BEV Industry in India

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Auto Sales Rev up in June As States Unlock Inventory Build-Up in Anticipation of Big July Offtake

Auto sales rev up in June as States unlock Inventory build-up in anticipation of big July offtake OUR BUREAU New Delhi, July 1 With States steadily unlock- ing, automobile companies are seeing a significant risein enquiries and bookings and stepped up dispatches to deal- ers in June. The country’s largest car- maker, Maruti Suzuki India (MSIL), on Thursday reported domestic sales soaring more than three and half times to units in May. So, did ‘City’ 1,59,561 units in the previous 1,24,280 units in June com- maker Honda Cars India dis- month. pared to 32,903 units in May. patching 4,767 units. Bajaj Auto also reported Similarly, Hyundai Motor In- factory-gate sales jumping dia (HMIL) reported sales MG, Kia retail sales up two-and-half times to 1,55,640 jumping 62 per cent to 40,496 MG Motor India said it retail units from 60,342 units in May. units in June compared with sales trebled to 3,558 units in 25,001 in May. June from 1,016 units in May. CVs, tractors too Tata Motors reported a Similarly, Kia India registered In the commercial vehicle and growth of 59 per cent to 24,110 retail sales of 15,015 units tractor segments, also, com- units from 15,181 in May. against 11,050 units in May. panies reported multi-fold Shailesh Chandra, President, “The last few weeks have jump in their sales on Passenger Vehicles Business shown signs of improved cus- monthly basis. Unit, Tata Motors, said, “The PV tomer sentiment, and we con- According to Mitul Shah, industry’s sequential growth tinue to be optimistic about Head of Research at Reliance momentum got adversely im- the future. -

Innovation in India FINAL REPORT

Innovation in India FINAL REPORT Innovation in India FINAL REPORT CONTENTS CONTENTS Foreword by Liz Mohn 6 Setting the context 7 From the authors 8 Project background 9 I. Approach and methodology 11 1. Approach 11 2. Methodology 12 About this report 14 II. Innovation in India 15 A. Is India innovating – and if so, is it original? 15 B. Characteristics of innovation in India 17 C. Five archetypes of innovation in India 19 D. Types of innovators in India 28 E. Innovation at the industry level 40 III. Influencing factors 61 A. Internal influencing factors 61 B. External influencing factors 66 4 CONTENTS IV. Future projections 88 A. Future of India’s innovation landscape 88 B. Our methodology 89 C. Critical uncertainties and dimensions 90 D. Scenario development 92 E. Analysis of scenario-planning exercise 93 F. Key takeaways 95 V. Implications for Germany 96 A. Introduction 96 B. Customer: India is a large and growing customer, market and suitable test market for Germany 96 C. Competitor: With a strong base of engineering capability, India is emerging as a formidable competitor, especially in the area of frugal engineering 97 D. Collaborator: India’s role as a collaborator on innovation with Germany is developing 99 E. Talent hub: India has evolved into a high-quality source of abundant R&D capability and human capital for German firms 102 F. Ecosystem: Many large German companies want to innovate in India due to the innovation ecosystem 103 G. Key takeaways 104 VI. Recommendations 105 A. Recommendations for India 106 B. Recommendations for Germany (in the context of India) 116 C. -

Electric Vehicle Conference 2021 Sector Report.Pdf

India Equity Research | Electric Vehicle Conference © May 23, 2021 Sector Report Emkay Electric Vehicle Conference Your success is our success Refer to important disclosures at the end of this report Decoding Electric Vehicle Disruption We organized our first ‘Electric Vehicle’ conference, featuring eminent speakers representing This report is solely produced by Emkay Global. The following person(s) are responsible for the production the entire EV value chain – Global & Indian OEMs, Government associations, Battery of the recommendation: manufacturers, Component suppliers, Sustainable mobility players and Charging infrastructure companies. We witnessed full-house participation with over 700 investor Raghunandhan N L [email protected] meetings over a period of two days. Across the value chain, the expectation of EV adoption +91 22 6624 2428 is high, and now the debate has shifted from “when” to “how fast”. Recent moves of firms across the value-chain on the product line-up and investment fronts, as well as their resolve Mumuksh Mandlesha to go ‘all electric’ have notably reset the expectations regarding the pace of EV adoption. The [email protected] key takeaways given below highlight initial signs of improving EV adoption: +91 22 6612 1334 OEMs: New products expected to drive adoption: Global OEMs already have a wide range Bhargava Perni of products, which are being introduced either directly (e.g., Mercedes Benz) or through [email protected] collaborations (e.g., GreenPower). In addition, almost all domestic OEMs and startups (e.g, +91 22 6624 2429 Ather) are also indigenously developing and launching products. These launches should drive the evolution of consumer profile from ‘early adopters’ and ‘technophile purchasers’ to ‘mass adopters’ over the medium- to longer term. -

An Organization Study O CMR Institute N Organization Study on Hero

An Organization Study on Hero MotoCorp Limited (18MBAOS307) Submitted by MONCY PAUL 1CR19MBA51 Submitted to VISVESVARAYA TECHNOLOGICAL UNIVERSITY, BELAGAVI In partial fulfillment of the requirement for the award of the degree of MASTER OF BUSINESS ADMINISTRATION Under Guidance of Internal Guide Prof. Manjunatha. S Assistant Professor Department of Management Studies CMR Institute of Technology Bangalore Department of Management Studies and Research Center CMR Institute of Technology #132, AECS Layout, Kundalahalli, Bengaluru - 560037 Class of 2019-21 1 2 DECLARATION I, Mr. Moncy Paul bearing USN 1CR19MBA51 hereby declare that the organization study conducted at Herp MotoCorp is record of independent work carried out by me under the guidance of Prof. Manjunatha.S faculty of M.B.A Department of CMR Institute of Technology, Bengaluru. I also declare that this report is prepared in partial fulfilment of the university Regulations for the award of degree of Master of Business Administration by Visvesvaraya Technological University, Belagavi. I have undergone an organization study for a period of four weeks. I further declare that this report is based on the original study undertaken by me and has not been submitted for the award of any degree/diploma from any other University/Institution. Disclaimer The enclosed document is the outcome of a student academic assignment, and does not represent the opinions/views of the University or the institution or the department or any other individuals referenced or acknowledged within the document. The data and Information studied and presented in this report have been accessed in good faith from secondary sources/web sources/public domain, including the organisation’s website, solely and exclusively for academic purposes, without any consent/permission, express or implied from the organization concerned. -

MAY 2021 | E-MAGAZINE May 2021 Page 2

EVreporter MAY 2021 | E-MAGAZINE May 2021 Page 2 WHAT'S INSIDE 5 Opex based incentive structure needed to promote e-bus adoption and usage | e- bus operator Prasanna Purple Setting up a Public EV charging station (PCS) in India | 10 Considerations and RoI estimates Hero MotoCorp and Gogoro to build electric 2W battery swapping 15 network in India | Industry experts share their views Localization Needed to realize true benefits of Electrification in 22 India | Status of localization for small electric cars How Jendamark went about building rotor, motor and inverter 27 assembly lines for Dana TM4 Shared EV Charging hubs - a solution for charging and efficient 30 real-estate utilisation 33 Top EV sellers of Apr 2021 News May 2021 Page 3 Bytes SMEV releases EV sales data for FY 20-21. Indian EV industry sold 236,802 units including electric 2Ws, electric 3Ws and electric 4Ws. Data excludes EVs not registered with the transport authority. Electric 2Ws - Total sales - 143,837 units, out of which High-speed EVs - 40,836 and low speed EVs - 103,000. Decline of 6% over FY 19-20 when 1,52,000 units were sold. Electric 3Ws - Registered sales of 88,378 units against 140,683 units sold in FY 20. Electric 4Ws - Registered sales of 4,588 units as against 3,000 units in FY 20. Hero Electric announced the sale of over 50,000 electric two-wheelers in 2020, the highest for any electric two-wheeler company in India. Through 2021, the company plans to expand its Ludhiana-based manufacturing facility from an existing capacity of 70,000 units per year to 2.5 lakh per annum. -

4W FE Declaration 2019-20.Xlsx

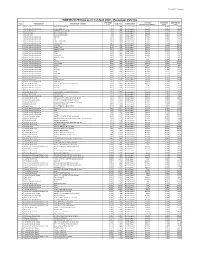

BS-VI 4W FE Declaration SIAM BS VI FE Data as on 1st April 2020 – Passenger Vehicles Kerb Weight Fuel Type Declared FE Declared CO2 S.no. Manufacturer Vehicle Model / Variant Engine cc Emission Stage (Kgs) (Gasoline/Diesel/CNG etc.) (Kmpl) (g/km) 1 Renualt India Renault KWID 0.8L MT 737 799 Bharat Stage VI Gasoline 20.710 114.50 2 Maruti Suzuki India Limited S-Presso [Std, LXI] 740 998 Bharat Stage VI Gasoline 21.400 110.81 3 Nissan Motor India DATSUN redi GO 0.8L MT 740 799 Bharat Stage VI Gasoline 20.710 114.50 4 Renualt India Renault KWID 1L MT 751 999 Bharat Stage VI Gasoline 21.700 109.30 5 Renualt India Renault KWID 1L AMT 756 999 Bharat Stage VI Gasoline 22.000 107.80 6 Maruti Suzuki India Limited TOUR H1 757 796 Bharat Stage VI Gasoline 22.050 107.54 7 Maruti Suzuki India Limited Alto 762 796 Bharat Stage VI Gasoline 22.050 107.54 8 Maruti Suzuki India Limited S-Presso [VXI, VXI+] 763 998 Bharat Stage VI Gasoline 21.700 109.28 9 Maruti Suzuki India Limited S-Presso AGS 767 998 Bharat Stage VI Gasoline 21.700 109.28 10 Maruti Suzuki India Limited TOUR H2 815 998 Bharat Stage VI Gasoline 21.620 109.63 11 Maruti Suzuki India Limited WagonR 1.0 820 998 Bharat Stage VI Gasoline 21.790 108.78 12 Maruti Suzuki India Limited WagonR 1.0 AGS 825 998 Bharat Stage VI Gasoline 21.790 108.78 13 Maruti Suzuki India Limited WagonR 1.2 835 1,197 Bharat Stage VI Gasoline 20.520 115.51 14 Maruti Suzuki India Limited Celerio 840 998 Bharat Stage VI Gasoline 21.620 109.63 15 Maruti Suzuki India Limited Celerio AGS 840 998 Bharat Stage VI Gasoline -

STUDY of ELECTRIC SCOOTERS Markets, Cases and Analyses STUDY of ELECTRIC SCOOTERS Markets, Cases and Analyses

STUDY OF ELECTRIC SCOOTERS Markets, cases and analyses STUDY OF ELECTRIC SCOOTERS Markets, cases and analyses Study prepared by Sidera Consult at the request of the German Cooperation, through the GIZ (Deutsche Gesellschaft für Internationale Zusammenarbeit GmbH) and the Ministry of Economy (ME). Authors: Carolina Ures Daniel Guth Diego Ures Victor Andrade Ministry of Economy January 2020 FEDERATIVE REPUBLIC OF BRAZIL Presidency of the Republic Jair Messias Bolsonaro Minister of Economy Paulo Roberto Nunes Guedes Special Secretary for Productivity, Employment and Competitiveness Carlos Alexandre da Costa Secretary for Development of Industry, Trade, Services and Innovation Gustavo Leipnitz Ene Technical support Cooperação Alemã para o Desenvolvimento Sustentável por meio da Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ) GmbH National Director Michael Rosenauer Project director Jens Giersdorf COORDINATION AND IMPLEMENTATION Coordination and operation staff Proofreading ME - André Sequeira Tabuquini, Bruno de Almeida Ribeiro, Ana Terra Gustavo Duarte Victer, Marcelo Vasconcellos de Araújo Lima, Ricardo Zomer e Thomas Paris Caldellas Layout design GIZ - Anna Palmeira, Bruno Carvalho, Fernando Sources, Marcus Barbara Miranda Regis e Jens Giersdorf Translation Authors Enrique Villamil Carolina Ures, Daniel Guth, Diego Ures e Victor Andrade PUBLICADO POR Technical coordination Efficient Propulsion Systems Project – PROMOB-e (Bilateral Carolina Ures (Sidera) e Fernando Sources (GIZ) Technical Cooperation Project between the Secretariat of Development of the Industry, Trade, Services and Innovation Technical review - SDIC and the German Cooperation for Sustainable Fernando Sources (GIZ) Development (GIZ) CONTACTS SDCI/Ministry of Economy Deutsche Gesellschaft für Internationale Zusammenarbeit Esplanada dos Ministérios BL J - Zona Cívico-Administrativa, (GIZ) GmbH CEP: 70053-900, Brasília - DF, Brasil. SCN Quadra 1 Bloco C Sala 1501 – 15º andar Ed. -

Electric Mobility in India Disclaimer

The case for Electric Mobility in India Disclaimer © 2018 TFE Consulting GmbH All rights reserved. May 2018, Munich, Germany No part of this report may be used or reproduced in any manner or in any form or by any means without mentioning its original source. TFE Consulting is not herein engaged in rendering professional advice and services to you. TFE Consulting makes no warranties, expressed or implied, as to the ownership, accuracy, or adequacy of the content of this report. TFE Consulting shall not be liable for any indirect, incidental, consequential, or punitive damages or for lost revenues or profits, whether or not advised of the possibility of such damages or losses and regardless of the theory of liability. The case for electric mobility in India 2 Table of Contents 1 Executive summary 4 2 The case for electric mobility in India 7 3 Growth scenario and ecosystem 10 4 Drivers of electric vehicles in India 12 5 Strategic motivations for mobility service providers to adopt EVs 15 6 Business models 6.1 Charging infrastructure 16 6.2 Battery technology 18 6.3 Digital and information technology 20 7 Looking ahead 21 Table of Figures The digital and technological revolution in electric mobility 22 1: Top 10 EV manufacturers 8 Our electric mobility services 23 2: Projected growth of EVs in India 10 3: EV ecosystem in India 11 End notes 24 4: Motivation to migrate to EVs 13 Other TFE Reports 25 Imprint 26 The case for electric mobility in India 3 Executive Summary Executive summary India is the fifth largest car market in the world and has the potential to become one of the top three in the near fu- ture – with about 400 million customers in need of mobility solutions by the year 2030. -

FADA Releases July'21 Vehicle Retail Data

FEDERATION OF AUTOMOBILE DEALERS ASSOCIATIONS 804-805-806, Surya Kiran, 19, K G Marg New Delhi - 110 001 (INDIA) T +91 11 6630 4852, 2332 0095, 4153 1495 E [email protected] CIN U74140DL2004PNL130324 FOR IMMEDIATE RELEASE FADA Releases July’21 Vehicle Retail Data • Total vehicle retails for the month of July’21 rise by 34.12% on YoY basis. When compared to July’19 (a regular pre-covid month), recovery is visible as the deficit reduces to low double digits of -13.22%. • On YoY basis, all categories were in green with 2W up by 28%, 3W up by 83%, PV up by 63%, Tractor up by 7% and CV up by 166%. • After Tractors, PV for the first time shows strong numbers by clocking 24% growth when compared to pre-covid month of July’19. • FADA has been raising red flag about semi-conductor shortage since quite some time. The situation is now becoming grave with ever-increasing supply-side constraints. • rd The delta variant and a possibility of 3 wave continues to remain a threat for stable Auto Retails. 9th August’21, New Delhi: The Federation of Automobile Dealers Associations (FADA) today released Vehicle Retail Data for July’21. July’21 Retails Commenting on how July’21 performed, FADA President, Mr. Vinkesh Gulati said, “With entire country now open, July continues to see robust recovery in Auto Retails as demand across all categories remain high. The low base effect also continues to play its part. With all categories in green, CV’s continue to see increase in demand specially in M&HCV segment with the Government rolling out infrastructure projects in many parts of the country. -

White Paper – Automotive Industry

White Paper – Automotive Industry Technology Cluster Manager (TCM) Technology Centre System Program (TCSP) Office of DC MSME, Ministry of MSME October, 2020 TCSP: Technology Cluster Manager White Paper: Automotive Industry Table of Contents 1 INTRODUCTION ......................................................................................................................................... 7 1.1 BACKGROUND .................................................................................................................................................. 7 1.2 OBJECTIVE OF WHITE PAPER ................................................................................................................................ 7 2 SECTOR OVERVIEW .................................................................................................................................... 8 2.1 GLOBAL SCENARIO ............................................................................................................................................. 8 Structure of Automotive Industry ............................................................................................................ 9 Global Business Trends .......................................................................................................................... 10 Product and Demand ............................................................................................................................. 12 Production and Supply Chain ................................................................................................................ -

Bengaluru Boy Bags Rs 60 Lakh Job at Google

JULY 2019 PAGE 1 Globally Recognized Editor-in-Chief: Azeem A. Quadeer, M.S., P.E. JULY 2019 Vol 10, Issue 7 Bengaluru boy bags Rs 60 lakh job at Google INSIDE Google, Apple, Amazon and Facebook are some of biggest tech com- panies in the world. And working in one of these companies is like a dream come true for most people. But landing up a job in these com- panies isn’t easy. Individuals need to pass several rounds of interviews to get a nod from the recruiters at these tech giant. Naturally, few make the cut. But now, a Bengaluru-based boy has broken that glass ceiling bagged a coveted spot at Google. Women have heads shaved by mob His salary? Rs 60 lakh. of men because they resisted rape The 22-year-old student of International Institute of Information Tech- nology Bangalore (IIIT-B) has landed a job at Google with a package of Rs 60 lakh. KB Shyam recently completed his five-year dual degree ATTN: INVESTORS course at IIIT_B and he will fly to Warsaw, Poland in October this year to join Google. But bagging his dream job at one of the biggest tech companies wasn’t easy. Shyam, who hails from Chennai, had to clear an online interview, Invest in an on-site interview at Munich, Germany and a team matching process to decide his team - all in a span of five months. It was only after he Dallas - Fort Worth Area completed each level that he was able to get a position at Google. -

The India Electric Vehicle Opportunity: Market Entry Toolkit

March 2021 The India Electric Vehicle Opportunity: Market Entry Toolkit Connected Places Authors Lovedeep Brar Bob Burgoyne Lovisa Eriksson Rimaljit Likhari Thalia Skoufa Lowri Williams Acknowledgments The authors would like to thank Aman Hans, Lead Consultant - Vivek Sharanappa, Co-founder the following individuals and National Energy Storage Mission, and CEO, BuyMyEV organisations for their valuable NITI Aayog contributions to this report S R Venkatesan, MD, Transvahan (errors or omissions remain the Mark Hartmann, CTO Latent Heat Technologies responsibility of the authors): Solutions Professor Dr Ashish Verma, Ms. Sonal Bhartia, Director, Ashutosh Humnabadkar, SVP, Associate Professor, Investment Banking Advisory, EY eMobility, Quanzen Transportation Systems Engineering (TSE) and Convenor, Shipra Bhutada, Founder, User Sumeet Jain, Head of UK IISc Sustainable Transportation Connect Research Agency, Outbound India Desk, HSBC Lab (IST Lab), Indian Institute of Benagluru Science (IISc) Amit B Jain, International Director, Debi Prasad Dash, Executive EY-UK Project partners: Enzen, Project Director, IESA Lithium, Shakti Foundation, Ankit Kumar, CEO, GoZero Mobility Fields of View, Everything Eco, Manoj M Desai, General Manager WRI, ISGF, UrbanMorph, C40 - Automotive Electronics Harsha Lingam, COO, Global Cities, Benagluru Directorate of Department, ARAI Business Inroads Urban Land Transport, Shell’s E4 Accelerator Programme Shalendra Gupta, CFO, Altigreen Siddharth Mukne, Associate Propulsion Labs Director, UKIBC Other organisations: SunMobility,