NASDAQ DUCK 2002.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2002 Opinions

ERIE COUNTY LEGAL JOURNAL (Published by the Committee on Publications of the Erie County Legal Journal and the Erie County Bar Association) Reports of Cases Decided in the Several Courts of Erie County for the Year 2002 LXXXV ERIE, PA JUDGES of the Courts of Erie County during the period covered by this volume of reports COURTS OF COMMON PLEAS HONORABLE WILLIAM R. CUNNINGHAM -------- President Judge HONORABLE GEORGE LEVIN ---------------------------- Senior Judge HONORABLE ROGER M. FISCHER ----------------------- Senior Judge HONORABLE FRED P. ANTHONY --------------------------------- Judge HONORABLE SHAD A. CONNELLY ------------------------------- Judge HONORABLE JOHN A. BOZZA ------------------------------------ Judge HONORABLE STEPHANIE DOMITROVICH --------------------- Judge HONORABLE ERNEST J. DISANTIS, JR. ------------------------- Judge HONORABLE MICHAEL E. DUNLAVEY -------------------------- Judge HONORABLE ELIZABETH K. KELLY ----------------------------- Judge HONORABLE JOHN J. TRUCILLA --------------------------------- Judge Volume 85 TABLE OF CASES -A- Ager, et al. v. Steris Corporation ------------------------------------------------ 54 Alessi, et al. v. Millcreek Township Zoning Hearing Bd. and Sheetz, et al. 77 Altadonna; Commonwealth v. --------------------------------------------------- 90 American Manufacturers Mutual Insurance Co.; Odom v. ----------------- 232 Azzarello; Washam v. ------------------------------------------------------------ 181 -B- Beaton, et. al.; Brown v. ------------------------------------------------------------ -

In Re Victor Romm

United States Bankruptcy Court Northern District of Illinois Eastern Division Transmittal Sheet for Opinions for Publishing and Posting on Website Will this Opinion be Published? No Bankruptcy Caption: In re Victor Romm Bankruptcy No. 05 B 46897 Adversary Caption: Pearle Vision, Inc. and Pearle, Inc. v. Victor Romm Adversary No. 06 A 69 Date of Issuance: December 13, 2006 Judge: A. Benjamin Goldgar Appearance of Counsel: Attorney for debtor Victor Romm: John O. Noland, Jr., Chicago, IL Attorneys for Pearle Vision, Inc. and Pearle Inc.: John D. Silk, Rothschild, Barry & Myers, Chicago, IL, Craig P. Rieders, Genovese Joblove & Battista, P.A., Miami, FL UNITED STATES BANKRUPTCY COURT NORTHERN DISTRICT OF ILLINOIS EASTERN DIVISION In re: ) Chapter 7 ) VICTOR ROMM, ) No. 05 B 46897 ) Debtor. ) ______________________________________ ) ) PEARLE VISION, INC., and PEARLE, ) INC., ) ) Plaintiffs, ) ) v. ) No. 06 A 69 ) VICTOR ROMM, ) ) Defendant. ) Judge Goldgar MEMORANDUM OPINION Before the court for ruling is the motion of debtor Victor Romm to dismiss the first amended adversary complaint of plaintiffs Pearle Vision, Inc. and Pearle, Inc. (collectively “Pearle”). For the reasons that follow, the motion to dismiss will be denied. 1. Background In deciding Romm’s motion, the court has considered both the first amended complaint and its exhibits, taking all facts alleged to be true. See Hollander v. Brown, 457 F.3d 688, 690 (7th Cir. 2006). The court has also reviewed the debtor’s petition and schedules, along with the district court’s docket and papers filed in the related action styled Pearle Vision, Inc., et al. v. Romm, et al., No. 04 C 4349 (N.D. -

Two Locals Perish in Car Crash

Mailed free to requesting homes in Eastford, Pomfret & Woodstock Vol. IV, No. 19 Complimentary to homes by request (860) 928-1818/e-mail: [email protected] ‘Courage is the price that life exacts for granting peace.’ FRIDAY, JANUARY 23, 2009 Two Quiet Corner observes historic inauguration day locals OBAMA SWORN IS AS 44TH U.S. PRESIDENT BY MATT SANDERSON regation, and emerged from that VILLAGER STAFF WRITER dark chapter stronger and united, Barack Obama was sworn in as we cannot help but believe that the perish in the 44th president of the United old hatreds shall someday pass; that States Tuesday, Jan. 20, at the presi- the lines of tribe shall soon dis- dential inauguration, and has solve. …” moved into his new residence with It was estimated that more than car crash his family at 1600 Pennsylvania Ave. two million people crowded the in Washington, D.C. He is the first National Mall and the parade route U.S. president of African-American along Pennsylvania Avenue just to AREA’S FIRST descent. be a part of the occasion. “… We are shaped by every lan- After being sworn in and reciting FATALITIES IN 2009 guage and culture,” said Obama in the oath of office while keeping his Matt Sanderson photo the midst of his inaugural address. left hand over the Lincoln Bible “Drawn from every end of this Bethany Mongeau and her mother Barbara Barrows, both of Brooklyn, attended BY MATT SANDERSON earth; and because we have tasted the inauguration ceremony of President Barack Obama in Washington, D.C., VILLAGER STAFF WRITER Turn To INAUGURATION, A14 the bitter swill of Civil War and seg- page Tuesday, Jan. -

Owner Info with Codes.Pdf

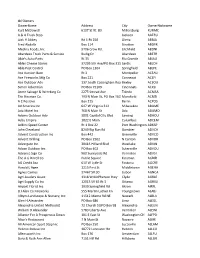

tbl Owners OwnerName Address City OwnerNickname Kurt McDowell 6107 St Rt. 83 Millersburg KURMC A & A Truck Stop Jackson AATRU Jack H Abbey Rd 1 Rt 250 Olena ABBJA Fred Abdalla Box 114 Stratton ABDFR Medina Foods, Inc 9706 Crow Rd. Litchfield ABDNI Aberdeen Truck Parts & Service Budig Dr Aberdeen ABETR Abie's Auto Parts Rt 35 Rio Grande ABIAU Ables Cheese Stores 37295 5th Ave/PO Box 311 Sardis ABLCH Able Pest Control PO Box 1304 Springfield ABLPE Ace Auction Barn Rt 3 Montpelier ACEAU Ace Fireworks Mfg Co Box 221 Conneaut ACEFI Ace Outdoor Adv 137 South Cassingham RoadBexley ACEOU Simon Ackerman PO Box 75109 Cincinnati ACKSI Acme Salvage & Wrecking Co 2275 Smead Ave Toledo ACMSA The Bissman Co. 193 N Main St, PO Box 1628Mansfield ACMSI A C Positive Box 125 Berlin ACPOS Ad America Inc 647 W Virginia 312 Milwaukee ADAME Ada Motel Inc 768 N Main St Ada ADAMO Adams Outdoor Adv 3801 Capital City Blvd Lansing ADAOU Adco Empire 1822 E Main Columbus ADCEM Adkins Speed Center Rt 1 Box 22 Port Washington ADKSP John Cleveland 8249 Big Run Rd Gambier ADVCH Advent Construction Inc Box 442 Greenville ADVCO Advent Drilling PO Box 2562 N Canton ADVDR Advergate Inc 30415 Hilliard Blvd Westlake ADVIN Advan Outdoor Inc PO Box 402 Sutersville ADVOU Advance Sign Co 900 Sunnyside Rd Vermilion ADVSI The A G Birrell Co Public Square Kinsman AGBIR AG Credit Aca 610 W Lytle St Fostoria AGCRE Harold L Agee 1215 First St Middletown AGEHA Agnes Carnes 37467 SR 30 Lisbon AGNCA Agri-Leaders Assoc 1318 W McPherson Hwy Clyde AGRLE Agri Supply Co Inc 12015 SR 65 Rt 3 Ottawa -

Calls (This Was Old Days) Were to Secretaries/Pas Of

Excellence. NO EXCUSES! 68 Ways to Launch Your Journey. NOW. Tom Peters 27 March 2014 1 To John Hetrick Inventor of the auto air bag, 1952 2 This plea for Excellence is a product of Twitter, where I hang out. A lot. Usually, my practice is a comment here and a comment there—driven by ire or whimsy or something I’ve read or observed. But a while back—and for a while—I adopted the habit of going off on a subject for a semi-extended period of time. Many rejoinders and amendments and (oft brilliant) extensions were added by colleagues from all over the globe. So far, some 68 “tweetstreams” (or their equivalent from some related environments) have passed (my) muster—and are included herein. There is a lot of bold type and a lot of RED ink and a lot of (red) exclamation marks (!) in what follows. First, because I believe this is important stuff. And second, because I am certain there are no excuses for not cherrypicking one or two items for your T.T.D.N. list. (Things To Do NOW.) Excellence. No Excuses. Now. 3 Epigraph: The ACCELERATING Rate of Change “The greatest shortcoming of the human race is our inability to understand the exponential function.”—Albert A. Bartlett* *from Erik Brynjolfsson and Andrew McAfee, The Second Machine Age, “Moore’s Law and the Second Half of the Chessboard”/“Change” is not the issue—change has always been with us. But “this time” may truly be different. The ACCELERATION of change is unprecedented—hence, the time for requisite action is severely compressed. -

Competition Makes Minority Enrollment Small

(£mmtrttntt iaUu GJamptta Vol. LXXVI NO. 8 The University of Connecticut Friday, September 16,1982 j Competition makes minority enrollment small by Liz Hayes Staff Writer few minorities in the state to because there are so few dents to UConn. "It's our goal place more restrictions on to better the situation for the In 1981, the 913 minority begin with, this added com- minority students here to girls than boys. Boys are en- students enrolled at UConn petition makes it more dif- begin with. fall of 1981," Wiggins said. couraged to play football. made up 5.8% of the entire ficult for UConn to enroll the Carol Wiggins, Vice Presi- While the disparity between Girls spend more time study- student body, but state fig- numbers of minorities they dent of Student Affairs and minority and non-minority en- ing and learn to organize their ures show that minorities ac- would like to. Services, said that she was rollment is great, the ratio of time much better." he said. count for 9.9% of Connecticut's Williams said that the main "concerned that there seems male to female students at Vlandis said that he felt total population. reason minorities choose to be such a small percentage UConn is nearly 50:50, accord- those students who knew The reason for this dis- other universities over UConn of minority students at the ing to the 1982-83 University how to organize their time crepancy, according to Larry is because UConn doesn't university. We are very active- of Connecticut Bulletin. well were able to get higher Williams, Assistant Direc tor of offer the financial aid and ly trying to do something The Bulletin's registration grades than those students Admissions at UConn. -

Entered 07/24/15 17:02:16 Page 1 of 54

Case 15-03005-sgj Doc 21 Filed 07/24/15 Entered 07/24/15 17:02:16 Page 1 of 54 U.S. BANKRUPTCY COURT NORTHERN DISTRICT OF TEXAS ENTERED TAWANA C. MARSHALL, CLERK THE DATE OF ENTRY IS ON THE COURT'S DOCKET The following constitutes the ruling of the court and has the force and effect therein described. Signed July 24, 2015 ______________________________________________________________________ IN THE UNITED STATES BANKRUPTCY COURT FOR THE NORTHERN DISTRICT OF TEXAS DALLAS DIVISION IN RE: § § ALCO STORES, INC., § CASE NO. 14-34941-SGJ-11 Debtor. § (Chapter 11) _____________________________________________________________________________ BLACKHAWK NETWORK, INC., and § BLACKHAWK NETWORK § CALIFORNIA, INC., § Plaintiffs, § v. § ADVERSARY NO. 15-03005 § ALCO STORES, INC., § Defendant. § MEMORANDUM OPINION AND ORDER GRANTING DEBTOR-DEFENDANT’S MOTION FOR SUMMARY JUDGMENT [DE # 6] 1 Case 15-03005-sgj Doc 21 Filed 07/24/15 Entered 07/24/15 17:02:16 Page 2 of 54 I. INTRODUCTION “Just as medieval alchemists bent all their energies to discovering a formula that would transmute dross into gold, so too do modern creditors’ lawyers spend prodigious amounts of time and effort seeking to convert their clients’ general, unsecured claims against a bankruptcy debtor into something more substantial.”1 The above words, penned by Judge Carolyn King more than twenty years ago, seem fitting today in the above-referenced adversary proceeding (the “Adversary Proceeding”). The subject of this Adversary Proceeding is stored value cards (“SVCs”) that can be purchased -

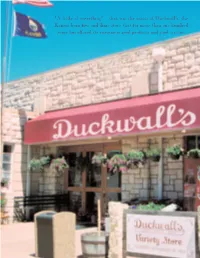

That Was the Motto of Duckwall's, the Kansas-Born Five and Dime Store That for More Than One Hundred Years Has Offered Its Customers Good Products and Good Service

"A little of everything"—that was the motto of Duckwall's, the Kansas-born five and dime store that for more than one hundred years has offered its customers good products and good service. Come Back to the Five & Dime by David A. Haury or more than a century many Kansans enjoyed the convenience, and for the younger family members excitement, of shopping in the local five and dime store. This was the place to find inexpensive household items, Fbuy a discount bag of candy, relax at the soda fountain with a cherry coke, or, in the case of this author, select the best plastic models to assemble. Duckwall’s variety store in Cottonwood Falls. The earliest Duckwall’s began in 1901 in Abilene as a “racket” store, similar to this store (inset) pho- tographed in 1909, probably in Manhattan. All photographs courtesy Duckwall-ALCO Stores, Inc. KANSAS HERITAGE: WINTER 2004 Some younger Kansans may have missed this pleasure as Abilene, and for about four hundred dollars purchased and during the last quarter of the twentieth century many began managing a “racket” store. Racket stores might best downtown five and dime stores have closed and been re- be described as discount variety stores with a focus on the placed with larger discount stores, usually on the outskirts smaller and less expensive items used to furnish a home. of town. The home-grown Duckwall’s (and later ALCO) Its name originated from the tin peddler carts of old, chain, based in Abilene, fortunately has been with us now whose pots and pans clanged and rattled on their hooks, for more than a hundred years, and during that time it has creating a great racket as they were pushed through the streets. -

Cowen Research Themes

COWEN RESEARCH THEMES EDGE COMPUTING2021 & 5G MOBILITY TECHNOLOGY ESG & ENERGY TRANSITION ROBOTICS & AUTOMATION NEW PARADIGMS IN COMPUTING CONSUMER TRANSFORMATION CANNABIS LIQUID BIOPSY TARGETED THERAPIES CENTRAL NERVOUS SYSTEM ELECTION 2020 U.S. / CHINA COMPETITION & DECOUPLING BIG TECH & GOVERNMENT EQUITY & FAIRNESS COWEN TABLE.COM/THEMES2021 OF CONTENTS COWENCOWEN.COM/THEMES2021RESEARCH FROM COWEN DIRECTOR OF RESEARCH ROBERT FAGIN COVID-19 forced a year of “creative destruction,” wherein businesses rushed to challenge conventional models and adapt to new norms. In many cases, such as with e-commerce and telehealth, a multi-year march toward adoption was dramatically accelerated by a stay-at-home and work-from-home environment. Simultaneously, a politically and socially charged atmosphere, including a contentious U.S. election and deepening geopolitical rifts such as United States- China relations, further increased market tension and uncertainty. Remarkably, despite this backdrop of general unease and disorder, extraordinary innovation persisted in areas as diverse as targeted medical therapies, edge computing, 5G, robotics and automation, electrified transportation, and the adoption of clean energy. In this Handbook, we once again feature themes where Cowen’s domain expertise has been central to the discussion and debate. In nearly all cases, Cowen Research EDGE COMPUTING & 5G PAGE 4 | VIDEO PODCAST offered its hallmark collaborative approach to help inform our viewpoints, working MOBILITY TECHNOLOGY PAGE 10 | VIDEO PODCAST across sector teams to provide valuable perspective, and incorporating the views of our Washington Research Group in a rapidly shifting political environment. Each ESG & ENERGY TRANSITION PAGE 16 | VIDEO PODCAST theme highlighted is accompanied by a listing of relevant Cowen reports and events, which we hope supports deeper engagement on these pivotal issues. -

Discount Stores & Specialty Retailers

2013 Profile & Analysis: Discount Stores & Specialty Retailers® TABLE OF CONTENTS INTRODUCTION Executive Summary ......................................................................................................2 Details & Definitions .....................................................................................................9 Explanation of Data Elements ..................................................................................... 11 Statistical Analysis of Contents ...................................................................................14 Indexes of Leading Companies ...................................................................................33 Major Mergers & Acquisitions ......................................................................................41 Major Trade Associations ............................................................................................42 Calendar of Major Trade Shows ..................................................................................51 Exclusions Index .........................................................................................................56 WARNING: It has come to the attention of Chain Store Guides, LLC that subscribers to som e of its publications have, on occasion, used these publications to compile mailing lists, marketing aids, and/or other types of data, which are sold or otherwise provided to third parties. Such use may be illegal and a violation of the federal copyright laws. Chain Store Guides, LLC intends to exercise -

Welcome to the City of Horton, KS

Welcome to the City of Horton, KS New Resident & Visitors Guide ___________________________________________________________________________________________ City of Horton 205 E. 8th St. PO Box 30 785.486.2681 Horton KS 66439-0030 fax 785.486.2381 Horton's History Horton was founded in 1886 and named after Albert H. Horton, chief of justice of the Supreme Court. By 1887 Horton was incorporated as a third class city by the district judge. Horton is an agricultural community located in northeast Kansas, on the south central edge of Brown County, at what is known as the "Junction" of the Chicago, Kansas, and Nebraska Railroad. Elevation is 1,134 feet above sea level. Population zoomed to approximately 4,000 shortly after the town was started, reached its peak in 1923 (5,012) and is now down to about 1,700 with the closing of the Rock Island Shops. A poster that was issued in 1886 to advertise the town of Horton, soon after it was laid out and the first lots sold, was headed "The Prodigy of the West- the Wonder of Kansas". It contained a great deal of information about the "Magic City", as Horton was called. It exploited the town as the best place for capitalists to make money. Pioneers who settled in this area before Horton was founded have infiltrated into the families of railroad workers who flocked to the "Magic City" to work for the Rock Island, leaving a heritage of ancestors of which we can be proud. Hotels: At one point there were 900 employees at the Rock Island Shops and 13 hotels! The Hotel Windsor was the first commercial hotel built in town in 1887-1888. -

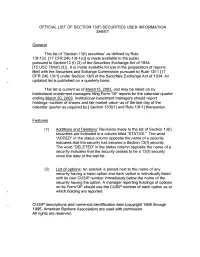

List of Section 13F Securities, First Quarter 2003

OFFICIAL LIST OF SECTION 13(F) SECURITIES USER INFORMATION SHEET General This list of "Section 13(f) securities" as defined by Rule 13f-I (c) [17 CFR 240.13f-l(c)] is made available to the public pursuant to Section13 (f) (3) of the Securities Exchange Act of 1934 [I5 USC 78m(f) (3)]. It is made available for use in the preparation of reports filed with the Securities and Exhange Commission pursuant to Rule 13f-1 [17 CFR 240.1 3f-11 under Section 13(f) of the Securities Exchange Act of 1934. An updated list is published on a quarterly basis. This list is current as of Marchl5, 2003, and may be relied on by institutional investment managers filing Form 13F reports for the calendar quarter ending March 30, 2003. Institutional investment managers should report holdings--number of shares and fair market value--as of the last day of the calendar quarter as required by [ Section 13(f)(l) and Rule 13f-I] thereunder. Features (1) Additions and Deletions: Revisions made to the list of Section 13(f) securities are indicated in a column titled "STATUS." The word "ADDED" in the status column opposite the name of a security indicates that the security has become a Section 13(f) security. The word "DELETED" in the status column opposite the name of a security indicates that the security ceases to be a 13(f) security since the date of the last list. (2) List of options: An asterisk is placed next to the name of any security having a listed option and each option is individually listed with its own CUSlP number immediately below the name of the security having the option.