The Efficiency of Auction Houses

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

FAMÍLIA DE SALTIMBANQUIS DE PICASSO Context Biogràfic, Artístic I Interpretatiu

FAMÍLIA DE SALTIMBANQUIS DE PICASSO Context biogràfic, artístic i interpretatiu Assumpció Cardona Iglésias TFG Tutora: Teresa M. Sala Història de l´Art. Universitat de Barcelona, 2018 INDEX INTRODUCCCIÓ: Objectius i metodologia .................................................................................... 4 Comentari de les fonts bibliogràfiques ......................................................................................... 6 I.CONTEXT BIOGRÀFIC I ARTÍSTIC . ETAPA ENTRE BARCELONA I PARÍS ................................... 13 1.1.Barcelona 1895-1904 ........................................................................................................ 13 1.2.Influència de Rusiñol ......................................................................................................... 14 1.3.Viatges a París ................................................................................................................... 16 1.4.París 1904-1905................................................................................................................. 17 II. FAMÍLIA DE SALTIMBANQUIS .................................................................................................. 19 2.1. Etapa rosa ......................................................................................................................... 19 2.1.1. Del blau al rosa .......................................................................................................... 19 2.1.2.Començament etapa rosa ......................................................................................... -

In Southeast Asia

A Publication of the SEAMEO Regional Centre for Archaeology and Fine Arts Volume 17 Number 1 January - April 2007 • ISSN 0858-1975 IN SOUTHEAST ASIA SEAMEO-SPAFA Regional Centre for Archaeology and Fine Arts SPAFA Journal is published three times a year by the SEAMEO-SPAFA Regional Centre for Archaeology and Fine Arts. It is a forum for scholars, researchers, professionals and those interested in archaeology, performing arts, visual arts and cultural activities in Southeast Asia to share views, ideas and experiences. The opinions expressed in this journal are those of the contributors and do not necessarily reflect the views of SPAFA. SPAFA's objectives : • Promote awareness and appreciation of the cultural heritage of Southeast Asian countries; • Help enrich cultural activities in the region; • Strengthen professional competence in the fields of archaeology and fine arts through sharing of resources and experiences on a regional basis; • Increase understanding among the countries of Southeast Asia through collaboration in archaeological and fine arts programmes. The SEAMEO Regional Centre for Archaeology Editorial and Fine Arts (SPAFA) promotes professional Pisit Charoenwongsa competence, awareness and preservation of cultural heritage in the fields of archaeology and Assistants fine arts in Southeast Asia. It is a regional centre Malcolm Bradford constituted in 1985 from the SEAMEO Project in Nawarat Saengwat Archaeology and Fine Arts, which provided the Pattanapong Varanyanon acronym SPAFA. The Centre is under the aegis of Tang Fu Kuen -

L'art Contemporain Ou Le Fétichisme Du Lucre

L’art contemporain ou le fétichisme du lucre Marine Crubilé To cite this version: Marine Crubilé. L’art contemporain ou le fétichisme du lucre. Art et histoire de l’art. Université Michel de Montaigne - Bordeaux III, 2018. Français. NNT : 2018BOR30009. tel-01827296 HAL Id: tel-01827296 https://tel.archives-ouvertes.fr/tel-01827296 Submitted on 2 Jul 2018 HAL is a multi-disciplinary open access L’archive ouverte pluridisciplinaire HAL, est archive for the deposit and dissemination of sci- destinée au dépôt et à la diffusion de documents entific research documents, whether they are pub- scientifiques de niveau recherche, publiés ou non, lished or not. The documents may come from émanant des établissements d’enseignement et de teaching and research institutions in France or recherche français ou étrangers, des laboratoires abroad, or from public or private research centers. publics ou privés. Université Bordeaux Montaigne École Doctorale Montaigne Humanités (ED 480) THÈSE DE DOCTORAT EN « ARTS ET SCIENCE DE L’ART » MICA EA4426 L’art contemporain ou le fétichisme du lucre Présentée et soutenue publiquement le 1er juin 2018 par Marine CRUBILÉ Sous la direction de Bernard Lafargue Membres du jury M. Alain CHAREYRE-MÉJAN, Professeur des Universités, Esthétique, Université Aix- Marseille. (Rapporteur) M. Jacinto LAGEIRA, Professeur des Universités, Esthétique, Université Paris 1 Panthéon- Sorbonne. (Rapporteur) Mme. Mylène DUC, Professeure d’Esthétique, Expert, Université Montpellier 3. M. Pierre CABROL, Professeur de Droit, Expert, IUT Bordeaux Montaigne. Image de couverture : Vincent Gicquel, Attraction, huile sur toile, 190 x 140 cm, 2017. REMERCIEMENTS Je souhaite exprimer toute ma gratitude à mon Directeur de thèse Bernard Lafargue, qui a fait preuve à mon égard d’un soutien indéfectible et sans qui cette thèse n’aurait jamais vu le jour. -

Jeudi 24 Octobre 2013 À 13H30 Estampes Anciennes, Archives, Manuscrits, Livres Anciens Et Modernes

Jeudi 24 octobre 2013 à 13h30 Estampes anciennes, archives, manuscrits, livres anciens et modernes Ghislaine KAPANDJI et Élie MORHANGE, Commissaires-Priseurs. Agrément 2004-508 – RCS Paris B 477 936 447. 46 bis, passage Jouffroy – 75 009 Paris. [email protected] site www.kapandji-morhange.com. Tél : 01 48 24 26 10 • Fax : 01 48 24 26 11 VENTE AUX ENCHÈRES PUBLIQUES HÔTEL DROUOT – SALLE 12 9, RUE DROUOT – 75009 PARIS JEUDI 24 OCTOBRE 2013 À 13H30 ESTampes DE piranÈSE archiVES, MANUSCRITS LIVRES ANCIENS & MODERNES Experts Galerie TERRADES Antoine CAHEN 8, rue d’Alger- 75001 Paris Tél. : +33 (0)1 40 20 90 51 [email protected] Présente les lots 1 à 32 Christian GALANTARIS 11, rue Jean Bologne – 75116 Paris Tél. : +33 (0)1 47 03 49 65 Email : [email protected] Présente les lots 36 à 50 Yves SALMON Le Roy de Toullan 2, allée des Aulnes Exposition publique sur table : 56760 PENESTIN Drouot Richelieu, salle 12 Tél. : +33 (0)6 10 89 18 64 Mercredi 23 Octobre, de 11h00 à 18h00 Email : [email protected] Jeudi 24 octobre de 11h00 à 12h00 Présente les lots 51 à 414 Téléphone pendant l’exposition et la vente : 01 48 00 20 12 Le catalogue est disponible en ligne sur www.kapandji-morhange.com et www.drouotlive.com 444 Reproduit en 1e de couverture : Lot 465 Reproduit en 2e de couverture : Lot 371 bis Reproduit en 3e de couverture : Lot 5 Reproduit en 4e de couverture : Lot 282 Sommaire ESTAMPES DE PIRANÈSE Vente à 13h30 lots 1 à 35 ARCHIVES & AUTOGRAPHES Lionne, Turenne, Marie-Thérèse d’Autriche, Latour-Maubourg lots 36 à -

Dossier De Premsa

DOSSIER DE PREMSA ÍNDEX 1. ‘Palau Mira Picasso’, per Víctor Fernández 2. Seccions de l’exposició 3. Selecció d’obres 4. Josep Palau i Fabre sobre Picasso 5. La Fundació 6. Més informació 7. Premsa ‘PALAU MIRA PICASSO’ Josep Palau i Fabre (1917-2008) és una de les figures més singulars de la literatura catalana del segle passat. A més de poeta, dramaturg, traductor i assagista, Palau és conegut com una de les principals autoritats en els estudis picassians, amb una extensa bibliografia que encara avui segueix sent considerada com a fonamental per conèixer el geni malagueny. A diferència d’altres investigadors, l’escriptor català va comptar amb el suport del mateix Pablo Picasso que el va ajudar proporcionant-li nombroses dades i documentació sobre la seva vida i la seva obra. L’exposició celebra l’amistat entre l’escriptor català i l’artista malagueny. Palau va ser un dels autors que millor va saber observar la vida i l’obra de Pablo Picasso. És justament la capacitat de mirar de Palau, investigador picassià i fidel amic del pintor, el que es vol mostrar. Per això es basa en el mateix arxiu del poeta, amb una selecció de les fotografies que va prendre durant el seu seguiment picassià. Són imatges, majoritàriament inèdites, en què retrata Picasso, però també aquells llocs i persones relacionats amb la biografia de l’artista. Tot això, alhora, també serveix per donar a conèixer una faceta desconeguda de Palau: la de fotògraf. Amb la seva càmera va retratar tant el pintor com els principals decorats que conformen la cartografia de l’autor de Les senyoretes d’Avinyó, a més d’obres i personatges, una fascinació que Palau va mantenir viva fins al final de la seva vida. -

Picasso Versus Rusiñol

Picasso versus Rusiñol The essential asset of the Museu Picasso in Barcelona is its collection, most of which was donated to the people of Barcelona by the artist himself and those closest to him. This is the museum’s reason for existing and the legacy that we must promote and make accessible to the public. The exhibition Picasso versus Rusiñol is a further excellent example of the museum’s established way of working to reveal new sources and references in Picasso’s oeuvre. At the same time, the exhibition offers a special added value in the profound and rigorous research that this project means for the Barcelona collection. The exhibition sheds a wholly new light on the relationship between Picasso and Rusiñol, through, among other resources, a wealth of small drawings from the museum’s collection that provide fundamental insight into the visual and iconographic dialogues between the work of the two artists. The creation of new perspectives on the collection is one of the keys to sustaining the Museu Picasso in Barcelona as a living institution that continues to arouse the interest of its visitors. Jordi Hereu Mayor of Barcelona 330 The project Picasso versus Rusiñol takes a fresh look at the relationship between these two artists. This is the exhibition’s principal merit: a new approach, with a broad range of input, to a theme that has been the subject of much study and about which so much has already been written. Based on rigorous research over a period of more than two years, this exhibition reviews in depth Picasso’s relationship — first admiring and later surpassing him — with the leading figure in Barcelona’s art scene in the early twentieth century, namely Santiago Rusiñol. -

Movimientos Artísticos Contemporáneos Siglo Xx

MOVIMIENTOS ARTÍSTICOS CONTEMPORÁNEOS SIGLO XX Magdalena Adrover Gayá 1º Comunicación Audiovisual Curso 2008-2009 ÍNDICE 1. Introducción Página 2 2. Arquitectura Página 3 Escuela de Chicago Página 3 Modernismo Página 6 Expresionista y futurista Página 12 Racionalismo y funcionalismo Página 17 Orgánica Página 18 3. Cubismo Página 21 Pintura Página 21 Escultura Página 29 4. Fauvismo Página 32 5. Expresionismo Alemán Página 35 6. Dadaismo Página 49 7. Surrealismo Página 54 8. Abstracción Página 61 1 INTRODUCCIÓN La ruptura con los módulos y formas tradicionales es una de las características del arte contemporáneo. Los avances científicos han ofrecido al hombre unas enormes posibilidades para el desarrollo de su personalidad. El artista ha accedido a su completa libertad. El mundo actual produce un gran desasosiego, de ahí que el arte exprese la paradoja de nuestra vida: de un lado, un mundo tecnificado que busca lo más barato y sencillo, y por otro, la insatisfacción del espíritu. La escultura se ha convertido en un objeto que se mueve, e igualmente la pintura y la misma escultura confunden sus límites. El arte es un reflejo de las circunstancias que se producen en este siglo: cambios, transformaciones constantes,... La obra de arte cambia su concepto: − No necesita imitar la naturaleza ni representar objetos ni acontecimientos. − Invención de objetos y conceptos, por los que el artista se expresa. − La obra nace de la mente del artista (no quiere representar lo que ve, sino que lo interpreta). El arte es subjetivo. Dice Hamilton: “(...) porque la obra de arte se origina en la mente de un autor, tiene que ser comprendida por el espectador”. -

Vllg.Com INCUBATOR Agile

INCUBATOR Agile vllg.com Agile INCUBATOR Agile ABOUT vllg.com Agile is based Edgar Walthert’s postgraduate exam-project with the same name from TypeMedia in The Hague. The text-pattern and display settings contain a liveliness that was derived from an organic work process while the type family was in development. INCUBATOR Agile ABOUT vllg.com In a time when new text faces are published almost every day, Edgar noticed a gap between clean, rather technical faces, and those typefaces with pronounced influences from handwriting. What he found lacking was a design that united the advantages of these two approaches — a typeface that was natural, yet clear. INCUBATOR Agile ABOUT vllg.com Starting with experimental, unusual letterforms, the design gradually evolved, in a process of fine-tuning and adapting the characters to each other until they formed a harmonious whole. INCUBATOR Agile ABOUT vllg.com COMPARED TO MANY OTHER DIGITALLY PRODUCED FONTS, AGILE HAS A LARGE NUMBER OF UNIQUE SHAPES — SIMILAR SEGMENTS THAT NEVERTHELESS ARE NOT SIMPLY CLONES OF EACH OTHER, BUT HAVE BEEN ADAPTED TO THE INDIVIDUAL LETTERS. THIS APPROACH LENDS AGILE ITS LIVELY AND ORGANIC NATURE. INCUBATOR Agile ABOUT vllg.com STYLES Agile is available in 10 weights, from the extremely thin Hairline to the mighty Fat. The 10 upright styles are accompanied by 10 true italics — 20 fonts in all, each including small caps, extensive language support, several sets of numerals, a fine choice of ligatures, many alternate letters and more. Hairline Hairline Italic Thin Thin Italic Extralight Extralight Italic Light Light Italic Book Book Italic Medium Medium Italic Bold Bold Italic Extrabold Extrabold Italic Black Black Italic Fat Fat Italic INCUBATOR Agile ABOUT vllg.com INCUBATOR SUPPORTED LANGUAGES Edgar Walthert / 2011 Agile offers extensive language support Edgar Walthert is a type and graphic designer based in Amsterdam. -

Art Moderne Et Contemporain Art Primitif Curiosités

ART MODERNE ET CONTEMPORAIN ART PRIMITIF CURIOSITÉS Photographies d’artistes HÔTEL DROUOT salle 10 Mercredi 9 juin 2010 INDEX A F O AESCHBASCHER Arthur 181 à 185 FAUBERT Jean 252 OLOVSON Gudmar 292 AGAM Yaacov 186, 187 FICHET Pierre 253 OPPENHEIM Dennis 51 ALMASY Paul 143, 149, 153, 156, 157 FILLON Arthur 254 P ANDREEV Igor 188 FINI Léonor 138 PAPART Max 125 à 127, 293 ARDEN QUIN Carmelo 189, 190 FLOCON Albert 255 PASCIN Jules 294, 295 ARMAN 52, 191, 192 FOUJITA Léonard 110 ARNAL François 193 PEIRE Luc 296 G PENKOAT Pierre 297 à 300 ARTHUR BERTRAND Huguette 194 GALASSI René 256, 257 ARTOF 195 PICART LE DOUX Charles 301, 302 GAUTHUS Alain 258 PICASSO Pablo 128, 129 GHIGLION-GREEN Maurice 67 B PICHETTE James 303 à 305, BATTUT Michèle 196 GIACOMETTI Alberto 111 POIROT MATSUDA 306,307 BAZAINE Jean 96 GILIOLI Emilio 259 POMAR Julio 308 BEAUDIN André 197, 198 GILLET Roger Edgar 260 POUGNY Jean 130 BEÖTHY Étienne 199 à 202 GOETZ Henri 112 à 116, 261 PRINNER Anton 309 BERTHOLLE Jean 203 à 206 GORDE Jacques 262, 263 BOISROND François 207 GUITET James 264 R BOKOR Miklos 208, 209 GUTH Hella 265 RAGE Patrick 310 BOLIN Gustav 210, 285 H RANCILLAC Bernard 311 à 315 BORSI Manfredo 211 HAINS Raymond 53 RECALCATI 89 BOSSER Jacques 97 HALPERN Renée 266 REIMPRÉ Thibaut de 316, 317 BOUMEESTER Christine 212, 213 HARTLEY Henry 267 REYMOND Carlos 318 BOUQUETON Marcel 214 HARTUNG Hans 117 ROCHER Maurice 319 BOUSSARD Jacques 215 HENRY Pierre 90 RODIN Auguste 320 BRAUNER Victor 98 HILAIRE Camille 268 ROMATHIER Georges 321, 322 BRUNET Guy 216 HUMBLOT Robert 64 ROUSSEAU -

La Influència De L'art Català Sobre Picasso a Través De Dues

La influència de l’art català sobre Picasso a través de dues generacions: Santiago Rusiñol i Isidre Nonell com a paradigmes (1897-1904) Eduard Vallès Pallarès ADVERTIMENT. La consulta d’aquesta tesi queda condicionada a l’acceptació de les següents condicions d'ús: La difusió d’aquesta tesi per mitjà del servei TDX (www.tdx.cat) i a través del Dipòsit Digital de la UB (diposit.ub.edu) ha estat autoritzada pels titulars dels drets de propietat intel·lectual únicament per a usos privats emmarcats en activitats d’investigació i docència. No s’autoritza la seva reproducció amb finalitats de lucre ni la seva difusió i posada a disposició des d’un lloc aliè al servei TDX ni al Dipòsit Digital de la UB. No s’autoritza la presentació del seu contingut en una finestra o marc aliè a TDX o al Dipòsit Digital de la UB (framing). Aquesta reserva de drets afecta tant al resum de presentació de la tesi com als seus continguts. En la utilització o cita de parts de la tesi és obligat indicar el nom de la persona autora. ADVERTENCIA. La consulta de esta tesis queda condicionada a la aceptación de las siguientes condiciones de uso: La difusión de esta tesis por medio del servicio TDR (www.tdx.cat) y a través del Repositorio Digital de la UB (diposit.ub.edu) ha sido autorizada por los titulares de los derechos de propiedad intelectual únicamente para usos privados enmarcados en actividades de investigación y docencia. No se autoriza su reproducción con finalidades de lucro ni su difusión y puesta a disposición desde un sitio ajeno al servicio TDR o al Repositorio Digital de la UB. -

Federal Register / Vol. 61, No. 170 / Friday, August 30, 1996 / Notices

46134 Federal Register / Vol. 61, No. 170 / Friday, August 30, 1996 / Notices LIBRARY OF CONGRESS work must be an original work of must first file or serve a Notice of Intent authorship that: to Enforce (NIE) on such parties. Copyright Office (1) is not in the public domain in its A copyright owner may file an NIE in [Docket No. 96±4] source country through expiration of the Copyright Office within two years of term of protection; the date of restoration of copyright. Copyright Restoration of Works in (2) is in the public domain in the Alternatively, an owner may serve an Accordance With the Uruguay Round United States due to: NIE on an individual reliance party at Agreements Act; List Identifying (i) noncompliance with formalities any time during the term of copyright; Copyrights Restored Under the imposed at any time by United States however, such notices are effective only Uruguay Round Agreements Act for copyright law, including failure to against the party served and those who Which Notices of Intent To Enforce renew, publishing the work without a have actual knowledge of the notice and Restored Copyrights Were Filed in the proper notice, or failure to comply with its contents. NIEs appropriately filed Copyright Office any manufacturing requirements; with the Copyright Office and published (ii) lack of subject matter protection in herein serve as constructive notice to all AGENCY: Copyright Office, Library of the case of sound recordings fixed reliance parties. Congress. before February 15, 1972; or Pursuant to the URAA, the Office is ACTION: Publication of Second List of (iii) lack of national eligibility (e.g., publishing its second four month list Notices of Intent to Enforce Copyrights the work is from a country with which identifying restored works and the Restored Under the Uruguay Round the United States did not have copyright ownership for Notices of Intent to Enforce a restored copyright filed with Agreements Act. -

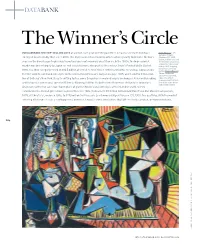

Databank the Winner’S Circle

DATABANK The Winner’s Circle IN EXAMINING THE TOP-SELLING LOTS at auction each year over the past three decades, several trends have Pablo Picasso’s Les femmes d’Alger emerged, most notably that, since 2006, the Impressionist and modern artists who regularly took home the lion’s (Version ‘O’), 1955, below, sold for a record share on the block began to give way to postwar and contemporary practitioners. In the 1980s, the Impressionist $179 million at auction, at Christie’s New York market was driven largely by Japanese real estate tycoons, who pushed Vincent van Gogh’s Portrait du Dr. Gachet, in May 2015, topping the previous record 1890, to a then category record of $82.5 million at Christie’s New York in 1990. In 2004 this record was surpassed by holder, Francis Bacon’s the first work to command nine digits on the block—Pablo Picasso’s Garçon à la pipe, 1905, which sold for $104.2 mil- Three Studies of Lucian Freud, 1969, lion at Sotheby’s New York. Despite shifting tastes, some things have remained largely unchanged. All record-breaking opposite, which commanded $142 mil- artists have been men and, save for Willem de Kooning, left this life by the time their most stellar sales took place. lion at the same house in November 2013. And nearly all the top sales have taken place at giants Christie’s and Sotheby’s, at their London and New York establishments. Overall, prices have skyrocketed since 1986, from a mere $11 million for Edouard Manet’s La Rue Mosnier aux paveurs, 1878, at Christie’s London in 1986, to $179 million for Picasso’s Les femmes d’Alger (Version ‘O’), 1955, this past May.