Alaska Air Group (ALK)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

News Release

Contacts: SJC - Rosemary Barnes 408-392-1199 / [email protected] Alaska Airlines – Media Relations 206-304-0008 / [email protected] April 4, 2018 NEWS RELEASE New Daytime, Nonstop Service to New York’s JFK on Alaska Airlines from Silicon Valley’s Airport -- No. 1 Requested Domestic Market by Silicon Valley Travelers; Daily, Daytime Nonstop Flight Begins July 6, 2018 -- San José, Calif. – Alaska Airlines today announced plans to begin daily, nonstop service to New York’s John F. Kennedy Airport (JFK) from Mineta San José International Airport (SJC) beginning July 6, 2018. The new service is significant as it marks the first daytime nonstop flight from SJC to JFK, the No. 1 requested domestic market by Silicon Valley travelers. Tickets are on sale now at www.alaskaair.com. Silicon Valley business and leisure travelers will love the addition of a direct, daytime flight to New York,” said San José Mayor Sam Liccardo. “I thank CEO Brad Tilden and his team at Alaska Airlines for launching this new nonstop service to New York-JFK, and for continuing to invest in destinations that are a high priority for our travelers.” Alaska will operate the daily service using modern Airbus A320 aircraft as follows: City Pair Departs Arrives San José – New York/JFK 7:05 a.m. 3:43 p.m. New York/JFK – San José 4:45 p.m. 8:23 p.m. Times are local. Average flight time is 6 hours. “We continue to add exciting new destinations from San Jose, providing our valued guests more nonstop options to meet their business and leisure needs,” said John Kirby, Alaska’s vice president of capacity planning. -

Adaptive Connected.Xlsx

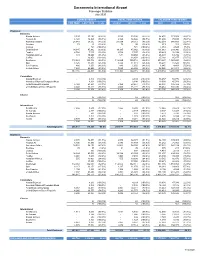

Sacramento International Airport Passenger Statistics July 2020 CURRENT MONTH FISCAL YEAR TO DATE CALENDAR YEAR TO DATE THIS YEAR LAST YEAR % +/(-) 2020/21 2019/20 % +/(-) 2020 2019 % +/(-) Enplaned Domestic Alaska Airlines 3,593 33,186 (89.2%) 3,593 33,186 (89.2%) 54,432 173,858 (68.7%) Horizon Air 6,120 14,826 (58.7%) 6,120 14,826 (58.7%) 31,298 75,723 (58.7%) American Airlines 28,089 54,512 (48.5%) 28,089 54,512 (48.5%) 162,319 348,689 (53.4%) Boutique 79 95 (16.8%) 79 95 (16.8%) 613 201 205.0% Contour - 721 (100.0%) - 721 (100.0%) 4,461 2,528 76.5% Delta Airlines 14,185 45,962 (69.1%) 14,185 45,962 (69.1%) 111,063 233,946 (52.5%) Frontier 4,768 7,107 (32.9%) 4,768 7,107 (32.9%) 25,423 38,194 (33.4%) Hawaiian Airlines 531 10,660 (95.0%) 531 10,660 (95.0%) 26,393 64,786 (59.3%) Jet Blue - 16,858 (100.0%) - 16,858 (100.0%) 25,168 85,877 (70.7%) Southwest 112,869 300,716 (62.5%) 112,869 300,716 (62.5%) 899,647 1,963,253 (54.2%) Spirit 8,425 11,318 (25.6%) 8,425 11,318 (25.6%) 38,294 15,526 146.6% Sun Country 886 1,650 (46.3%) 886 1,650 (46.3%) 1,945 4,401 (55.8%) United Airlines 7,620 46,405 (83.6%) 7,620 46,405 (83.6%) 98,028 281,911 (65.2%) 187,165 544,016 (65.6%) 187,165 544,016 (65.6%) 1,479,084 3,288,893 (55.0%) Commuters Alaska/Skywest - 4,304 (100.0%) - 4,304 (100.0%) 36,457 50,776 (28.2%) American/Skywest/Compass/Mesa - 8,198 (100.0%) - 8,198 (100.0%) 18,030 45,781 (60.6%) Delta/Skywest/Compass 5,168 23,651 (78.1%) 5,168 23,651 (78.1%) 62,894 146,422 (57.0%) United/Skywest/GoJet/Republic 4,040 16,221 (75.1%) 4,040 16,221 (75.1%) -

Womencorporatedirectors Visionary Awards May 10, 2017

WomenCorporateDirectors Visionary Awards May 10, 2017 WCD WomenCorporateDirectors (WCD) is grateful to the sponsors of the 2017 Visionary Awards GLOBAL INSTITUTE LEAD SPONSOR AND GLOBAL LEAD SPONSOR GLOBAL EXECUTIVE SPONSOR GLOBAL INSTITUTE LEADER SPONSOR GLOBAL INSTITUTE HOST SPONSOR AND GLOBAL INSTITUTE BENEFACTOR AND GLOBAL STRATEGIC SPONSOR STRATEGIC SPONSOR SUPPORTING SPONSOR GLOBAL INSTITUTE SIP AND SHOP HOST GLOBAL INSTITUTE HOST SPONSOR AND SPONSOR STRATEGIC SPONSOR GLOBAL INSTITUTE SUPPORTER GLOBAL INSTITUTE HOST GLOBAL INSTITUTE SUPPORTER GLOBAL INSTITUTE SUPPORTER GLOBAL INSTITUTE SPONSOR GLOBAL INSTITUTE SUPPORTER VISIONARY AWARDS TABLE SPONSORS Arlington Advisory Partners WomenCorporateDirectors Visionary Awards 1 Agenda 6:00 p.m. Reception 7:10 p.m. Welcome Remarks by Kapila Anand WCD Lead Director and Secretary, Director Extended Stay America, Inc., Retired Partner and Senior Advisor, KPMG; WCD Chapter Chair and Lead Director, WCD Foundation, Susan Stautberg, Chairman and Chief Executive Officer WCD Foundation; Co-Author of Women on Board, introduction of Mistress of Ceremonies, Deborah Norville (Executive Producer and Host of “Exposed with Deborah Norville” on Reelz Channel, Anchor of Inside Edition; Board member, Viacom Corporation; Director, Broadcasters Foundation of America) and introduction of Jill Kanin-Lovers (Director, Heidrick & Struggles and Homeownership Preservation Foundation; WCD New York member and Co-Chair Visionary Awards Committee), Mel Lagomasino (Chief Executive Officer & Managing Partner, WE Family Offices; Director, The Walt Disney Company, The Coca-Cola Company, and the Americas Society; WCD South Florida member and Co-Chair Visionary Awards Committee), and Pam Reeve Lead Director, American Tower Corporation; Chairman of the Board Frontier Communications; Chairman of the Board, The Commonwealth Institute; WCD Boston member and Chair Visionary Awards Event. -

Speaker Biographies 2014

Pacific Northwest Enterprise Risk Forum ~Speaker Biographies~ Mary Bennett, R.Ph., Vice President, Ethical Leadership Group - NAVEX Global Mary Bennett, R.Ph. is a Vice President, Advisory Services for NAVEX Global™ and pharmacist by training. She joined the organization as its first employee in 1999 after serving as Vice President in the Compliance and Integrity office at Caremark, where she implemented the requirements of one of the first government agreements in healthcare. With NAVEX Global, Mary works across all industries, creating and facilitating award winning training programs, conducting large and small program assessments, developing compliance communications, and helping clients develop best practice programs from the ground up. Andrew Blau, Director - Deloitte & Touche LLP Andrew Blau leads Strategic Risk Services, a new practice at Risk Advisory focused on helping clients spot, assess, and manage the most critical long-term risks to their enterprise. Previously, he was a Director at Monitor Deloitte, where he used scenarios and futures thinking to help clients understand and adapt to the uncertainties likely to shape their future. He joined Deloitte in 2013 as president and chief executive of Global Business Network, world famous for the use of scenarios and other tools that help organizations identify strategic risks, opportunities, and options in a complex and uncertain world. Andrew’s work ranges widely across topics crucial to business, government, and NGO leaders: from the future of personal mobility and transportation in Asia to the future of health and healthcare in the US, and from the future of global commerce to the evolution of corporate strategy. He has advised CEOs and leadership teams across a variety of fields, including telecommunications, media, financial services, consumer products, health care/life science, industrials, energy, and philanthropy, and served clients on six of the world’s seven continents. -

Air Travel Consumer Report

Air Travel Consumer Report A Product Of THE OFFICE OF AVIATION CONSUMER PROTECTION Issued: August 2021 Flight Delays1 June 2021 January - June 2021 Mishandled Baggage, Wheelchairs, and Scooters 1 June 2021 January -June 2021 Oversales1 2nd Quarter 2021 Consumer Complaints2 June 2021 (Includes Disability and January - June 2021 Discrimination Complaints) Airline Animal Incident Reports4 June 2021 Customer Service Reports to 3 the Dept. of Homeland Security June 2021 1 Data collected by the Bureau of Transportation Statistics. Website: http://www.bts.gov 2 Data compiled by the Office of Aviation Consumer Protection. Website: http://www.transportation.gov/airconsumer 3 Data provided by the Department of Homeland Security, Transportation Security Administration 4 Data collected by the Office of Aviation Consumer Protection. TABLE OF CONTENTS Section Page Section Page Flight Delays Flight Delays (continued) Introduction 3 Table 8 35 Explanation 4 List of Regularly Scheduled Domestic Flights with Tarmac Delays Over 3 Hours, By Marketing/Operating Carrier Branded Codeshare Partners 5 Table 8A Table 1 6 List of Regularly Scheduled International Flights with 36 Overall Percentage of Reported Flight Tarmac Delays Over 4 Hours, By Marketing/Operating Carrier Operations Arriving On-Time, by Reporting Marketing Carrier Appendix 37 Table 1A 7 Mishandled Baggage Overall Percentage of Reported Flight Ranking- by Marketing Carrier (Monthly) 39 Operations Arriving On-Time, by Reporting Operating Carrier Ranking- by Marketing Carrier (YTD) 40 Table 1B 8 -

Alaska Air Group Sustainability Report 2012

Alaska Air Group Sustainability Report 2012 Reporting period January 1, 2010, to December 31, 2011 WHO WE ARE Welcome Alaska Air Group is committed to leading our industry in environmental stewardship. We are dedicated to honorable and responsible relationships with our customers, employees, investors, business partners and the communities where we fly. This is Air Group’s first full Sustainability Report and expands on our first Environmental Report that we published in 200. This Sustainability Report summarizes the significant effects of our environmental, economic and social goals, progress and impacts. Our intention is to transparently document our corporate social responsibility efforts and use this report as a platform for dialogue and collaboration to drive continued improvement and innovation. We report on the facilities that are maintained by Alaska Air Group. Although we do not document the environmental or social impacts of our suppliers, where relevant we describe collaborative improvement efforts and procurement restrictions. This report covers Air Group’s two carriers, Alaska Airlines and Horizon Air. We describe aggregated data for Air Group as well as separate data for the two airlines where the information is relevant and available. This report summarizes data from Jan. , 200, to Dec. 3, 20. Where available, we include data showing trends over multiple years. This report is consistent with Level B requirements of the internationally recognized Global Reporting Initiative. Although the report has not been externally assured, financial and governance data drawn from our 2011 Annual Report (as reported on Form 0k) were audited by KPMG. Our current plan is to publish a Sustainability Report every other year. -

Investor Updates

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, DC 20549 FORM 8-K CURRENT REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 April 25, 2019 (Date of earliest event reported) ALASKA AIR GROUP, INC. (Exact Name of Registrant as Specified in Its Charter) Delaware (State or Other Jurisdiction of Incorporation) 1-8957 91-1292054 (Commission File Number) (IRS Employer Identification No.) 19300 International Boulevard, Seattle, Washington 98188 (Address of Principal Executive Offices) (Zip Code) (206) 392-5040 (Registrant's Telephone Number, Including Area Code) (Former Name or Former Address, if Changed Since Last Report) Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2. below): o Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) o Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) o Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) o Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (17 CFR 230.405) or Rule 12b-2 of the Securities Exchange Act of 1934 (17 CFR 240.12b-2). o Emerging growth company If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. -

Pilots Jump to Each Section Below Contents by Clicking on the Title Or Photo

November 2018 Aero Crew News Your Source for Pilot Hiring and More... ExpressJet is taking off with a new Pilot Contract Top-Tier Compensation and Work Rules $40/hour first-year pay $10,000 annual override for First Officers, $8,000 for Captains New-hire bonus 100% cancellation and deadhead pay $1.95/hour per-diem Generous 401(k) match Friendly commuter and reserve programs ARE YOU READY FOR EXPRESSJET? FLEET DOMICILES UNITED CPP 126 - Embraer ERJ145 Chicago • Cleveland Spend your ExpressJet career 20 - Bombardier CRJ200 Houston • Knoxville knowing United is in Newark your future with the United Pilot Career Path Program Apply today at expressjet.com/apply. Questions? [email protected] expressjet.com /ExpressJetPilotRecruiting @expressjetpilots Jump to each section Below contents by clicking on the title or photo. November 2018 20 36 24 50 32 Also Featuring: Letter from the Publisher 8 Aviator Bulletins 10 Self Defense for Flight Crews 16 Trans States Airlines 42 4 | Aero Crew News BACK TO CONTENTS the grid New Airline Updated Flight Attendant Legacy Regional Alaska Airlines Air Wisconsin The Mainline Grid 56 American Airlines Cape Air Delta Air Lines Compass Airlines Legacy, Major, Cargo & International Airlines Hawaiian Airlines Corvus Airways United Airlines CommutAir General Information Endeavor Air Work Rules Envoy Additional Compensation Details Major ExpressJet Airlines Allegiant Air GoJet Airlines Airline Base Map Frontier Airlines Horizon Air JetBlue Airways Island Air Southwest Airlines Mesa Airlines Spirit Airlines -

Q3 2019 Alaska Air Group Inc Earnings Call on October 24, 2019 / 8:30PM

Client Id: 77 THOMSON REUTERS STREETEVENTS EDITED TRANSCRIPT ALK - Q3 2019 Alaska Air Group Inc Earnings Call EVENT DATE/TIME: OCTOBER 24, 2019 / 8:30PM GMT OVERVIEW: Co. reported 3Q19 GAAP net income of $322m, adjusted net income of $326m and adjusted EPS of $2.63. THOMSON REUTERS STREETEVENTS | www.streetevents.com | Contact Us ©2019 Thomson Reuters. All rights reserved. Republication or redistribution of Thomson Reuters content, including by framing or similar means, is prohibited without the prior written consent of Thomson Reuters. 'Thomson Reuters' and the Thomson Reuters logo are registered trademarks of Thomson Reuters and its affiliated companies. Client Id: 77 OCTOBER 24, 2019 / 8:30PM, ALK - Q3 2019 Alaska Air Group Inc Earnings Call CORPORATE PARTICIPANTS Andrew R. Harrison Alaska Air Group, Inc. - Executive VP & Chief Commercial Officer of Alaska Airlines Inc. Benito Minicucci Alaska Air Group, Inc. - President & COO of Alaska Airlines Inc and CEO of Virgin America Inc Bradley D. Tilden Alaska Air Group, Inc. - Chairman, CEO & President Brandon S. Pedersen Alaska Air Group, Inc. - CFO, Executive VP of Finance & Treasurer Christopher Michael Berry Alaska Air Group, Inc. - VP of Finance & Controller Emily Halverson Nathaniel Pieper Alaska Airlines, Inc. - SVP of Fleet, Finance and Alliances Shane R. Tackett Alaska Air Group, Inc. - Executive VP of Planning & Strategy of Alaska Airlines, Inc. CONFERENCE CALL PARTICIPANTS Brandon Robert Oglenski Barclays Bank PLC, Research Division - VP & Senior Equity Analyst Catherine Maureen O'Brien Goldman Sachs Group Inc., Research Division - Equity Analyst Daniel J. McKenzie The Buckingham Research Group Incorporated - Research Analyst Duane Thomas Pfennigwerth Evercore ISI Institutional Equities, Research Division - Senior MD Helane R. -

Investor Updates

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, DC 20549 FORM 8-K CURRENT REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 January 15, 2021 (Date of earliest event reported) ALASKA AIR GROUP, INC. (Exact Name of Registrant as Specified in Its Charter) Delaware (State or Other Jurisdiction of Incorporation) 1-8957 91-1292054 (Commission File Number) (IRS Employer Identification No.) 19300 International Boulevard Seattle Washington 98188 (Address of Principal Executive Offices) (Zip Code) (206) 392-5040 (Registrant's Telephone Number, Including Area Code) (Former Name or Former Address, if Changed Since Last Report) Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2. below): ☐ Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) ☐ Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) ☐ Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) ☐ Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) Securities registered pursuant to Section 12(b) of the Act: Title of each class Ticker Symbol Name of each exchange on which registered Common stock, $0.01 par value ALK New York Stock Exchange Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (17 CFR 230.405) or Rule 12b-2 of the Securities Exchange Act of 1934 (17 CFR 240.12b-2). -

Alaska Airlines Ranks Highest in Traditional Network Carrier Satisfaction Rankings for Fifth Straight Year in J.D. Power and Associates Study

Alaska Airlines Ranks Highest in Traditional Network Carrier Satisfaction Rankings For Fifth Straight Year In J.D. Power And Associates Study SEATTLE - Alaska Airlines ranked highest in airline customer satisfaction among traditional network carriers for the fifth consecutive year by J.D. Power and Associates in its 2012 North America Airline Satisfaction StudySM. The airline also ranked highest J.D. Power and Associates' annual segment rankings in 2008, 2009, 2010 and 2011. "We're humbled to receive high honors from our customers five consecutive years in a row," said Alaska Air Group President and CEO Brad Tilden. "This honor would not be possible without the hard work of our dedicated employees whose commitment to safety, customer service and cutting-edge innovation has made travel on Alaska Airlines among the best in the industry." Alaska Airlines ranked highest in four of the seven measures ranked by travelers, including check-in; reservation; flight crew; and boarding/deplaning/baggage. Alaska is the only U.S. carrier to offer a baggage service guarantee, which provides customers with a $20 discount coupon on a future Alaska Airlines flight or 2,000 Alaska Airlines Mileage Plan frequent flier miles if their luggage is not at the carousel within 20 minutes after their flight arrives at the gate. Learn more about the guarantee online at fcp://@Eagle.AlaskaAir.com,%236000705/Mailbox/blank//bit.ly/ncl8 http://bit.ly/ncl8k. J.D. Power and Associates' 2012 North America Airlines Satisfaction StudySM is based on responses from more than 13,500 passengers who flew on a major North America carrier between July 2011 and April 2012. -

North American Airlines Take Off by Alan Wise, Ketil Gjerstad, Marguerite Fitzgerald, and Jason Guggenheim

The 2017 Consumer Value Creators Series NorTh AmeriCAN AirliNeS TAke off By Alan Wise, Ketil Gjerstad, Marguerite Fitzgerald, and Jason Guggenheim he airline industry is dominating The Top Ten Tthe travel and tourism sector—out- Of the top ten performers on this year’s pacing hotels, cruise lines, and others in travel and tourism list, nine are in the air- the sector in terms of value creation. North line industry and seven are based in North American carriers in particular have bene- America. (See the exhibit.) That includes fited from restructuring, scale efficiencies, five US carriers: and consolidation over the past decade, giving them a strong position and lower • Hawaiian Holdings, parent company of costs in a robust market. Hawaiian Airlines (which finished first) In 2017, The Boston Consulting Group con- • Delta Air Lines (fourth) ducted its annual study of the total share- holder return (TSR) of more than 2,300 • Southwest Airlines (fifth) publicly traded companies in 33 industry sectors, including 80 companies in travel • Alaska Air Group (sixth) and tourism. (See “How Top Value Creators Outpace the Market—for Decades,” BCG • JetBlue Airways (tenth) article, July 2017.) It’s tempting to cite lower fuel costs as the From 2012 through 2016, the global travel reason for this collective strength, but and tourism sector delivered an average that’s likely a subordinate factor at best. annual return of 19%. It ranked ninth Lower fuel prices affect all carriers world- among the 33 sectors we analyzed and sec- wide, not only those in the US. ond among the five consumer segments.