任 何 部 分 內 容 而 產 生 或 因 倚 賴 該 等 內 容 而 引 致 的 任 何 損 失 承 擔 任 何 責 任 。 本 公 告 僅 供 參 考 , 並 不 構 成 收 購 、 購 買 或 認 購 證 券 的 邀 請 或 遊 說 要 約 , 或 邀 請 訂 立 協 議 進 行 上 述 任 何 事 宜 , 亦 無 意 招 攬 任 何 要 約 以 收 購 、 購 買 或 認 購 任 何 證 券 。 本 公 告 並 非 供 於 美 國 或 美 國 境 內 直 接 或 間 接 派 發 。 本 公 告 及 其 所 載 資 料 並 不 構 成 或 組 成 在 美 國 購 買 、 認 購 或 出 售 證 券 的 部 分 要 約 。 除 非 根 據 1933 年 美 國 證 券 法 ( 經 修 訂 ()「 證 券 法 」)登 記 或 獲 適 用 豁 免 登 記 規 定 , 否 則 證 券 不 得 在 美 國 提 呈 發 售 或 出 售 。 在 美 國 公 開 發 售 任 何 證 券 將 通 過 載 有 與 本 公 司 及 管 理 層 有 關 的 詳 細 資 料 以 及 財 務 報 表 的 招 股 章 程 的 方 式 進 行 。 本 公 告 所 述 證 券 並 無 及 將 不 會 根 據 證 券 法 登 記 , 且 不 會 在 美 國 公 開 發 售 任 何 證 券 。 本 公 告 所 述 證 券 將 根 據 所 有 適 用 法 律 法 規 出 售 。 本 公 告 或 其 所 載 資 料 並 非 用 以 招 攬 金 錢 、 證 券 或 其 他 代 價 , 而 倘 為 回 應 本 公 告 或 其 所 載 資 料 而 寄 出 金 錢 、 證 券 或 其 他 代 價 , 則 不 會 獲 接 納 。 本 公 告 並 非 歐 洲 經 濟 區(「 歐 洲 經 濟 區 」)成 員 國 所 實 施 歐 盟 指 令 2003 / 71 / EC( 及 其 任 何 修 訂 )所 界 定 之 招 股 章 程 。 無 PRIIPs 重 要 資 訊 文 件 - 由 於 不 可 於 歐 洲 經 濟 區 進 行 零 售 , 故 並 無 編 製 PRIIPs 重 要 資 訊 文 件 。 本 公 告 及 有 關 據 此 提 呈 發 行 證 券 之 任 何 其 他 文 件 或 資 料 並 非 由 英 國《 2000 年 金 融 服 務 與 市 場 法 》( 經 修 訂 )第 21 條 所 界 定 之 認 可 人 士 發 佈 , 而 有 關 文 件 及 ╱ 或 資 料 亦 未 經 其 批 准 。 因 此 , 有 關 文 件 及 ╱ 或 資 料 並 不 會 向 英 國 公 眾 人 士 派 發 , 亦 不 得 向 英 國 公 眾 人 士 傳 遞 。 有 關 文 件 及 ╱ 或 資 料 僅 作 為 財 務 推 廣 向 在 英 國 擁 有 相 關 專 業 投 資 經 驗 及 屬 於《 2000 年 金 融 服 務 與 市 場 法 》2005 年( 財 務 推 廣 )命 令( 經 修 訂 ) (「 財 務 推 廣 命 令 」)第 19 (5) 條 所 界 定 之 投 資 專 業 人 士 , 或 屬 於 財 務 推 廣 命 令 第 49 (2) (a) 至 (d) 條 範 圍 之 人 士 , 或 根 據 財 務 推 廣 命 令 可 以 其 他 方 式 -

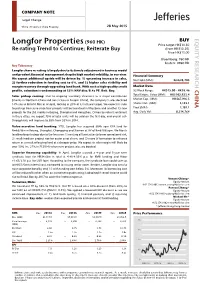

Longfor Properties(960

COMPANY NOTE Target Change China | Property | China Property 28 May 2015 EQUITY RESEARCH (960 HK) BUY Longfor Properties Price target HK$14.50 Re-rating Trend to Continue; Reiterate Buy (from HK$12.30) Price HK$13.00 Bloomberg: 960 HK Reuters: 0960.HK Key Takeaway Longfor share re-rating is largely due to its timely adjustment in business model and prudent financial management despite high market volatility, in our view. Financial Summary We expect additional upside will be driven by: 1) upcoming increase in sales, Net Debt (MM): Rmb28,705 2) further reduction in funding cost to 6%, and 3) higher sales visibility and margin recovery through upgrading land bank. With such a high-quality credit Market Data profile, valuation is undemanding at 35% NAV disc/8.4x PE. Reit. Buy. 52 Week Range: HK$15.00 - HK$8.46 CHINA Total Entprs. Value (MM): HK$102,923.4 Sales pickup coming: Due to ongoing inventory clearance as a major contribution (mainly in Northern China and tier-3 cities in Eastern China), the company’s sales declined Market Cap. (MM): HK$67,016.3 14% yoy to Rmb10.8bn as of April, locking in 20% of its full-year target. We expect its sales Shares Out. (MM): 5,155.1 to pick up from June since four projects will be launched in May/June and another 13 new Float (MM): 1,181.1 projects for the 2H, mainly in Beijing, Shanghai and Hangzhou. Driven by robust sentiment Avg. Daily Vol.: 8,214,764 in these cities, we expect 75% of total units will be sold on the first day, and overall sell- through rate will improve to 58% from 52% in 2014. -

China Property Sector

China / Hong Kong Industry Focus China Property Sector Refer to important disclosures at the end of this report DBS Group Research . Equity 19 Apr 2021 Spotlight on future land supply • Solid sales growth momentum sustained with strong HSI: 28,970 potential to ink another year of record-high sales • Developers poised to meet their 2021 targets ANALYST Jason LAM +852 3668 4179 [email protected] • Future land supply and new starts as keys to watch for Danielle WANG CFA, +852 3668 4176 [email protected] • Sector top picks: Vanke, COLI, CIFI and Logan Ken HE CFA, +86 21 3896 8221 [email protected] Solid performance in 1Q21; strong potential for another year of Ben Wong [email protected] record-high residential sales. Residential sales in Mar rose 63% y-o-y (or 44% vs Mar-19) on the back of a 38% (or 19% vs Mar- Recommendation & valuation 19) increment in residential GFA sold and 19% (or 21% vs Mar- 19) rise in residential ASP, marking another solid month of FY22F physical market performance. We believe the market is well- Target Price Price Rec Mkt Cap PE poised to post another record-high sales value this year – as it HK$ HK$ US$bn x will likely attain 2020’s level even if the market records a 12.5% y- o-y decline for the remaining nine months. China Overseas Developers well on track to achieve their 2021 targets. Presales 20.15 25.70 BUY 28.4 4.0 (688 HK) growth of 30 listed developers we track on a weighted-average China Vanke 'H' 28.25 45.56 BUY 49.9 5.3 basis remained strong at 47% y-o-y (or +33% vs Mar 2019) in (2202 HK) Mar (Feb-21: 144%), as compared to their c.10% weighted Logan Property 12.50 16.44 BUY 8.9 3.5 average presales target for 2021.