2021 Virtual Market Update

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Parker Review

Ethnic Diversity Enriching Business Leadership An update report from The Parker Review Sir John Parker The Parker Review Committee 5 February 2020 Principal Sponsor Members of the Steering Committee Chair: Sir John Parker GBE, FREng Co-Chair: David Tyler Contents Members: Dr Doyin Atewologun Sanjay Bhandari Helen Mahy CBE Foreword by Sir John Parker 2 Sir Kenneth Olisa OBE Foreword by the Secretary of State 6 Trevor Phillips OBE Message from EY 8 Tom Shropshire Vision and Mission Statement 10 Yvonne Thompson CBE Professor Susan Vinnicombe CBE Current Profile of FTSE 350 Boards 14 Matthew Percival FRC/Cranfield Research on Ethnic Diversity Reporting 36 Arun Batra OBE Parker Review Recommendations 58 Bilal Raja Kirstie Wright Company Success Stories 62 Closing Word from Sir Jon Thompson 65 Observers Biographies 66 Sanu de Lima, Itiola Durojaiye, Katie Leinweber Appendix — The Directors’ Resource Toolkit 72 Department for Business, Energy & Industrial Strategy Thanks to our contributors during the year and to this report Oliver Cover Alex Diggins Neil Golborne Orla Pettigrew Sonam Patel Zaheer Ahmad MBE Rachel Sadka Simon Feeke Key advisors and contributors to this report: Simon Manterfield Dr Manjari Prashar Dr Fatima Tresh Latika Shah ® At the heart of our success lies the performance 2. Recognising the changes and growing talent of our many great companies, many of them listed pool of ethnically diverse candidates in our in the FTSE 100 and FTSE 250. There is no doubt home and overseas markets which will influence that one reason we have been able to punch recruitment patterns for years to come above our weight as a medium-sized country is the talent and inventiveness of our business leaders Whilst we have made great strides in bringing and our skilled people. -

Annex 1: Parker Review Survey Results As at 2 November 2020

Annex 1: Parker Review survey results as at 2 November 2020 The data included in this table is a representation of the survey results as at 2 November 2020, which were self-declared by the FTSE 100 companies. As at March 2021, a further seven FTSE 100 companies have appointed directors from a minority ethnic group, effective in the early months of this year. These companies have been identified through an * in the table below. 3 3 4 4 2 2 Company Company 1 1 (source: BoardEx) Met Not Met Did Not Submit Data Respond Not Did Met Not Met Did Not Submit Data Respond Not Did 1 Admiral Group PLC a 27 Hargreaves Lansdown PLC a 2 Anglo American PLC a 28 Hikma Pharmaceuticals PLC a 3 Antofagasta PLC a 29 HSBC Holdings PLC a InterContinental Hotels 30 a 4 AstraZeneca PLC a Group PLC 5 Avast PLC a 31 Intermediate Capital Group PLC a 6 Aveva PLC a 32 Intertek Group PLC a 7 B&M European Value Retail S.A. a 33 J Sainsbury PLC a 8 Barclays PLC a 34 Johnson Matthey PLC a 9 Barratt Developments PLC a 35 Kingfisher PLC a 10 Berkeley Group Holdings PLC a 36 Legal & General Group PLC a 11 BHP Group PLC a 37 Lloyds Banking Group PLC a 12 BP PLC a 38 Melrose Industries PLC a 13 British American Tobacco PLC a 39 Mondi PLC a 14 British Land Company PLC a 40 National Grid PLC a 15 BT Group PLC a 41 NatWest Group PLC a 16 Bunzl PLC a 42 Ocado Group PLC a 17 Burberry Group PLC a 43 Pearson PLC a 18 Coca-Cola HBC AG a 44 Pennon Group PLC a 19 Compass Group PLC a 45 Phoenix Group Holdings PLC a 20 Diageo PLC a 46 Polymetal International PLC a 21 Experian PLC a 47 -

Constituents & Weights

2 FTSE Russell Publications 19 August 2021 FTSE 100 Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) 3i Group 0.59 UNITED GlaxoSmithKline 3.7 UNITED RELX 1.88 UNITED KINGDOM KINGDOM KINGDOM Admiral Group 0.35 UNITED Glencore 1.97 UNITED Rentokil Initial 0.49 UNITED KINGDOM KINGDOM KINGDOM Anglo American 1.86 UNITED Halma 0.54 UNITED Rightmove 0.29 UNITED KINGDOM KINGDOM KINGDOM Antofagasta 0.26 UNITED Hargreaves Lansdown 0.32 UNITED Rio Tinto 3.41 UNITED KINGDOM KINGDOM KINGDOM Ashtead Group 1.26 UNITED Hikma Pharmaceuticals 0.22 UNITED Rolls-Royce Holdings 0.39 UNITED KINGDOM KINGDOM KINGDOM Associated British Foods 0.41 UNITED HSBC Hldgs 4.5 UNITED Royal Dutch Shell A 3.13 UNITED KINGDOM KINGDOM KINGDOM AstraZeneca 6.02 UNITED Imperial Brands 0.77 UNITED Royal Dutch Shell B 2.74 UNITED KINGDOM KINGDOM KINGDOM Auto Trader Group 0.32 UNITED Informa 0.4 UNITED Royal Mail 0.28 UNITED KINGDOM KINGDOM KINGDOM Avast 0.14 UNITED InterContinental Hotels Group 0.46 UNITED Sage Group 0.39 UNITED KINGDOM KINGDOM KINGDOM Aveva Group 0.23 UNITED Intermediate Capital Group 0.31 UNITED Sainsbury (J) 0.24 UNITED KINGDOM KINGDOM KINGDOM Aviva 0.84 UNITED International Consolidated Airlines 0.34 UNITED Schroders 0.21 UNITED KINGDOM Group KINGDOM KINGDOM B&M European Value Retail 0.27 UNITED Intertek Group 0.47 UNITED Scottish Mortgage Inv Tst 1 UNITED KINGDOM KINGDOM KINGDOM BAE Systems 0.89 UNITED ITV 0.25 UNITED Segro 0.69 UNITED KINGDOM -

DATABANK INSIDE the CITY SABAH MEDDINGS the WEEK in the MARKETS the ECONOMY Consumer Prices Index Current Rate Prev

10 The Sunday Times February 10, 2019 BUSINESS Liam Kelly LETTERS 56-year-old chairman of before Serco and others got Send your letters, including executive had the audacity to arrangements a business has. Mrs M&S awaits her love sausage housebuilder Taylor Wimpey into a pickle for overcharging SIGNALS full name and address, describe me as a “dangerous For those already using a has been keen to link his the government to tag AND NOISE . to: The Sunday Times, threat” to the company. supported package, there is Much derision for Marks & Prufrock wonders name to several recruitment criminals, ushering in a 1 London Bridge Street, Calantzopoulos has likely to be no additional cost. Spencer after the high street whether Rowe, 51, plans to processes, including the dark period for outsourcers. London SE1 9GF. Or email: spearheaded PMI’s drive for For those using spreadsheets, stalwart unveiled a heart- treat the Mrs M&S in his life — chairmanships of John Lewis Beeston knows how tricky [email protected] safer products. That doesn’t bridging products are shaped “love sausage” as a his wife, Jo, an ardent Marks Partnership and the suit hire recruitment can be: he’s on Letters may be edited make him a hypocrite, but a available at about £20 a year. treat for a romantic breakfast shopper — to a love sausage chain Moss Bros. the nominations committee realist. André is an engineer: Our MTD service is live to on Valentine’s Day. on Thursday. He has been at Taylor of the Premier League, careful, methodical, logical. -

Act Annual Conference

EVENT OVERVIEW ACT ANNUAL CONFERENCE 21-22 May 2019 Manchester Central, UK ATTENDEE PROFILE TOTAL 9/10 DELEGATES ATTENDEES WOULD RECOMMEND 1075 THE EVENT TO A FRIEND/COLLEAGUE FROM OR ATTEND AGAIN 388COMPANIES 88 DELEGATES SPONSORS AND REPRESENTING 323 EXHIBITORS COMPANIES 97SPEAKERS 548 INCLUDING: • Anglo American • London Stock Exchange • Arup • Mitsubishi • ASOS • National Express • AstraZeneca • National Oilwell Varco SENIORITY OF • BAE Systems • Pearson • Balfour Beatty • Petrofac Services CORPORATE AUDIENCE • BASF • Primark • BT • PZ Cussons • Burberry • RELX • Centrica • Renewi • Compass Group • Rentokil • Deliveroo • Royal Dutch Shell • Drax • Sainsbury’s • Dyson • Schneider Electric • easyJet • Scottish Power • Electrocomponents • Serco • Equiniti • Sky • Etihad Airways • Stagecoach • Farfetch • Statoil • Google UK • Tate & Lyle • GSK • Tesco • Halfords • Thames Water • Hammerson • Thomas Cook • Heathrow Airport • Travelport • Hitachi Capital • UK Power Networks • InterContinental Hotels • Urenco • ITV • Virgin Media • JD Sports Fashion • Vodafone • John Lewis • WorldPay BOARD LEVEL/STRATEGIC LEADER 52% • Just Eat • Yildirim Holdings MANAGERIAL 30% OF COMPANIES CORPORATE SENIOR OPERATIONAL 17% THAT ATTENDED DELEGATES WITH JOB AS DELEGATES TITLES INCLUDING: TACTICAL 1% WERE GROUP TREASURER, HEAD 50% CORPORATE. 107 OF TREASURY, HEAD OF CORPORATE FINANCE EVENT OVERVIEW CONTENT AND FEEDBACK TOTAL NETWORKING TOTAL CONTENT AVAILABLE 10.3 29.4 HOURS HOURS LIBOR DIGITAL TREASURY TOP TOPICS SUSTAINABLE FINANCE PAYMENT INNOVATION AND RISKS OPEN BANKING GLOBAL AND DOMESTIC FINANCING MACROECONOMIC ENVIRONMENT EVENT APP SOCIAL MEDIA UNIQUE USERS: 435 726 TWEETS TOTAL APP GENERATED USING PAGE VIEWS: 74,666 #ACTAC19 DELEGATE FEEDBACK “THE ACT ANNUAL CONFERENCE PROVIDES AN EXCELLENT “IF YOU ONLY ATTEND ONE EVENT IN A YEAR, MAKE IT THE OPPORTUNITY TO NETWORK WITH OTHER TREASURY ACT ANNUAL CONFERENCE. -

Board of Directors

Board of Directors 1. John McFarlane OBE 2. Tim O’Toole CBE 3. Chris Surch Chairman Chief Executive Group Finance Director Appointed to the Board: 2013 Appointed to the Board: 2009 Appointed to the Board: 2012 Skills and experience: He was appointed to the Skills and experience: He was appointed to Skills and experience: He has a strong track Board in December 2013 and became Chairman the Board in 2009 and became Chief Executive record of financial leadership as well as extensive in January 2014. John has a proven track record in 2010. Tim brings to the Board a wealth of operational, strategic and international experience. of implementing cultural transformation and driving international transport management experience Chris was previously Group Finance Director of through strategic change. He was formerly CEO gained over a number of years in the sector. Prior Shanks Group plc, also for a period of time serving of Australia and New Zealand Banking Group Ltd, to joining the Company, he was Managing Director, as their acting Chief Executive. Following an early Group Executive Director of Standard Chartered plc London Underground, having previously been at career with Price Waterhouse, he joined TI Group and Chairman of Aviva plc. He will step down as Transport for London, and prior to which he was plc in 1995. He held a number of senior roles there Chairman at the conclusion of the forthcoming President and Chief Executive of Consolidated and following the merger of TI Group plc with Annual General Meeting. Rail Corporation. Smiths Group plc he went on to hold further senior Other appointments: Chairman of Barclays plc Other appointments: He is a Non-Executive finance roles, latterly serving as Finance Director of and Barclays Bank plc, and a Non-Executive Director of CSX Corporation, a rail freight their Speciality Engineering division. -

Diversified International Fund As of April 30, 2018

Diversified International Fund As of April 30, 2018 SCHEDULE OF INVESTMENTS MARKET % TOTAL NET ISSUER SHARES VALUE ASSETS Australia CSL Ltd 814,527 $ 104,331,664 0.83% Macquarie Group Ltd 1,257,437 $ 102,403,171 0.81% Mirvac Group 31,695,172 $ 53,190,044 0.42% Treasury Wine Estates Ltd 2,867,805 $ 40,963,586 0.32% Dexus 5,413,746 $ 38,500,008 0.30% Total Australia $ 339,388,473 2.69% Austria Erste Group Bank AG 1,747,280 $ 85,444,781 0.68% Raiffeisen Bank International AG 1,820,658 $ 61,458,171 0.49% Total Austria $ 146,902,952 1.16% Brazil Vale SA 11,208,800 $ 155,596,011 1.23% Itausa - Investimentos Itau SA 24,445,471 $ 94,552,447 0.75% Banco do Brasil SA 8,072,700 $ 84,616,792 0.67% Ambev SA 8,524,800 $ 56,747,641 0.45% Hypera SA 4,186,014 $ 37,809,402 0.30% MRV Engenharia e Participacoes SA 5,609,500 $ 23,922,679 0.19% Petrobras Distribuidora SA 3,559,400 $ 23,493,140 0.19% Itausa - Investimentos Itau SA 591,015 $ 2,277,547 0.02% Total Brazil $ 479,015,659 3.79% Canada Brookfield Asset Management Inc 3,415,802 $ 135,387,020 1.07% Toronto-Dominion Bank/The 2,134,900 $ 119,901,584 0.95% Canadian National Railway Co 1,551,948 $ 119,869,686 0.95% Suncor Energy Inc 2,765,500 $ 105,756,494 0.84% Dollarama Inc 839,416 $ 96,706,581 0.77% Alimentation Couche-Tard Inc 2,195,346 $ 94,913,086 0.75% TransCanada Corp 2,122,306 $ 89,986,634 0.71% Bank of Montreal 1,101,600 $ 84,459,289 0.67% Canadian Natural Resources Ltd 2,005,800 $ 72,361,584 0.57% Bank of Nova Scotia/The 1,122,400 $ 68,990,076 0.55% Open Text Corp 968,800 $ 34,203,594 0.27% Total -

Case No COMP/M.3554 - SERCO / NEDRAILWAYS / NORTHERN RAIL

EN Case No COMP/M.3554 - SERCO / NEDRAILWAYS / NORTHERN RAIL Only the English text is available and authentic. REGULATION (EEC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 16/09/2004 Also available in the CELEX database Document No 32004M3554 Office for Official Publications of the European Communities L-2985 Luxembourg COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 16.09.2004 In the published version of this decision, some information has been omitted pursuant to Article SG-Greffe(2004) D/204043/204044 17(2) of Council Regulation (EC) No 139/2004 concerning non-disclosure of business secrets and other confidential information. The omissions are shown thus […]. Where possible the information PUBLIC VERSION omitted has been replaced by ranges of figures or a general description. MERGER PROCEDURE ARTICLE 6(1)(b) DECISION To the notifying party Subject: Case No COMP/M.3554 - Serco/NedRailways/Northern Rail JV Notification of 13.8.2004 pursuant to Article 4 of Council Regulation No 139/20041 Dear Sir/Madam, 1. On 13.08.2004, Serco Group plc (“Serco”) and NedRailways BV (“NedRailways”) notified their intention to acquire joint control of the Northern passenger rail franchise (“Northern franchise”) within the meaning of Article 3(1)(b) of the EC Merger Regulation (“EC Merger Regulation”). 2. After examining the notification, the Commission has concluded that the notified operation falls within the scope of the Merger Regulation and that it does not raise any serious doubts as to its compatibility with the common market and with the EEA agreement. I. THE PARTIES 3. Serco is active in transport services including rail and metro in the UK, where it runs the Docklands Light Railway and the Metrolink in Manchester. -

FORWARD Annual Report and Accounts 2001 >EQUIPPED >Being Prepared Is Everything

Smiths Group plc Annual report and accounts 2001 >FORWARD Annual report and accounts 2001 >EQUIPPED >Being prepared is everything. At Smiths we focus on the future. What will our customers want tomorrow? How can we exploit technology to provide enhanced solutions for their most demanding applications? How can we extend our capabilities to give them the service they need? We are constantly searching for ways to add value for our customers. This is how we generate profitable organic growth. >DISCOVERY >Discovery is about being always one step ahead. It is about meeting needs in ways that others haven’t yet thought of. It is about developing products that provide innovative solutions for the toughest applications. Through total commitment to research and development, Smiths seeks sustainable competitive advantage. >TEAMWORK >At Smiths we believe in teamwork. We work closely with our suppliers and customers to build productive partnerships and long-term relationships. Within the company, too, teamwork is essential. Not just working together day by day, but focusing everyone's efforts on maximum efficiency, productivity, flexibility and responsiveness. Through teamwork we seek to be a leader. >REACH >In a world where efficiency is paramount, customers want to deal with fewer, better suppliers. At Smiths we have the necessary size and diversity. We are global. Our products are wide-ranging. We have the reach to be our customers’ preferred supplier. 01 03 01 As a first-tier supplier working directly 03 We are a leading supplier of products used with prime manufacturers, we are during critical and intensive care procedures, delivering systems for front-line defence and for continuing care during recovery. -

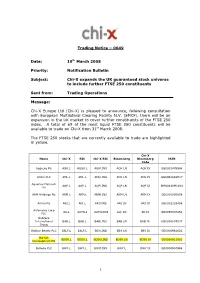

20080319 Trading Notice Functional 0049

Trading Notice – 0049 Date: 19 th March 2008 Priority: Notification Bulletin Subject: Chi-X expands the UK guaranteed stock universe to include further FTSE 250 constituents Sent from: Trading Operations Message: Chi-X Europe Ltd (Chi-X) is pleased to announce, following consultation with European Multilateral Clearing Facility N.V. (EMCF), there will be an expansion in the UK market to cover further constituents of the FTSE 250 index. A total of 69 of the most liquid FTSE 250 constituents will be available to trade on Chi-X from 31 st March 2008. The FTSE 250 stocks that are currently available to trade are highlighted in yellow. Chi-X Name Chi-X RIC Chi-X RIC Bloomberg Bloomberg ISIN Code Aggreko Plc AGK.L AGGK.L AGKl.INS AGK LN AGK IX GB0001478998 Amlin PLC AML.L AML.L AMLl.INS AML LN AML IX GB00B2988H17 Aquarius Platinum AQP.L AQP.L AQPl.INS AQP LN AQP IX BMG0440M1284 Ltd ARM Holdings Plc ARM.L ARM.L ARMl.INS ARM LN ARM IX GB0000595859 Arriva Plc ARI.L ARI.L ARIl.INS ARI LN ARI IX GB0002303468 Autonomy Corp AU.L AUTN.L AUTNl.INS AU/ LN AU IX GB0055007982 PLC Babcock International BAB.L BAB.L BABl.INS BAB LN BAB IX GB0009697037 Group Balfour Beatty PLC BALF.L BALF.L BBYl.INS BBY LN BBY IX GB0000961622 Barratt BDEV.L BDEV.L BDEVl.INS BDEV LN BDEV IX GB0000811801 Development Plc Bellway PLC BWY.L BWY.L BWYl.INS BWY.L BWY IX GB0000904986 1 Biffa PLC BIFF.L BIFF.L BIFFl.INS BIFF LN BIFF IX GB00B129PL77 Bradford & Bingley BB.L BB.L BBl.INS BB/ LN BB IX GB0002228152 PLC Bunzl PLC BNZL.L BNZL.L BNZLl.INS BNZL LN BNZL IX GB00B0744B38 Burberry -

Evenlode Investment View January 2020

Evenlode Investment View January 2020 In this month’s investment view, I’ll review 2019 for Evenlode Income and briefly discuss my thoughts on the outlook. I’ve also included a summary of the fourth quarter as an appendix for those interested. It’s been a relatively quiet start to 2020 so far, with Evenlode Income up +1.3% and the UK market +1.2%*. The full year results season is commencing with lots of company updates due over the next few weeks. I’ll discuss some key themes that we’re hearing from the corporate world in February’s investment view. From Pessimism to Optimism At the beginning of 2019, investor sentiment was quite negative with worries over rising interest rate rises, trade tariffs, the global economy and Brexit. This had caused a significant sell-off in most stock markets at the end of 2018 and was beginning to create a valuation environment that we felt was as interesting as it had been for three or four years. Since then sentiment has, quite sharply, swung towards optimism. Though the global economy did slow during the year, it’s just about muddled along, and perhaps most significantly for financial assets, monetary policy was eased. Towards the end of the year better news on US/China trade tariffs and more clarity on the UK’s political situation also helped. This meant 2019 ended up being a strong year for most global stock markets. A Long-Term Approach Evenlode Income returned 24.3% during the year compared to 19.2% for the FTSE All-Share. -

Delivering Responsible Infrastructure Solutions

John Laing Group plc John Laing Group DELIVERING Annual Report & Accounts RESPONSIBLE INFRASTRUCTURE SOLUTIONS 2019 John Laing Group plc Annual Report & Accounts 2019 WE ARE JOHN LAING DELIVERING INFRASTRUCTURE SOLUTIONS JOHN LAING IS DELIVERING INFRASTRUCTURE SOLUTIONS. WE ARE INVESTORS AND PARTNERS BEHIND RESPONSIBLE INFRASTRUCTURE PROJECTS WHICH RESPOND TO PUBLIC NEEDS, EMPOWER SUSTAINABLE GROWTH AND IMPROVE THE LIVES OF THE COMMUNITIES IN WHICH WE WORK. CLARENCE CORRECTIONAL CENTRE, THE INTERCITY EXPRESS PROGRAMME, ASIA PACIFIC EUROPE AND MIDDLE EAST p / 18 p / 24 I-75 ROAD, RUTA DEL CACAO, NORTH AMERICA LATIN AMERICA p / 32 p / 42 Our Alignment to the United Nations Sustainable Development Goals While our projects have overlaps across many of the UN SDGs, we have identified 5 priority SDGs which our investments most directly contribute to. For further information on this, please see page 64. 2019 HIGHLIGHTS CONTENTS FINANCIAL HIGHLIGHTS OVERVIEW 1 > NAV per share at 337p at 31 December 2019 2019 Highlights 2 At a Glance (31 December 2018 – 323p) 4 Our Global Reach Overview > 4.3% increase since 31 December 2018; 7.2% increase before 6 Chairman’s Statement dividends paid; STRATEGIC REPORT > 10.7% increase at constant currency and before dividends paid1 8 Chief Executive Officer’s Review > Final dividend 7.66p per share (including a special dividend 14 Our Strategy and Business Model of 3.98p per share), giving a total dividend for 2019 of 9.50p 16 Key Performance Indicators 20 Regional Review > Investment commitments of £184 million