China Oceanwide Synergies in the Acquisition of Genworth

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Fidelity® Emerging Markets Index Fund

Quarterly Holdings Report for Fidelity® Emerging Markets Index Fund January 31, 2021 EMX-QTLY-0321 1.929351.109 Schedule of Investments January 31, 2021 (Unaudited) Showing Percentage of Net Assets Common Stocks – 92.5% Shares Value Shares Value Argentina – 0.0% Lojas Americanas SA rights 2/4/21 (b) 4,427 $ 3,722 Telecom Argentina SA Class B sponsored ADR (a) 48,935 $ 317,099 Lojas Renner SA 444,459 3,368,738 YPF SA Class D sponsored ADR (b) 99,119 361,784 Magazine Luiza SA 1,634,124 7,547,303 Multiplan Empreendimentos Imobiliarios SA 156,958 608,164 TOTAL ARGENTINA 678,883 Natura & Co. Holding SA 499,390 4,477,844 Notre Dame Intermedica Participacoes SA 289,718 5,003,902 Bailiwick of Jersey – 0.1% Petrobras Distribuidora SA 421,700 1,792,730 Polymetal International PLC 131,532 2,850,845 Petroleo Brasileiro SA ‑ Petrobras (ON) 2,103,697 10,508,104 Raia Drogasil SA 602,000 2,741,865 Bermuda – 0.7% Rumo SA (b) 724,700 2,688,783 Alibaba Health Information Technology Ltd. (b) 2,256,000 7,070,686 Sul America SA unit 165,877 1,209,956 Alibaba Pictures Group Ltd. (b) 6,760,000 854,455 Suzano Papel e Celulose SA (b) 418,317 4,744,045 Beijing Enterprises Water Group Ltd. 2,816,000 1,147,720 Telefonica Brasil SA 250,600 2,070,242 Brilliance China Automotive Holdings Ltd. 1,692,000 1,331,209 TIM SA 475,200 1,155,127 China Gas Holdings Ltd. 1,461,000 5,163,177 Totvs SA 274,600 1,425,346 China Resource Gas Group Ltd. -

Climate-Change Journalism in China: Opportunities for International

Climate-change journalism in China: opportunities for international cooperation By Sam Geall Foreword by Hu Shuli 中国气候变化报道: 国际合作中的机遇 山姆·吉尔 序——胡舒立 Climate-change journalism in China: opportunities for international cooperation 中国气候变化报道:国际合作中的机遇 © International Media Support 2011. Any reproduction, modification, publication, transmission, transfer, sale distribution, display or exploitation of this information, in any form or by any means, or its storage in a retrieval system, whether in whole or in part, without the express written permission of the individual copyright holder is prohibited without prior approval by IMS. Cover image by Angel Hsu. © 国际媒体支持组织 版权所有 2011 任何媒体、网站或个人未经“国际媒体支持组织”的书面许可,不得引用、复 制、转载、摘编、发售、储存于检索系统,或以其他任何方式非法使用本报告全 部或部分内容。 封面照片由徐安琪摄。 International Media Support (IMS) Communications Unit, Nørregade 18, Copenhagen K 1165, Denmark Phone: +4588327000, Fax: +4533120099 Email: [email protected] www.i-m-s.dk Caixin Media Floor 15/16, Tower A, Winterless Center, No.1 Xidawanglu, Chaoyang District, Beijing 100026, P.R.China http://english.caing.com/ chinadialogue Suite 306 Grayston Centre, 28 Charles Square, London N1 6HT, United Kingdom Phone: +442073244767 Email: [email protected] www.chinadialogue.net Climate-change journalism in China: opportunities for international cooperation By Sam Geall1 Foreword by Hu Shuli2 p4 1. Sam Geall is deputy editor of chinadialogue. The author acknowledges generous contributions to the research and analysis in this report from Li Hujun, Wang Haotong, Eliot Gao and Lisa Lin. Essential input and support were also provided by Martin Breum, Martin Gottske, Isabel Hilton, Tan Copsey, Li Dawei, Ma Ling, Hu Shuli, Bruce Lewenstein and Jia Hepeng. 2. Hu Shuli is editor-in-chief of Caixin Media (the Beijing-based media group that publishes Century Weekly and China Reform), the former founding editor of Caijing magazine and a prominent investigative journalist and commentator. -

Printmgr File

THIS WEB PROOF INFORMATION PACK IS IN DRAFT FORM. The information contained herein is incomplete and subject to change and it must be read in conjunction with the section headed “Warning” on the cover of this Web Proof Information Pack. OUR HISTORY AND CORPORATE STRUCTURE Important Milestones The following are the important milestones in our history to date: Year Event August 1999 Our Company was incorporated in the PRC. July 2000 We first obtained accreditation of ISO 9001 in respect of our quality control system. October 2000 We became listed on the SZSE. July 2003 We received certification from TüV Rheinland, German for our quality management system. August 2003 We acquired all the operating assets of Zhongbiao. November 2003 We acquired the crane machinery business of Hunan Puyuan Construction Machinery Co., Ltd. December 2004 We manufactured the QUY200 crawler crane, the then largest crawler crane in the PRC. March 2005 We developed and manufactured a 12-tons high pressure washing vehicle ZLJ520GQX. July 2005 The Company received CE certification for pumping machines and entered into the European market. July 2006 We implemented our share reform, where the non-tradable Shares of our Company were converted into tradable Shares. August 2006 Our Company’s tower crane was first exported to Europe. October 2006 We successfully manufactured and developed the QUY600 crawler crane, the then largest crawler crane in the PRC. November 2006 Our Company manufactured the YZ27 road roller with the largest vibrating power in the PRC. September 2008 We acquired CIFA. August 2009 We manufactured a four-bridge chassis six-joint jibs 56m pump-truck. -

Incentives in China's Reformation of the Sports Industry

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Keck Graduate Institute Claremont Colleges Scholarship @ Claremont CMC Senior Theses CMC Student Scholarship 2017 Tapping the Potential of Sports: Incentives in China’s Reformation of the Sports Industry Yu Fu Claremont McKenna College Recommended Citation Fu, Yu, "Tapping the Potential of Sports: Incentives in China’s Reformation of the Sports Industry" (2017). CMC Senior Theses. 1609. http://scholarship.claremont.edu/cmc_theses/1609 This Open Access Senior Thesis is brought to you by Scholarship@Claremont. It has been accepted for inclusion in this collection by an authorized administrator. For more information, please contact [email protected]. Claremont McKenna College Tapping the Potential of Sports: Incentives in China’s Reformation of the Sports Industry Submitted to Professor Minxin Pei by Yu Fu for Senior Thesis Spring 2017 April 24, 2017 2 Abstract Since the 2010s, China’s sports industry has undergone comprehensive reforms. This paper attempts to understand this change of direction from the central state’s perspective. By examining the dynamics of the basketball and soccer markets, it discovers that while the deregulation of basketball is a result of persistent bottom-up effort from the private sector, the recentralization of soccer is a state-led policy change. Notwithstanding the different nature and routes between these reforms, in both sectors, the state’s aim is to restore and strengthen its legitimacy within the society. Amidst China’s economic stagnation, the regime hopes to identify sectors that can drive sustainable growth, and to make adjustments to its bureaucracy as a way to respond to the society’s mounting demand for political modernization. -

Lu Zhiqiang China Oceanwide

08 Investment.FIN.qxp_Layout 1 14/9/16 12:21 pm Page 81 Week in China China’s Tycoons Investment Lu Zhiqiang China Oceanwide Oceanwide Holdings, its Shenzhen-listed property unit, had a total asset value of Rmb118 billion in 2015. Hurun’s China Rich List He is the key ranked Lu as China’s 8th richest man in 2015 investor behind with a net worth of Rmb83 billlion. Minsheng Bank and Legend Guanxi Holdings A long-term ally of Liu Chuanzhi, who is known as the ‘godfather of Chinese entrepreneurs’, Oceanwide acquired a 29% stake in Legend Holdings (the parent firm of Lenovo) in 2009 from the Chinese Academy of Social Sciences for Rmb2.7 billion. The transaction was symbolic as it marked the dismantling of Legend’s SOE status. Lu and Liu also collaborated to establish the exclusive Taishan Club in 1993, an unofficial association of entrepreneurs named after the most famous mountain in Shandong. Born in Shandong province in 1951, Lu In fact, according to NetEase Finance, it was graduated from the elite Shanghai university during the Taishan Club’s inaugural meeting – Fudan. His first job was as a technician with hosted by Lu in Shandong – that the idea of the Shandong Weifang Diesel Engine Factory. setting up a non-SOE bank was hatched and the proposal was thereafter sent to Zhu Getting started Rongji. The result was the establishment of Lu left the state sector to become an China Minsheng Bank in 1996. entrepreneur and set up China Oceanwide. Initially it focused on education and training, Minsheng takeover? but when the government initiated housing Oceanwide was one of the 59 private sector reform in 1988, Lu moved into real estate. -

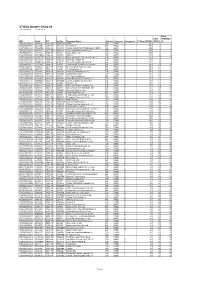

STOXX Greater China 80 Last Updated: 01.08.2017

STOXX Greater China 80 Last Updated: 01.08.2017 Rank Rank (PREVIOU ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) (FINAL) S) TW0002330008 6889106 2330.TW TW001Q TSMC TW TWD Y 113.9 1 1 HK0000069689 B4TX8S1 1299.HK HK1013 AIA GROUP HK HKD Y 80.6 2 2 CNE1000002H1 B0LMTQ3 0939.HK CN0010 CHINA CONSTRUCTION BANK CORP H CN HKD Y 60.5 3 3 TW0002317005 6438564 2317.TW TW002R Hon Hai Precision Industry Co TW TWD Y 51.5 4 4 HK0941009539 6073556 0941.HK 607355 China Mobile Ltd. CN HKD Y 50.8 5 5 CNE1000003G1 B1G1QD8 1398.HK CN0021 ICBC H CN HKD Y 41.3 6 6 CNE1000003X6 B01FLR7 2318.HK CN0076 PING AN INSUR GP CO. OF CN 'H' CN HKD Y 32.0 7 9 CNE1000001Z5 B154564 3988.HK CN0032 BANK OF CHINA 'H' CN HKD Y 31.8 8 7 KYG217651051 BW9P816 0001.HK 619027 CK HUTCHISON HOLDINGS HK HKD Y 31.1 9 8 HK0388045442 6267359 0388.HK 626735 Hong Kong Exchanges & Clearing HK HKD Y 28.0 10 10 HK0016000132 6859927 0016.HK 685992 Sun Hung Kai Properties Ltd. HK HKD Y 20.6 11 12 HK0002007356 6097017 0002.HK 619091 CLP Holdings Ltd. HK HKD Y 20.0 12 11 CNE1000002L3 6718976 2628.HK CN0043 China Life Insurance Co 'H' CN HKD Y 20.0 13 13 TW0003008009 6451668 3008.TW TW05PJ LARGAN Precision TW TWD Y 19.7 14 15 KYG2103F1019 BWX52N2 1113.HK HK50CI CK Property Holdings HK HKD Y 18.3 15 14 CNE1000002Q2 6291819 0386.HK CN0098 China Petroleum & Chemical 'H' CN HKD Y 16.4 16 16 HK0823032773 B0PB4M7 0823.HK B0PB4M Link Real Estate Investment Tr HK HKD Y 15.4 17 19 HK0883013259 B00G0S5 0883.HK 617994 CNOOC Ltd. -

WIC Template 13/9/16 11:52 Am Page IFC1

In a little over 35 years China’s economy has been transformed Week in China from an inefficient backwater to the second largest in the world. If you want to understand how that happened, you need to understand the people who helped reshape the Chinese business landscape. china’s tycoons China’s Tycoons is a book about highly successful Chinese profiles of entrepreneurs. In 150 easy-to- digest profiles, we tell their stories: where they came from, how they started, the big break that earned them their first millions, and why they came to dominate their industries and make billions. These are tales of entrepreneurship, risk-taking and hard work that differ greatly from anything you’ll top business have read before. 150 leaders fourth Edition Week in China “THIS IS STILL THE ASIAN CENTURY AND CHINA IS STILL THE KEY PLAYER.” Peter Wong – Deputy Chairman and Chief Executive, Asia-Pacific, HSBC Does your bank really understand China Growth? With over 150 years of on-the-ground experience, HSBC has the depth of knowledge and expertise to help your business realise the opportunity. Tap into China’s potential at www.hsbc.com/rmb Issued by HSBC Holdings plc. Cyan 611469_6006571 HSBC 280.00 x 170.00 mm Magenta Yellow HSBC RMB Press Ads 280.00 x 170.00 mm Black xpath_unresolved Tom Fryer 16/06/2016 18:41 [email protected] ${Market} ${Revision Number} 0 Title Page.qxp_Layout 1 13/9/16 6:36 pm Page 1 china’s tycoons profiles of 150top business leaders fourth Edition Week in China 0 Welcome Note.FIN.qxp_Layout 1 13/9/16 3:10 pm Page 2 Week in China China’s Tycoons Foreword By Stuart Gulliver, Group Chief Executive, HSBC Holdings alking around the streets of Chengdu on a balmy evening in the mid-1980s, it quickly became apparent that the people of this city had an energy and drive Wthat jarred with the West’s perception of work and life in China. -

Hang Seng Indexes Announces Index Review Results

14 August 2020 Hang Seng Indexes Announces Index Review Results Hang Seng Indexes Company Limited (“Hang Seng Indexes”) today announced the results of its review of the Hang Seng Family of Indexes for the quarter ended 30 June 2020. All changes will take effect on 7 September 2020 (Monday). 1. Hang Seng Index The following constituent changes will be made to the Hang Seng Index. The total number of constituents remains unchanged at 50. Inclusion: Code Company 1810 Xiaomi Corporation - W 2269 WuXi Biologics (Cayman) Inc. 9988 Alibaba Group Holding Ltd. - SW Removal: Code Company 83 Sino Land Co. Ltd. 151 Want Want China Holdings Ltd. 1088 China Shenhua Energy Co. Ltd. - H Shares The list of constituents is provided in Appendix 1. The Hang Seng Index Advisory Committee today reviewed the fast expanding innovation and new economy sectors in the Hong Kong capital market and agreed with the proposal from Hang Seng Indexes to conduct a comprehensive study on the composition of the Hang Seng Index. This holistic review will encompass various aspects including, but not limited to, composition and selection of constituents, number of constituents, weightings, and industry and geographical representation, etc. The underlying aim of the study is to ensure the Hang Seng Index continues to serve as the most representative and important benchmark of the Hong Kong stock market. Hang Seng Indexes will report its findings and propose recommendations to the Advisory Committee within six months. The number of constituents of the Hang Seng Index may increase during this period. Hang Seng Indexes Announces Index Review Results /2 2. -

Hang Seng Indexes Announces Index Review Results

25 February 2016 HANG SENG INDEXES ANNOUNCES INDEX REVIEW RESULTS Hang Seng Indexes Company Limited (“Hang Seng Indexes”) today announced the results of its review of the Hang Seng Family of Indexes for the quarter ended 31 December 2015. All changes will be effective on 14 March 2016 (Monday). 1. Hang Seng Index The following constituent changes will be made to the Hang Seng Index. The total number of constituents is fixed at 50. Inclusion: Code Company FAF (%) Sub-Index Cheung Kong Infrastructure 1038 25 Utilities Holdings Ltd. Removal: Code Company FAF (%) Sub-Index China Resources Beer 291 50 Commerce & Industry (Holdings) Co. Ltd. The list of constituents is provided in Appendix 1. 2. Hang Seng China Enterprises Index There is no change to the constituents of the Hang Seng China Enterprises Index. The total number of constituents is fixed at 40. The list of constituents is provided in Appendix 2. 3. Hang Seng Composite LargeCap & MidCap Index The following constituent changes will be made to the Hang Seng Composite LargeCap & MidCap Index. The total number of constituents will increase from 280 to 299. more… HANG SENG INDEXES ANNOUNCES INDEX REVIEW RESULTS/ 2 Inclusion: Code Company 10 Hang Lung Group Ltd. 109 Good Resources Holdings Ltd. 136 HengTen Networks Group Ltd. 400 Cogobuy Group 405 Yuexiu Real Estate Investment Trust 607 Fullshare Holdings Ltd. 715 China Oceanwide Holdings Ltd. 911 Hang Fat Ginseng Holdings Co. Ltd. 958 Huaneng Renewables Corporation Ltd. - H Shares 1071 Huadian Power International Corporation Ltd. - H Shares 1282 China Goldjoy Group Ltd. 1308 SITC International Holdings Co. -

Istoxx® Developed and Emerging Markets Ex Usa Pk Vn Real Estate

ISTOXX® DEVELOPED AND EMERGING MARKETS EX USA PK VN REAL ESTATE Components1 Company Supersector Country Weight (%) Vonovia SE Real Estate Germany 3.58 Goodman Group Real Estate Australia 2.31 Mitsubishi Estate Co. Ltd. Real Estate Japan 2.14 Mitsui Fudosan Co. Ltd. Real Estate Japan 2.06 Sun Hung Kai Properties Ltd. Real Estate Hong Kong 2.00 Link Real Estate Investment Tr Real Estate Hong Kong 1.79 DEUTSCHE WOHNEN Real Estate Germany 1.71 Sumitomo Realty & Development Real Estate Japan 1.50 SEGRO Real Estate Great Britain 1.44 CK Asset Holdings Ltd Real Estate Hong Kong 1.33 China Resources Land Ltd. Real Estate China 1.14 SM Prime Holdings Inc Real Estate Philippines 1.11 LEG IMMOBILIEN Real Estate Germany 1.06 SCENTRE GROUP Real Estate Australia 1.04 UNIBAIL-RODAMCO-WESTFIELD Real Estate France 1.04 AROUNDTOWN (FRA) Real Estate Germany 0.85 China Overseas Land & Investme Real Estate China 0.84 WHARF REIC Real Estate Hong Kong 0.78 Mirvac Group Real Estate Australia 0.78 DEXUS Real Estate Australia 0.77 Nippon Building Fund Inc. Real Estate Japan 0.77 Stockland Real Estate Australia 0.75 Japan Real Estate Investment C Real Estate Japan 0.73 SWISS PRIME SITE Real Estate Switzerland 0.73 CAPTIALAND INT COMM TRUST Real Estate Singapore 0.71 GECINA Real Estate France 0.70 Ayala Land Inc Real Estate Philippines 0.69 Ascendas Real Estate Investmen Real Estate Singapore 0.68 New World Development Co. Ltd. Real Estate Hong Kong 0.66 CANADIAN APARTMENT PROP REIT Real Estate Canada 0.66 NIPPON PROLOGIS REIT Real Estate Japan 0.63 NOMURA REIT.MASTER FUND Real Estate Japan 0.62 CapitaLand Ltd. -

The Coronavirus Cover-Up: a Timeline

SITUATION BRIEF April 10, 2020 • China Studies Program The Coronavirus Cover-Up: A Timeline How the Chinese Communist Party Misled the World about COVID-19 and Is Using the World Health Organization As an Instrument of Propaganda Executive Summary The People’s Republic of China (PRC) and its ruling Chi- assertions, the harm would have been significantly reduced. nese Communist Party (CCP) have deceived the world Instead, the PRC’s actions and WHO’s inaction precipitat- about the coronavirus since its appearance in late 2019. In ed a pandemic, leading to a global economic crisis and a this situation brief, the Victims of Communism Memorial growing loss of human life. Foundation compares the timeline and facts with China’s ongoing disinformation campaign about the coronavirus’ As a matter of justice, and to prevent future pandemics, the origins, nature, and spread. This brief also demonstrates PRC must be held accountable through demands for eco- how the World Health Organization (WHO) has promoted nomic reparations and other sanctions pertaining to human and helped legitimize China’s false claims. rights. China should also be suspended from full member- ship in the WHO and the WHO, which U.S. taxpayers fund The consequences of China’s deception and the WHO’s cre- annually, must be subject to immediate investigation and re- dulity are now playing out globally. It is normally difficult to form. Media organizations reporting on the claims of China assign culpability to governments and organizations charged and WHO regarding the pandemic without scrutiny or con- with ensuring public health in any pandemic, but the coro- text must be cautioned against misleading the public. -

COVID-19 and China: a Chronology of Events (December 2019-January 2020)

COVID-19 and China: A Chronology of Events (December 2019-January 2020) Updated May 13, 2020 Congressional Research Service https://crsreports.congress.gov R46354 SUMMARY R46354 COVID-19 and China: A Chronology of Events May 13, 2020 (December 2019-January 2020) Susan V. Lawrence In Congress, multiple bills and resolutions have been introduced related to China’s Specialist in Asian Affairs handling of a novel coronavirus outbreak in Wuhan, China, that expanded to become the coronavirus disease 2019 (COVID-19) global pandemic. This report provides a timeline of key developments in the early weeks of the pandemic, based on available public reporting. It also considers issues raised by the timeline, including the timeliness of China’s information sharing with the World Health Organization (WHO), gaps in early information China shared with the world, and episodes in which Chinese authorities sought to discipline those who publicly shared information about aspects of the epidemic. Prior to January 20, 2020—the day Chinese authorities acknowledged person-to-person transmission of the novel coronavirus—the public record provides little indication that China’s top leaders saw containment of the epidemic as a high priority. Thereafter, however, Chinese authorities appear to have taken aggressive measures to contain the virus. The Appendix includes a concise version of the timeline. A condensed version is below: Late December: Hospitals in Wuhan, China, identify cases of pneumonia of unknown origin. December 30: The Wuhan Municipal Health Commission issues “urgent notices” to city hospitals about cases of atypical pneumonia linked to the city’s Huanan Seafood Wholesale Market. The notices leak online.