BCC Pension Fund Annual Report 2014/15

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Buckinghamshire Standing Advisory Council on Religious Education

Buckinghamshire Standing Advisory Council on Religious Education Annual Report 2017-18 Learning and growing through challenging RE 1 Contents Page No. Foreword from the Chair……………………………………………………………….. 1. Standards and quality of provision of RE: 2. Managing the SACRE and Partnership with the LA and Other Key Stakeholders: 3. Effectiveness of the Agreed Syllabus: 4. Collective Worship: 5. SACRE and School Improvement: Appendix 1: Examination data…………………….………………………………… Appendix 2: Diversity in Christianity ……………………………………………… Appendix 3: SACRE Membership and attendance for the year 2016/2017…… 2 Learning and growing through challenging RE Foreword from the Chair of SACRE September 2017 - July 2018 As with any organisation it is the inspiration given by the members that provides the character. I shall focus on some of the creativity we have valued in Bucks SACRE this year both from our members and during our visits to schools. In addition, we receive wise counsel from our Education Officer at Bucks CC, Katherine Wells and our RE Adviser Bill Moore. At our meeting in October we learned that Suma Din our Muslim deputy had become a school governor and would no longer fulfil her role with SACRE. However, her legacy to us is her book published by the Institute of Education Press entitled ‘Muslim Mothers and their children’s schooling.’ See SACRED 7, for a review. (For this and all other references to SACRED see the website at the end of this section). In her contribution to SACRED 6 Suma wrote; From the Qur’an, I understand my role as being a ‘steward’ on this earth; one who will take care, take responsibility and hand on a legacy to those who come after them. -

Royal Holloway University of London Aspiring Schools List for 2020 Admissions Cycle

Royal Holloway University of London aspiring schools list for 2020 admissions cycle Accrington and Rossendale College Addey and Stanhope School Alde Valley School Alder Grange School Aldercar High School Alec Reed Academy All Saints Academy Dunstable All Saints' Academy, Cheltenham All Saints Church of England Academy Alsop High School Technology & Applied Learning Specialist College Altrincham College of Arts Amersham School Appleton Academy Archbishop Tenison's School Ark Evelyn Grace Academy Ark William Parker Academy Armthorpe Academy Ash Hill Academy Ashington High School Ashton Park School Askham Bryan College Aston University Engineering Academy Astor College (A Specialist College for the Arts) Attleborough Academy Norfolk Avon Valley College Avonbourne College Aylesford School - Sports College Aylward Academy Barnet and Southgate College Barr's Hill School and Community College Baxter College Beechwood School Belfairs Academy Belle Vue Girls' Academy Bellerive FCJ Catholic College Belper School and Sixth Form Centre Benfield School Berkshire College of Agriculture Birchwood Community High School Bishop Milner Catholic College Bishop Stopford's School Blatchington Mill School and Sixth Form College Blessed William Howard Catholic School Bloxwich Academy Blythe Bridge High School Bolton College Bolton St Catherine's Academy Bolton UTC Boston High School Bourne End Academy Bradford College Bridgnorth Endowed School Brighton Aldridge Community Academy Bristnall Hall Academy Brixham College Broadgreen International School, A Technology -

Bourne End Academy

Bourne End Academy Headteacher: Mr L Muhammad New Road Bourne End Buckinghamshire SL8 5BW T: 01628 819022 F: 01628 810689 E: [email protected] www.E-ACT.org.uk Consultation 5 December 2019 Dear Parent/Carer Expansion of Catchment Area I am writing to advise that Bourne End Academy is consulting on changing its catchment area as of September 2021 to extend towards both the villages of Burnham/Farnham Royal and areas of West Wycombe. A plan of the proposed extension is attached for your information. The plan highlights where our existing catchment area is - marked with just a solid line and no shading; where Burnham Park Academy’s catchment area was - shaded in light blue with diagonal lines; and where the proposed extension is – both areas marked by diagonal lines on either side of our existing catchment. The extension into Burnham is in response to a request from Buckinghamshire County Council for Bourne End Academy to expand the catchment as a result of the Secretary of State for Education's recent decision to close Burnham Park Academy. Bourne End Academy is therefore proposing to expand its catchment area to include all areas of the former Burnham Park catchment. Following the closure of Burnham Park Academy, children from this area for whom Bourne End Academy is the closest school are now eligible for free transport to the school (provided they live further than 3 miles away or their walking route is deemed unsafe). The extension into the Great Marlow catchment area is to ensure children in rural parts of Buckinghamshire have sufficient choice of school to address peaks in demand and in response to the increased popularity of the school with parents. -

Special Schools and Mainstream Schools with Additionally Resourced Provision

SPECIAL EDUCATIONAL NEEDS IN BUCKINGHAMSHIRE CONTACT DETAILS FOR SPECIAL SCHOOLS AND MAINSTREAM SCHOOLS WITH ADDITIONALLY RESOURCED PROVISION January 2016 INDEX Page Mainstream Primary Schools 3 Mainstream Secondary Schools 5 Special Schools 6 Transport 8 The initials below indicate the facilities available at each school. ASD - autistic spectrum disorder HI - hearing impairment MLD - moderate learning difficulties PD - physical disability SEMH - social, emotional and mental health needs SLCN - speech, language and communication difficulties SLD - severe learning difficulties VI - visual impairment 2 SPECIAL EDUCATION IN MAINSTREAM SCHOOLS Mainstream, or ordinary, schools can usually offer the support detailed in a Statement of Special Educational Needs or Education, Health and Care Plan. This means that most children with Statements of Special Educational Needs or Education, Health and Care Plans will be able to attend their local mainstream school. The following pages provide a list of mainstream schools with additionally resourced provision for children with specific kinds of learning difficulties. Placement within additionally resourced provision is only for children who have Statements of Special Educational Needs or Education, Health and Care Plans. MAINSTREAM PRIMARY SCHOOLS Aylesbury Area Aston Clinton School (SLCN) Tel: 01296 630276 Twitchell Lane, Aston Clinton Fax: 01296 632413 Aylesbury HP22 5JJ Oak Green School (ASD) Tel: 01296 423895 Southcourt Fax: 01296 431677 Aylesbury HP21 8LJ Stoke Mandeville Combined School (HI) Tel: -

NHC Regional Schools

NHC Regional Schools at H.W.J.C on 23 November 2019 Boys YR6+7 U30Kg Boys YR6+7 U34Kg GOLD Jamie Leroux Loughton Middle GOLD Lucas Cleaver Saffron Walden County High SILVER Jay Crowley Henlow Middle School SILVER Chayse Franklin Disraeli School BRONZE 0 BRONZE 0 BRONZE 0 BRONZE 0 FIFTH 0 FIFTH 0 FIFTH 0 FIFTH 0 Entry: 2 Entry: 2 Boys YR6+7 U38Kg Boys YR6+7 U42Kg GOLD Reece Parker St Bartholomews GOLD Anthony Egby Bohunt SILVER Kai Karimov Oasis Academy Silvertown SILVER Louis Elsom Amesbury BRONZE Ahmad Evloev St James Primary School BRONZE 0 BRONZE Daniel WealleansEgerton Rothesay School BRONZE 0 FIFTH 0 FIFTH 0 FIFTH 0 FIFTH 0 Entry: 4 Entry: 2 Boys YR6+7 U46Kg Boys YR6+7 U50Kg GOLD Lenny Tancock Bishops Stortford high GOLD Asa Ward Fitzwimarc SILVER 0 SILVER Harrison Elliott Carrington Junior School BRONZE 0 BRONZE 0 BRONZE 0 BRONZE 0 FIFTH 0 FIFTH 0 FIFTH 0 FIFTH 0 Entry: 1 Entry: 2 Boys YR6+7 U55Kg Boys YR6+7 O55Kg GOLD Albert Newbury-kemp Hemel Hempstead GOLD Billy Simpson Haberdasher Askes SILVER 0 SILVER 0 BRONZE 0 BRONZE 0 BRONZE 0 BRONZE 0 FIFTH 0 FIFTH 0 FIFTH 0 FIFTH 0 Entry: 1 Entry: 1 NHC Regional Schools at H.W.J.C on 23 November 2019 Girls YR6+7 U32Kg Girls YR6+7 U36Kg GOLD Charlotte Hunt Bourne End Academy GOLD Chloe Lymer Oaklands SILVER 0 SILVER 0 BRONZE 0 BRONZE 0 BRONZE 0 BRONZE 0 FIFTH 0 FIFTH 0 FIFTH 0 FIFTH 0 Entry: 1 Entry: 1 Girls YR6+7 U40Kg Girls YR6+7 U44Kg GOLD Jessica Rush John Colet GOLD Jessica Garrett Woodlands School Basildon SILVER Maria Zielinska St Thomas of Canterbury Catholic Primary School SILVER -

Buckingham ITE Partnership Initial Teacher Education Inspection Report Inspection Dates Stage 1: 29/06/2015 Stage 2: 07/12/15

Buckingham ITE Partnership Initial teacher education inspection report Inspection dates Stage 1: 29/06/2015 Stage 2: 07/12/15 This inspection was carried out by Her Majesty’s Inspectors in accordance with the ‘Initial teacher education inspection handbook’. This handbook sets out the statutory basis and framework for initial teacher education (ITE) inspections in England from September 2015. The inspection draws on evidence from each phase and separate route within the ITE partnership to make judgements against all parts of the evaluation schedule. Inspectors focused on the overall effectiveness of the ITE partnership in securing high-quality outcomes for trainees. Inspection judgements Key to judgements: Grade 1 is outstanding; grade 2 is good; grade 3 is requires improvement; grade 4 is inadequate Primary and Secondary QTS Overall effectiveness 2 How well does the partnership secure consistently high quality outcomes for trainees? The outcomes for trainees 2 The quality of training across the 2 partnership The quality of leadership and 2 management across the partnership Primary and secondary routes Information about this ITE partnership This is the first inspection of the Buckingham Partnership, which was formed in 2012 as a School Direct partnership. The partnership was awarded accreditation in 2013. Trainees follow core, School Direct and School Direct (salaried) routes. All trainees who successfully complete their training are recommended for qualified teacher status (QTS) and gain a Postgraduate Certificate of Education (PGCE) from the University of Buckingham. The partnership offers a blend of academic and school-based teacher education over 12 months. The partnership also undertakes to maintain contact with former trainees and provide further support if required, for up to five years after they qualify and obtain their first post as a newly qualified teacher (NQT). -

SECONDARY SCHOOLS DIRECTORY for Parents Who Are Applying for a Secondary School Place from September 2014

SECONDARY SCHOOLS DIRECTORY For parents who are applying for a secondary school place from September 2014 45 0 100 0 30 0 90 0 25 0 90 0 15 0 85 0 12 0 40 0 General Introduction Contact Us information The Secondary Schools Directory is Website www.buckscc.gov.uk written for parents who are applying Email [email protected] We have tried to make the Directory It is possible that other schools for a school place for their child. It as clear as possible but in some places may become an Academy after this includes a list of the secondary schools When you send us an email, make we have had to use more complicated Directory, and the Moving up to in Buckinghamshire, maps to show you sure you include your child’s name, language. Please contact us if you Secondary School guide, have gone where the schools are and gives you date of birth and current school. would like us to explain anything to to print. If you would like to check a more information about admission you. school’s status at any time, speak to rules. them direct and they will let you know. Telephone 01296 383250 At the time of going to print, the Make sure you read the Directory County Council is aware of the When we say ‘we’, ‘our’, ‘us’, ‘The with the 2015 ‘Moving up to uncertainty surrounding the future Admissions & Transport Team’ or Secondary School’ guide or the Office hours of Khalsa Secondary Academy at ‘Buckinghamshire LA’ we are talking ‘In-Year’ transfer information on our 9am – 5.30pm Monday to Thursday its existing location in Stoke Poges. -

Autism Spectrum Disorder : a Focus on Buckinghamshire Sarah Tilston

Autism Spectrum Disorder : A focus on Buckinghamshire Sarah Tilston - Designated Clinical Officer for SEND Gareth Drawmer - Head of Service Achievement & Learning • Understanding the local and national picture • What is Autism Spectrum Disorder (ASD)? • Diagnosis pathways for ASD • ASD provision within Buckinghamshire • Future planning for ASD provision Understanding the local and national picture Changes in SEN 2012 2013 2014 2015 2016 2017 2018 Buckinghamshire 3.40 3.40 3.30 3.20 3.10 3.10 3.10 South East 2.90 2.90 2.90 2.90 2.90 3.00 3.10 England 2.80 2.80 2.80 2.80 2.80 2.80 2.90 Change in types of SEND Changes in ASD EHCP Numbers What is Autism Spectrum Disorder? Understanding as in the classroom EnableNet.Info Girls and Autism It is recognised that girls with Autism Spectrum Disorder will often present later and with different areas of concern to boys. They are often overlooked within the educational setting until they are teenagers and social and educational pressures increase and they become less able to mask their disorder. Assessment by the Neurodevelopmental Team will be adjusted accordingly with less reliance on raw test data and consideration of how girls adapt their behaviours The sensory spectrum Diagnosis pathways for ASD Autism Diagnosis in Buckinghamshire 0-4 years : Community Paediatrics and Child Development Team. CDT also includes therapists for multi-disciplinary assessment 5-17 : Neurodevelopmental SPA from January 2019 with joint service provided by CAMHS and Paediatrics. (Previously 5-10 Paediatrics and 11-18 CAMHS) 18+ : The Adult ASD Diagnostic Service runs from the Whiteleaf Centre in Aylesbury offering diagnosis and post diagnostic treatment Neurodevelopmental Diagnostic Pathway (Single Point of Access) • Oxford Health Foundation Trust and Buckinghamshire Health Care Trust are collaborating to deliver a Buckinghamshire Neurodevelopmental 5-17+ year old ‘Single Point of Access for Assessment and Treatment’. -

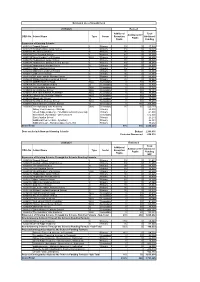

Dfes No. School Name Type Sector Additional Reception Pupils

Estimated Use of Growth Fund 2019/2020 Revised Additional Total Additional Yr7 DfES No. School Name Type Sector Reception Additional Pupils Pupils Funding Expansion of Existing Schools 8252022 Dagnall School I Primary 15 0 27,526 8252027 Denham Village Infant School I Primary 15 0 28,120 8252000 The Disraeli School C Primary 30 0 61,606 8252025 East Claydon School I Primary 15 0 27,062 8253039 Great Kimble C of E School P(A) Primary 15 0 25,656 8252276 Haddenham Junior School J Primary 30 0 53,021 8253073 Haddenham St Marys C of E School I Primary 15 0 25,434 8252242 Hughenden Primary School C Primary 15 0 28,596 8252007 Mary Towerton School I Primary 15 0 27,914 8252006 Millbrook Combined School C Primary 30 0 58,344 8252001 Oak Green School C Primary 30 0 57,184 8253376 St Louis Catholic Primary School C Primary 30 0 55,516 8252288 William Harding Combined School C Primary 30 0 55,463 8254095 AMERSHAM SCHOOL S(A) Secondary 0 30 75,576 8254004 The Buckingham School U Secondary 0 30 75,802 8254000 Chiltern Hills Academy S(A) Secondary 0 30 77,720 8255409 Great Marlow School S(A) Secondary 0 30 75,283 8254001 THE HIGHCREST ACADEMY S(A) Secondary 0 30 80,464 8254070 Holmer Green Senior School S(A) Secondary 0 60 154,064 8254067 Mandeville School U Secondary 0 30 78,058 8254084 Sir William Ramsay School S(A) Secondary 0 30 77,677 8254701 Saint Michael's Catholic School U Secondary 0 180 463,094 8256905 The Aylesbury Vale Academy S(A) Secondary 30 60 220,733 Abbey View Academy - Start-up Primary 69,000 Green Ridge Academy - Potential Diseconomy less Adj Primary -51,000 St Michaels (Aylesbury) - Diseconomies Secondary 612,000 East Claydon School Primary 26,279 Additional Year 5 Class - Aylesbury Primary 25,041 Eddlesborough - Historical Agreement - Est. -

Bourne End Academy Bourne End

BOURNE END ACADEMY Teacher of Computer Science MPS / UPS Part-time or Full-time Suitable for NQTs or experienced teachers Required January – August 2017 BOURNE END ACADEMY New Road Bourne End Bucks SL8 5BW HEADTEACHER: Mrs Andrea Jacobson Tel: 01628 819022 Fax: 01628 810689 e-mail: [email protected] Website: www.bea.bucks.sch.uk Bourne End Academy Bourne End Academy is an Upper School in the village of Bourne End in Buckinghamshire. Bourne End has good rail links to London, Marylebone and is closely placed to major motorways. Our school has 650 boys and girls in Years 7 to 13. Our students reflect a mixed ability intake. Buckinghamshire is a wholly selective authority and the top 30% of Year 6 pupils are selected for grammar school education. About three quarters of our students come from the immediate environs of Bourne End. We have an Alternative Resource Provision that supports students with autism. Bourne End Academy opened in September 2014. Its predecessor school (The Wye Valley School) was placed in special measures in January 2013: the key areas for improvement were attainment and achievement, leadership and the quality of teaching. Behaviour was and is very good. Our students are committed and enthusiastic. In January 2013, there was significant leadership change and the school has been developing at pace. The pace of change is exciting and impact is discernible. There has been a tide change in terms of student expectation, academic challenge, intervention and staffing. Bourne End Academy is sponsored by Wycombe High School, a local outstanding school, led by a National Leader of Education who is the Executive Headteacher of both Bourne End Academy and Wycombe High School. -

Newsletter 3

DECEMBER 2018 ISSUE 36 www.gms.bucks.sch.uk MESSAGE FROM THE HEADTEACHER Welcome to this Christmas edition of ‘The Voice’, which signals the end of IMPORTANT REMINDER the first full term of this academic year. This edition of ‘The Voice’ showcases ABOUT DATES IN some of the school activities and events that have occurred since the last THE WINTER TERM edition. However, this is just a taster of the multitude of articles and Term will end with final photographs that are on our school website. assemblies on Wednesday 19th There is one event that I wish to particularly highlight for the wearing of non-uniform, all the money collected December; buses have been in this edition of ‘The Voice’ and that is the recent school is donated to charity. booked for 1.00pm. production of ‘We Will Rock You’ that saw, once again, The new term starts, for the combined efforts of the Drama Department, the I began this academic year talking to all year groups all pupils, on Thursday 3rd Music Department and students from Years 7-13, who about the importance of compassion: a key word in January 2019. came together to deliver two evenings of outstanding our vision statement. I explained being compassionate entertainment. The quality of the acting and singing involved being kind. Roald Dahl wrote, “kindness is my was excellent and the comedic performances, due to number one attribute in a human being. I’ll put it before Please note all our … courage or bravery or generosity or anything else… important dates and the students’ impeccable timing, delivery and facial expressions, had the audiences laughing relentlessly Kindness … covers everything to my mind. -

Lord Grey News Grey Lord

15 March 2018, edition 11 Follow us at @lgartdept. We have some fantastic artwork being produced by students. Below is a piece by Megan McConnell and it is far beyond the level of skill that she started with. You will see more excellent artwork on Instagram and this platform is really inspiring our younger learners. Mrs Grant Head of Creative Technologies Lord Grey News YEAR 11 STUDENTS ONLY 30 SCHOOL DAYS TO YOUR FIRST EXAM! DO NOT FORGET TO SIGN UP TO THE EASTER REVISION SESSIONS! See page 2. Year 8 Parents’ Evening Tonight… Year 8 Parents’ Evening Tonight… Year 8 Parents’ Evening Tonight... 1 ONLY 30 YEAR 11 REVISION SESSION DURING SCHOOL DAYS THE EASTER HOLIDAYS TO YOUR FIRST DO NOT FORGET TO SIGN UP EXAM! FOR YOUR SESSIONS. 2 Many congratulations to all the students who have received a Headteacher’s Award. Very well done and keep up the good work!! Forename Surname Form Awards Marco Alecu C10 1 Owen Alford C07 1 Ayaan Ali E02 1 Priscilla Anim E09 1 China Barclay L03 1 Suma Begum E02 1 Kia Bowser E07 1 Hayley Bright L14 1 Lewis Campbell C06 1 Lucas Capel T07 1 Aaron Cockram L02 1 Rachel Cook L15 1 Alex Cunha C02 1 Millie Doolan E12 1 Ebenezer Dua E15 1 Faith Essilfie L02 2 Zara Fleming L05 1 Oliver Gill-Hammond E12 1 Ubayedul Haque C14 1 Daniel Hogg L14 1 Mercy Ilozor L03 1 Tizio Irie E01 1 Kelsie Jackson-King L04 1 Jamie Johnson- Green L03 2 Kaleb Justice L03 1 Michael Kyei E03 1 3 Many congratulations to all the students who have received a Headteacher’s Award.